Current FHA Loan Rates: Today’s Averages, APRs & Factors

FHA loans remain one of the most accessible paths to homeownership, especially for first-time buyers and those with modest credit histories. But before you commit, you need to know where current FHA loan rates stand and how they stack up against other options. Rates shift daily based on market conditions, and even a fraction of a percentage point can mean thousands of dollars over the life of your loan.

With over 25 years of experience funding more than $150 million in mortgages, I've helped countless buyers navigate FHA financing, from understanding rate quotes to closing on time. This guide breaks down today's average FHA rates and APRs, explains the factors that influence what you'll actually pay, and shows you how to position yourself for the best possible terms. Whether you're comparing lenders or just starting your research, you'll walk away with the numbers and context you need to make a confident decision.

What FHA loan rates mean and why they matter

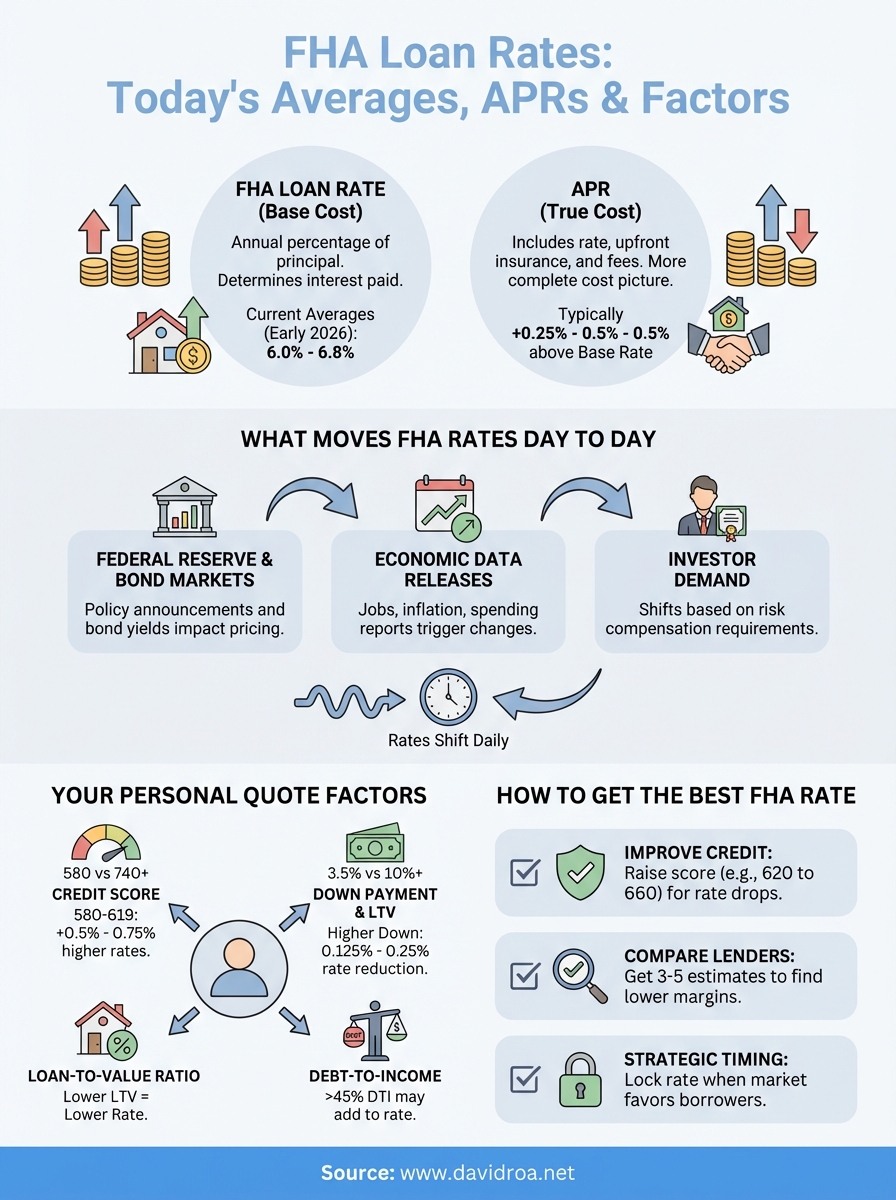

Your FHA loan rate is the annual cost of borrowing, expressed as a percentage of your principal balance. It determines how much interest you'll pay on top of the home price over the course of your mortgage term. Unlike conventional loans that often require 20% down and strong credit, FHA loans allow you to qualify with as little as 3.5% down and scores as low as 580, making them a popular choice for buyers who don't fit traditional lending boxes.

Why the interest rate determines your total cost

The rate you lock in directly controls your monthly payment and lifetime interest expense. On a $300,000 FHA loan at 6.5%, you'll pay roughly $1,896 per month in principal and interest. Drop that rate to 6%, and your payment falls to around $1,799, saving you nearly $100 monthly and over $35,000 across a 30-year term. Even small rate differences compound dramatically over time, which is why tracking current FHA loan rates matters before you commit to a lender.

A single percentage point difference can shift your total repayment by tens of thousands of dollars.

How FHA rates compare to conventional loans

FHA rates typically run slightly lower than conventional rates for borrowers with similar credit profiles, especially if your score sits below 700. This happens because FHA loans carry government insurance that protects lenders from default, reducing their risk and allowing them to price more competitively. However, you'll pay mortgage insurance premiums (both upfront and monthly) that can offset some of the rate advantage, so you need to compare total monthly costs, not just the interest rate itself, when evaluating your options.

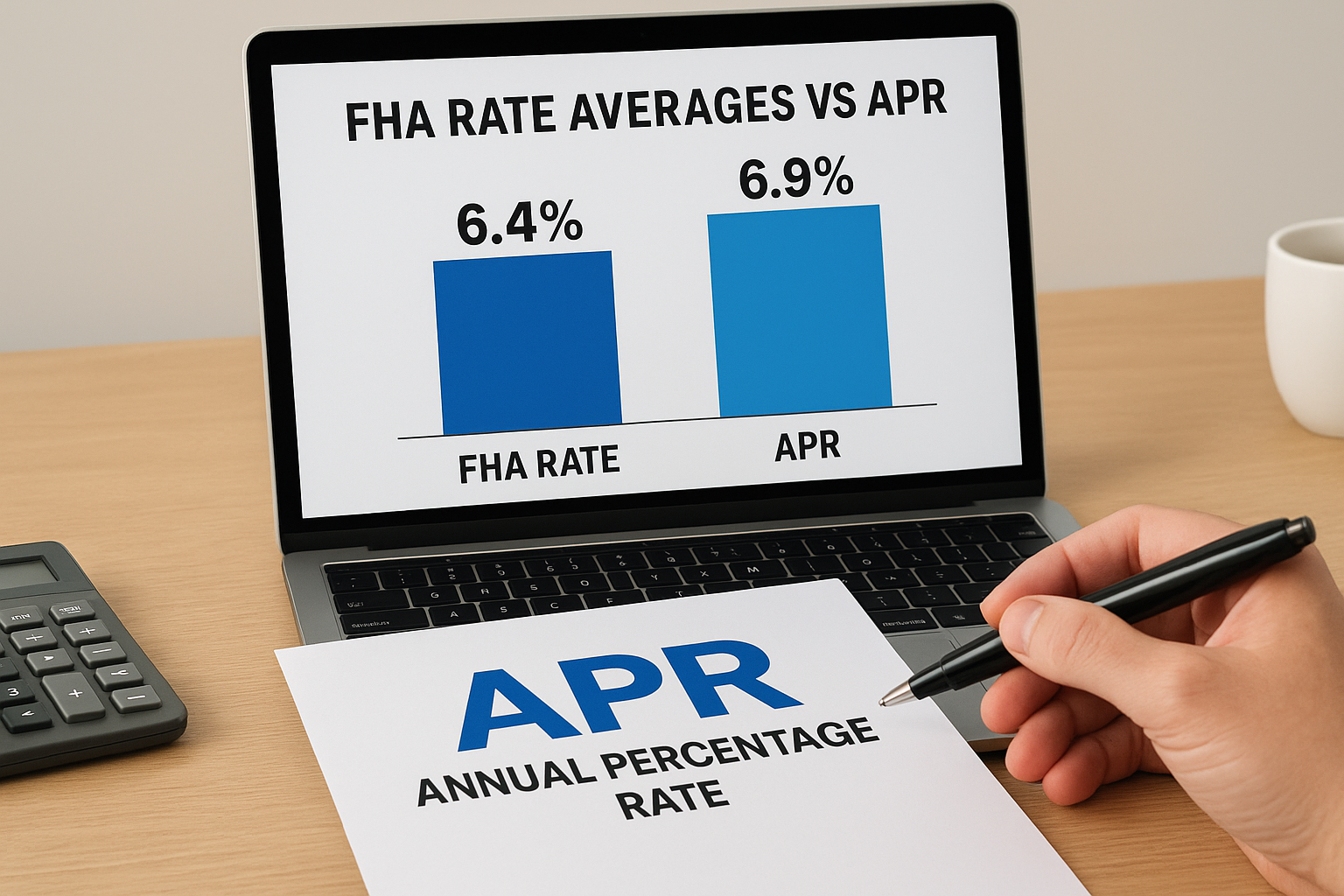

Today's FHA rate averages vs APR and what to track

As of early 2026, current FHA loan rates hover between 6.0% and 6.8% for 30-year fixed mortgages, depending on your credit profile and lender. These rates shift daily based on broader economic signals, so what you see quoted today may differ from what you lock in next week. The annual percentage rate (APR) runs higher, typically 0.25% to 0.5% above the base rate, because it includes your upfront mortgage insurance premium, closing costs, and other fees amortized over the loan term.

What APR reveals about your true cost

APR gives you a more complete picture of borrowing expenses than the interest rate alone. For example, a 6.5% FHA rate with a 6.85% APR means you'll pay roughly $3,850 annually in fees spread across your loan, on top of standard interest. You should compare APRs across lenders to identify who's padding quotes with hidden charges versus offering transparent pricing.

APR accounts for every mandatory cost, not just your base interest rate.

Tracking both numbers helps you spot lenders who advertise low rates but bury costs in upfront fees or inflated insurance premiums. Always request side-by-side APR comparisons when shopping for your FHA loan, and ask lenders to break down what drives the difference between their rate and APR.

What moves FHA rates day to day

Current FHA loan rates respond to three primary forces: Federal Reserve policy decisions, bond market activity, and incoming economic data. Lenders adjust pricing multiple times daily based on how these factors shift investor demand for mortgage-backed securities. When demand for bonds increases, yields drop and mortgage rates follow downward. When uncertainty spikes or inflation fears grow, rates climb as investors require higher returns to compensate for risk.

Federal Reserve policy and bond markets

The Federal Reserve controls short-term interest rates, but its policy announcements ripple through long-term mortgage pricing by signaling where inflation and economic growth are headed. When the Fed raises rates to cool inflation, current FHA loan rates typically rise within days. The 10-year Treasury yield serves as the benchmark for mortgage pricing, and lenders track this number hourly to adjust their rate sheets.

Bond market volatility can swing mortgage rates by half a percentage point in a single week.

Economic data releases

Monthly reports on employment, inflation, and consumer spending trigger immediate rate changes. Strong jobs numbers or rising consumer prices often push rates higher because they suggest the Fed may need to keep borrowing costs elevated. Weak data can lower rates as investors anticipate slower growth and potential Fed rate cuts.

What changes your FHA rate quote

While current FHA loan rates reflect national averages, your personal quote depends on factors lenders use to price risk. Two borrowers applying on the same day can receive rate differences of one percentage point or more based on their individual financial profiles. Understanding these variables helps you anticipate where you'll fall within the rate spectrum and identify which factors you can improve before applying.

Credit score impact

Your credit score drives the biggest pricing variation between borrowers. Scores of 580 to 619 typically trigger rates 0.5% to 0.75% higher than what borrowers with 740+ scores receive. A borrower with a 600 score might see a 6.8% rate while someone at 760 gets quoted 6.0% on the same loan amount. Lenders price this way because lower scores statistically predict higher default rates, and they pass that risk through as higher interest charges.

Every 20-point credit score increase can save you $30 to $50 per month in interest.

Loan-to-value ratio and down payment

Your down payment percentage affects your rate through loan-to-value (LTV) calculations. Put down 10% instead of the FHA minimum 3.5%, and you'll often qualify for a 0.125% to 0.25% rate reduction. Higher equity reduces lender exposure, especially if home values decline shortly after closing. Debt-to-income ratio also matters, with ratios above 45% sometimes adding 0.125% to your quoted rate depending on the lender's pricing matrix.

How to get the best FHA rate for your profile

Securing competitive current FHA loan rates requires strategic timing and preparation, not just submitting applications to the first lender who quotes you. You can improve your rate by boosting your credit score, shopping multiple lenders, and locking when market conditions favor borrowers. Each of these steps compounds your savings potential, and most take less time to execute than you'd expect.

Improve your credit before you apply

Raising your score from 620 to 660 typically lowers your rate by 0.25% to 0.375%, which translates to $45 to $70 monthly on a $300,000 loan. Pay down credit card balances to below 30% utilization, dispute any reporting errors, and avoid opening new accounts for at least six months before applying. Small changes deliver measurable rate improvements when you cross pricing thresholds at 640, 680, and 720.

Lenders reprice at specific credit score tiers, so even a 10-point increase can unlock better rates.

Compare at least three lenders

Different lenders price FHA loans with varying margins above their base cost, so you'll often see rate spreads of 0.25% to 0.5% for identical borrower profiles. Request loan estimates from three to five lenders within a two-week window to compare APRs without harming your credit score through multiple inquiries.

Quick wrap-up

Understanding current FHA loan rates requires tracking both the interest rate and APR while recognizing that your personal quote depends on credit score, down payment, and market timing. Rates change daily based on Federal Reserve policy and economic data, but you control the factors that determine where you land within the pricing spectrum. Improving your credit score and comparing multiple lenders remain the most effective ways to secure competitive terms that save you thousands over your loan term.

FHA financing opens doors for buyers who don't fit conventional lending requirements, and knowing how rates work helps you time your application and choose the right lender. If you're ready to explore FHA loan options with transparent pricing and personalized guidance based on 25+ years of lending experience, connect with me to discuss your specific situation. I'll help you navigate rate quotes, qualify for the best terms your profile supports, and close on time without surprises.