Investment Property Mortgage Calculator: Cash Flow & DSCR

Running the numbers before you buy a rental property isn't optional, it's the difference between building wealth and bleeding cash every month. An investment property mortgage calculator helps you estimate your monthly payment, but the real value comes when you layer in rental income, expenses, and metrics like DSCR (Debt Service Coverage Ratio) to see whether a deal actually works.

I've funded over $150 million in loans across residential, commercial, and investment properties over 25+ years as a mortgage broker and active real estate investor. I also flip properties myself, so I use these same calculations before every acquisition. The numbers either justify the deal or they don't, no amount of gut feeling replaces a clear cash flow projection.

In this guide, you'll get a full walkthrough of how to use a mortgage calculator built for investment properties, not just to estimate payments, but to evaluate cash flow, ROI, cap rate, and DSCR. Whether you're buying your first rental or adding to an existing portfolio, these are the exact metrics lenders and investors use to decide if a property is worth financing.

What you need before you start

Before you open an investment property mortgage calculator and start punching in numbers, gathering the right inputs matters as much as the math itself. Garbage in, garbage out is the most accurate way to describe what happens when you guess at figures. Lenders and underwriters will verify every number you submit, so the more accurate your inputs are upfront, the fewer surprises you'll face at closing.

Accurate data at this stage separates a deal you can defend to a lender from one that falls apart in underwriting.

Property details

You need specific facts about the property itself before any calculation makes sense. The purchase price sets your loan amount, and the property type (single-family, 2-4 unit, multifamily, etc.) affects which loan products you qualify for and what down payment is required. Pull the most recent property tax bill and confirm the figure directly with the county assessor's office rather than relying on a listing estimate.

Here's what to collect before you start:

- Purchase price or current appraised value

- Property type and number of units

- Annual property taxes (from the county assessor)

- Annual hazard insurance estimate (call your insurer directly)

- HOA fees, if applicable

- Current rent roll or comparable market rents from recent leases

Loan terms and financing

Your loan amount, interest rate, and loan term directly determine your monthly payment, so confirm these before you run any projections. Investment properties typically require a 15-25% down payment, and rates run 0.5-0.75% higher than primary residence loans. If you're comparing scenarios, note your credit score range as well, since it determines your rate tier and directly affects what a lender will approve.

Key loan inputs to have ready:

- Loan amount (purchase price minus your down payment)

- Interest rate (get an actual quote, not a national average)

- Loan term (15 or 30 years)

- Loan type (conventional, DSCR, hard money)

- Whether taxes and insurance will be escrowed

Operating expense estimates

Most investors underestimate ongoing operating costs, which skews cash flow projections and leads to real shortfalls mid-ownership. Budget for property management (8-12% of collected rent), maintenance and repairs (a standard baseline is 1% of purchase price per year), and vacancy (5-10% of gross annual rent). Collect these figures before running the full calculation so your output reflects what the property will actually cost to hold.

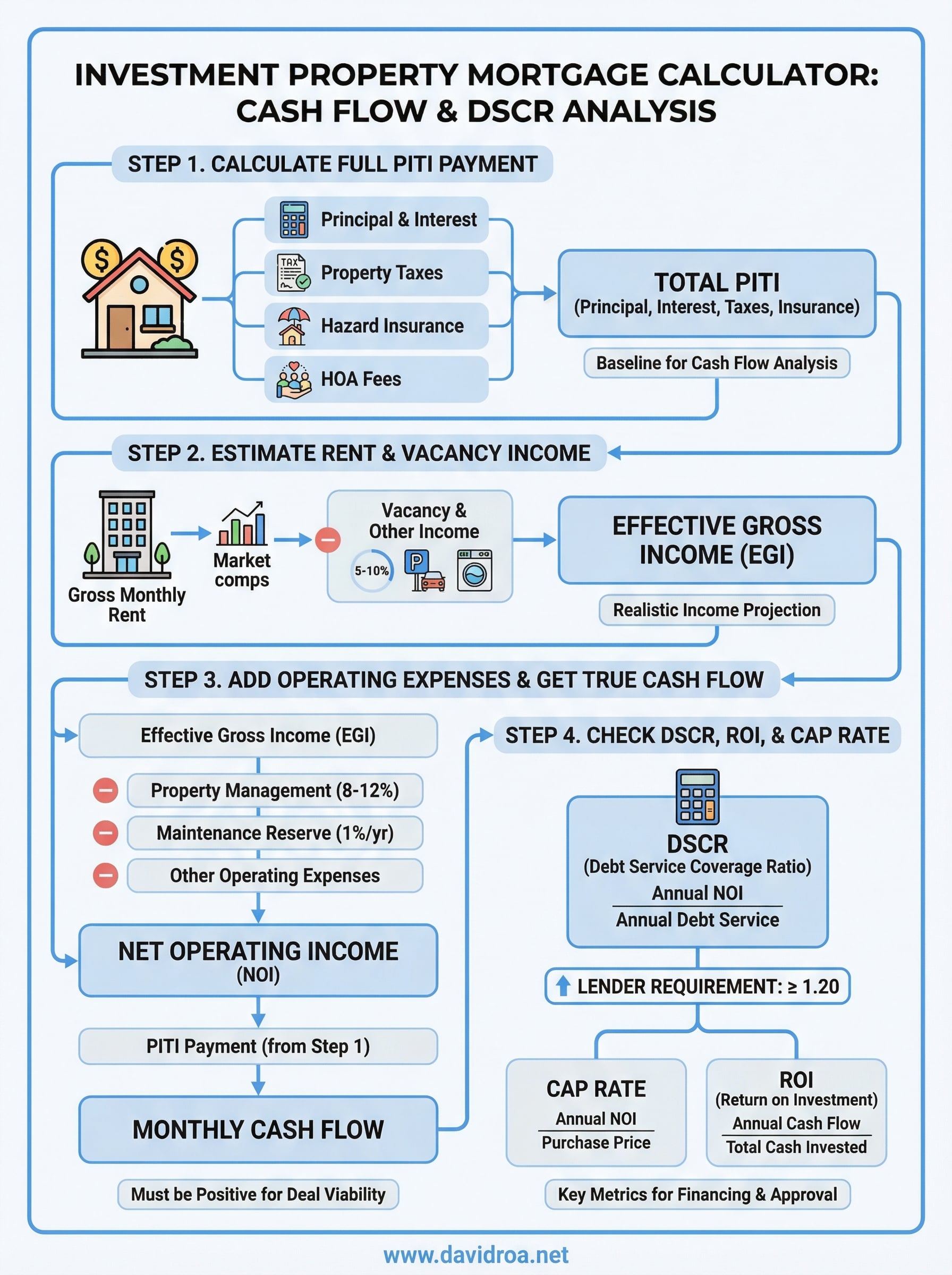

Step 1. Calculate your loan payment and full PITI

Your monthly mortgage payment is not just principal and interest. Full PITI (Principal, Interest, Taxes, and Insurance) is what you actually owe each month, and it's the figure every investment property mortgage calculator should use as the baseline for your cash flow analysis. Lenders use PITI, not just P&I, when evaluating your DSCR, so you need to work with the same number they will.

Calculate Principal and Interest First

The P&I portion of your payment comes from your loan amount, interest rate, and term. Use the standard amortization formula or any basic mortgage calculator to get this figure. For example, a $300,000 loan at 7.5% over 30 years produces a monthly P&I payment of roughly $2,098.

Getting an actual rate quote from a lender beats using a national average every time, because even a 0.25% difference changes your payment and your DSCR.

Add Taxes, Insurance, and HOA to Get Full PITI

Once you have your P&I, add the monthly cost of property taxes and hazard insurance to get your true PITI. Divide annual taxes and insurance by 12 to convert them to monthly figures. If there's an HOA, include that as well.

Here's a sample PITI breakdown for a $375,000 purchase with 20% down:

| Cost Component | Annual | Monthly |

|---|---|---|

| Principal & Interest | - | $2,098 |

| Property Taxes | $6,000 | $500 |

| Hazard Insurance | $1,800 | $150 |

| HOA | $600 | $50 |

| Total PITI | $2,798 |

Step 2. Estimate rent, vacancy, and other income

Your gross rental income is the starting point for every cash flow projection, but it's not the number you'll actually collect. Plugging raw rent into an investment property mortgage calculator without adjusting for vacancy and additional income gives you a distorted picture of what the property will actually produce each month. Getting this input right is what separates a realistic projection from wishful thinking.

Find Your Gross Monthly Rent

Before you project real income, you need a market-supported rent figure, not what a seller claims the property "should" rent for. Pull comparable active listings and recently signed leases for similar units in the same neighborhood. If the property is already occupied, confirm the rent against the current lease agreement rather than assuming it matches market rate. Use the lower of market rent or in-place rent to keep your projection conservative and defensible.

Use comps from within a half-mile radius and match on unit size, condition, and amenities for the most reliable rent estimate.

Adjust for Vacancy and Other Income

Vacancy reduces your effective income, and every rental property experiences it regardless of how strong the local market is. Apply a 5-10% vacancy factor by multiplying gross monthly rent by 0.90 to 0.95. Then add any supplemental income sources like parking, laundry, or storage fees to arrive at your Effective Gross Income (EGI), which is the figure you carry into your expense and cash flow calculation.

| Income Component | Calculation | Example |

|---|---|---|

| Gross Monthly Rent | Market rate x units | $2,200 |

| Vacancy (8%) | $2,200 x 0.92 | -$176 |

| Additional Income | Parking, laundry | +$100 |

| Effective Gross Income | $2,124 |

Step 3. Add operating expenses and get true cash flow

Operating expenses are where most first-time investors underestimate their true costs. Once you have your Effective Gross Income (EGI) from Step 2, you subtract all operating expenses to get your Net Operating Income (NOI), and then subtract your PITI payment to arrive at actual monthly cash flow. Any investment property mortgage calculator that skips this step gives you an incomplete picture.

Identify Every Operating Expense

Your operating expenses include everything it costs to run the property outside of your mortgage payment. Property management fees typically run 8-12% of collected rent. Set aside 1% of the purchase price annually for maintenance and repairs, split that by 12 for your monthly reserve. Also budget for utilities you cover as the landlord, landscaping, pest control, and any recurring costs tied to that specific property.

Underestimating expenses is the single most common reason investors end up cash-flow negative within the first year.

Calculate Net Operating Income and Cash Flow

Subtract your total monthly operating expenses from your Effective Gross Income to get NOI. Then subtract your full PITI payment from Step 1 to get your true monthly cash flow. Here's how that looks using the same example from the previous steps:

| Line Item | Monthly |

|---|---|

| Effective Gross Income | $2,124 |

| Property Management (10%) | -$212 |

| Maintenance Reserve (1%/yr) | -$313 |

| Other Operating Expenses | -$75 |

| Net Operating Income | $1,524 |

| PITI Payment | -$2,798 |

| Monthly Cash Flow | -$1,274 |

If your cash flow is negative at this stage, the deal needs renegotiation on price, terms, or both before you move forward.

Step 4. Check DSCR, ROI, and cap rate for approval

Your NOI and cash flow numbers tell you how the property performs, but lenders and investors use three specific ratios to decide whether the deal clears the bar for financing and acquisition. Running these calculations through an investment property mortgage calculator or manually lets you compare your deal against real approval thresholds before you submit a loan application.

Calculate Your DSCR

DSCR (Debt Service Coverage Ratio) measures whether the property generates enough income to cover its debt. Divide your annual NOI by your annual debt service (PITI multiplied by 12) to get the ratio. Most DSCR lenders require a minimum of 1.20, meaning the property earns 20% more than it costs to service the debt. A DSCR below 1.0 means the property operates at a loss and will not qualify for most investment loan programs.

A DSCR of 1.25 or higher gives you a cushion against vacancy spikes or unexpected repairs without triggering lender concern.

| Metric | Formula | Example |

|---|---|---|

| DSCR | Annual NOI / Annual Debt Service | $18,288 / $33,576 = 0.54 |

Calculate ROI and Cap Rate

Cap rate isolates the property's income performance independent of financing by dividing annual NOI by the purchase price. ROI (Return on Investment) reflects your actual cash-on-cash return by dividing annual cash flow by total cash invested, including your down payment and closing costs. Both metrics let you compare properties side by side on equal footing regardless of how each deal is structured.

| Metric | Formula |

|---|---|

| Cap Rate | Annual NOI / Purchase Price |

| ROI | Annual Cash Flow / Total Cash Invested |

Next steps

You now have a complete framework to run a real deal analysis, not just an estimate of your monthly payment. Every step in this guide builds on the last: your PITI sets the debt baseline, your EGI adjusts for vacancy, your NOI reflects true operating performance, and your DSCR determines whether a lender will finance the deal. If any ratio comes back short, adjust the purchase price, down payment, or expected rent before moving forward.

Run every property you evaluate through this investment property mortgage calculator process before you make an offer. Deals that look strong on paper often fail when you layer in real expenses and vacancy, so the numbers either hold up or they tell you to walk away. When your analysis shows a DSCR above 1.20 and positive monthly cash flow, you're ready to move toward financing. Connect with David Roa to get an actual rate quote and review your deal before you commit.