What Is Private Mortgage Insurance (PMI)? Costs And Removal

If you're putting less than 20% down on a home, you've likely encountered the term private mortgage insurance (PMI). This additional monthly cost catches many buyers off guard, adding hundreds of dollars to their mortgage payment. Understanding what is private mortgage insurance PMI and how it works can save you money and help you plan your path to homeownership more effectively.

PMI exists to protect lenders when borrowers make smaller down payments. From a lender's perspective, a lower down payment means higher risk, and PMI offsets that risk. While it benefits the lender, you're the one paying for it. The good news? PMI isn't permanent, and there are clear strategies to remove it once you've built enough equity in your home.

With over 25 years of experience helping homebuyers navigate mortgage options, from conventional loans to FHA and specialized programs, I've walked countless clients through PMI decisions at every stage of the process. This guide breaks down how PMI works, what it actually costs, and the specific steps you can take to eliminate this expense from your monthly payment. Whether you're a first-time buyer weighing your down payment options or a current homeowner looking to drop PMI, you'll have the clarity you need to make informed decisions.

What PMI is and when you need it

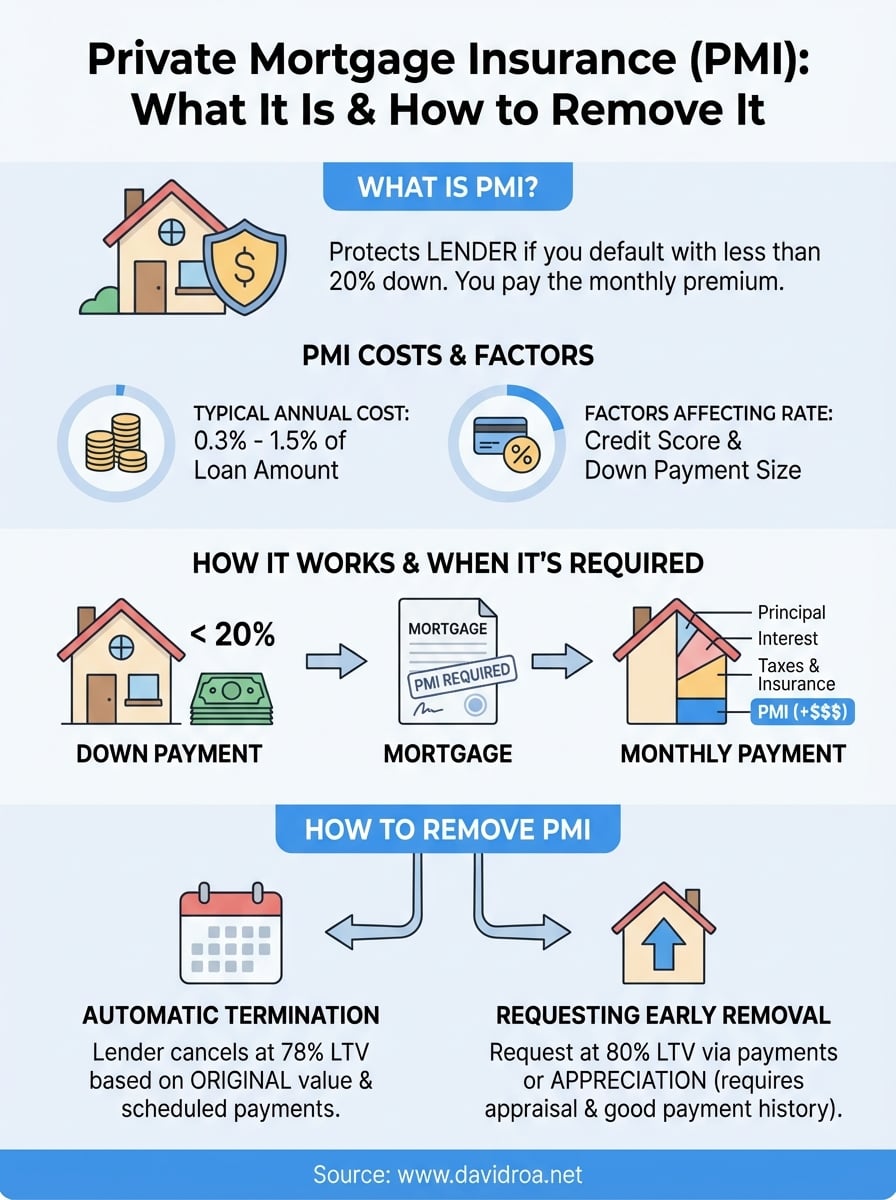

Private mortgage insurance is a monthly fee added to your mortgage payment when you borrow more than 80% of your home's value. The insurance protects your lender if you default on the loan, but you pay the premium as part of your ongoing housing costs. Banks treat higher loan-to-value ratios as riskier, and PMI gives them confidence to approve your mortgage even with a smaller down payment.

The 20% down payment threshold

You'll encounter PMI when your down payment falls below 20% of the home's purchase price. If you buy a $300,000 home with $45,000 down (15%), you're borrowing $255,000, which represents 85% of the property value. That loan-to-value ratio triggers the PMI requirement automatically. The same rule applies whether you're buying your first home or your fifth.

PMI kicks in at 80.01% loan-to-value and remains until you reach 78% or lower through payments or appreciation.

Refinancing can also bring PMI into the picture. If your home's current value doesn't support at least 20% equity, a new conventional loan will include PMI even if your original mortgage didn't have it. Many homeowners discover this when trying to refinance shortly after purchase, before their property has appreciated or they've paid down enough principal.

Common situations that trigger PMI

First-time buyers frequently pay PMI because saving a full 20% down payment takes years in many markets. A couple buying that same $300,000 home would need $60,000 cash for the down payment alone, not counting closing costs. Choosing a 10% or 15% down payment gets them into the home faster, with PMI as the trade-off for earlier homeownership.

Sellers relocating for work often face PMI on their next purchase. Your equity from selling one home might not cover 20% down in a more expensive market. Stretching to a larger home before you've built substantial equity in your current property leaves you short of that threshold. Investment property purchases also require PMI if you're putting less than 20% down, though investor loans typically demand higher down payments overall to qualify.

Loan types that require PMI

Conventional loans backed by Fannie Mae or Freddie Mac are the primary loan type where what is private mortgage insurance PMI becomes a factor. These government-sponsored enterprises set the 80% loan-to-value threshold as their standard, and virtually all conventional lenders follow this guideline. The specific PMI rates and removal rules tie directly to these conforming loan standards.

FHA loans use a different system called mortgage insurance premium (MIP), not PMI, though it serves a similar purpose. VA loans for military members and USDA loans for rural properties skip mortgage insurance entirely, even with zero down payment. That's why understanding your loan type determines whether PMI applies and what alternatives you might pursue.

Why lenders require PMI and who it protects

Lenders use PMI as financial protection against losses when your down payment doesn't give them enough cushion in the deal. A 20% down payment creates a buffer where the lender can recoup their investment even if they need to foreclose and sell the property below market value. When you put down less, the lender takes on more exposure, and PMI transfers that risk to an insurance company.

The risk assessment behind PMI

Banks calculate risk based on how much of their own money they could lose if you stop making payments. With a 5% down payment on a $300,000 home, the lender finances $285,000 while you've contributed only $15,000. If the housing market drops 10% and you default, the property might sell for $270,000 at foreclosure. After selling costs, the lender faces a substantial loss that your small down payment can't cover.

PMI reimburses the lender for 20-30% of the loan amount, reducing their actual risk to levels comparable with a traditional 20% down payment loan.

Statistical data shows borrowers with smaller down payments default at higher rates. You have less equity at stake, making it easier to walk away when financial troubles hit. Understanding what is private mortgage insurance PMI means recognizing that lenders use historical patterns to price risk, and borrowers with less skin in the game represent measurable added risk that requires mitigation.

Who PMI actually protects

The insurance policy protects your lender exclusively, not you. If you default, PMI pays the bank a portion of their losses, typically covering 20% to 30% of the original loan amount. You've been paying premiums monthly, but you receive zero benefit from that coverage. The lender gets compensated while you still face foreclosure, damaged credit, and loss of your down payment.

Many buyers assume PMI protects them if they fall behind on payments or need to sell underwater. PMI doesn't prevent foreclosure, reduce your payment obligations, or help you keep your home during hardship. Your monthly premium serves purely as the lender's insurance policy that they require you to fund. Once you build 20% equity through payments or appreciation, they no longer need that protection, which is why PMI becomes removable at that threshold.

How PMI costs work and how to estimate them

PMI costs typically range from 0.3% to 1.5% of your original loan amount annually, divided into monthly payments added to your mortgage bill. A $250,000 loan with 0.5% PMI costs $1,250 per year, or roughly $104 monthly. Your actual rate depends on your credit score, down payment size, and loan type, with better credit and larger down payments earning lower premiums.

How lenders calculate your PMI rate

Insurance companies price PMI based on risk factors they can measure and predict. Your credit score carries the most weight in determining your rate. A borrower with a 760 credit score putting 10% down might pay 0.4% annually, while someone with a 680 score and the same down payment could pay 0.9% or higher. Each 20-point drop in credit score typically increases your PMI rate by several basis points.

Down payment percentage directly affects your premium. Putting 15% down costs less than 10% down, and 5% down triggers the highest PMI rates in the spectrum. Lenders view smaller equity stakes as proportionally riskier. Understanding what is private mortgage insurance PMI means recognizing that every additional percentage point of down payment reduces both your loan amount and your insurance rate simultaneously.

A borrower with excellent credit (740+) putting 15% down typically pays 0.3% to 0.5% annually, while fair credit (680-699) with 5% down can reach 1.2% or higher.

Quick estimation method for your situation

You can estimate PMI by multiplying your loan amount by 0.5% to 1% for a rough annual cost, then dividing by 12 for the monthly figure. A $300,000 loan at 0.75% equals $2,250 annually or $187.50 monthly. This ballpark helps you budget before getting formal quotes from lenders, though your actual rate requires underwriting review.

Request specific PMI quotes when comparing loan offers. Lenders must disclose your exact PMI premium in your Loan Estimate within three days of application. Comparing these numbers across multiple lenders reveals which ones negotiate better rates with PMI companies, potentially saving you $50 to $100 monthly on the same loan scenario.

How you pay PMI and how to avoid it

Most borrowers pay PMI as a monthly addition to their mortgage payment, bundled with principal, interest, property taxes, and homeowners insurance. Your lender collects the premium and forwards it to the insurance company on your behalf. This standard approach keeps your total housing payment in one place, though it increases your monthly obligation until you reach the equity threshold to drop coverage.

Monthly premium vs. upfront payment options

The typical monthly PMI payment gets added automatically to your mortgage statement. You'll see it itemized separately, making it easy to track exactly what you're paying for this insurance. Monthly premiums remain constant unless you refinance or request PMI removal, and they continue until you take action to eliminate them through equity buildup.

Some lenders offer upfront PMI where you pay the entire premium at closing as a one-time cost. This eliminates the monthly charge but requires thousands of dollars in additional cash at purchase. A $250,000 loan might have $5,000 to $7,500 in upfront PMI for several years of coverage. Lender-paid PMI represents another option where the bank covers your premium in exchange for a slightly higher interest rate, typically 0.25% to 0.50% higher over the loan's life.

Upfront and lender-paid PMI options remove the monthly charge but cost more over time compared to monthly premiums you can cancel after reaching 20% equity.

Strategies to avoid PMI entirely

Saving a full 20% down payment eliminates PMI from the start. If you're $10,000 to $15,000 short of that threshold, delaying your purchase a few months to reach 20% saves you years of insurance premiums. Many buyers find this worth the wait when they calculate total PMI costs against a slightly longer savings timeline.

Piggyback loans offer another route around PMI. You take a primary mortgage for 80% of the purchase price, a second mortgage for 10% to 15%, and cover the remaining 5% to 10% as your down payment. This structure avoids PMI because your first mortgage stays at or below 80% loan-to-value. The second mortgage typically carries a higher interest rate but often costs less than PMI, and you can pay it off aggressively without removal restrictions.

Understanding what is private mortgage insurance PMI means recognizing that multiple paths exist to minimize or eliminate this expense based on your financial situation and timeline.

How to remove PMI and the rules to know

Federal law gives you clear rights to remove PMI once you've built sufficient equity in your home. The Homeowners Protection Act of 1998 established specific thresholds and procedures that lenders must follow, taking the guesswork out of when and how you can eliminate this monthly expense. Understanding what is private mortgage insurance PMI includes knowing exactly when you're entitled to cancel it and the steps required to make that happen.

The automatic termination at 78% LTV

Your lender must automatically cancel your PMI when your loan balance reaches 78% of the home's original purchase price, provided you're current on payments. This happens through your regular monthly payments without any action required from you. If you bought a home for $300,000, the lender terminates PMI once your remaining balance drops to $234,000, regardless of current market value or appraisals.

The termination date gets calculated from your original amortization schedule at closing, so you know the exact month years in advance. Lenders must notify you annually about your PMI status and projected removal date. This automatic removal protects you if you forget to request cancellation, though waiting for 78% costs you several extra months of premiums compared to requesting removal at 80%.

Automatic termination at 78% LTV uses your original purchase price and scheduled payments, requiring no appraisal or request from you.

Requesting early removal at 80% equity

You can request PMI cancellation once you reach 80% loan-to-value through payments, typically six months to a year before automatic termination kicks in. Your lender reviews your payment history, confirms you're current, and verifies no subordinate liens exist on the property. Meeting these conditions obligates the lender to approve your removal request.

Early removal based on appreciation requires an appraisal proving your home's increased value creates 20% equity. Most lenders require at least two years of ownership before considering appreciation-based removal, and you'll pay $400 to $600 for the appraisal out of pocket. The new value must show 20% equity, and you need perfect payment history for the past year with no late payments in the previous six months.

Wrapping it up

Understanding what is private mortgage insurance PMI gives you control over a significant monthly expense that many homeowners overlook. You now know PMI protects your lender when you put less than 20% down, costs between 0.3% and 1.5% of your loan amount annually, and becomes removable at 80% loan-to-value through either scheduled payments or appreciation-based equity growth. These mechanics apply whether you're buying your first home or refinancing an existing property.

Your path forward depends on your specific situation. Buyers close to 20% down might delay purchase briefly to avoid PMI entirely, while those needing to move quickly can plan their removal strategy from day one. Current homeowners paying PMI should track their equity and request cancellation as soon as they reach the threshold, potentially saving hundreds monthly.

Working with an experienced loan officer helps you navigate PMI decisions and identify the best financing structure for your goals. If you're ready to explore mortgage options or discuss strategies to minimize PMI costs, reach out to discuss your specific situation and get personalized guidance based on over 25 years of lending experience.