VA Cash-Out Refinance Lenders: Rates, Rules, And Top Picks

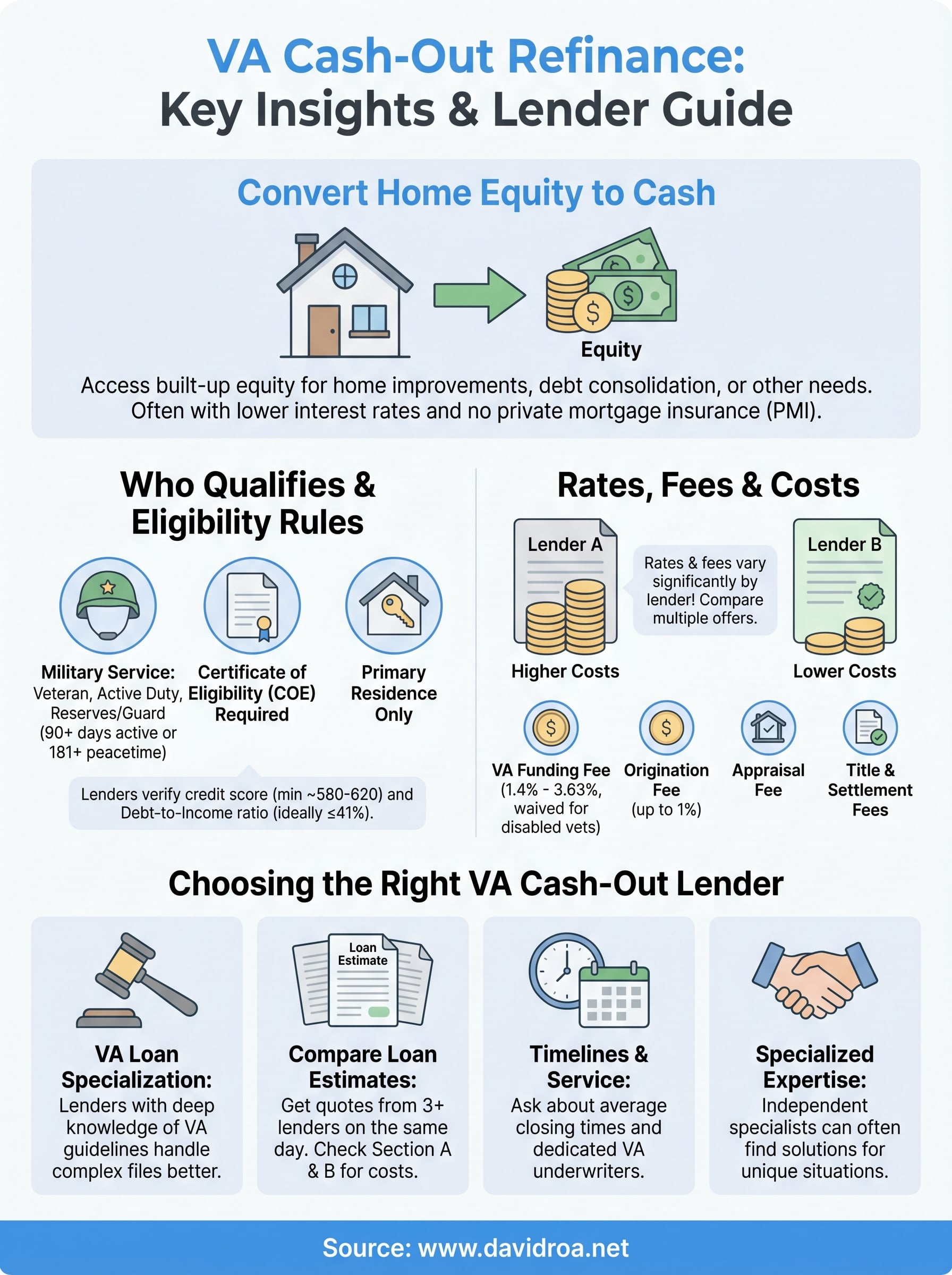

If you've built equity in your home and served in the military, a VA cash-out refinance lets you turn that equity into usable cash, without the restrictions conventional loans impose. But not all VA cash-out refinance lenders offer the same rates, timelines, or level of service, and picking the wrong one can cost you thousands over the life of the loan.

With over 25 years in mortgage lending and more than $150 million funded, I've helped veterans and active-duty service members navigate this exact decision. At David Roa, we work directly with borrowers to match them with the right VA loan product, whether that's a straightforward refinance or a more complex scenario that bigger lenders tend to overlook.

This guide breaks down how VA cash-out refinances work, what the current rates look like, who qualifies, and which lenders are worth your time. By the end, you'll have everything you need to make a confident choice and move forward with the right partner.

Why VA cash-out refinance lenders matter

The lender you choose for a VA cash-out refinance directly shapes your rate, timeline, and total loan cost. This isn't a product where all lenders work from the same playbook. Some lenders process VA loans daily and understand the VA's guidelines deeply. Others treat VA loans as a secondary product and lack the internal expertise to handle complex files efficiently, which slows down closing and can create costly surprises at the last minute.

The VA loan is a benefit, not a standard product

Your VA home loan benefit comes from the U.S. Department of Veterans Affairs, but private lenders actually fund and service these loans. That means the VA sets the rules on eligibility and loan limits, while each lender sets its own interest rates, fees, and underwriting standards within those rules. Two lenders can offer you a VA cash-out refinance on the same day and come in with rates that differ by half a percent or more.

The VA guarantees the loan, but your lender determines the cost. That gap can add up to tens of thousands of dollars over the life of the loan.

That difference compounds fast. On a $300,000 loan, a 0.5% rate gap adds roughly $30,000 in extra interest over 30 years. When you compare VA cash-out refinance lenders side by side, you're not just comparing rates. You're comparing total loan costs, service quality, and the likelihood that your file closes on time and without last-minute complications.

What the wrong lender actually costs you

Working with a lender who lacks VA loan experience creates problems that go well beyond a higher rate. Underwriting delays are common when loan officers aren't fluent in VA guidelines, especially for cash-out transactions that require a full appraisal and a Net Tangible Benefit review. These delays can push your closing date back by weeks and, in some cases, cause a rate lock to expire, forcing you to renegotiate under less favorable conditions.

Beyond timing, lender fees vary significantly from one company to the next. Origination fees, discount points, and third-party closing costs all differ. A lender with a lower advertised rate may offset that with higher fees, leaving you worse off than a lender who quoted a slightly higher rate with minimal upfront costs. Running a full cost comparison, not just a rate comparison, is the only way to see the real picture.

Lender specialization shapes your outcome

Not every mortgage company keeps dedicated VA loan specialists on staff. A lender that closes hundreds of VA loans per month operates very differently from a bank that handles a handful each quarter. Specialists know when to push back on an appraisal, how to structure a file to meet the Net Tangible Benefit requirement, and how to resolve VA underwriting issues quickly before they threaten your closing date.

For veterans with more complex situations, such as variable income, multiple properties, or recent credit events, lender expertise becomes even more critical. A knowledgeable loan officer can often find a workable path forward that a less experienced one would miss entirely, which is exactly why choosing the right partner from the start matters so much.

VA cash-out rates, fees, and closing costs

VA cash-out refinance rates tend to run slightly higher than VA purchase loan rates because the lender takes on more risk when you pull equity out rather than simply buying a home. As of early 2026, most VA cash-out refinance lenders are quoting rates in the 6.5% to 7.5% range for well-qualified borrowers, though your exact rate depends on several factors specific to your financial profile.

What drives your interest rate

Your credit score is the single biggest variable lenders use to set your rate. Borrowers with scores above 740 typically receive the most competitive offers, while scores in the 620-680 range will push your rate noticeably higher. Lenders also weigh your loan-to-value ratio (LTV): the more equity you leave in the home after the cash-out, the lower the lender's risk, and often the better your rate.

Debt-to-income ratio and the size of the loan both factor into your pricing as well. Larger loan amounts sometimes come with sharper rates because they generate more revenue for the lender per transaction. Shopping at least three lenders on the same day gives you a real-time snapshot of where the market sits and which offer actually fits your situation.

Even a 0.25% rate difference on a $350,000 loan adds more than $17,000 in interest over a 30-year term.

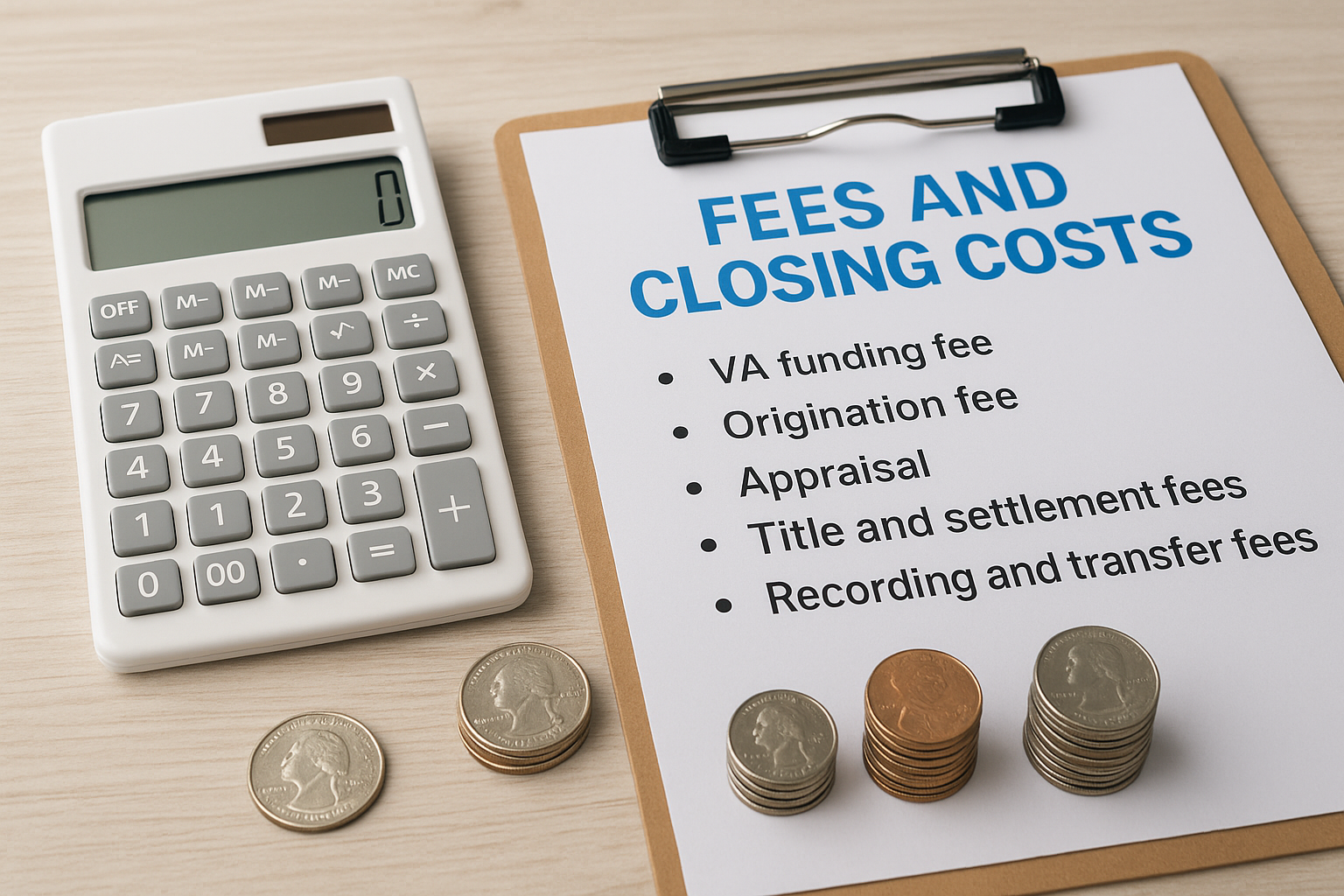

Fees and closing costs to budget for

VA loans limit what lenders can charge, but closing costs still add up. Here are the primary costs you should expect:

- VA funding fee: 3.3% for most cash-out refinances (waived if you carry a VA disability rating)

- Origination fee: Typically up to 1% of the loan amount

- Appraisal: Usually $500-$900 for the VA-required full appraisal

- Title and settlement fees: Vary by state but commonly run $800-$1,500

- Recording and transfer fees: Set by your local government

Rolling these costs into the loan is an option, but doing so increases your principal balance and your monthly payment. Compare the total loan cost across lenders, not just the rate, before you commit to anything.

VA rules and borrower eligibility basics

Before you contact VA cash-out refinance lenders, you need to confirm you actually qualify for this loan type. The VA sets firm eligibility standards that every lender must verify, and no lender can waive them regardless of how strong your credit looks. Understanding these rules upfront saves you time and protects you from starting an application that can't close.

Service and certificate of eligibility requirements

Your military service record determines whether you can access a VA cash-out refinance at all. Generally, you qualify if you served at least 90 consecutive days of active duty during wartime, 181 days during peacetime, or six years in the National Guard or Reserves. Surviving spouses of service members who died in the line of duty may also qualify under specific conditions.

You must obtain a Certificate of Eligibility (COE) before any lender can process your VA cash-out application, and most experienced lenders will pull this directly through the VA's automated system on your behalf.

You can request your COE through the VA's official website or let your lender handle it. Either way, having this document ready speeds up the underwriting process and confirms your entitlement before you spend time on paperwork.

What lenders look for beyond your military service

Meeting VA service requirements gets you in the door, but lenders still evaluate your financial profile independently. Most lenders want to see a minimum credit score between 580 and 620, though competitive rates typically require 680 or higher. Your debt-to-income ratio (DTI) should generally stay at or below 41%, though some lenders allow higher DTI with compensating factors like strong cash reserves.

The property itself must be your primary residence to use the VA cash-out option. Investment properties and vacation homes do not qualify. Additionally, lenders must verify a Net Tangible Benefit, meaning the new loan must clearly improve your financial position compared to your current loan terms. This protects you from refinancing into a worse situation, and it's a step that separates VA loans from most conventional refinance products.

How to compare VA cash-out lender offers

Comparing VA cash-out refinance lenders takes more than glancing at the rate each company advertises online. Lenders structure their offers differently, which means you need a consistent framework to evaluate what each quote actually includes. The most reliable approach is to collect at least three competing quotes on the same day, so you're working with current market data rather than numbers that were pulled at different points as rates shifted.

Use the Loan Estimate to make real comparisons

Within three business days of submitting a full application, every lender is legally required to provide you with a Loan Estimate, a standardized three-page document that breaks down your interest rate, monthly payment, closing costs, and projected total interest paid over the life of the loan. This form exists specifically to make lender comparison straightforward, and you should request one from each lender before making any commitment or paying any fees.

The Annual Percentage Rate (APR) on the Loan Estimate reflects both the interest rate and most lender fees combined, making it a more accurate comparison point than the advertised rate alone.

Pay close attention to Section A of the Loan Estimate, which itemizes origination charges, and Section B, which covers third-party services the lender requires. These two sections reveal where lenders quietly add cost that their headline rate never shows you upfront.

Ask the right questions before you commit

Rates and fees only tell part of the story. You should ask each lender about their average closing timeline for VA cash-out loans specifically, because a slow lender can let your rate lock expire and force you to renegotiate under worse conditions. Find out whether they keep dedicated VA underwriters on staff rather than loan officers who handle VA files only occasionally alongside conventional loans.

Ask directly how they handle situations where a VA appraisal comes in below the expected value. An experienced lender navigates that scenario without stalling the deal. A less specialized one may simply have no answer. How a lender responds to that question tells you as much about their actual competence as any rate they quote you.

Top VA cash-out refinance lenders to consider

No single lender is the right fit for every veteran, and the best choice depends on your financial profile, your timeline, and how complex your file looks to an underwriter. That said, a few categories of lenders consistently perform well on VA cash-out transactions, and knowing where to look helps you build a realistic shortlist before you start collecting Loan Estimates.

Large national VA specialists

Navy Federal Credit Union, Veterans United Home Loans, and USAA are three of the most recognized names in the VA lending space. These lenders close high volumes of VA loans each month, which means their teams are experienced with the full VA process, including cash-out transactions, COE verification, and Net Tangible Benefit documentation. Navy Federal and USAA limit membership to military-affiliated borrowers, while Veterans United works with any eligible veteran or service member.

Volume alone does not guarantee the best rate or the most attentive service, especially if your situation involves irregular income, recent credit events, or a tight closing timeline.

The trade-off with large national lenders is that customer service quality and loan officer continuity vary significantly depending on who handles your file. Some borrowers report difficulty reaching the same person twice during underwriting, which creates friction when issues need a fast resolution.

Mortgage brokers and independent loan officers

Working with a mortgage broker gives you access to multiple lenders through a single point of contact, which simplifies the comparison process without requiring you to manage separate applications at several institutions. Brokers who specialize in VA cash-out refinance lenders know which wholesale partners offer competitive pricing for your specific credit tier, loan size, and property type.

At David Roa, we bring over 25 years of mortgage experience to every VA loan file we work on. Our approach is direct: we assess your full financial picture, identify the right loan structure, and stay with you through every step of underwriting, including complex income documentation, prior credit events, and scenarios that larger lenders routinely decline. If your file doesn't fit a standard template, an independent specialist is usually better positioned to find a viable path forward than a call center-based operation.

Next steps

You now have the framework to move forward with confidence. Understanding how VA cash-out refinance lenders differ in rates, fees, and expertise gives you a real advantage when you start collecting quotes. The next move is straightforward: gather your Certificate of Eligibility, pull your credit report, and contact at least three lenders so you can compare Loan Estimates side by side on the same day.

Choosing the right lender makes a measurable difference in your total loan cost and how smoothly your file closes. If your situation involves irregular income, prior credit events, or a timeline that can't afford delays, working with a specialist matters even more. For a direct conversation with someone who has 25-plus years of VA lending experience and a record of closing complex files, connect with David Roa today. We'll review your full picture and help you structure the right loan from the start.