Prequalify For FHA Mortgage Online: Steps And Requirements

Getting a clear answer on whether you qualify for a home loan shouldn't require a dozen phone calls and a stack of paperwork. When you prequalify for FHA mortgage financing online, you get a realistic picture of your buying power, often within minutes, so you can shop for homes with confidence instead of guesswork.

FHA loans remain one of the most accessible paths to homeownership, especially if your credit score isn't perfect or you don't have a large down payment saved up. But the eligibility requirements can be confusing, and not every lender handles them the same way. With over 25 years in mortgage lending and more than $150 million funded, I've walked thousands of borrowers through this exact process, from first-time buyers to clients using FHA financing with ITIN numbers who thought homeownership was out of reach.

This guide breaks down the specific steps, credit and income requirements, and what to expect when you prequalify for an FHA mortgage online. Whether you're buying your first home or exploring your options after a financial setback, you'll have a clear roadmap by the end of this article, and you'll know exactly what lenders are looking for before you apply.

FHA prequalification basics and eligibility

Prequalification is not the same as approval, but it's the most important first step you can take before making an offer on a home. When you prequalify for an FHA mortgage, a lender reviews your self-reported financial information and gives you an estimate of how much you could borrow under FHA guidelines. It takes no hard credit pull, no commitment, and no application fee, so there's no reason to skip this step.

What prequalification actually means

Prequalification gives you a fast snapshot of where you stand financially before you invest serious time into the homebuying process. You provide basic details about your income, assets, and credit score range, and the lender runs those numbers against FHA guidelines to tell you whether you're likely eligible and for how much. Think of it as a practice run before the formal preapproval process, which involves verified documents and a hard credit inquiry.

Prequalification does not guarantee a loan, but it gives you a realistic target range so you can shop with confidence instead of wasting time on homes that are outside your budget.

This step also helps you catch problems early. If your debt-to-income ratio is too high or your credit score falls below the minimum threshold, you find out now rather than after you've already made an offer on a home.

Core FHA eligibility requirements

FHA loans are insured by the Federal Housing Administration, which means lenders take on less risk and can approve borrowers with lower scores and smaller down payments than conventional loans typically allow. Below are the key benchmarks you need to meet:

| Requirement | Minimum Standard |

|---|---|

| Credit Score | 580+ for 3.5% down; 500-579 for 10% down |

| Down Payment | 3.5% of the purchase price (with 580+ score) |

| Debt-to-Income Ratio | 43% standard max; some lenders allow up to 50% |

| Employment History | 2 years of steady income or employment history |

| Property Type | Primary residence only |

| Mortgage Insurance | 1.75% upfront MIP plus an annual premium |

Your citizenship or documentation status does not automatically disqualify you either. ITIN holders who are non-U.S. citizens can qualify for FHA financing through specific lenders, which opens the door for a large group of borrowers that conventional banks routinely turn away.

How FHA compares to conventional financing

Conventional loans reward high credit scores and larger down payments with lower rates and no mortgage insurance once you reach 20% equity. FHA loans are designed for borrowers who are still building their financial profile and cannot meet those thresholds. The trade-off is mortgage insurance premiums (MIP) that stay on the loan for its full term in most cases, unless you refinance into a conventional product once your equity position improves.

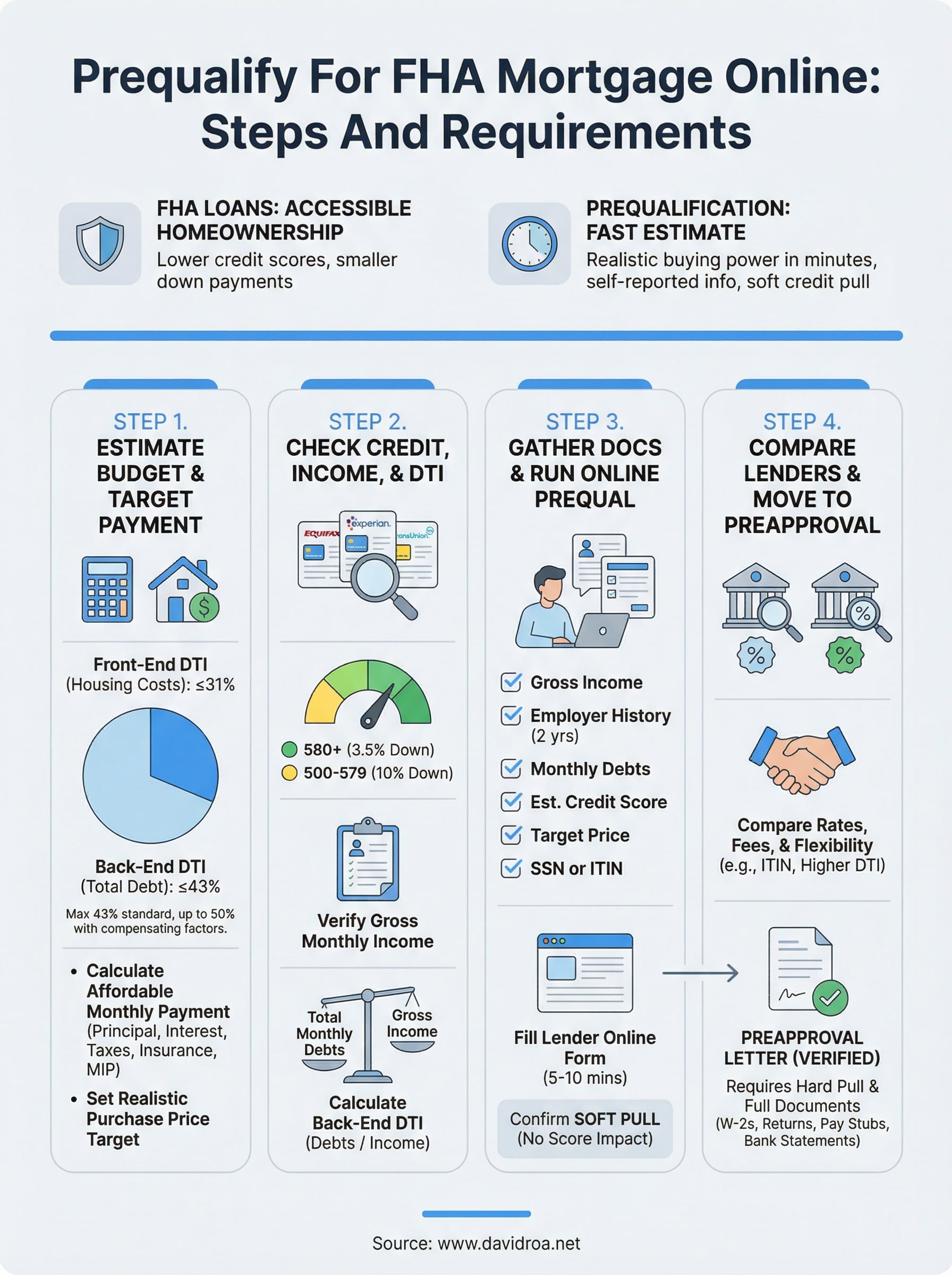

Step 1. Estimate your budget and target payment

Before you prequalify for FHA mortgage financing, you need a realistic number in mind, not just "as much as possible." Lenders look at your debt-to-income ratio first, which means your monthly home payment has to fit inside a specific percentage of your gross monthly income. Knowing your target payment before you talk to a lender puts you in a much stronger position during that conversation.

Calculate what you can afford

Your front-end DTI ratio (housing costs only) should stay at or below 31% of your gross monthly income under standard FHA guidelines, though some lenders allow up to 40%. Your back-end DTI (all monthly debts combined) should not exceed 43%, though certain lenders approve up to 50% with compensating factors. Here is a quick reference to estimate your affordable payment range:

| Gross Monthly Income | 31% Front-End Max | 43% Back-End Max |

|---|---|---|

| $4,000 | $1,240 | $1,720 |

| $5,500 | $1,705 | $2,365 |

| $7,000 | $2,170 | $3,010 |

| $9,000 | $2,790 | $3,870 |

Subtract your existing monthly debt payments from the back-end maximum first. Whatever is left tells you the actual room you have for a mortgage payment, not the full column number.

Set a realistic purchase price target

Once you know your maximum monthly payment, work backward to a purchase price. At a 6.5% interest rate on a 30-year FHA loan, every $100,000 borrowed costs roughly $632 per month in principal and interest alone. Add property taxes, homeowner's insurance, and the FHA annual MIP (approximately 0.55% of the loan balance per year), and your total payment runs noticeably higher than just principal and interest.

For a $250,000 loan, budget roughly $1,700 to $1,900 per month total, depending on your local tax rate. Locking in this number before you start browsing listings keeps you focused on homes that will actually close.

Step 2. Check your credit, income, and DTI

Before you prequalify for FHA mortgage financing with any lender, you need to know exactly where your numbers stand. Running your own check first means no surprises during the lender conversation and gives you time to fix issues before they cost you a better rate or a denial.

Pull your credit report and score

You can pull your credit report for free at AnnualCreditReport.com, which is the only federally authorized source. Review all three bureaus, Equifax, Experian, and TransUnion, because FHA lenders use your middle score from all three when making a decision. Look for any late payments, collection accounts, or errors that might be dragging your score below the 580 threshold. Dispute factual errors directly through each bureau's website before you submit any loan application.

Even one disputed collection account removed from your report can move your score 20 to 40 points, which may be the difference between a 3.5% and a 10% down payment requirement.

Verify your income and calculate your DTI

Lenders calculate your debt-to-income ratio using your gross monthly income, not take-home pay. Add up all fixed monthly debt obligations, including car payments, student loans, minimum credit card payments, and any existing mortgage or rent payments. Then divide that total by your gross monthly income. Use this template to run the math before you call a lender:

| Item | Your Number |

|---|---|

| Gross Monthly Income | $________ |

| Monthly Debt Payments | $________ |

| Back-End DTI (Debts / Income) | ________% |

| Max FHA Back-End DTI Allowed | 43% (up to 50% with compensating factors) |

| Available Room for Mortgage | $________ |

If your back-end DTI exceeds 43%, pay down a small revolving balance or eliminate a loan before applying. That one adjustment can shift your eligibility significantly without requiring a higher income.

Step 3. Gather documents and run online prequal

Having your documents ready before you prequalify for FHA mortgage financing online cuts the process from 30 minutes to under 10. Most online prequalification tools ask the same core questions, so pulling your information together in one place first means you answer accurately instead of guessing at numbers.

Documents you need on hand

You do not need to upload anything during prequalification, but you do need accurate numbers in front of you to fill in the form correctly. Lenders verify everything during the full preapproval phase, so your goal here is accuracy, not perfection. Keep these items open before you start:

- Gross monthly income: Pull from a recent pay stub or tax return, not your take-home amount

- Employer name and start date: Two-year employment history is required

- Monthly debt obligations: Car loans, student loans, and credit card minimums

- Estimated credit score range: Use the number from your Step 2 check

- Target purchase price: Use the budget you set in Step 1

- Social Security Number or ITIN: Required to complete any prequalification form

If you are a non-U.S. citizen with an ITIN, confirm with the lender upfront that they offer ITIN-based FHA financing, because standard prequalification forms do not always present that as a visible option.

How to run the online prequalification

Go directly to a lender's website and locate their prequalification or "get started" form. Fill in each field using the verified numbers you gathered above. Most forms take 5 to 10 minutes and return an estimated loan amount instantly.

Before you submit, confirm whether the form runs a soft pull (no credit score impact) or a hard inquiry. Prequalification should never require a hard pull. If a lender insists on one at this stage, move to a different lender.

Step 4. Compare lenders and move to preapproval

Once you prequalify for FHA mortgage financing with one lender, do not stop there. Running the same basic prequalification with two or three lenders costs you nothing and gives you real data to compare, because FHA interest rates, lender fees, and underwriting flexibility vary more than most borrowers expect. The difference of even 0.25% on your rate translates to thousands of dollars over the life of a 30-year loan, so treating the first result as the final result is a costly habit.

What to compare across lenders

Not every lender handles FHA loans the same way. Some specialize in non-standard borrower profiles, such as ITIN holders or self-employed applicants, while others follow rigid guidelines that reject those scenarios outright. Use this comparison template when you speak with each lender:

| Factor | What to Ask |

|---|---|

| Interest Rate | What is your current FHA 30-year fixed rate? |

| Lender Fees | What origination and processing fees do you charge? |

| DTI Flexibility | Do you approve back-end DTI above 43%? |

| ITIN Acceptance | Do you offer FHA loans for non-U.S. citizens? |

| Closing Timeline | How long does your full preapproval take? |

| Loan Officer Access | Will I have one dedicated point of contact? |

How to move from prequalification to preapproval

Preapproval carries real weight with sellers because it involves verified documents and a hard credit pull, not just self-reported numbers. Once you have selected your lender, gather this full package before you make the call to avoid delays:

- W-2s or 1099s from the past two years

- Federal tax returns for the same two-year period

- Pay stubs from the last 30 days

- Bank statements covering the past two to three months

- Photo ID plus your Social Security Number or ITIN

A preapproval letter locks in your estimated loan amount and signals to sellers that you are a serious, qualified buyer ready to move quickly.

Submit everything at once rather than piece by piece. Incomplete files slow the underwriting process and can delay your closing timeline significantly.

Wrap-up and what to do now

When you prequalify for FHA mortgage financing, you are not just checking a box. You are gathering real data about your financial position so you can make a smarter, faster move when the right home appears. The four steps in this guide follow a specific order for a reason: budget first, credit second, documents third, lender comparison fourth. Skipping ahead costs you time and accuracy.

Your next move is simple. Pull your credit report today, run the DTI math from Step 2, and collect the document list from Step 3 before you contact a single lender. That preparation separates borrowers who close on time from those who scramble at the last minute. If your scenario involves an ITIN, a self-employment income structure, or a credit score that conventional lenders reject, working with an experienced FHA specialist matters far more than using the nearest bank. Connect with David Roa to start your FHA prequalification and get answers from a lender who has seen every borrower profile.