Portfolio Loan Lenders: Benefits, Rates, And Requirements

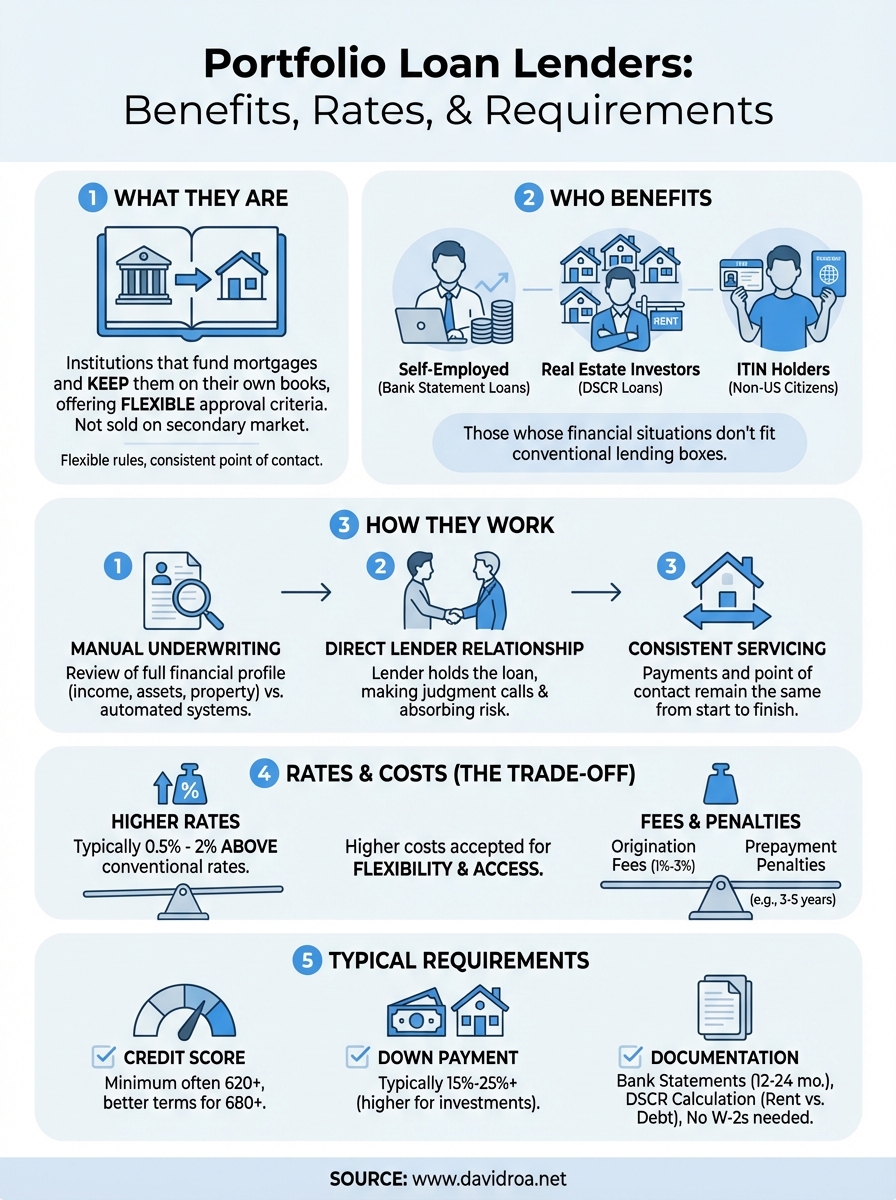

Not every borrower fits neatly into the box that conventional lenders require. Self-employed professionals, real estate investors, and ITIN holders often get turned away by banks that sell their loans on the secondary market and can't flex their guidelines. That's where portfolio loan lenders come in, financial institutions that fund mortgages and keep them on their own books, giving them the freedom to set their own approval criteria.

After more than 25 years in the lending industry and over $150 million funded, I've helped hundreds of borrowers secure financing through portfolio loan programs when traditional options fell short. At David Roa, we work directly with portfolio lenders who specialize in scenarios that conventional underwriting overlooks, from DSCR investor loans to non-QM products built for real-world financial situations.

This article breaks down how portfolio loans work, what rates and requirements to expect, and how to determine whether this lending path makes sense for your situation.

Why portfolio loan lenders matter

The conventional mortgage market runs on a strict set of rules because lenders who originate loans typically sell them to Fannie Mae, Freddie Mac, or private investors on the secondary market. Those buyers set the guidelines, and lenders must follow them precisely. When your income is irregular, your credit history is thin, or your property doesn't fit standard criteria, that system works against you. Portfolio loan lenders break that cycle by holding loans in-house instead of selling them off.

The conventional lending gap

Conventional underwriting was built around W-2 employees with two years of stable employment history and a straightforward debt-to-income ratio. That model leaves out a significant portion of today's borrowers. Self-employed business owners, real estate investors with multiple properties, and ITIN holders all fall outside the parameters that Fannie Mae and Freddie Mac set for conforming loans.

When a bank sells your loan on the secondary market, it's no longer your lender. The investor who bought that loan is. Portfolio lenders stay your lender from day one through payoff.

The gap creates real consequences for real transactions. A real estate investor with strong cash flow from rental properties but limited W-2 income gets rejected by a conventional lender even when the numbers clearly support the loan. A self-employed borrower who writes off significant business expenses might show a low adjusted gross income on paper despite running a profitable operation. Portfolio lenders evaluate the full financial picture rather than just the single tax return line that conforming underwriting requires.

Who actually benefits from portfolio lending

Borrowers who gain the most from working with portfolio loan lenders fall into a few clear categories. Property investors who qualify through DSCR metrics, non-U.S. citizens using an ITIN, borrowers who have experienced a recent credit event like a short sale, and professionals with layered income structures all benefit significantly. These are not edge cases. They represent a large and growing segment of borrowers who have the genuine ability to repay but don't match a conventional template.

Your ability to qualify isn't only about creditworthiness. It's about whether the lender's guidelines match your actual financial reality. Portfolio lenders write their own rules, which means they can structure a loan around your situation rather than forcing you into a category that doesn't fit.

How portfolio loan lenders work

Portfolio loan lenders fund mortgages using their own capital, which means they set their own underwriting standards and service the loan themselves for its full term. You deal with the same institution from application through payoff. Because there is no secondary market buyer dictating the terms, the lender has genuine flexibility to evaluate your income, assets, and property type in a way that reflects real-world financial situations.

The underwriting process

Portfolio lenders typically assign an underwriter who reviews your full financial profile rather than running your application through an automated system built for conforming loans. They weigh factors like bank statement deposits, rental income from investment properties, or business cash flow instead of relying solely on tax returns. This manual review process takes longer, but it also allows the lender to make judgment calls that a conventional approval engine never could.

The lender's willingness to hold the loan gives them a direct stake in your ability to repay, which shapes how they evaluate risk from the start.

Common documentation for portfolio underwriting includes 12 to 24 months of bank statements, a current rent roll for investment properties, or a DSCR calculation that measures the property's income against the proposed debt payment.

Loan servicing and your relationship with the lender

Because the lender keeps the loan, your monthly payment and point of contact stay consistent. You are not transferred to a third-party servicer six months after closing. That continuity matters when you need to modify terms, refinance into a new product, or ask questions about your account. You know who to call and they know your file.

Portfolio loan rates, fees, and penalties

Portfolio loans cost more than conventional loans, and that's the trade-off you accept in exchange for flexible underwriting. Interest rates on portfolio loan programs typically run 0.5 to 2 percentage points above conforming loan rates, depending on your credit profile, loan size, and the lender's risk assessment. That spread reflects the fact that the lender absorbs the full risk of your loan rather than offloading it to a secondary market buyer.

Interest rates and why they're higher

When you work with portfolio loan lenders, the rate reflects the lender's direct exposure to your loan over its full term. Your specific rate depends on factors like your credit score, loan-to-value ratio, and property type. A borrower with a 720 credit score putting 25 percent down will see a materially better rate than someone at 650 with minimal equity.

Rates on DSCR investor loans and bank statement programs sit at the higher end of the portfolio rate range because of the additional flexibility those products offer. You can often negotiate a lower rate by bringing a larger down payment or accepting a shorter fixed period on an adjustable-rate structure.

The rate premium is worth examining carefully before you assume a portfolio loan is too expensive for your goals.

Fees and prepayment penalties

Origination fees on portfolio loans typically range from 1 to 3 percent of the loan amount, which runs higher than conventional products. Some lenders also add prepayment penalty clauses, charging you if you pay off or refinance within a set period, often three to five years. Review that structure before signing because it directly affects your exit plan.

- Origination fee: 1 to 3 percent of the loan amount

- Underwriting fee: $500 to $1,500

- Prepayment penalty: typically 1 to 3 percent of the remaining balance if triggered early

Requirements and who a portfolio loan fits

Portfolio loan lenders set their own qualification standards, so requirements vary more than they do with conventional products. That said, most lenders share a common baseline. You will generally need a minimum credit score of 620, though stronger borrowers at 680 and above unlock better pricing. Down payment requirements typically start at 15 to 25 percent, depending on the property type and program. Investment properties usually require more equity than primary residences.

Core qualification benchmarks

Your income documentation depends on which portfolio product you apply for. Bank statement loans require 12 to 24 months of personal or business statements to establish average monthly deposits. DSCR loans skip personal income entirely and qualify you based on whether the property's rental income covers the proposed debt payment, usually requiring a ratio of 1.0 or higher. Both approaches give you a legitimate path to approval without W-2s or full tax return analysis.

The right documentation strategy depends on your specific income structure, so identify which program matches your financial profile before you apply.

Borrower profiles that fit best

Some borrowers consistently get better results with portfolio programs than they ever would through conventional channels. Self-employed professionals who write off significant business expenses benefit because portfolio lenders look at actual cash flow rather than adjusted gross income. Real estate investors with multiple financed properties benefit because DSCR underwriting removes the debt-to-income barrier that conventional guidelines impose. Foreign nationals and ITIN holders also fit well since many portfolio lenders build programs specifically for borrowers without a Social Security number or U.S. credit history.

How to find and compare portfolio loan lenders

Finding the right lender takes more than a quick search. Portfolio loan lenders range from small community banks to specialty non-QM lenders, and many don't advertise their programs publicly. Your fastest route is working with a mortgage broker who holds active relationships with multiple portfolio lenders, since they can match your specific scenario to the right program without you contacting each lender one by one.

Where to look

Your strongest starting point is a non-QM specialty broker rather than a retail bank branch. Community banks and credit unions also hold loans in-house but rarely promote those products, so a direct call can open options you wouldn't find online. Focus on lenders who specifically build programs around DSCR loans, bank statement income, or ITIN borrowers, since those lenders already understand the borrower profiles that conventional underwriting rejects.

A broker with current non-QM lender relationships will get you accurate guidelines and pricing faster than researching lenders on your own.

What to compare before you commit

Once you have two or three options in front of you, review rates, origination fees, and prepayment penalty terms together rather than evaluating each factor in isolation. A lower rate paired with a five-year prepayment penalty can cost you more than a slightly higher rate with no exit restriction if you plan to sell or refinance early. Request a Loan Estimate from each lender so you compare standardized figures across the same loan scenario.

Key points to evaluate side by side:

- Rate and APR

- Origination and underwriting fees

- Prepayment penalty length and percentage triggered

- Minimum down payment for your specific property type

Final take

Portfolio loan lenders give you a real path to financing when conventional underwriting closes the door. If your income is self-employed, your properties generate strong rental revenue, or you hold an ITIN instead of a Social Security number, a portfolio program evaluates your actual financial picture rather than a rigid template built for someone else's situation.

The trade-off is straightforward. You pay higher rates and fees in exchange for flexible qualification standards and a lender who stays accountable to you throughout the loan term. That cost is often worth it when the alternative is no loan at all.

Before you apply, get clear on your income documentation, target down payment, and exit timeline so you can compare lenders on the factors that actually matter for your deal. If you want guidance from a lender who works with these programs daily, connect with David Roa to review your options.