Crest Capital Equipment Financing: Rates, Terms & Reviews

If you're a small or mid-sized business owner shopping for equipment financing, there's a good chance you've come across Crest Capital equipment financing during your research. They've built a reputation as a direct lender specializing in equipment loans and leases, and they market heavily to businesses looking for fast approvals and flexible terms. But is the reality as good as the pitch?

Before you commit to any lender, it pays to understand exactly what you're signing up for, the rate structures, the fine print on terms, and what actual borrowers say about working with them. As a mortgage broker owner and commercial lending professional with over 25 years in the financing industry, I've helped business owners at David Roa navigate equipment purchases, SBA loans, and working capital decisions. I've seen firsthand how choosing the wrong lender, or the wrong loan structure, can cost a business thousands of dollars over the life of a contract.

This article breaks down Crest Capital's equipment financing program in detail: what they offer, who qualifies, how their rates and terms compare, and what their customer reviews actually reveal. Whether Crest Capital ends up being the right fit or you'd benefit from exploring other options, you'll walk away with the information you need to make a confident, well-informed decision for your business.

What Crest Capital equipment financing covers

Crest Capital positions itself as a direct equipment lender, meaning they fund deals from their own balance sheet rather than brokering your application to a third party. That matters because it gives them more control over approvals and funding speed. Understanding the scope of what they finance, and what they won't touch, is the first thing you need to nail down before you invest time in an application.

Types of equipment they finance

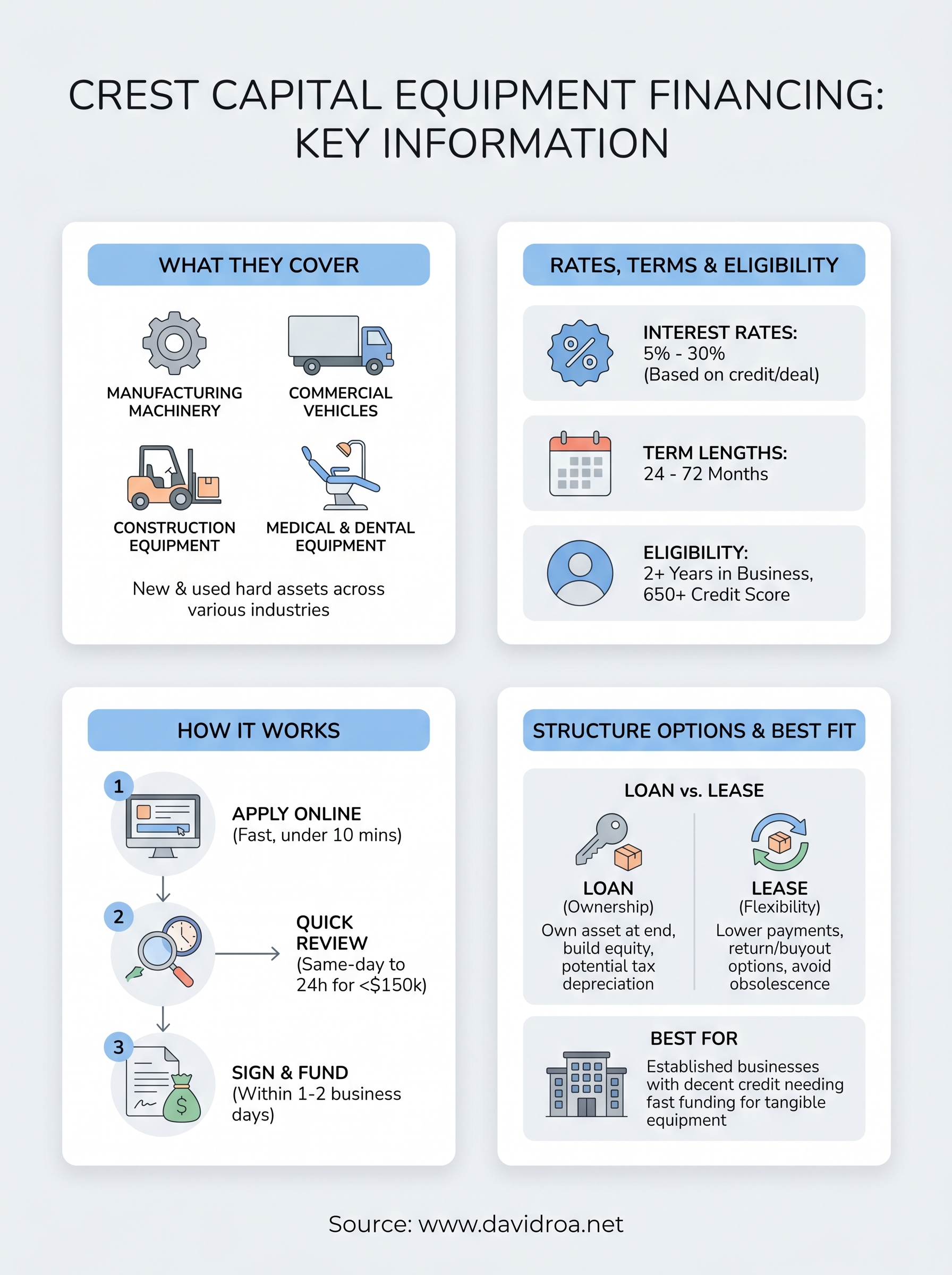

Crest Capital equipment financing covers a broad range of business-use assets, which is one of the reasons they attract borrowers from so many different industries. They fund both new and used equipment, and their model leans heavily toward hard assets: things that hold identifiable value and can serve as collateral for the loan or lease.

Here are the main equipment categories they typically finance:

- Manufacturing and production machinery: CNC machines, presses, conveyors, and industrial tools

- Commercial vehicles: trucks, trailers, vans, and fleet vehicles used for business

- Construction equipment: excavators, loaders, forklifts, and earthmoving machines

- Medical and dental equipment: diagnostic imaging, dental chairs, laser systems, and lab equipment

- Restaurant and food service equipment: commercial ovens, refrigeration units, and prep stations

- Technology and IT hardware: servers, networking gear, and point-of-sale systems

- Office furniture and fixtures: modular workstations, phone systems, and AV equipment

One practical note: Crest Capital generally does not finance software on its own or working capital needs, so if your purchase is primarily digital or service-based, you will likely need a different financing product.

Industries they serve

Crest Capital works with businesses across dozens of industry verticals, which gives their platform flexibility most bank-based lenders can't match. You'll find their programs used heavily in healthcare, construction, transportation, food service, and professional services. They do not restrict financing to a single sector, which means whether you run a dental practice or a logistics company, your equipment type likely fits within their scope.

Industry-specific experience matters in equipment lending because lenders need to understand residual asset values, useful life, and depreciation curves for the equipment they're securing. Crest Capital's focus on equipment-only financing means their underwriters are generally more comfortable assessing a wide variety of asset types compared to a generalist bank lending officer.

Loan and lease amounts

Crest Capital works with financing amounts ranging from $5,000 up to $500,000 per transaction, which makes them accessible for smaller purchases like a single commercial appliance while still accommodating mid-market equipment acquisitions. Deals above $500,000 may require additional underwriting or may fall outside their standard program, so if your purchase exceeds that ceiling, you will want to confirm eligibility before applying.

Their programs are structured as either equipment loans (where you own the asset outright after making all payments) or equipment leases (where you make periodic payments for use of the asset with options at the end of the term). This distinction carries real financial implications for your balance sheet, tax treatment, and end-of-term flexibility, which is something worth discussing with a lending professional before you choose a structure. The right option depends on your cash flow, how long you plan to use the equipment, and whether ownership or flexibility matters more to your business at this stage.

Rates, terms, fees, and total cost

Understanding what Crest Capital equipment financing actually costs you is more involved than just looking at a quoted interest rate. The total cost of a financing deal includes your rate, your term length, origination fees, and any end-of-lease charges that apply to your specific agreement. Before you sign anything, you need to see the full picture.

Interest rates and APR range

Crest Capital does not publish a fixed rate table on their website, which is common among equipment lenders because rates are tied to your credit profile, time in business, equipment type, and deal size. Based on publicly available reviews and borrower disclosures, rates on equipment loans and leases through Crest Capital generally fall in the 5% to 30% range, with the most competitive rates reserved for businesses with strong credit history, two or more years in operation, and clean financial records. Startups or borrowers with bruised credit should expect rates closer to the upper end of that range.

If a lender quotes you a monthly payment without disclosing the APR upfront, always ask for the full cost-of-capital figure before you agree to anything.

Term lengths available

Crest Capital structures most transactions on terms ranging from 24 to 72 months, though the specific options available to you will depend on what you're financing and how much you're borrowing. Shorter terms mean higher monthly payments but less total interest paid over the life of the deal. Longer terms reduce your monthly cash outflow but increase what you pay in total. Matching your repayment term to the useful life of the equipment is one of the most practical ways to avoid paying off a lease on gear that's already worn out.

Fees and additional charges

Crest Capital charges an origination or documentation fee, which typically ranges from $150 to $250 depending on the deal. For lease structures, you may also encounter an end-of-term buyout fee if you choose to purchase the equipment rather than return or renew. Late payment fees apply on most agreements, so reviewing the payment terms in your contract before signing protects you from unnecessary charges. Ask specifically about prepayment penalties as well, since some equipment financing contracts include them.

Eligibility requirements and needed documents

Before you spend time filling out an application, you need to confirm that your business actually meets the baseline standards Crest Capital equipment financing uses to evaluate borrowers. Their requirements are more accessible than what a traditional bank would demand, but they still apply a credit-based underwriting model, so preparation matters.

Credit score and time in business

Crest Capital targets established businesses with a minimum credit score of around 650, though some programs may accommodate scores slightly below that threshold depending on the deal structure and equipment type. Your personal credit score carries significant weight in the approval decision, especially for smaller businesses where the owner and the company are financially intertwined. In addition to your credit score, Crest Capital generally requires that your business has been operating for at least two years. If you're a startup or have less than two years of history, your options within their platform become limited.

The stronger your credit profile going in, the more leverage you have to negotiate on rate and term, so pulling your credit report before you apply is always a smart move.

Your annual revenue and cash flow also factor into underwriting. Crest Capital wants to see that the business generates enough income to handle the new monthly payment without strain. There is no publicly stated minimum revenue figure, but reviewers and borrowers consistently note that deals go smoother when annual revenue is at least $100,000.

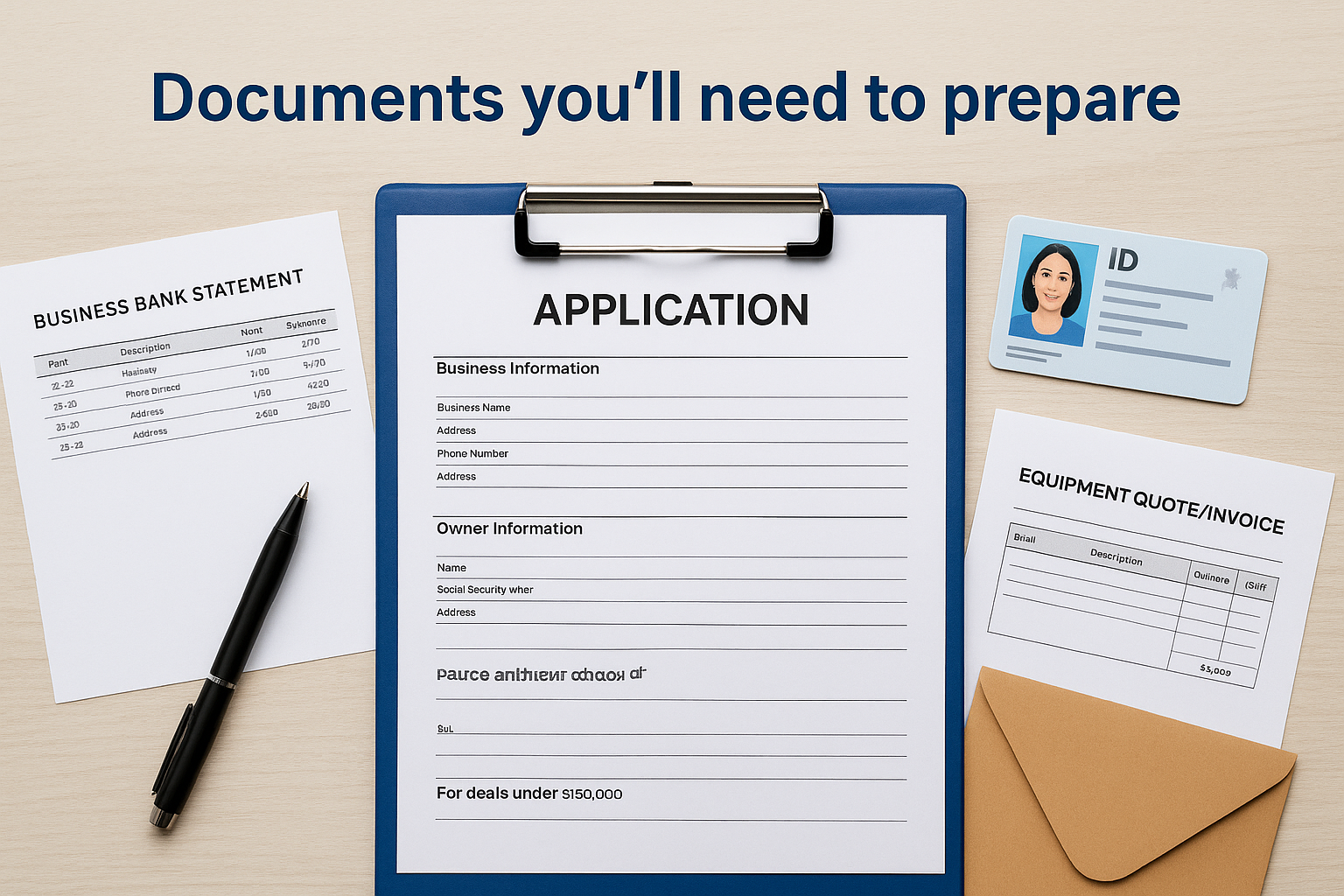

Documents you'll need to prepare

Crest Capital keeps their documentation requirements lean compared to a full bank underwrite, but you still need to come prepared. Having these materials ready before you start speeds up the process and reduces back-and-forth delays.

Here is what you should have on hand:

- Completed application: Basic business and ownership information, including your EIN and personal Social Security number

- Business bank statements: Typically the most recent three to six months to verify cash flow

- Government-issued ID: A valid driver's license or passport for the primary business owner

- Equipment quote or invoice: A detailed description of what you're financing, including vendor name and purchase price

- Business financials: For larger deals, tax returns or profit-and-loss statements may be required to support the application

For deals under $150,000, Crest Capital often operates on a streamlined approval process that requires minimal documentation beyond the application and bank statements.

How to apply and what happens after approval

The application process for Crest Capital equipment financing is designed to move quickly, and that speed is one of the main reasons borrowers choose them over traditional bank lenders. Most applicants can complete the initial application in under 10 minutes online, and the platform is built for business owners who can't afford to spend days assembling paperwork just to get a decision.

Submitting your application

You start by visiting Crest Capital's website and completing their online application form. The form collects basic business details such as your legal business name, time in operation, and estimated annual revenue. You'll also enter your personal information and Social Security number since personal credit plays a central role in their underwriting model. Attaching your equipment quote or invoice at the same time, along with recent bank statements, speeds the review and cuts down on the back-and-forth that typically slows approvals.

What happens during the review

Once you submit, Crest Capital's underwriting team reviews your file and pulls a credit check. For deals under $150,000, this review generally takes same-day to 24 hours, which is one of their more practical advantages compared to bank lenders that require days or weeks just to acknowledge an application. Larger transactions or applications with more complicated credit histories take longer to process, so setting realistic expectations going in prevents unnecessary frustration.

Approval speed depends largely on how complete your application is when you submit it, so having your documents organized before you start saves meaningful time.

After approval: signing and funding

After the approval decision comes through, Crest Capital sends you a full contract with your loan or lease terms clearly outlined. Read through the entire document before you sign anything. Pay close attention to your rate, repayment schedule, any applicable fees, and the end-of-term conditions on lease agreements, particularly if you plan to buy the equipment outright at the end.

Once you sign and return the agreement, funding typically arrives within one to two business days, either by direct deposit to your account or as a payment sent directly to your equipment vendor. If anything in the contract differs from what you discussed during the application process, ask for clarification before you commit.

Understanding Crest Capital loan and lease options

When you dig into Crest Capital equipment financing, you'll find that one of the most important decisions you make isn't just about rate or term. It's about choosing the right financial structure for your situation. Crest Capital offers both equipment loans and equipment leases, and while both put equipment in your hands, they work differently and carry real implications for your taxes, balance sheet, and options at the end of the contract.

Equipment loans: ownership from day one

With an equipment loan, Crest Capital lends you the purchase price of the equipment, and you take legal ownership immediately. The equipment serves as collateral for the debt, which means if you default, the lender can repossess it. Your monthly payments cover principal plus interest, and once you make your final payment, the asset belongs to your business free and clear.

This structure works well when you want to build long-term equity in a durable asset, plan to use it for many years, or need to carry it on your balance sheet. Loans also let you depreciate the asset over time under IRS rules, which can reduce your taxable income during the repayment period. If the equipment holds its value and plays a permanent role in your operations, a loan structure typically costs you less over time than a lease.

If you're unsure how equipment ownership affects your tax picture, talk to a CPA before you choose between a loan and a lease structure.

Equipment leases: flexibility over ownership

A lease means you pay for the right to use equipment over a defined period rather than purchasing it outright. At the end of the term, your agreement will typically give you the option to buy the equipment at a set price, return it to Crest Capital, or renew the lease. This structure suits businesses that rely on technology or tools that become outdated quickly, since you're not locked into owning gear that may lose practical value before the contract ends.

Leases often carry lower monthly payments than a loan for the same equipment, which helps preserve operating cash flow in the near term. That said, you don't build equity during the lease, and if you renew multiple times or exercise a buyout at the end, the total cost of the transaction can exceed what a straight purchase loan would have run you. Always model out both structures before you commit.

When Crest Capital makes sense and alternatives

Crest Capital equipment financing fits a specific type of borrower well, and knowing whether you fall into that category saves you time and protects your credit from unnecessary hard pulls. The platform works best when you have an established business with decent credit, a clear equipment purchase in mind, and a need for a decision faster than a bank can provide.

When Crest Capital is the right fit

Your strongest case for using Crest Capital is when you run a business with at least two years of operating history, a credit score above 650, and you're financing a tangible, hard asset that falls squarely within their coverage categories. If you need funds in hand within days rather than weeks, their streamlined approval process for deals under $150,000 is a real advantage. Business owners in manufacturing, construction, healthcare, and food service tend to get the most straightforward experience with their platform because those equipment categories fit neatly into their underwriting model.

Crest Capital also suits borrowers who want to keep the process simple without going through the full documentation burden of a bank loan.

The structure also works well if you value a direct lender relationship and prefer working with a company that funds the deal themselves rather than shopping your application to multiple sources. That directness typically means more predictable terms and a single point of contact from approval through funding.

When to look at other options

If your credit score falls below 620, your business is less than two years old, or you need financing above $500,000, Crest Capital may not be the right starting point. In those situations, exploring SBA 7(a) loans or SBA 504 programs gives you access to government-backed capital with longer terms and lower rates for qualified borrowers. The SBA route requires more documentation and takes longer to close, but the cost of capital is often meaningfully lower for deals that qualify.

For real estate investors or business owners who need asset-based financing tied to cash flow rather than personal credit, DSCR loans and commercial bridge products may serve your situation better than a traditional equipment lease or loan. Working with a lender who understands the full picture of your financial position, rather than one product in isolation, helps you make the choice that actually fits your business goals.

Final takeaways

Crest Capital equipment financing works well for established businesses that need a fast decision on a tangible asset purchase and can meet the credit and time-in-business thresholds. Their direct lending model, streamlined approvals, and broad equipment coverage make them a practical option for business owners who qualify. That said, their rates vary widely, and the total cost of the deal depends heavily on your credit profile, term length, and whether you choose a loan or lease structure.

Before you apply anywhere, take time to understand your full financial picture. If your credit needs work, your deal is above $500,000, or you'd benefit from an SBA-backed program with longer terms, you likely have better options available. Getting the right structure from the start saves you real money over the life of the contract. If you want guidance on which financing path fits your business, reach out to a commercial lending expert at David Roa before you commit.