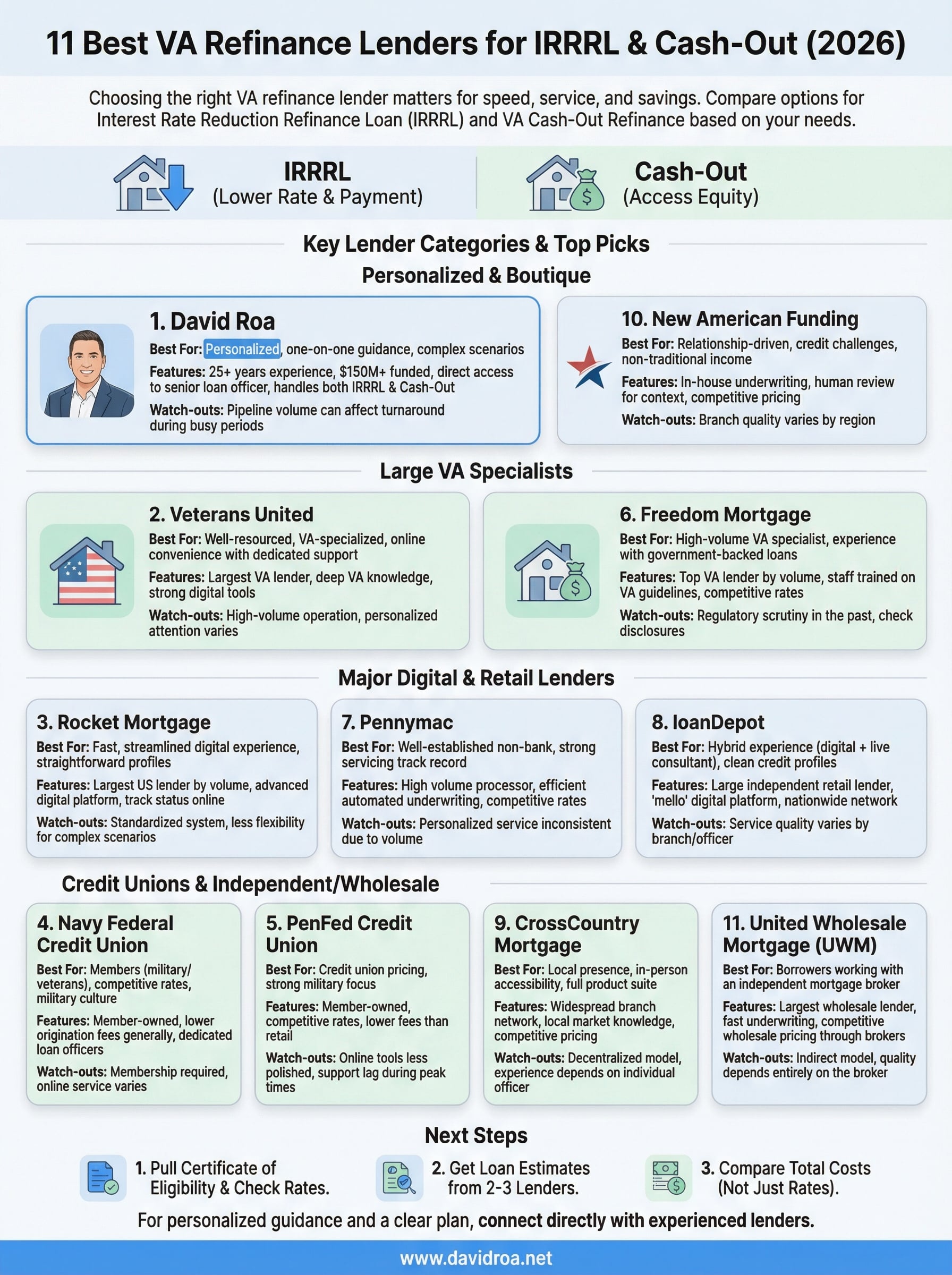

11 Best VA Refinance Lenders for IRRRL & Cash-Out (2026)

If you're a veteran or active-duty service member carrying a VA loan at a rate higher than what's available right now, refinancing could save you hundreds per month. But not all VA refinance lenders offer the same rates, turnaround times, or level of service, and picking the wrong one can cost you more than just money. It can cost you months of unnecessary back-and-forth.

Whether you're eyeing an Interest Rate Reduction Refinance Loan (IRRRL) to lower your payment with minimal paperwork or a VA cash-out refinance to tap into your home's equity, the lender you choose matters. Some specialize in speed. Others in customer service. A few do both well. The goal of this guide is to help you compare the options side by side so you can make a confident decision.

With over 25 years in mortgage lending and more than $150 million funded across residential, commercial, and investment loans, I've worked with veterans through every type of refinance scenario, straightforward and complex. At David Roa, we handle VA refinances directly and understand what separates a smooth closing from a frustrating one. That hands-on experience shaped how we evaluated each lender on this list.

Below, you'll find 11 of the best VA refinance lenders for 2026, broken down by what they do well, where they fall short, and who they're the best fit for. Let's get into it.

1. David Roa

With over 25 years of mortgage lending experience and more than $150 million funded, David Roa brings a level of hands-on expertise that most va refinance lenders simply can't match. Based in Chicago and licensed to serve clients nationwide, the focus here is on veterans who want direct access to a senior loan officer, not a rotating cast of call center representatives.

Best for

Veterans and active-duty service members who want personalized, one-on-one guidance through both IRRRL and cash-out refinance transactions. If your situation is complex, such as irregular income, investment properties, or non-standard documentation, this is the kind of lender who will work through it with you rather than hand you a denial letter.

VA refinance options offered

David Roa handles both core VA refinance products with a consultative approach, meaning you review the numbers together before committing to anything. The two options available are:

- IRRRL (Interest Rate Reduction Refinance Loan): Streamlined refinance to lower your rate with minimal documentation

- VA Cash-Out Refinance: Access your home's equity while potentially improving your rate and loan terms

A VA cash-out refinance can let you access up to 100% of your home's appraised value, which most conventional refinance products simply won't allow.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and an existing VA loan to qualify for an IRRRL. For a cash-out refinance, expect lenders to look for a minimum credit score around 620, sufficient home equity, and verifiable income. David Roa walks you through what documentation you need upfront, which cuts down on last-minute surprises at closing.

Fees and pricing notes

Expect transparent, upfront pricing with no hidden origination fees buried in the fine print. The VA funding fee still applies based on your service history and prior use of your benefit, but David Roa makes sure you know exactly what your closing costs look like before you sign anything.

Watch-outs

Because this is a boutique operation rather than a large-scale servicer, pipeline volume can affect turnaround time during busy periods. If you're working against a tight deadline, flag that at the start of the conversation. All communication is direct, which most clients find refreshing, but you'll want your documents organized and ready to move when the process begins.

2. Veterans United

Veterans United is one of the largest dedicated VA lenders in the country, and that focus shows. They've built their entire operation around military borrowers, which means their loan officers understand VA guidelines at a deep level. If you want a lender that lives and breathes VA loans, Veterans United is a serious contender among va refinance lenders.

Best for

Veterans looking for a well-resourced, VA-specialized lender with strong digital tools and a large support team. This is a particularly strong fit if you want online convenience paired with dedicated VA expertise rather than working with a generalist lender.

VA refinance options offered

Veterans United offers both the IRRRL for rate-and-term refinancing and VA cash-out refinance loans. Their online platform lets you start and track your application from any device, which cuts down on the back-and-forth that slows down many refinance timelines.

Veterans United funded over $17 billion in VA loans in 2023, making them the top VA purchase lender by volume according to government data.

Typical requirements to expect

You'll need your Certificate of Eligibility and a minimum credit score of around 620 for most programs, though their lending advisors can help you review your options if your score falls below that threshold.

Fees and pricing notes

Veterans United charges a standard origination fee, and the VA funding fee applies based on your service history. Rates are competitive, but you should always request a Loan Estimate and compare it against other quotes before committing.

Watch-outs

Veterans United is a high-volume operation, so your experience can vary depending on which loan officer you're assigned. You may not get the same personalized attention you'd find with a boutique lender, especially if your file has any complexity.

3. Rocket Mortgage

Rocket Mortgage is the largest mortgage lender in the United States by volume, and their digital-first platform has set the standard for online loan applications over the past decade. They serve a wide range of borrowers, and their VA refinance offering is a legitimate option worth considering, especially if you prefer managing your loan online rather than over the phone.

Best for

Borrowers who want a fast, streamlined digital experience and are comfortable handling most of the process through an app or web portal. Rocket Mortgage works well for veterans with straightforward financial profiles who don't need a lot of hand-holding through the refinance process.

VA refinance options offered

Rocket Mortgage offers both the IRRRL and VA cash-out refinance, and their platform lets you upload documents, check your rate, and track your loan status from one dashboard. This makes them one of the more convenient va refinance lenders for tech-comfortable borrowers.

Rocket Mortgage processed over one million loans in a single year, which reflects the scale of their operation but also the level of standardization baked into their process.

Typical requirements to expect

You'll need a minimum credit score of 620 and a valid Certificate of Eligibility. Their automated underwriting system moves quickly, but it also applies rigid qualification criteria that can trip up borrowers with non-traditional income documentation.

Fees and pricing notes

Rocket Mortgage charges an origination fee, and their rates are competitive but not always the lowest available. Always pull a Loan Estimate to compare their total cost against other quotes.

Watch-outs

Their large scale means you're working within a standardized system, not with a dedicated loan officer who knows your file. Complex scenarios, such as investment properties or irregular income, often require more flexibility than their platform allows.

4. Navy Federal Credit Union

Navy Federal Credit Union is a member-owned institution serving military members, veterans, and their families. As one of the largest credit unions in the country, they bring significant VA lending volume alongside a reputation for competitive rates that often undercuts traditional bank offerings. If you're already a member or qualify for membership, they're worth a close look.

Best for

Veterans and active-duty service members who are already Navy Federal members or plan to join before applying. Their rates tend to be sharper than many banks, and their military-focused culture means staff generally understand VA loan nuances better than a generalist lender would.

VA refinance options offered

Navy Federal offers both the IRRRL and VA cash-out refinance products. Among va refinance lenders in the credit union space, they also provide dedicated loan officers who work specifically with military borrowers through every step of the refinance process.

Navy Federal has over 13 million members and consistently ranks among the top VA lenders by volume each year.

Typical requirements to expect

You'll need membership eligibility tied to military service, a valid Certificate of Eligibility, and a credit score that typically meets or exceeds 620. Income verification requirements are standard for cash-out refinances.

Fees and pricing notes

Navy Federal generally offers lower origination fees than many retail banks. The VA funding fee still applies, but their overall closing cost structure tends to be more borrower-friendly than large commercial lenders.

Watch-outs

Membership is required before you can apply, so if you're not already a member, factor in that setup step. Their branch network is solid near military bases, but online service quality can vary depending on which loan officer handles your file.

5. PenFed Credit Union

PenFed Credit Union is one of the largest federal credit unions in the country, and they've built a strong reputation among military borrowers for offering competitive rates on VA loan products. Unlike some of the big retail lenders on this list, PenFed operates as a member-owned institution, which often translates to lower fees and more favorable terms for qualified borrowers.

Best for

Veterans who want credit union pricing without sacrificing product depth. PenFed is a particularly good fit if you prefer working with a lender that has a genuine military focus and can offer rates that give large commercial va refinance lenders a run for their money.

VA refinance options offered

PenFed offers both the IRRRL and VA cash-out refinance, and their loan officers are familiar with the full range of VA program guidelines. Their online portal handles most of the application process efficiently.

PenFed serves over 2.9 million members and is federally insured by the NCUA, which provides an added layer of financial stability for borrowers.

Typical requirements to expect

You'll need membership eligibility before applying, which is open to military members, veterans, and certain qualifying civilians. A minimum credit score of around 620 and a valid Certificate of Eligibility are standard requirements for both refinance products.

Fees and pricing notes

PenFed typically charges lower origination fees than most retail lenders, and their overall closing costs tend to be transparent and straightforward.

Watch-outs

Their online tools are functional but not as polished as Rocket Mortgage's platform, and customer service response times can lag during peak periods. If your file has any complexity, confirm upfront that your loan officer has handled similar scenarios.

6. Freedom Mortgage

Freedom Mortgage consistently ranks among the top VA lenders by volume in the United States, and their deep focus on government-backed loans gives them a genuine edge over generalist va refinance lenders. Their specialization in VA, FHA, and USDA products means the staff you work with has real familiarity with the rules that govern these programs.

Best for

Veterans who want a high-volume VA specialist with significant experience processing both streamline and cash-out refinances. Freedom Mortgage is a solid fit if your priority is working with a lender that handles VA loans as a core product rather than an afterthought.

VA refinance options offered

Freedom Mortgage offers both the IRRRL and VA cash-out refinance, and they actively market VA loans as one of their flagship products. Their loan officers are trained specifically on VA guidelines, which helps keep your file moving through underwriting without unnecessary delays.

Freedom Mortgage has ranked as a top-five VA lender by origination volume in multiple consecutive years according to publicly available government lending data.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and a credit score that generally meets the 620 minimum threshold. Income documentation requirements follow standard VA guidelines for cash-out refinances.

Fees and pricing notes

Their rates are competitive within the VA space, but origination fees vary by loan type and borrower profile. Request a full Loan Estimate before committing so you can compare their total cost structure against other quotes.

Watch-outs

Freedom Mortgage has faced regulatory scrutiny in the past related to customer service practices, so read your disclosures carefully and confirm all terms in writing before signing anything.

7. Pennymac

Pennymac is one of the largest non-bank mortgage servicers in the United States, and their VA refinance program is a serious option backed by significant operational infrastructure. They process a high volume of government-backed loans each year, which means their underwriting team has solid familiarity with VA guidelines and what it takes to close a file cleanly.

Best for

Veterans who want a well-established, non-bank lender with a strong track record in government loan servicing. Pennymac fits best for borrowers with straightforward financials who want competitive rates without needing a lot of hands-on guidance.

VA refinance options offered

Pennymac offers both the IRRRL and VA cash-out refinance, and their online portal lets you start the application and upload documents without needing to schedule a call first. As va refinance lenders go, they bring solid product depth without overcomplicating the process for standard borrowers.

Pennymac ranks among the top mortgage servicers in the country, managing hundreds of billions in unpaid principal balance across their loan portfolio.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and a minimum credit score of around 620. Income verification follows standard VA guidelines for cash-out refinances, and their automated system moves files quickly when borrowers meet the standard criteria.

Fees and pricing notes

Pennymac offers competitive rate pricing across VA products, and their Loan Estimate will clearly outline origination charges and third-party closing costs. Their overall fee structure sits in line with industry averages for non-bank lenders.

Watch-outs

Because Pennymac operates at high volume, personalized service can be inconsistent depending on who handles your file. If your situation involves any complexity, confirm upfront that your loan officer has experience with similar scenarios before your application enters underwriting.

8. loanDepot

loanDepot is one of the largest independent retail mortgage lenders in the United States, and their VA refinance program carries the weight of a company that processes a high volume of government-backed loans annually. They've invested heavily in both digital tools and a nationwide network of loan consultants, giving borrowers multiple ways to engage with the process.

Best for

Veterans who want a hybrid experience combining online convenience with access to a live loan consultant when needed. Among va refinance lenders, loanDepot works well for borrowers with clean credit profiles who want flexibility in how they communicate throughout the process.

VA refinance options offered

loanDepot offers both the IRRRL and VA cash-out refinance, and their mello platform allows you to track your loan status and upload documents digitally from application to closing.

loanDepot has funded over $275 billion in loans since its founding in 2010, reflecting significant operational scale across VA and conventional products.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and a minimum credit score that typically falls around 620. Cash-out refinances require full income documentation in line with standard VA underwriting guidelines.

Fees and pricing notes

Their origination fees and rate pricing sit within typical industry ranges for non-bank lenders. Always request a full Loan Estimate to see your complete closing cost picture before you commit to moving forward.

Watch-outs

loanDepot's service quality varies by branch and loan officer, so vet your assigned consultant early. Complex files can slow down in their system if the loan officer handling your case lacks experience with non-standard scenarios.

9. CrossCountry Mortgage

CrossCountry Mortgage has grown into one of the most geographically widespread independent lenders in the country, with licensed loan officers operating across nearly every state. Their VA loan program benefits from that reach, making them a practical choice among va refinance lenders if you want a local point of contact without sacrificing product depth.

Best for

Veterans who value local presence and in-person accessibility paired with a full suite of VA refinance products. CrossCountry is a strong fit if you prefer sitting across from your loan officer rather than managing everything through a digital portal.

VA refinance options offered

CrossCountry Mortgage offers both the IRRRL and VA cash-out refinance, and their loan officers are trained on the full VA program guidelines. Their branch structure means you can often work with someone in your market who understands local property values and closing timelines.

CrossCountry Mortgage operates in all 50 states and has grown to over 7,000 employees since its founding in 2003, reflecting the depth of their operational infrastructure.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and a minimum credit score that typically falls around 620 for most VA refinance products. Cash-out refinances require full income documentation per standard VA underwriting guidelines.

Fees and pricing notes

CrossCountry's origination fees and rate pricing are competitive but vary by branch location and loan officer. Always request a full Loan Estimate to compare their total closing cost structure against other quotes before committing.

Watch-outs

Because CrossCountry operates through a decentralized branch model, your experience depends heavily on the individual loan officer you work with. Vet your contact early and confirm they have direct experience closing VA refinances before your file enters underwriting.

10. New American Funding

New American Funding is a family-owned independent lender that has grown into one of the more recognizable names in the mortgage industry. Their VA refinance program sits within a broader product lineup that covers most major loan types, and their loan officers carry a reputation for working with borrowers whose files don't fit neatly into a standard template.

Best for

Veterans who want a relationship-driven lender with a genuine commitment to underserved borrowers. Among va refinance lenders, New American Funding stands out for their willingness to work with borrowers who have credit challenges or non-traditional income documentation that larger automated platforms often reject outright.

VA refinance options offered

New American Funding offers both the IRRRL and VA cash-out refinance, and their in-house underwriting model gives them more control over how individual files are evaluated rather than relying entirely on automated decisions.

Their in-house underwriting means a human reviewer can weigh context that an automated system would simply flag and reject.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and a credit score that generally meets the 620 minimum threshold. Cash-out refinances require full income documentation consistent with standard VA underwriting guidelines.

Fees and pricing notes

Their rate pricing and origination fees are competitive within the independent lender space. Always request a full Loan Estimate to compare their total closing cost picture against other quotes before you commit.

Watch-outs

New American Funding's branch quality varies by region, so confirm your assigned loan officer has direct experience closing VA refinances before your file moves into underwriting.

11. United Wholesale Mortgage

United Wholesale Mortgage (UWM) operates as the largest wholesale mortgage lender in the United States, which means they work exclusively through independent mortgage brokers rather than lending directly to consumers. If you want access to their VA refinance programs, you'll need to apply through a licensed broker who has a relationship with UWM. That indirect model is worth understanding before you factor them into your comparison of va refinance lenders.

Best for

Veterans who are already working with an independent mortgage broker and want that broker to have access to competitive wholesale pricing. UWM is a strong fit if your broker sources loans through their platform and can leverage their rates on your behalf.

VA refinance options offered

UWM offers both the IRRRL and VA cash-out refinance through their broker network. Their operational scale means underwriting turnaround times are generally fast when files come in clean and complete.

UWM funded over $108 billion in loan volume in 2023, making them one of the most active mortgage lenders in the country by production.

Typical requirements to expect

You'll need a valid Certificate of Eligibility and a minimum credit score around 620. Your broker handles the application submission, so the process depends heavily on their familiarity with UWM's specific documentation requirements.

Fees and pricing notes

Wholesale pricing through UWM can be sharper than retail alternatives, since the broker earns compensation separately rather than through inflated lender margins. Request a full Loan Estimate from your broker to see the complete cost breakdown before moving forward.

Watch-outs

Because you never deal with UWM directly, the quality of your experience depends entirely on your broker. Vet your broker's track record with VA loans before assuming the wholesale pricing advantage outweighs the added layer in the process.

Next steps

You now have a clear picture of how the top va refinance lenders stack up across both IRRRL and cash-out options. The right lender depends on your priorities, whether that's the lowest rate, fastest turnaround, or a loan officer who will actually pick up the phone when you have a question.

Before you apply anywhere, pull your Certificate of Eligibility, check your current rate against what's available today, and get Loan Estimates from at least two or three lenders so you can compare the total cost, not just the rate. Small differences in origination fees and closing costs add up fast over the life of a refinance.

If you want to work through your numbers with someone who has over 25 years of lending experience and has funded more than $150 million in loans, connect with David Roa directly. You'll get straight answers and a clear plan, no runaround.