Rental Property Cash Flow Calculator: Estimate ROI Fast

Running the numbers on a rental property before you buy separates successful investors from those who end up underwater. A rental property cash flow calculator helps you estimate monthly income, expenses, and returns, so you can make informed decisions, not gut-feeling gambles. Without clear financial projections, you risk overpaying for properties that drain your bank account instead of building wealth.

In this guide, you'll learn exactly how to calculate cash flow, cash-on-cash return, cap rate, and net operating income. We'll walk through each metric step by step and show you how to use these numbers to evaluate whether a deal makes financial sense. By the end, you'll have the tools to analyze any investment property with confidence.

With over 25 years of experience funding real estate investors through DSCR loans, hard money financing, and fix-and-flip capital, I've seen what separates profitable deals from money pits. The difference almost always comes down to running accurate numbers upfront, and pairing those numbers with the right financing structure for your strategy.

What a rental cash flow calculator should include

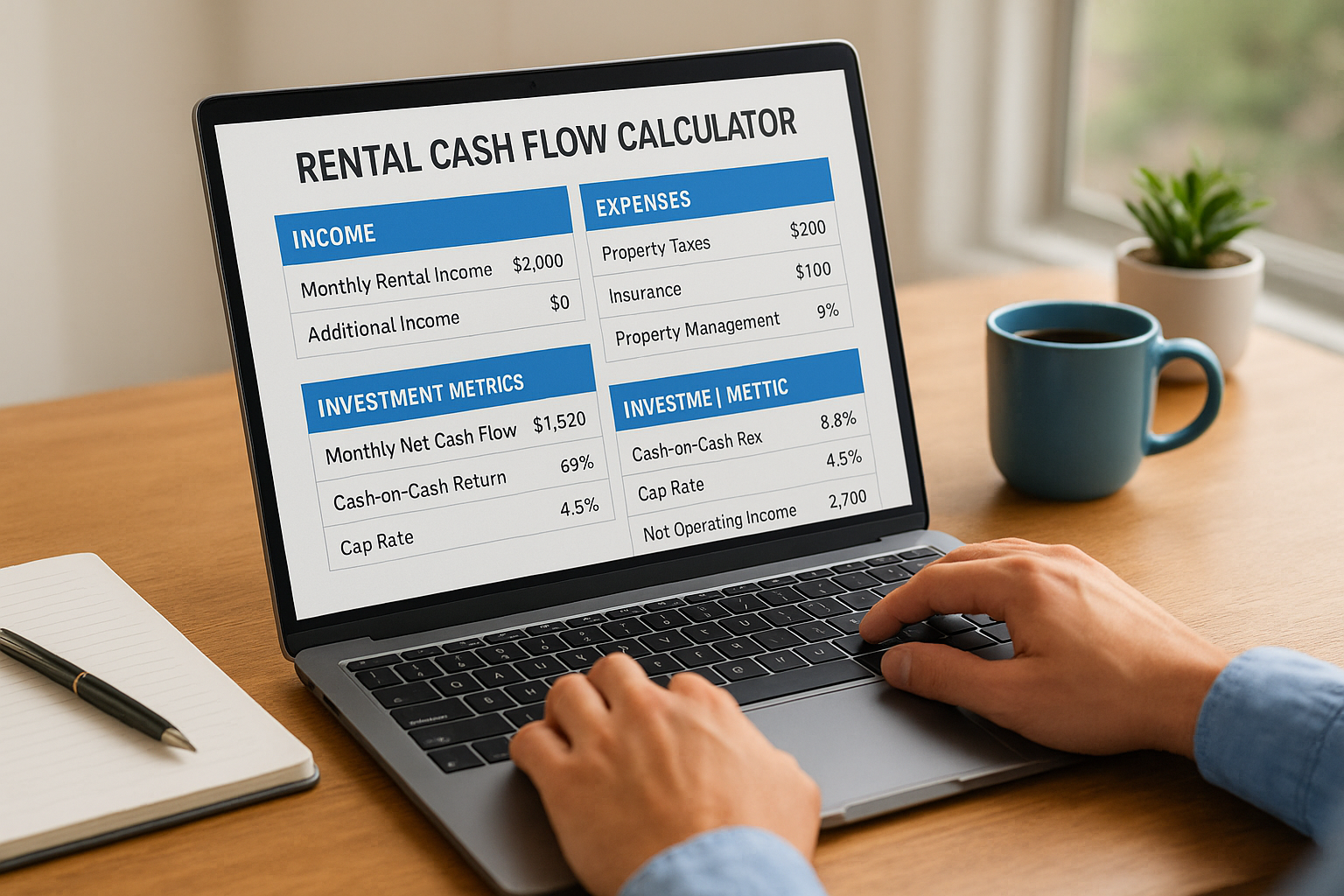

A reliable rental property cash flow calculator needs seven core components to give you accurate projections. These include purchase price, financing details, monthly rental income, operating expenses, vacancy allowance, capital expenditures, and key performance metrics. Most investors skip critical expense categories and end up with overly optimistic projections that don't match reality.

Income inputs

Your calculator must capture monthly rental income as the starting point for all calculations. Include rent from all units if you're analyzing a multi-family property, plus any additional income streams like parking fees, laundry revenue, or storage rentals. Don't inflate these numbers based on best-case scenarios you found on listing sites. Use actual market rents from comparable properties in the same neighborhood.

The most common mistake investors make is using asking rents instead of verified market rents, which can inflate cash flow by 10-15%.

Expense categories

Operating expenses fall into fixed and variable costs that you need to track separately. Fixed expenses include property taxes, insurance, HOA fees, and property management (typically 8-10% of gross rent). Variable expenses cover maintenance, repairs, utilities you pay, and capital expenditures for big-ticket items like roofs or HVAC systems. Always include a vacancy rate between 5-10% to account for turnover periods.

Investment metrics

The calculator should automatically compute four key metrics from your inputs: monthly net cash flow, cash-on-cash return, cap rate, and net operating income. These numbers tell you whether the deal works financially before you commit capital. You need all four metrics because each reveals different aspects of the investment's performance and helps you compare properties on equal footing.

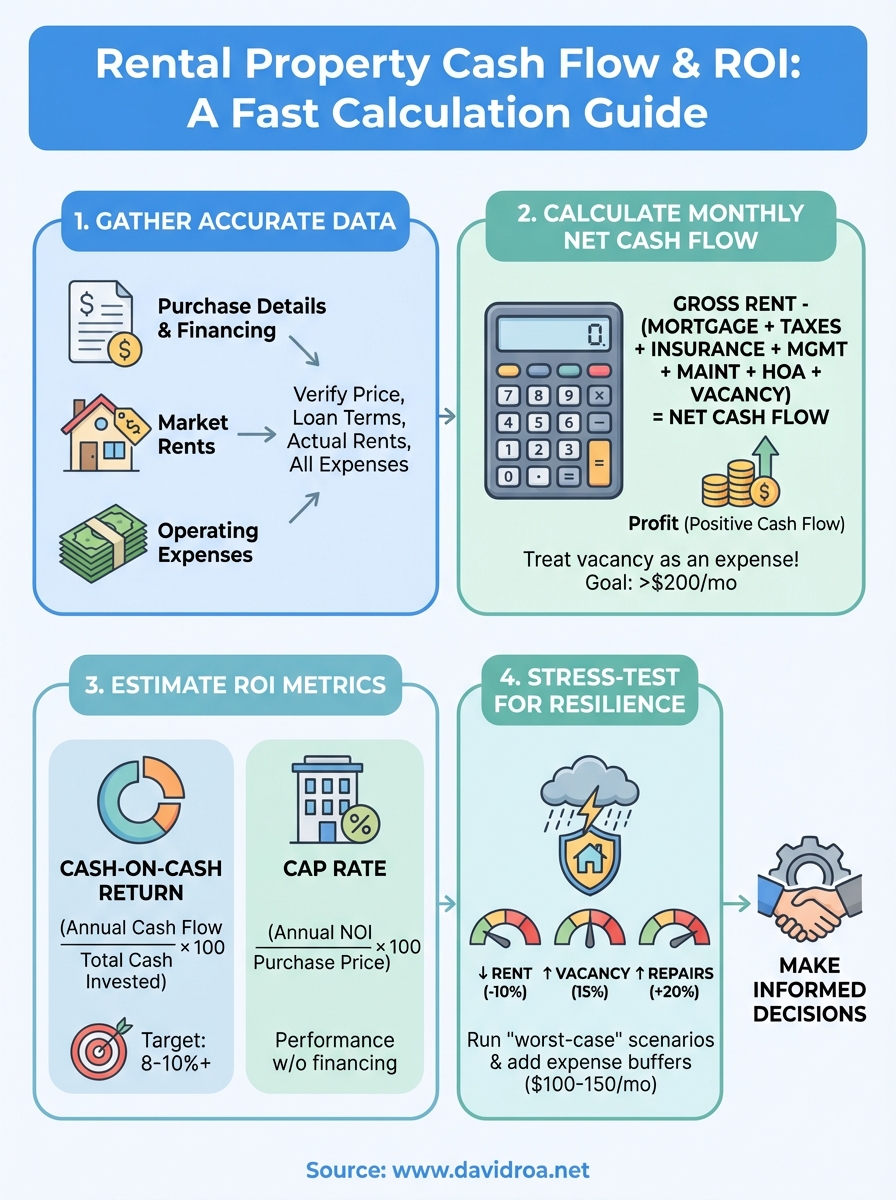

Step 1. Gather the numbers before you calculate

You need accurate data inputs before any rental property cash flow calculator can produce reliable results. Start by collecting documentation for the property's purchase price, financing terms, expected rental income, and all operating expenses. Investors who skip this step often input rough estimates that lead to wildly optimistic projections and bad investment decisions.

Property purchase details

Write down the exact purchase price including all acquisition costs like closing fees, transfer taxes, and inspection expenses. These numbers form your total capital investment, which directly affects your ROI calculations. For example, if you're buying a property for $250,000 with $8,500 in closing costs, your true purchase price is $258,500.

You also need documented proof of market rental rates from at least three comparable properties in the same zip code. Look at properties with similar square footage, bedroom count, and amenities that rented within the last 60 days. Pull this data from rental listing sites or ask local property managers for current market comps.

Financing terms

Document your loan amount, interest rate, and loan term from your lender before using any calculator. Include whether you're using conventional financing, DSCR loans, or hard money, since each option changes your monthly payment and affects cash flow differently. For instance, a DSCR loan at 7.5% on $200,000 over 30 years produces a monthly payment of roughly $1,398.

Accurate financing inputs matter more than rental income projections because your mortgage payment represents the largest fixed expense you'll face every month.

Step 2. Calculate monthly net cash flow the right way

Monthly net cash flow tells you how much money stays in your pocket after you've paid every expense on the property. This number determines whether your investment generates income or drains your capital each month. Most investors make mistakes by forgetting hidden expenses or using the wrong formula, which leads to negative surprises after closing.

The cash flow formula

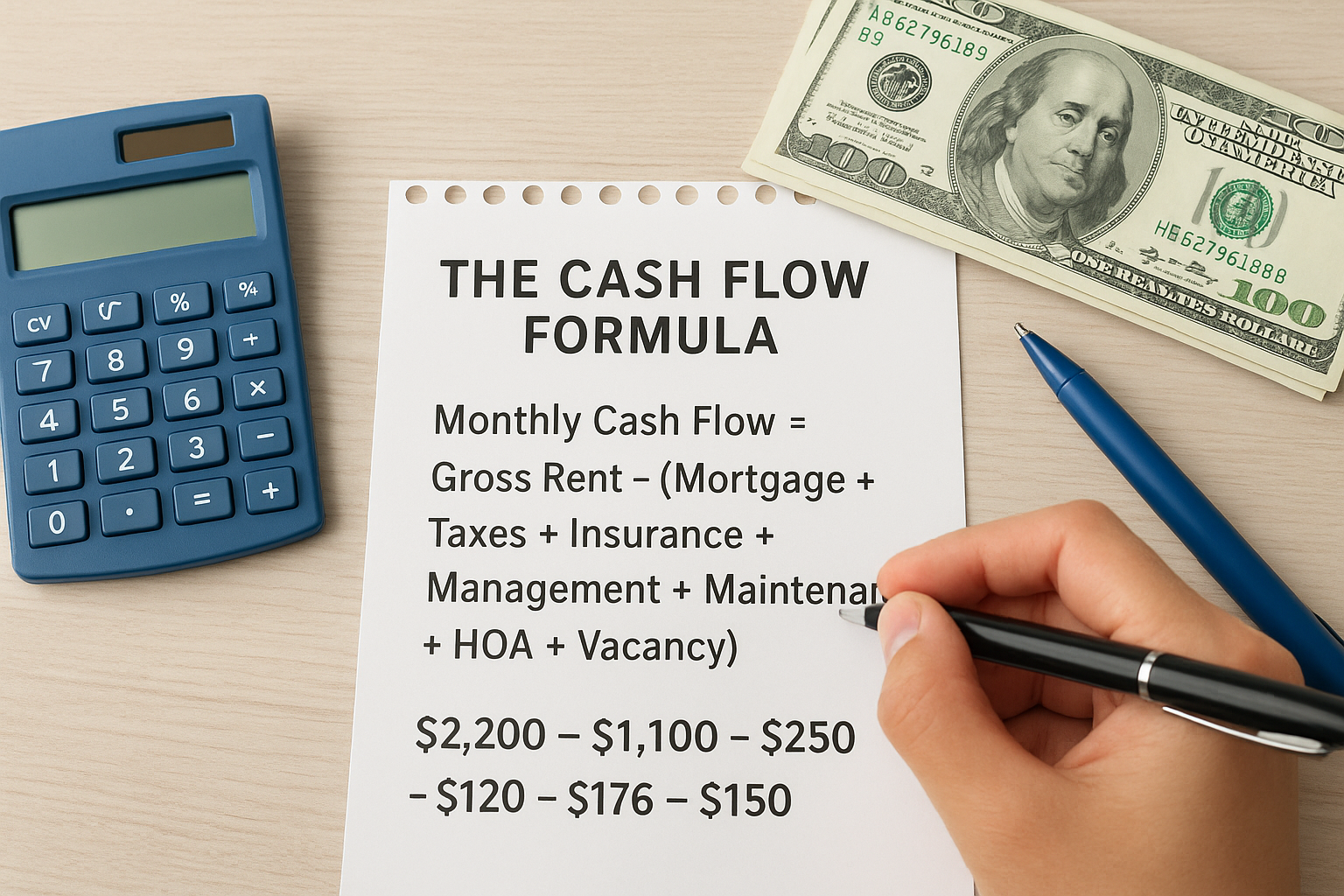

Start with gross monthly rent and subtract your mortgage payment, property taxes, insurance, property management fees, maintenance reserves, HOA fees, and vacancy allowance. The rental property cash flow calculator uses this formula to show your true monthly profit:

Monthly Cash Flow = Gross Rent - (Mortgage + Taxes + Insurance + Management + Maintenance + HOA + Vacancy)

Always calculate vacancy as a fixed monthly expense by multiplying gross rent by your vacancy rate. For example, if you collect $2,000 monthly rent with a 7% vacancy rate, set aside $140 per month ($2,000 × 0.07).

Apply the calculation

Take a property with $2,200 monthly rent, $1,100 mortgage payment, $250 property taxes, $120 insurance, $176 management (8%), $150 maintenance reserve, and $154 vacancy (7%). Your calculation looks like this: $2,200 - $1,100 - $250 - $120 - $176 - $150 - $154 = $250 monthly cash flow.

Properties with less than $200 monthly cash flow leave no room for unexpected repairs or extended vacancies, making them risky investments for most buyers.

Step 3. Estimate ROI with cash-on-cash and cap rate

Return metrics tell you how efficiently your investment generates profit relative to the capital you put in. Your rental property cash flow calculator needs to compute both cash-on-cash return and capitalization rate because each metric reveals different performance aspects. Cash-on-cash measures annual return on your down payment, while cap rate shows the property's profitability without financing factored in.

Cash-on-cash return formula

Calculate cash-on-cash return by dividing annual cash flow by total cash invested. Total cash invested includes your down payment, closing costs, and any immediate repairs. Use this formula:

Cash-on-Cash Return = (Annual Cash Flow ÷ Total Cash Invested) × 100

For example, if your property generates $3,000 annual cash flow and you invested $50,000 total (down payment plus costs), your return equals 6% ($3,000 ÷ $50,000 × 100).

Most experienced investors target a minimum 8-10% cash-on-cash return to justify the risk and effort of managing rental property.

Cap rate calculation

Cap rate measures property performance independent of financing by dividing net operating income by purchase price. Calculate it using:

Cap Rate = (Annual NOI ÷ Purchase Price) × 100

Properties with higher cap rates typically offer better returns but may come with more risk or require more management.

Step 4. Stress-test your deal before you buy

Running best-case numbers through your rental property cash flow calculator gives you false confidence in deals that won't survive reality. You need to test how the investment performs when expenses increase, rents drop, or vacancies extend beyond your initial projections. Properties that barely cash flow under perfect conditions become money pits when a single variable shifts against you.

Run worst-case scenarios

Test three scenarios using your calculator: 10% rent reduction, 15% vacancy rate instead of your baseline, and 20% higher maintenance costs. Run each scenario separately, then combine all three to see the absolute worst case. For example, if your baseline shows $250 monthly cash flow, a combined stress test might reveal negative $180 monthly cash flow, meaning you'd need to inject $2,160 annually to keep the property afloat.

Properties that still produce positive cash flow under worst-case scenarios give you the safety margin needed to weather market downturns and unexpected repairs.

Build in expense buffers

Add $100-150 monthly cushion to your expense projections beyond what the calculator shows. This buffer accounts for property tax increases, insurance rate hikes, and HOA fee adjustments that happen over time. Properties in older buildings need larger maintenance reserves because major systems like roofs, HVAC, and plumbing have shorter remaining lifespans.

Next steps

You now have the framework to analyze any investment property using a rental property cash flow calculator and determine profitability before closing. Take the next property you're considering and run all four metrics we covered: monthly cash flow, cash-on-cash return, cap rate, and net operating income. Document your findings in a spreadsheet so you can compare multiple properties side by side.

The numbers only tell part of the story. You also need financing that matches your investment strategy, whether that's DSCR loans for properties with strong rental income or hard money for quick flips that won't pencil with conventional terms. Properties that look marginal on paper can become excellent investments when paired with the right loan structure.

Ready to fund your next investment property? Contact David Roa to explore financing options built specifically for real estate investors, including DSCR loans that qualify based on property cash flow instead of personal income.