Zillow Foreclosure Center: How To Find Pre-Foreclosures

Finding foreclosure properties can be one of the smartest ways to build equity fast or land a home below market value. The Zillow Foreclosure Center gives buyers and investors a dedicated portal to search pre-foreclosures, bank-owned homes, and auction listings nationwide. But knowing how to navigate the platform, and understanding what you're actually looking at, requires more than just clicking around.

As a mortgage broker and active real estate investor with over 25 years in the lending business, I've helped buyers and flippers secure financing for distressed properties through programs like Fix and Flip loans, Hard Money lending, and DSCR loans. Whether you're a first-time buyer searching for a deal or an investor scaling your portfolio, understanding Zillow's foreclosure tools gives you a real edge when competing for these properties.

This guide breaks down how to find pre-foreclosures on Zillow, what each listing type actually means, and how to move from browsing to closing. You'll also learn which financing options work best for distressed property purchases, so you're ready to act when the right opportunity shows up.

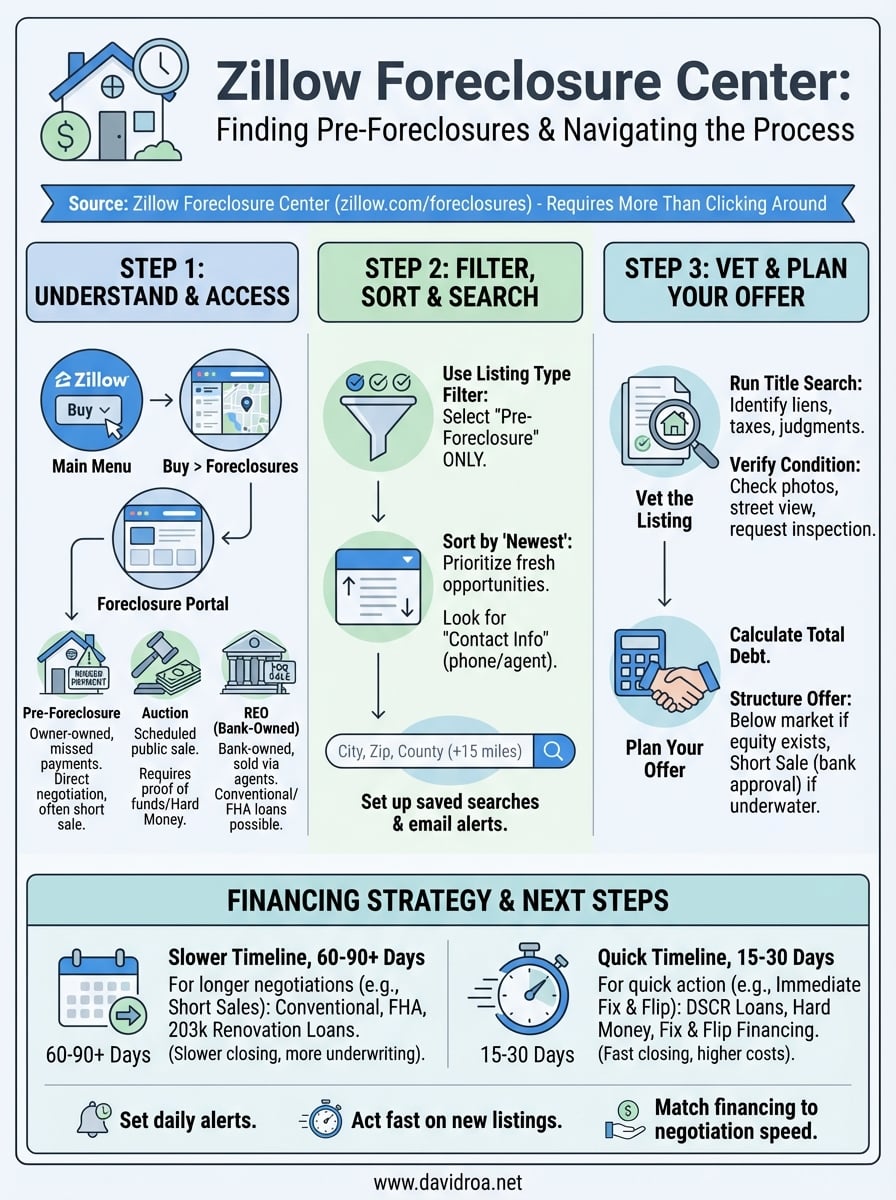

What Zillow shows as pre-foreclosure, auction, and REO

The Zillow Foreclosure Center breaks distressed properties into three distinct categories, and each one carries different risks, timelines, and purchase requirements. Knowing which type you're looking at helps you choose the right strategy and financing before you waste time on listings that won't work for your situation.

Pre-foreclosure properties

Pre-foreclosures are homes where the owner has missed mortgage payments but the bank hasn't taken legal possession yet. You'll see these labeled as "Pre-Foreclosure" on Zillow, and the property is still technically owned by the original borrower. Most pre-foreclosure deals happen through direct negotiation with the homeowner or their attorney, often as short sales where the lender agrees to accept less than the full loan balance.

Pre-foreclosure listings give you a chance to negotiate directly with homeowners before banks set strict auction or REO terms.

Auction listings

Auction properties are scheduled for public foreclosure sales, usually on courthouse steps or through online auction platforms. Zillow displays the auction date and minimum bid when available, but you typically need to bring cash or proof of funds to participate. Most auction buyers use Hard Money loans or private capital because traditional mortgage lenders can't close fast enough to meet auction deadlines.

REO (Real Estate Owned) properties

REO homes are bank-owned properties that didn't sell at auction and are now listed like traditional real estate. Banks handle these sales through real estate agents, and you can finance them with conventional mortgages, FHA loans, or renovation products like 203k loans. REO properties often need repairs, but you get a clear title and more time to complete inspections compared to auctions.

Step 1. Find the Zillow Foreclosure Center and key filters

The Zillow Foreclosure Center lives at zillow.com/foreclosures, but you can also reach it by clicking the "More" dropdown in the main navigation menu and selecting "Foreclosures" under the "Buy" section. Once you land on the portal, you'll see a map-based interface with listings grouped by location and foreclosure type. Start by entering your target city or zip code in the search bar at the top of the page to pull up available properties.

Accessing the foreclosure portal

You don't need a Zillow account to browse foreclosure listings, but creating one lets you save searches and set up email alerts when new pre-foreclosures hit the market. After entering your location, the system displays all distressed properties in that area, including pre-foreclosures, auctions, and REO homes. The default view shows all three categories mixed together, so your next step is filtering the results to focus on pre-foreclosures specifically.

Setting up saved searches with email alerts helps you spot pre-foreclosure opportunities before other buyers see them.

Setting up your search filters

Click the "Listing Type" filter on the left sidebar and select only "Pre-Foreclosure" to remove auction and REO properties from your results. You can also adjust price range, square footage, and number of bedrooms to narrow the list further. Most serious buyers add filters for property condition and days on market to find homes where owners might be more motivated to negotiate quickly.

Step 2. Search for pre-foreclosures the right way

Once you've filtered the Zillow Foreclosure Center to show only pre-foreclosures, your next step is sorting the results to surface the best opportunities first. Click the "Sort" dropdown at the top of the listing page and select "Newest" to see properties that just entered pre-foreclosure status. These homeowners are often more willing to negotiate because they haven't been bombarded with investor calls yet, and you can move quickly before competition heats up.

Prioritize listings with contact information

Properties showing a phone number or listing agent give you a direct path to start conversations. Scroll through your filtered results and flag any listing that includes contact details in the property description. Some pre-foreclosures on Zillow display the homeowner's attorney or the bank's asset manager, which means you can reach out immediately instead of tracking down public records.

Pre-foreclosures with visible contact information let you start negotiations faster than properties where you need to research ownership first.

Expand your search radius strategically

If your initial city search returns limited results, widen your zip code range by 10 to 15 miles to capture nearby properties. You can also search by county name to pull suburban and rural pre-foreclosures that other buyers overlook. Just make sure you adjust your financing strategy if you're crossing county lines, since property taxes and local ordinances can affect your total acquisition cost.

Step 3. Vet a pre-foreclosure listing before you act

Every listing you pull from the Zillow Foreclosure Center needs verification before you commit time or money to pursuing it. Pre-foreclosures carry hidden risks like multiple liens, unpaid property taxes, or structural damage that the homeowner won't disclose. Your job is confirming the property's actual situation through public records and visual inspection, not just trusting what Zillow displays on the listing page.

Check ownership and lien status

Start by running a title search through your county recorder's office or a title company to identify all liens against the property. You're looking for mortgage balances, tax liens, mechanics liens, and judgment liens that will need to be cleared or negotiated during the purchase. Properties with multiple lien holders require longer negotiation periods because each creditor must agree to the short sale terms.

Pre-foreclosures with clean title searches close faster than properties buried under multiple liens or code violations.

Verify property condition from available data

Look for recent photos, street view images, and tax assessor records to gauge the home's condition before scheduling a walkthrough. Check if the property shows signs of vacancy like overgrown landscaping or boarded windows, which often signal deferred maintenance. You can also request a preliminary inspection through the listing agent to identify major repair costs before making an offer.

Step 4. Plan your offer, financing, and due diligence

Once you've vetted a pre-foreclosure from the Zillow Foreclosure Center and confirmed it's worth pursuing, you need a concrete offer strategy that accounts for the seller's equity position, outstanding liens, and your financing timeline. Pre-foreclosure deals fall apart when buyers submit generic offers without understanding how much the bank will accept or which loan products can close fast enough to satisfy all parties involved.

Structure your offer based on equity position

Calculate the total debt load by adding all mortgage balances, tax liens, and creditor claims you found during your title search. If the homeowner has equity after covering these debts, you can negotiate directly for a below-market sale. When the property is underwater (debts exceed value), you're dealing with a short sale that requires bank approval before closing. Your offer should leave room for closing costs and any payoffs the lender demands to release the lien.

Match your financing to the timeline

Short sales and pre-foreclosure negotiations often take 60 to 90 days to finalize, which rules out Hard Money loans with high monthly costs. Use conventional mortgages, FHA loans, or 203k Renovation loans if the property qualifies and you have time for underwriting. Investors flipping the property immediately should secure DSCR loans or Fix and Flip financing that closes in 15 to 30 days to avoid delays that kill the deal.

Pre-foreclosure financing needs to match negotiation speed, not just purchase price and property condition.

Next steps to take

Finding pre-foreclosures through the Zillow Foreclosure Center gives you access to properties before they hit the auction block, but your success depends on moving fast with the right financing in place. Start by setting up saved searches with daily email alerts so you see new listings within hours of posting. Once you identify a target property, run your title search and reach out to the listing contact immediately to gauge the homeowner's motivation and timeline.

Your financing strategy determines whether you can close the deal or lose it to a cash buyer. Pre-foreclosures requiring quick closings work best with DSCR loans, Hard Money lending, or Fix and Flip financing that funds in 15 to 30 days. If you need help structuring a loan for a distressed property or want guidance on which financing option matches your investment goals, reach out to discuss your specific situation and get a clear path to closing.