FHA Loan Income Requirements: Limits, DTI, And Documents

FHA loans are known for their flexible credit requirements and low down payments, but many borrowers wonder whether their income will qualify, or disqualify, them. Understanding FHA loan income requirements is essential before you start house hunting, because the rules differ from conventional mortgages in ways that can work to your advantage. The good news: there's no minimum or maximum income limit for FHA loans. The not-so-good news: your debt-to-income ratio and employment stability matter more than you might expect.

With over 25 years originating FHA loans and more than $150 million funded, I've helped hundreds of borrowers navigate these requirements, including self-employed buyers, ITIN holders, and first-time homebuyers who thought they didn't qualify. This guide breaks down exactly what lenders look for: DTI thresholds, documentation requirements, and the income verification process that determines whether you'll get approved.

Do FHA loans have income limits

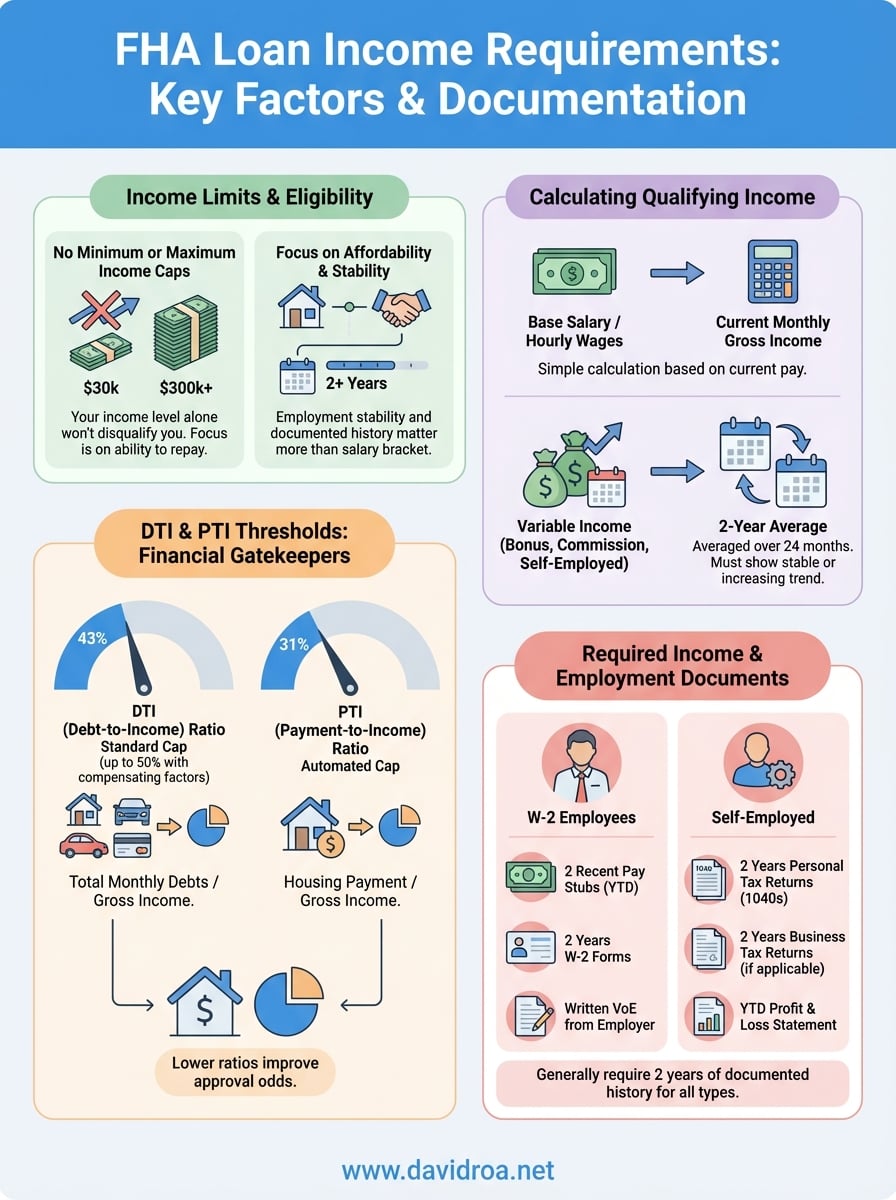

You won't find minimum or maximum income caps on FHA loans, which sets them apart from many other government-backed programs. The Federal Housing Administration designed these loans to help working Americans become homeowners, regardless of whether you earn $30,000 or $300,000 annually. Your income level alone won't disqualify you from FHA financing, but it does determine how much house you can afford and whether your debt load fits within acceptable ratios.

No minimum income requirement exists

FHA guidelines don't specify a floor for earnings, meaning you can qualify with modest wages as long as you meet other lending standards. I've closed loans for borrowers earning $2,500 per month and others bringing in $15,000 monthly. The key factor isn't the amount itself but whether your income is stable and documented through at least two years of employment history. Part-time workers, hourly employees, and commissioned sales professionals all qualify if they can prove consistent earnings over time.

FHA loans focus on your ability to repay, not your salary bracket.

No maximum income cap applies

Unlike USDA loans or certain state-specific programs, FHA financing doesn't cut you off at a certain earnings threshold. You could make $500,000 annually and still choose an FHA loan for its low down payment benefit or relaxed credit requirements. Many high earners select FHA products when they're rebuilding credit after a financial setback or want to preserve cash for other investments. The absence of an income ceiling makes these mortgages accessible across all economic levels.

What actually determines eligibility

Instead of income limits, lenders evaluate whether you can afford the monthly payment based on debt-to-income calculations and payment-to-income thresholds. Your gross monthly income must be sufficient to cover the new mortgage plus existing debts while staying within 43% DTI for standard approvals (or up to 50% with compensating factors). Employment stability matters more than the size of your paycheck. If you've worked steadily for two years and your income covers the projected housing costs, you meet the core fha loan income requirements regardless of whether you're a teacher earning $50,000 or a surgeon earning $400,000.

Lenders also scrutinize whether your income is likely to continue for at least three years after closing. This forward-looking requirement protects both you and the lender from approving a mortgage you can't sustain long-term.

How DTI and PTI shape FHA affordability

Your debt-to-income ratio and payment-to-income ratio act as the financial gatekeepers for FHA approval, determining whether lenders believe you can handle the mortgage payment alongside your existing obligations. These two metrics work together to measure affordability from different angles: DTI looks at your total monthly debts relative to gross income, while PTI focuses specifically on housing costs. Understanding both ratios helps you know whether you'll pass underwriting before you submit an application.

What DTI means for your approval

Lenders calculate your debt-to-income ratio by dividing all monthly debt payments (including the proposed mortgage, credit cards, car loans, student loans, and other obligations) by your gross monthly income. FHA guidelines allow up to 43% DTI for standard approvals, though some lenders push this to 50% or even 56.9% when you have compensating factors like substantial cash reserves or a low payment-to-income ratio. Every dollar you owe reduces your buying power, which is why paying down installment loans or credit card balances before applying can expand your approval amount significantly.

Your DTI directly controls how much house you can afford under FHA loan income requirements.

PTI sets the baseline payment threshold

Payment-to-income ratio measures only your new housing payment (principal, interest, taxes, insurance, and HOA fees) against gross monthly income, and FHA caps this at 31% for automated approvals. You can exceed this threshold with strong credit or significant reserves, but staying under 31% gives you the smoothest path through underwriting. If your projected housing payment hits 35% of your income while your total DTI sits at 42%, underwriters will scrutinize your financial stability more closely and may require additional documentation proving you can manage the higher payment burden without defaulting.

How lenders calculate qualifying income

Lenders don't simply look at your most recent paycheck or last year's tax return when evaluating fha loan income requirements. They follow specific formulas to calculate your qualifying monthly income, which determines your maximum loan amount and DTI ratio. The calculation method varies based on your income type, whether you're salaried, hourly, commissioned, self-employed, or receiving income from multiple sources. Understanding these formulas helps you predict your approval odds before you apply.

Base salary and hourly wages get the simplest treatment

Your lender divides your annual base salary by twelve to arrive at your gross monthly income. If you earn $60,000 yearly, your qualifying income sits at $5,000 per month. Hourly workers receive similar treatment, but underwriters multiply your hourly rate by the number of hours you work weekly, then multiply by 52 weeks and divide by 12 months. A full-time employee earning $25 per hour qualifies with $4,333 monthly income ($25 × 40 hours × 52 weeks ÷ 12 months).

Variable income requires two-year averaging

Bonuses, commissions, overtime, and self-employment income all get averaged over 24 months to establish a consistent baseline. Lenders pull your tax returns and W-2s for the past two years, add up the total variable earnings, and divide by 24 to calculate your monthly qualifying amount. If you earned $12,000 in bonuses last year and $18,000 the year before, your qualifying bonus income equals $1,250 monthly ($30,000 ÷ 24). This averaging protects both you and the lender from overestimating what you'll realistically bring home.

Your income must show a stable or increasing trend for lenders to count it toward qualification.

Declining variable income often gets excluded entirely from calculations, even if recent months looked strong. Underwriters scrutinize whether your earnings pattern suggests sustainable future income or temporary spikes that won't continue.

Income and employment documents you will need

Your lender will request specific documentation to verify the income you claimed on your application. These requirements aren't arbitrary - they help underwriters confirm that your earnings match what you stated and that you've maintained stable employment. The exact documents vary based on your employment type, but you can expect to provide at least two years of income history regardless of whether you're a W-2 employee or self-employed business owner.

W-2 employees need basic proof

Salaried and hourly workers provide the most straightforward documentation package for fha loan income requirements. Your lender will request your two most recent pay stubs showing year-to-date earnings, your W-2 forms from the past two years, and written verification of employment from your current employer. This verification typically arrives as a phone call or online confirmation that states your job title, hire date, salary, and whether your position is likely to continue. Some lenders also order an automated verification through The Work Number database, which pulls your employment and income data directly from your employer's payroll system.

Complete documentation upfront prevents delays during the underwriting process.

Self-employed borrowers face stricter documentation

Business owners, independent contractors, and freelancers must provide two years of personal tax returns (1040s with all schedules) and two years of business tax returns if you operate a partnership, S-corporation, or C-corporation. Your lender will also require a year-to-date profit and loss statement for your current business year, typically signed by a CPA if your net income exceeds certain thresholds. Schedule C filers should prepare to explain any large deductions that reduced your taxable income, since underwriters add back depreciation and certain business expenses when calculating your qualifying income.

Expect your CPA to play a role in preparing documentation that satisfies underwriting requirements while accurately representing your business income. Some lenders request business bank statements or a balance sheet to verify the financial health of your enterprise.

Common income snags and how to fix them

You can meet the basic fha loan income requirements but still hit roadblocks during underwriting when your income history contains irregularities or documentation gaps. These issues don't automatically disqualify you, but they force you to provide additional explanation and proof before your file can clear underwriting. Knowing the most frequent problems helps you address them proactively, whether you're still preparing to apply or already stuck in the approval process waiting for answers.

Job gaps and recent employment changes

Switching employers within six months of your application triggers additional scrutiny from underwriters, especially if you changed careers or moved from W-2 employment to self-employment. Your lender needs written confirmation that you've completed any probationary period at your new job and that your position is permanent rather than temporary or contract-based. You can overcome recent job changes by showing your move increased your income, kept you in the same field, or resulted from a corporate transfer rather than voluntary resignation. Provide offer letters, employment contracts, and detailed explanations of why you changed positions to help underwriters understand your situation.

Job changes that increase your income and demonstrate career advancement strengthen your application rather than weaken it.

Declining income trends raise red flags

Underwriters deny applications when your year-over-year earnings show a downward pattern without reasonable explanation. Self-employed borrowers face this issue most often, particularly when business deductions increased or revenue dropped in recent tax years. You fix declining income by providing a signed letter from your CPA explaining temporary circumstances that caused the dip, such as equipment purchases or market conditions that have since improved. Include current year-to-date profit and loss statements showing your income has rebounded to previous levels or exceeded past performance.

Missing documentation creates approval delays

Incomplete document packages account for most underwriting delays I see after 25 years originating loans. Your lender requests specific items for good reason, and partial responses force them to issue multiple document requests that push back your closing date. Gather every requested item before submitting anything, including all pages of tax returns, pay stubs showing year-to-date totals, and complete bank statements rather than screenshots or partial downloads.

What to do next

You now understand the fha loan income requirements that will shape your approval: no income limits exist, but your DTI ratio and employment stability determine whether you qualify for the home you want. Your next step involves gathering your income documentation before you start shopping for properties, which gives you a realistic picture of your buying power and prevents wasted time on homes outside your budget.

Start by pulling your most recent pay stubs, tax returns, and W-2s to calculate your own DTI ratio using the formulas outlined above. If your numbers fall within acceptable ranges, you're ready to speak with a lender who specializes in FHA financing and understands how to position your application for approval. Working with an experienced loan officer who has closed hundreds of FHA loans makes the difference between smooth sailing and repeated document requests that delay your closing.

Contact me directly to discuss your specific income situation and get pre-approved with confidence.