Cash On Cash Return vs Cap Rate: Key Differences Explained

Real estate investors often debate cash on cash return vs cap rate when analyzing potential deals. Both metrics matter, but they measure different things, and confusing them can lead to poor investment decisions. As someone who has funded over $150 million in loans and actively invests in real estate myself, I see this confusion regularly among clients evaluating their next property.

Here's the key distinction: cap rate ignores your financing, while cash on cash return puts your actual out-of-pocket investment under the microscope. This difference becomes critical when you're using leverage, whether through a conventional mortgage, a DSCR loan, or hard money financing, to acquire properties.

This article breaks down both metrics with clear definitions, formulas, and practical examples. You'll learn exactly when to use each one and how your financing strategy directly impacts your returns. By the end, you'll evaluate investment opportunities with the same precision that separates successful investors from the rest.

Why cap rate and cash-on-cash return matter

You need both metrics because they answer fundamentally different questions about your investment. Cap rate tells you how the property performs on its own, independent of how you pay for it. Cash on cash return reveals your actual profit based on the money you personally invest. Most investors make costly mistakes by relying on just one metric when evaluating deals.

They reveal different layers of profitability

Cap rate gives you the property's raw earning potential without considering your financing structure. When you compare a 7% cap rate building in one neighborhood against an 8% cap rate property across town, you're evaluating the assets themselves. This becomes your baseline for determining if a deal makes sense before you factor in loans, down payments, or leverage strategies.

Cash on cash return shows what happens after you apply your specific financing. If you put $100,000 down on that 7% cap rate property and generate $15,000 in annual cash flow, your cash on cash return hits 15%. This metric reflects your actual wallet performance, not theoretical returns. The gap between cap rate and cash on cash return reveals how effectively you're using leverage to amplify gains.

Understanding cash on cash return vs cap rate helps you screen opportunities faster and avoid properties that look good on paper but drain your actual resources.

Your financing strategy determines which metric matters more

All-cash buyers focus heavily on cap rate because their purchase price equals their investment. When you buy a $500,000 property outright, cap rate directly predicts your return. No loans mean no monthly debt service eating into profits, so the property's performance and your personal return align perfectly.

Leveraged investors prioritize cash on cash return because financing dramatically changes outcomes. A DSCR loan or conventional mortgage lets you control expensive properties with smaller down payments. Your $100,000 might secure a $400,000 building, creating returns that far exceed what cap rate alone suggests. However, negative leverage works both ways, where high interest rates can crush your actual cash flow despite a strong cap rate.

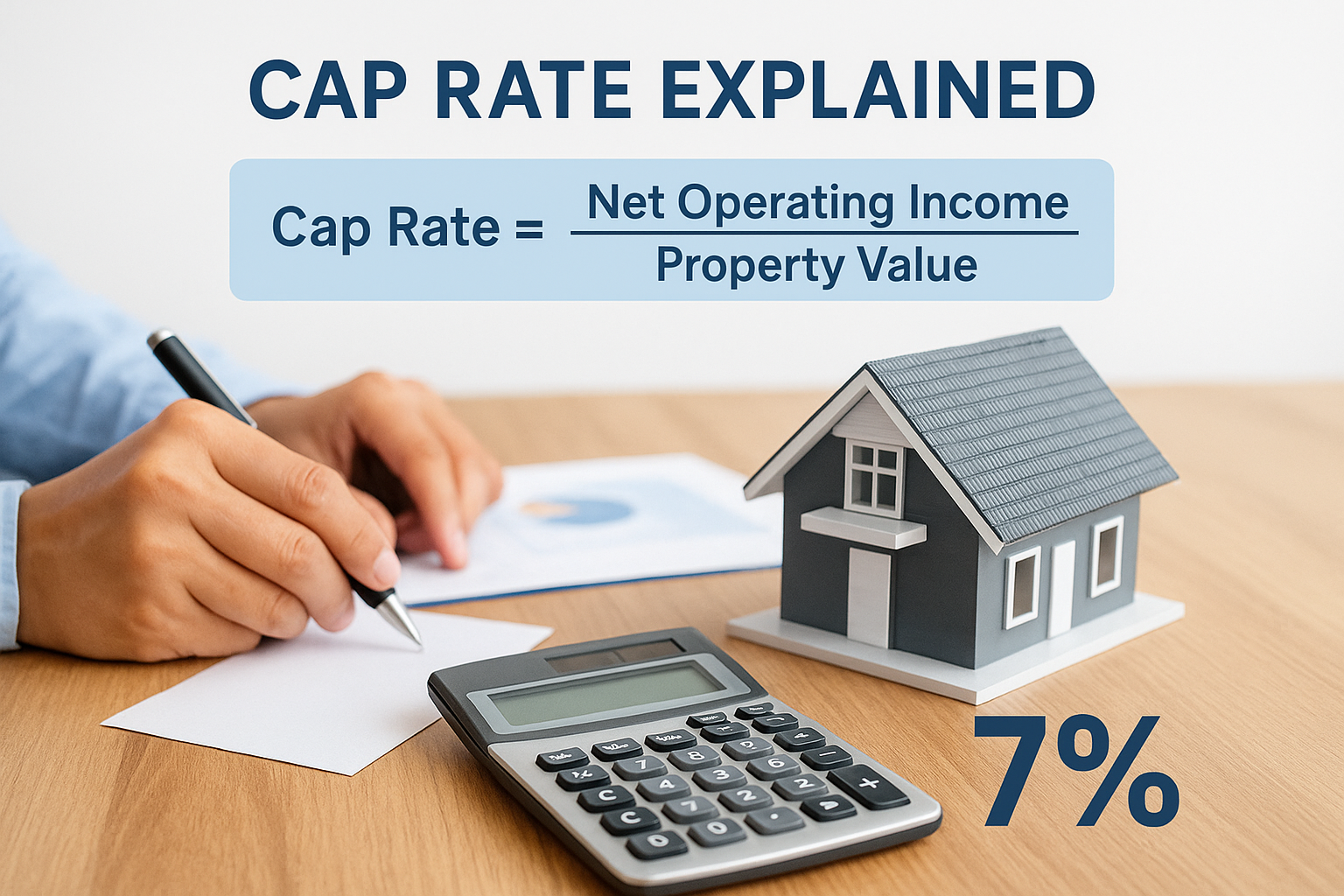

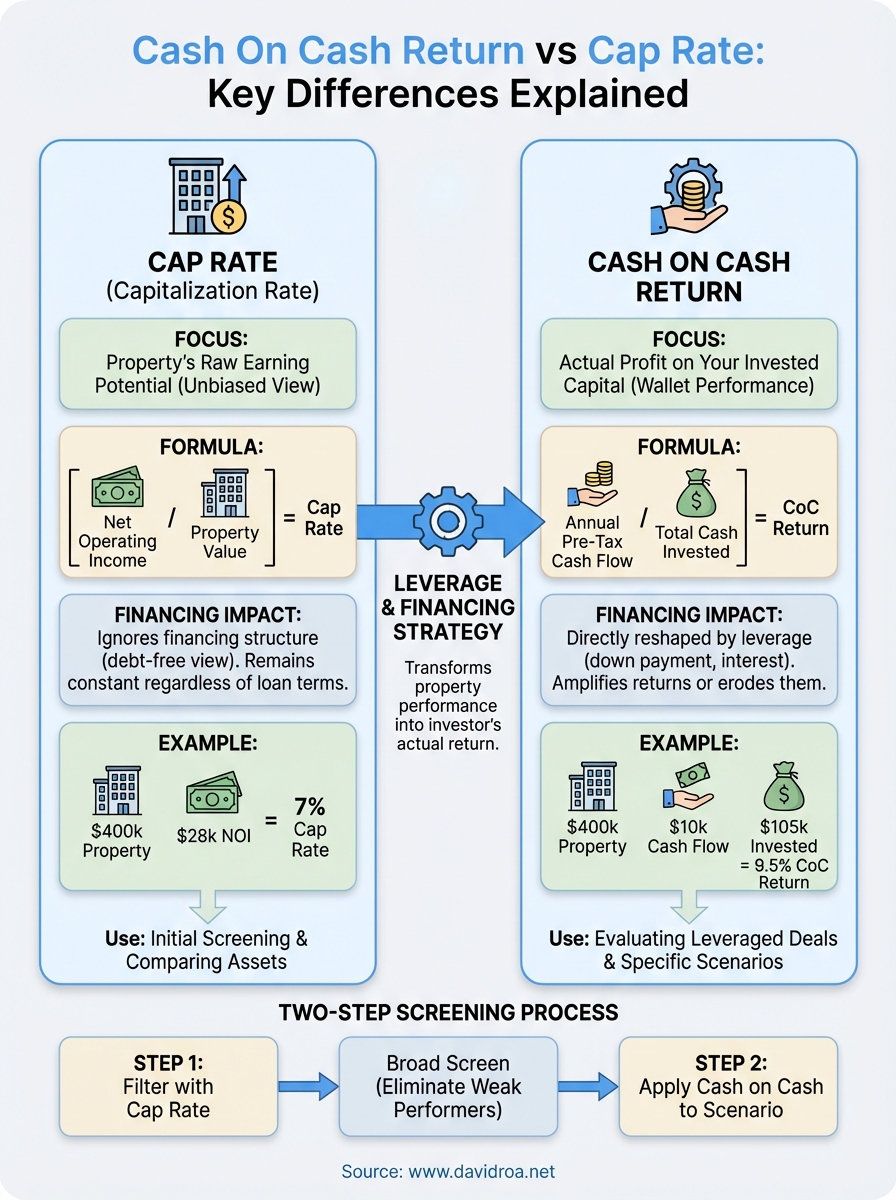

Cap rate explained with formula and example

Cap rate measures how much annual net operating income a property generates relative to its purchase price. This metric strips away financing complications and shows you the property's raw earning power. Investors use cap rate to compare different properties on equal footing, regardless of how those buildings get financed.

The formula is straightforward: Cap Rate = Net Operating Income / Property Value. Net operating income (NOI) equals your gross rental income minus operating expenses like property taxes, insurance, maintenance, and management fees. You exclude mortgage payments from this calculation because cap rate focuses solely on the property's performance, not your financing choices.

Cap rate gives you an unbiased view of asset performance before leverage enters the equation.

The cap rate formula in practice

Consider a $400,000 rental property that generates $40,000 in annual gross rents. Your operating expenses (taxes, insurance, repairs, management) total $12,000 per year. Your net operating income is $28,000 ($40,000 minus $12,000). Divide that $28,000 NOI by the $400,000 purchase price, and you get a 7% cap rate.

This 7% tells you what the building earns independent of financing. Whether you pay all cash, put down 20%, or structure a DSCR loan at 75% loan-to-value, the cap rate stays 7%. Understanding this baseline helps you evaluate if the property itself performs well before you layer in your personal financing strategy.

Cash-on-cash return explained with example

Cash on cash return measures your actual profit against the money you personally invested in a property. Unlike cap rate, this metric includes your financing costs and reveals what you earn on your down payment plus closing costs. Investors using leverage see the biggest gap between these two metrics.

The formula works like this: Cash on Cash Return = Annual Pre-Tax Cash Flow / Total Cash Invested. Your pre-tax cash flow equals net operating income minus your annual mortgage payments. Total cash invested includes your down payment, closing costs, and any immediate repairs or capital expenses you funded.

Cash on cash return shows your actual wallet performance after debt service, making it the critical metric for leveraged investors.

How leverage amplifies your returns

Take that same $400,000 property with $28,000 NOI from the cap rate example. You secure a DSCR loan at 75% loan-to-value, putting $100,000 down plus $5,000 in closing costs. Your annual mortgage payment totals $18,000. Your pre-tax cash flow becomes $10,000 ($28,000 NOI minus $18,000 debt service).

Divide that $10,000 by your $105,000 total investment, and your cash on cash return hits 9.5%. This exceeds the property's 7% cap rate because you're using the lender's money to amplify gains. The difference between cash on cash return vs cap rate shows exactly how leverage boosts your actual returns.

How financing changes cash-on-cash return and cap rate

Your financing structure leaves cap rate untouched but dramatically reshapes cash on cash return. This explains why the same property can deliver wildly different returns depending on your loan terms, down payment size, and interest rate. Understanding this relationship helps you structure deals that maximize your actual profits.

Cap rate remains independent of your financing

Cap rate ignores your mortgage because it measures the property's performance, not your payment structure. Whether you secure a DSCR loan at 7% interest or pay all cash, a building with $30,000 NOI and a $400,000 value maintains a 7.5% cap rate. This stability makes cap rate your baseline for comparing properties across different markets and financing scenarios.

Cap rate gives you the property's true earning power before debt service enters the picture.

Your loan terms directly reshape cash on cash return

Financing transforms cash on cash return through leverage and interest costs. A lower down payment means you invest less cash, potentially boosting your return percentage even after mortgage payments. However, higher interest rates can flip this advantage into a liability. When evaluating cash on cash return vs cap rate, you see exactly how your specific financing either amplifies or erodes the property's baseline performance. Smart investors run multiple scenarios with different loan structures to find the optimal leverage point.

How to use both metrics to screen deals fast

You screen deals efficiently by using cap rate first as your broad filter, then applying cash on cash return to your specific financing scenario. This two-step process eliminates properties that don't meet your baseline requirements before you waste time running detailed financing calculations. Most successful investors establish minimum thresholds for both metrics based on their market and investment strategy.

Start with cap rate to filter properties

Cap rate gives you a quick comparison tool across multiple properties without calculating individual financing terms. You set a minimum cap rate (often 6% to 8% for residential rentals, higher for commercial) and immediately eliminate listings below that threshold. This baseline screening happens in minutes because you only need the asking price and net operating income, both typically available in listing materials or easily estimated from rent rolls.

Cap rate filters out weak performers before you invest time analyzing financing scenarios.

Then apply cash on cash return to your scenario

After identifying properties that meet your cap rate minimum, you calculate cash on cash return using your actual financing terms. Run the numbers with your expected down payment percentage, interest rate, and loan structure like a DSCR loan or conventional mortgage. Understanding cash on cash return vs cap rate at this stage reveals which deals truly maximize your invested capital. Properties that clear both hurdles deserve deeper due diligence.

Final thoughts

Understanding cash on cash return vs cap rate gives you two lenses for evaluating every investment property. Cap rate shows you the asset's baseline performance independent of financing, while cash on cash return reveals your actual profit on invested capital. You need both metrics to make informed decisions, especially when leverage plays a role in your strategy.

Start your deal screening with cap rate thresholds to eliminate weak properties quickly. Then calculate cash on cash return using your specific financing scenario to find deals that maximize your actual returns. This two-step process saves you time and focuses your attention on opportunities that meet both performance baselines.

Your financing structure directly determines whether you amplify or erode a property's cap rate performance. If you're ready to explore DSCR loans, hard money financing, or conventional mortgages for your next investment property, connect with our team to structure deals that optimize your cash on cash returns while maintaining strong asset fundamentals.