Wells Fargo Equipment Finance: Loans, Leases & Login Help

If you're a business owner shopping for machinery, vehicles, or specialized tools, Wells Fargo equipment finance has likely come up in your research. Wells Fargo is one of the largest commercial lenders in the country, and their equipment financing division offers both loans and leases across a wide range of industries.

But finding clear answers about their programs, credit requirements, and online account access isn't always straightforward. That's exactly what this guide covers, from the types of financing Wells Fargo offers to how their login and payment portal works. At David Roa, we help business owners navigate equipment financing and SBA lending options every day, drawing on over 25 years of direct lending experience. We know what banks like Wells Fargo look for, and we also know when an alternative financing path might actually serve you better.

Here's a full breakdown of what Wells Fargo's equipment finance division provides, how to qualify, and what to consider before you apply.

What Wells Fargo Equipment Finance is

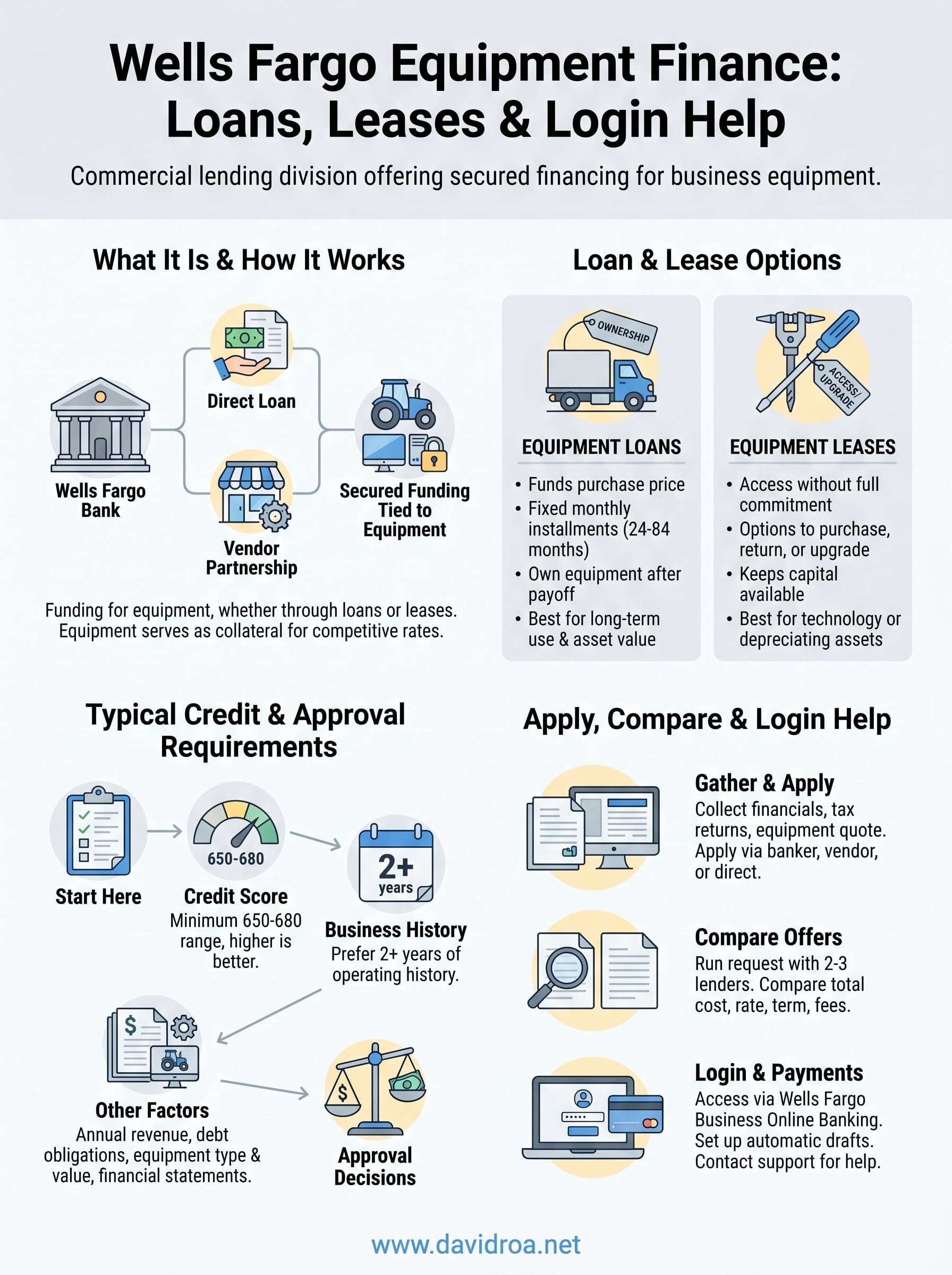

Wells Fargo Equipment Finance is the commercial lending division within Wells Fargo Bank that provides funding specifically for business equipment, whether through direct loans or lease agreements. Rather than drawing on a general business credit line, this division structures financing directly around the asset itself, which can make approval more accessible and terms more predictable for businesses across a wide range of sizes and industries.

How the division operates

The division works by providing secured financing tied to the equipment being purchased, meaning the equipment itself serves as collateral for the loan or lease. This structure gives Wells Fargo a layer of protection, which often translates into more competitive rates compared to unsecured business loans. The division operates through both direct bank channels and vendor partnerships, so you may encounter their programs through a manufacturer or dealer before you ever contact the bank directly.

Because the equipment acts as collateral, approval decisions often weigh the asset's value and your business's cash flow heavily, not just your credit score.

Who it serves

Wells Fargo's equipment financing programs target businesses across industries including construction, agriculture, healthcare, transportation, and technology. You don't need to be an existing Wells Fargo customer to apply, though having an established banking relationship with them can sometimes streamline the process. The division also works directly with equipment vendors and dealers, which means certain purchases may come with pre-arranged financing options already structured through Wells Fargo before you even walk into a branch or visit their website.

Understanding what this division actually does helps you evaluate whether it's the right fit for your specific purchase, timeline, and financial profile before you put time into an application.

Loan and lease options you can expect

Wells Fargo equipment finance offers two primary funding structures, and choosing the right one depends on how long you plan to use the equipment and whether ownership matters to your business model.

Equipment loans

With an equipment loan, Wells Fargo funds the purchase price of the asset, and you repay it in fixed monthly installments over a set term, typically ranging from 24 to 84 months. Once you pay off the loan, you own the equipment outright. This option works best when you plan to use the equipment long-term or when the asset holds strong resale value, such as heavy machinery or commercial vehicles.

If ownership and long-term asset value matter to your business, a loan usually beats a lease financially over time.

Equipment leases

Leasing gives you access to equipment without the full purchase commitment, which keeps your capital available for other operating needs. Wells Fargo structures leases with terms that typically include options to purchase at the end, return the equipment, or upgrade to newer models. Leasing tends to suit businesses that work with technology or specialized tools that become outdated quickly, since it limits the risk of owning depreciating assets outright.

Typical credit and approval requirements

Wells Fargo equipment finance sets qualification standards that reflect the bank's focus on lower-risk commercial lending. Understanding what they look for before you apply saves you time and helps you approach the process with realistic expectations about your approval odds.

Credit score and business history

Their review typically starts with a minimum credit score in the 650-680 range, though stronger scores improve your rate and terms significantly. They also prefer businesses with at least two years of operating history, which gives them a clearer picture of your revenue stability and repayment capacity.

Newer businesses with strong cash flow and solid collateral can still qualify, but expect more documentation requests and potentially higher rates.

Other factors that affect approval

Beyond your credit score, Wells Fargo reviews your annual revenue, existing debt obligations, and the type of equipment you plan to purchase. The asset's value and expected useful life factor into how much they will fund and at what terms. Providing complete financial statements and recent tax returns upfront speeds up the underwriting process and reduces the back-and-forth with their team considerably.

How to apply and compare offers

Applying for wells fargo equipment finance starts with gathering your core business documents before you contact them. Having your most recent two years of tax returns, current financial statements, and a clear equipment quote ready from day one keeps the process moving without unnecessary delays.

Submitting your application

You can apply through a Wells Fargo business banker, through a participating equipment vendor, or by contacting their commercial lending team directly. The vendor route often speeds things up since dealers with existing relationships can submit financing requests on your behalf. Either way, Wells Fargo will ask for business financials, ownership information, and details on the equipment you intend to purchase.

Applying through a vendor partner can reduce your processing time significantly since they handle much of the initial paperwork.

Comparing your offers

Before you sign anything, run the same request through at least two or three lenders to see how Wells Fargo's terms stack up. Pay close attention to the total cost of financing, not just the monthly payment, since rate differences and fees compound over a multi-year term.

Key numbers to compare across lenders:

- Interest rate or factor rate

- Loan term length

- Down payment requirement

- Prepayment penalties

- Total repayment amount

Login, payments, and customer support help

Once your wells fargo equipment finance loan or lease is active, managing your account online is straightforward. Wells Fargo provides account access through their standard business banking portal, where you can view statements, track your balance, and monitor payment schedules in one place.

If you financed through a vendor partner rather than directly through Wells Fargo, confirm which portal your account falls under before your first payment is due.

Accessing your online account

You log in through Wells Fargo's main business online banking platform at wellsfargo.com. If your equipment account was set up under a commercial lending agreement, your loan number and business credentials from enrollment are what you need to get started. Contact their business banking support line if your account isn't visible after logging in.

Making payments and reaching support

Payments can be set up as automatic drafts directly from your business checking account, which reduces the risk of late fees over a multi-year term. For questions about your loan balance, payoff amounts, or billing disputes, Wells Fargo's commercial lending support team is reachable by phone through the number listed on your loan documents or the back of any statement you receive.

Next steps

Wells Fargo equipment finance gives you a solid range of options, but it works best for businesses that meet their credit and revenue standards and have time to move through a traditional bank's underwriting process. If your profile fits, gather your financial documents, request quotes from multiple lenders, and compare the total repayment cost before you commit to any agreement.

If you run into tighter timelines, a newer business history, or a loan scenario that doesn't fit a bank's standard box, alternative lenders and SBA programs can fill that gap more effectively. David Roa has structured financing for business owners across construction, real estate, and commercial industries for over 25 years, including equipment loans and SBA 7a and 504 programs that many traditional banks won't touch. If you want a direct conversation about your options before you apply anywhere, connect with David Roa and get guidance built around your actual situation.