How To Refinance FHA Loan To Conventional: Step-By-Step

If you're still paying mortgage insurance on your FHA loan even though your home equity has grown, you're likely leaving money on the table every month. The decision to refinance FHA loan to conventional can eliminate that ongoing MIP cost, potentially lower your interest rate, and give you more flexibility with your mortgage terms. But knowing when you qualify, and how to navigate the process, makes all the difference between a smooth refinance and a frustrating one.

At David Roa, we've helped homeowners across the country work through exactly this transition. With over 25 years in mortgage lending and more than $150 million funded, we've guided countless borrowers from FHA loans into conventional financing at the right time and on the right terms. We understand the specific requirements, the common roadblocks, and the strategies that save you the most money.

This guide breaks down every step of the FHA-to-conventional refinance process. You'll learn the eligibility requirements you need to meet, how to prepare your application, and how to decide whether refinancing actually makes financial sense for your situation. We'll also cover the costs involved so there are no surprises at the closing table.

Know if switching makes sense for you

Not every FHA borrower should rush to refinance FHA loan to conventional. The move makes strong financial sense in specific situations, and it can actually cost you more if you switch at the wrong time. Before you pull together documents or call a lender, spend time understanding what you stand to gain and what the break-even point looks like for your specific numbers.

When MIP removal is the main driver

FHA loans require two types of mortgage insurance: an upfront MIP of 1.75% of the loan amount, and an annual MIP that you pay monthly. For most FHA loans originated after June 2013, that annual MIP stays for the life of the loan, regardless of how much equity you build. That's the key difference from conventional loans, where private mortgage insurance drops off automatically once you reach 20% equity.

If your FHA loan was originated after June 3, 2013, you will pay MIP for the entire loan term unless you refinance out of FHA entirely.

If your home has appreciated or you've paid down enough principal to reach at least 20% equity, switching to conventional removes the mortgage insurance requirement immediately. On a $300,000 loan balance with a monthly MIP of 0.85%, that's roughly $212 per month you stop paying. Over five years, that adds up to more than $12,700 in savings before factoring in any rate difference.

When a lower interest rate strengthens the case

Sometimes the rate environment shifts in your favor, or your credit score has improved significantly since you originally took out the FHA loan. Conventional loans reward stronger credit profiles with better pricing. If your score has moved from 640 to 720 or higher, you may now qualify for a conventional rate that beats your current FHA rate.

Use this framework to estimate whether the rate difference justifies refinancing:

| Loan Scenario | Est. Monthly Payment | Monthly Savings vs. FHA |

|---|---|---|

| $300K balance, 7.5% FHA rate + MIP | ~$2,312 | Baseline |

| $300K balance, 7.0% conventional, no PMI | ~$1,996 | ~$316 |

| $300K balance, 6.75% conventional, no PMI | ~$1,945 | ~$367 |

Once you know your estimated monthly savings, divide your total closing costs (typically 2% to 5% of the loan balance) by that number to find your break-even point in months. For example, if closing costs run $6,000 and you save $300 per month, you break even in 20 months. If you plan to stay in the home longer than that, the refinance pays for itself.

When switching may not be worth it

Refinancing has real costs, and a few situations make the math unfavorable. Knowing these upfront saves you time and a hard credit inquiry:

- Equity below 20%: You'll trade FHA MIP for conventional PMI, which may not produce meaningful savings.

- Close to loan payoff: Resetting the loan term adds more total interest than the MIP savings offset.

- Credit score below 620: Conventional lenders will either decline the application or price the loan at a rate that erases the benefit.

- Recent appraisal issues: If your home value has dropped, you may not have enough equity to qualify for conventional underwriting standards.

Run your own numbers against each of these scenarios before moving forward. A clear financial case, not just a desire to get rid of MIP, should drive your decision to refinance.

Check conventional refinance requirements

Before you can refinance FHA loan to conventional, you need to confirm you actually meet the minimum standards conventional lenders require. These aren't the same as FHA guidelines, and falling short on even one requirement can delay your application or push you toward a higher rate tier. Check each factor below against your current financial profile so you go into the process with a realistic picture.

Credit score and debt-to-income ratio

Conventional loans require a minimum credit score of 620, but that floor only gets you in the door. To qualify for pricing that actually beats your FHA rate and removes mortgage insurance, you want to be in the 680 to 740 range or higher. Below 680, lenders apply loan-level price adjustments that raise your rate and offset much of the benefit.

Your debt-to-income ratio (DTI) also matters. Most conventional lenders want your total monthly debt payments to stay at or below 45% of your gross monthly income, including the new mortgage payment. Some lenders go up to 50% with strong compensating factors like significant reserves, but don't count on that flexibility unless your credit score is above 720.

| Credit Score Range | Typical Rate Tier | PMI Requirement |

|---|---|---|

| 760+ | Best available pricing | Lowest PMI rate |

| 720-759 | Strong pricing | Low PMI rate |

| 680-719 | Standard pricing | Moderate PMI rate |

| 620-679 | Higher rate adjustments | Higher PMI rate |

Equity and loan-to-value ratio

Your loan-to-value ratio (LTV) determines both whether you qualify and whether you pay PMI. You need at least 3% equity (97% LTV) to qualify for a conventional refinance at all, but you need 20% equity (80% LTV) to skip PMI entirely. If you're between those points, the refinance may still benefit you depending on your current MIP rate versus the conventional PMI quote.

Get a current appraisal estimate before applying. Your home's current market value drives the LTV calculation, and values shift more than most borrowers expect.

Loan seasoning requirement

Most conventional lenders require that your FHA loan has been active for at least 12 months before they'll refinance it. You also need a clean 12-month payment history with no 30-day lates. One missed payment in the past year can complicate approval or require you to wait longer before reapplying.

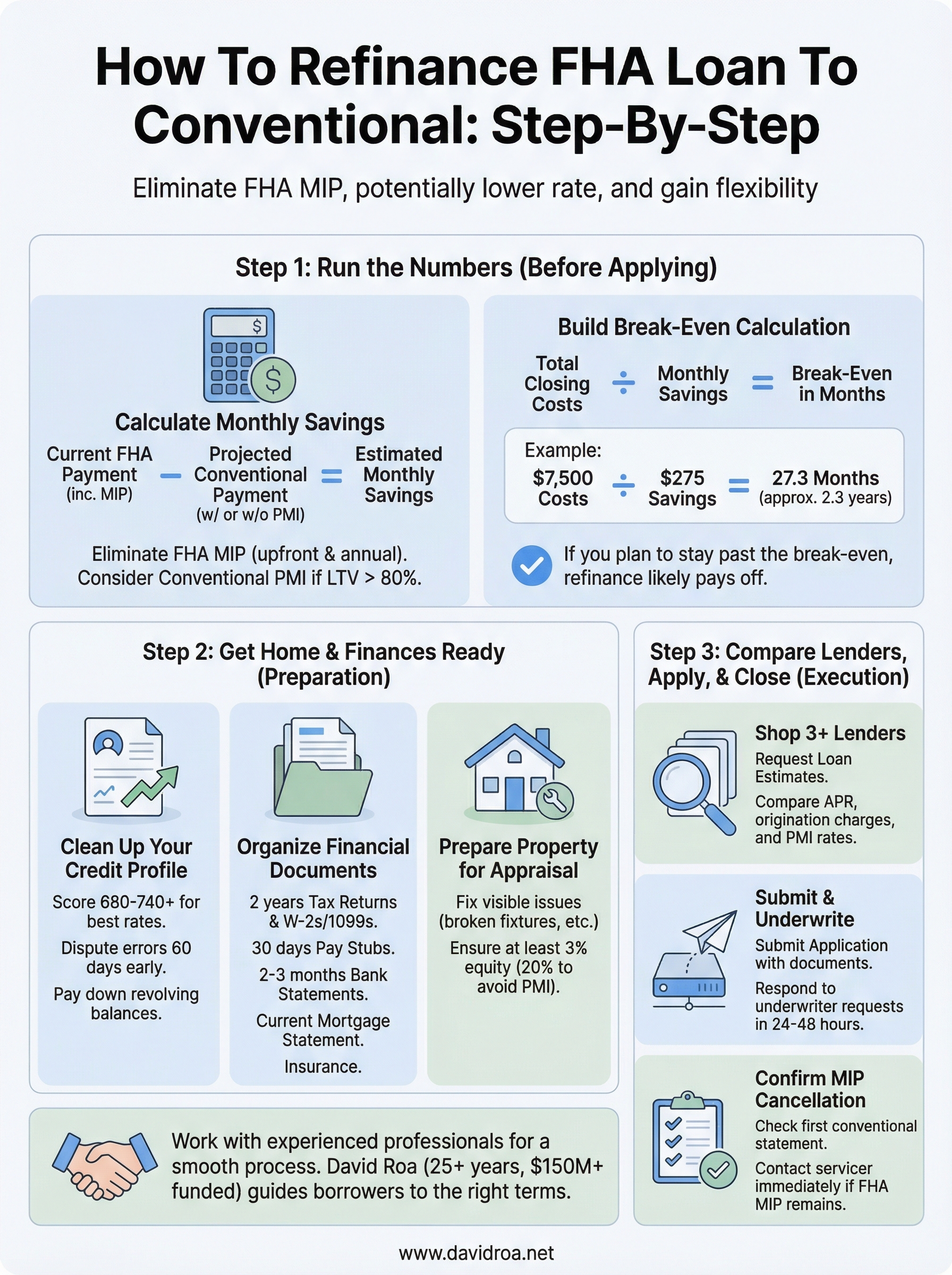

Step 1. Run the numbers before you apply

Running the numbers before you contact a lender saves you time and prevents you from committing to a refinance that doesn't actually benefit your situation. When you decide to refinance FHA loan to conventional, the financial case needs to be specific and clear, not just a rough feeling that you'll save money. Gather your current loan statement and a recent estimate of your home's market value before you do anything else.

Calculate your monthly savings

Your monthly savings come from two sources: eliminating MIP and potentially lowering your interest rate. Start by pulling your current MIP amount from your loan statement. For most FHA loans, it appears as a separate line item on your monthly bill. Then get a conventional rate quote for your loan amount and credit profile, and factor in whether you'll owe PMI based on your current LTV ratio. Subtract your projected conventional payment from your current FHA payment to get your estimated monthly savings.

If your LTV sits above 80%, request a conventional PMI quote anyway. In many cases, conventional PMI costs less per month than FHA's annual MIP, which means the switch still saves you money even without full equity.

Build your break-even calculation

Once you have your monthly savings number, divide your estimated closing costs by it. Closing costs typically run 2% to 5% of your loan balance. Use this formula to find your break-even point:

Break-Even (months) = Total Closing Costs / Monthly Savings

Example:

Closing costs: $7,500

Monthly savings: $275

Break-even: 7,500 / 275 = 27.3 months (about 2.3 years)

If you plan to stay in the home longer than your break-even point, the refinance makes strong financial sense. If you expect to sell or refinance again before that point, the upfront costs will likely outweigh the benefit. Complete this worksheet before you call any lender:

| Input | Your Number |

|---|---|

| Current FHA monthly payment (including MIP) | $ |

| Projected conventional payment (with or without PMI) | $ |

| Monthly savings | $ |

| Estimated closing costs (2-5% of balance) | $ |

| Break-even in months | months |

Step 2. Get your home and finances ready

Once your numbers confirm the refinance makes financial sense, the next step is preparing both your financial profile and your property condition before you formally apply. Lenders will scrutinize your credit, income, and home value during underwriting, and showing up prepared shortens the timeline significantly while reducing the chance of a last-minute denial or pricing surprise.

Clean up your credit profile

Your credit score directly affects the rate you'll receive when you refinance FHA loan to conventional. Pull your free credit report at AnnualCreditReport.com and review it carefully for errors, outdated accounts, or unresolved collections. Dispute any inaccuracies at least 60 days before you apply, since corrections take time to process and update your score.

A single disputed item resolved in your favor can shift your score into a better rate tier, which translates to thousands of dollars saved over the remaining loan term.

Pay down revolving credit balances to below 30% of each card's limit before applying. This adjustment produces faster score improvement than almost any other action you can take in a short window. Avoid opening new credit accounts or carrying large new balances in the 90 days leading up to your application, since both moves reduce your average account age and increase your utilization ratio.

Organize your financial documents

Lenders require specific documentation to verify your income, employment, and assets. Having everything ready before you apply prevents delays once your file moves to underwriting. Gather the items below and store them in one accessible folder:

- Last two years of federal tax returns (all pages and schedules)

- Last two years of W-2s or 1099s

- Most recent 30 days of pay stubs

- Two to three months of bank statements for all accounts

- Current mortgage statement showing your balance and payment history

- Homeowners insurance declarations page

Prepare your property for appraisal

Your home's appraised value sets your LTV ratio, which controls your PMI requirement and rate tier. Walk through the property and address visible maintenance issues such as broken fixtures, water stains, or damaged flooring before the appraiser visits. You don't need a full renovation, but deferred maintenance signals lower value and can pull the appraisal below the threshold you need to qualify.

Step 3. Compare lenders, apply, and close

Once your finances and property are ready, the final phase to refinance FHA loan to conventional comes down to three actions: getting competitive rate quotes, submitting a complete application, and moving efficiently through underwriting to close. Rushing this step or working with the first lender you find typically costs you money. Taking a few extra days to shop the market pays off.

Shop multiple lenders for rate quotes

Contact at least three lenders within a 14-day window. When multiple lenders pull your credit within that period, the credit bureaus count them as a single inquiry for scoring purposes, so shopping around does not hurt your score. Ask each lender for a Loan Estimate, which is the standardized three-page form lenders are required to provide within three business days of receiving your application information.

When comparing Loan Estimates, focus on the APR and total closing costs on page two, not just the interest rate on page one. Those two numbers together tell the real story.

Compare the following items side by side across all quotes:

| Item to Compare | Why It Matters |

|---|---|

| Interest rate and APR | APR reflects the true annual cost including fees |

| Origination charges | Varies significantly between lenders |

| PMI rate (if applicable) | Affects monthly payment if LTV is above 80% |

| Third-party fees | Appraisal, title, and settlement costs |

| Rate lock period | Confirms your rate holds through closing |

Submit your application and move through underwriting

Once you select your lender, submit your full application with all the documents you prepared in Step 2. Respond to every underwriter request within 24 to 48 hours. Delays in providing documentation are the most common reason refinances take longer than expected.

Confirm MIP cancellation after closing

After your new conventional loan closes, verify that your servicer stops collecting the FHA MIP immediately. Check your first conventional loan statement carefully. If you still see a mortgage insurance line item, contact your servicer directly and provide your closing disclosure as proof that the FHA loan was paid off. This step takes only a few minutes but prevents you from overpaying on a fee that should no longer exist.

Next steps for your refinance plan

You now have everything you need to refinance FHA loan to conventional with confidence. The process rewards borrowers who prepare early and understand their numbers before they ever contact a lender. Review your credit score, pull your current loan statement, and run your break-even calculation this week rather than waiting.

Once you confirm the move makes financial sense, gather your documents and start shopping lenders within a focused 14-day window to protect your credit score. The steps in this guide give you a clear path from your first calculation to your closing disclosure, with no guesswork involved.

Working with an experienced mortgage professional speeds up the process and helps you avoid costly mistakes. David Roa brings over 25 years of lending experience and a track record of more than $150 million funded to help you close on the right terms for your situation. Start your conventional refinance with David Roa and get a personalized rate quote today.