DSCR Loan Pre Approval: Steps, Docs, And Timeline (2026)

Getting a DSCR loan pre approval before you start shopping for investment properties isn't just smart, it's the difference between closing a deal and losing it to another buyer. Unlike conventional loans that scrutinize your W-2s and tax returns, DSCR loans qualify you based on a property's rental income potential, which means the pre-approval process looks different from what most borrowers expect.

But that difference is exactly where confusion creeps in. What documents do you actually need? What credit score gets you through the door? How long does the whole thing take? These are the questions I hear daily from investors, both first-timers and those scaling portfolios, and the answers aren't always straightforward.

With over 25 years in mortgage lending and my own active real estate investment portfolio, I've walked hundreds of investors through DSCR pre-approvals at David Roa. This guide breaks down the exact steps, documentation requirements, and realistic timeline you need in 2026, so you can move fast when the right property hits the market.

What DSCR loan pre-approval really means

A DSCR loan pre-approval is a lender's written confirmation that you qualify for financing up to a specific loan amount, based on the property's projected rental income rather than your personal employment income. Most investors mistake this for a conventional pre-approval, where a lender reviews W-2s, pay stubs, and your personal debt-to-income ratio to determine borrowing power. With a DSCR loan, the property does the qualifying, which changes what the lender reviews, what documents you submit, and how that approval letter reads.

How it differs from a conventional pre-approval

When you apply for a conventional mortgage, the lender runs your employment history and personal income through automated underwriting systems like Fannie Mae's Desktop Underwriter. A DSCR pre-approval skips that process entirely. Instead, the lender evaluates your credit score, liquid reserves, and a projected market rent analysis to determine your borrowing capacity before you've even identified a specific property.

This makes the pre-approval letter property-agnostic at the start. You get approved for a loan amount and a property type, such as a single-family rental, a 2-4 unit building, or a short-term rental, and then when you find a deal, the lender runs that specific property's numbers through the DSCR formula: monthly gross rent divided by monthly PITIA (principal, interest, taxes, insurance, and HOA). Most lenders require a minimum DSCR of 1.0, meaning the rent covers 100% of the payment.

A DSCR of 1.25 or higher typically unlocks better interest rates and lower reserve requirements, so targeting properties with strong rent-to-payment ratios from the start puts you in a materially stronger position at the closing table.

What a pre-approval letter actually commits the lender to

A dscr loan pre approval letter is not a binding loan guarantee, and understanding that distinction protects you when you're negotiating under contract. The letter states that based on your credit profile and the information you've provided, the lender is prepared to fund a loan up to a certain amount, subject to property-level underwriting once you go under contract.

After you submit an accepted offer, the lender orders an appraisal that includes a market rent analysis. The appraiser estimates what the property would reasonably rent for in the current market, and that number determines whether the DSCR clears the lender's threshold. Two conditions consistently appear in DSCR pre-approval letters: the property must appraise at or above the purchase price, and the appraiser's market rent estimate must produce a qualifying DSCR ratio. If the rent estimate falls short, your options are to renegotiate the purchase price, increase your down payment to reduce the monthly obligation, or walk away and find a better-performing property. Knowing this before you make offers lets you build appropriate contingencies into your contracts and avoid a situation where your earnest money is at risk.

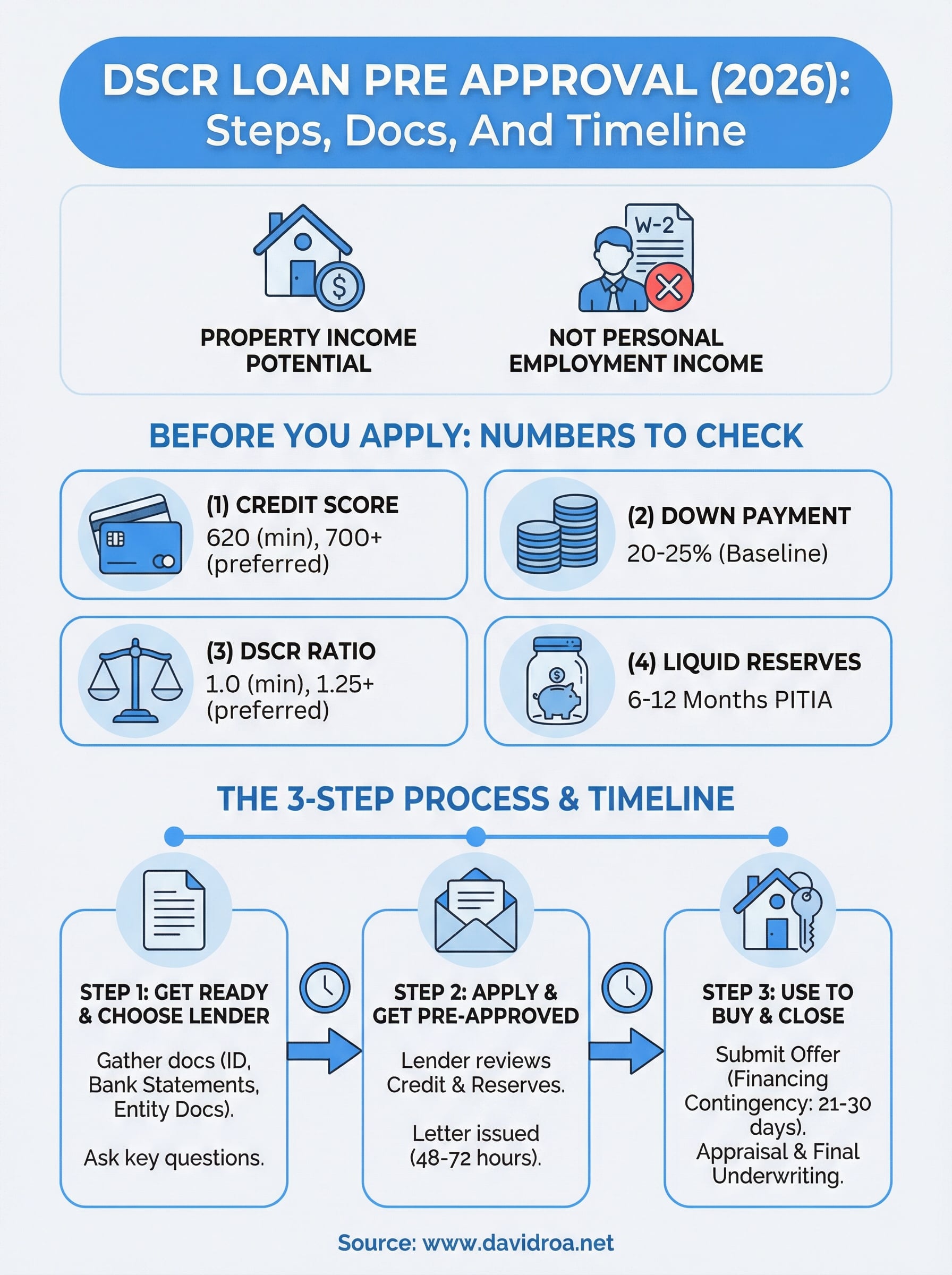

Before you apply: numbers and requirements to check

Before you submit anything to a lender, spend 20 minutes checking your numbers against standard DSCR loan pre approval thresholds. Walking in blind wastes time and can trigger unnecessary hard credit inquiries on your report. Most lenders publish their baseline requirements upfront, so use them as a filter before you start the formal process.

Credit score and down payment thresholds

Most DSCR lenders set a minimum credit score of 620, but anything below 700 typically triggers higher interest rates and stricter reserve requirements. Pull your credit report through AnnualCreditReport.com, the federally mandated free source, before you apply so you know exactly where you stand and can dispute any errors well in advance.

On the down payment side, plan to bring at least 20% to 25% of the purchase price to closing. Some lenders allow 15% for strong borrowers with a DSCR above 1.25, but 20% is the practical baseline to build your budget around. A larger down payment reduces your monthly PITIA, which directly improves your DSCR ratio on every deal you evaluate.

Running the DSCR formula on your target property before you apply, monthly gross rent divided by monthly PITIA at your expected loan amount, tells you immediately whether that deal will qualify.

| Requirement | Minimum Threshold | Preferred Range |

|---|---|---|

| Credit Score | 620 | 700+ |

| Down Payment | 15% (select lenders) | 20-25% |

| DSCR Ratio | 1.0 | 1.25+ |

| Liquid Reserves | 6 months PITIA | 12 months PITIA |

Liquid reserves you need in the bank

Reserves are the funds remaining in your accounts after your down payment and closing costs are paid. DSCR lenders typically require 6 to 12 months of the subject property's PITIA sitting in liquid accounts such as checking, savings, or money market accounts. Retirement accounts often count at 60% to 70% of their stated value.

Scaling investors face an additional layer here. Some lenders calculate required reserves across your entire rental portfolio, not just the new property you're purchasing. Confirm this policy with your lender before you formally apply so you're not caught short during underwriting.

Step 1. Get your file ready and choose a lender

Starting your dscr loan pre approval with a clean, organized file cuts processing time significantly and signals to lenders that you're a serious borrower. Most investors drag this step out by gathering documents reactively, one at a time, as lenders request them. Pulling everything together before your first conversation with any lender puts you in control of the timeline from the start.

Documents to pull together

DSCR lenders don't ask for W-2s or employment records, but they do need a specific set of documents to verify your credit profile and financial standing. Have these ready before you contact anyone:

- Government-issued photo ID (driver's license or passport)

- Two months of bank statements for every account you'll use to demonstrate reserves

- Mortgage statements for any properties you currently own

- Proof of entity if purchasing under an LLC (articles of organization and operating agreement)

- 12 months of platform statements if applying based on short-term rental income from Airbnb or VRBO

If you're buying through an LLC, confirm with the lender upfront whether they require a personal guaranty, because most DSCR lenders do, and having your entity documentation organized from day one prevents unnecessary delays in underwriting.

How to evaluate lenders

Not every lender who advertises DSCR loans actually specializes in them, and the gap in turnaround time, pricing, and flexibility becomes a real problem when you're under contract with a hard deadline. Ask each lender three direct questions before you submit anything: What is your minimum DSCR ratio? What is your average time from application to pre-approval letter? Do you allow DSCR loans for short-term rentals?

A lender who answers those questions with specific numbers and without hesitation has the experience you need. One who hedges or says "it depends" without any explanation is likely processing DSCR loans through a workflow built for conventional borrowers, which creates friction at every stage of your transaction and puts your closing date at risk.

Step 2. Submit the application and get pre-approved

Once your file is organized, submitting your dscr loan pre approval application is straightforward, but understanding what happens on the lender's end prevents you from chasing updates that won't change anything yet. Most DSCR lenders process applications through a dedicated non-QM platform, and the initial review focuses on two things: your credit profile and your ability to fund both the down payment and reserves.

What the lender reviews during processing

The lender's processor pulls your credit report immediately after you submit, which is why fixing errors beforehand matters. They verify your bank statements to confirm that reserve funds are seasoned, meaning they've been in your account for at least 60 days, not just deposited the week before you applied. Large, unexplained deposits trigger follow-up questions and slow everything down.

Here's what a standard DSCR pre-approval review covers at this stage:

- Credit pull: Hard inquiry on all three bureaus to confirm score and existing debt obligations

- Reserve verification: Bank statements reviewed for balance consistency and fund seasoning

- Entity check: LLC documents reviewed if you're taking title in a business name

- Scenario analysis: Lender confirms which property types and DSCR ratios your profile supports

Most DSCR lenders issue a pre-approval letter within 48 to 72 hours of receiving a complete file, so submitting everything at once rather than piecemeal is the fastest path to your letter.

How to follow up without slowing things down

After you submit, send a single confirmation email to your loan officer asking them to acknowledge receipt and confirm that your file is complete. That one message surfaces any missing items immediately rather than letting them sit unnoticed for days. After that, give the processor 24 hours before you follow up again.

If you haven't received your pre-approval letter by the end of business on day three, ask your loan officer a direct, specific question: "Is the delay on your end or is there something missing from my file?" That question produces a concrete answer and keeps the process moving without creating friction in the relationship.

Step 3. Use pre-approval to buy and close on time

Your dscr loan pre approval letter is a tool, and how you use it during the purchase process determines whether you close on time or watch deals collapse in the final stretch. Most investors treat the letter as a formality and then get caught off guard when property-level underwriting introduces new conditions. Understanding the sequence from offer to closing lets you set realistic expectations with sellers and agents and keeps your earnest money protected throughout the transaction.

Making offers with your pre-approval letter

When you submit an offer, attach your pre-approval letter and include a financing contingency that gives you at least 21 to 30 days to complete underwriting. DSCR loans require an appraisal with a market rent analysis, which typically adds 5 to 10 business days to the appraisal timeline compared to a conventional purchase appraisal. Sellers in competitive markets may push back on longer contingency windows, but cutting this period too short puts you at risk if the appraiser's rent estimate triggers a condition that requires renegotiation.

If the appraisal comes in below the purchase price or the rent estimate produces a DSCR below 1.0, you have three options: renegotiate the price, increase your down payment, or exit the contract within your contingency period.

Keeping your closing on track

Once you're under contract, notify your loan officer immediately and submit the signed purchase agreement the same day. Delays at this stage push the appraisal order back, which compresses every remaining step in your timeline. Your lender will issue a formal Loan Estimate within three business days of receiving the purchase agreement, as required under federal RESPA guidelines.

From that point, respond to every underwriting condition within 24 hours. Conditions that sit unanswered for two or three days create cascading delays that can push your closing date back by a week or more. Keep your bank balances stable, avoid opening new credit accounts, and do not make any large deposits without a clear paper trail to document the source.

Next steps

You now have the complete picture of what a dscr loan pre approval actually requires, from checking your credit score and reserves before you apply, to organizing your documents, submitting a clean file, and using your approval letter strategically once you're under contract. The process is straightforward when you follow the steps in the right order and know what each stage demands from you.

The most common mistake investors make at this point is waiting. Markets move fast, and sellers consistently favor buyers who can attach a pre-approval letter to an offer on day one. Your next move is simple: pull your credit report today, run the DSCR formula on two or three properties you've been watching, and confirm your reserve balances. Once those numbers check out, you're ready to start the formal process.

Reach out to David Roa to get your pre-approval started with a lender who has funded over $150 million in investment real estate loans.