Jumbo Loan Definition: 2026 Limits, Rates, And How It Works

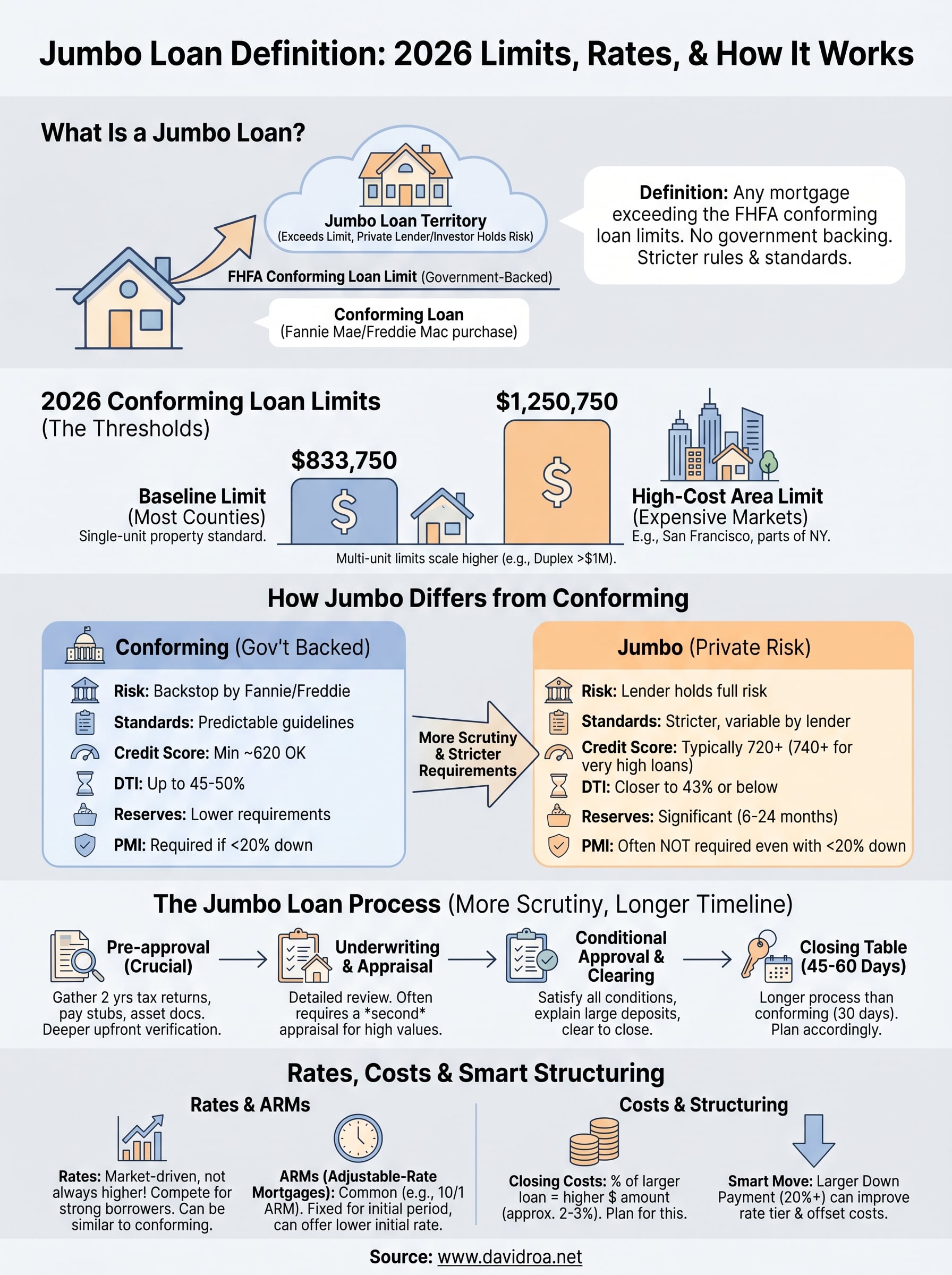

When the home you want costs more than what a conventional mortgage can cover, you enter jumbo loan territory. By jumbo loan definition, it's any mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA), and for 2026, that threshold matters more than ever as property values continue climbing across the country.

These loans exist for a reason: not every property fits inside a government-backed box. Whether you're buying a high-value home in the Chicago suburbs or investing in a luxury property elsewhere, a jumbo loan gives you the financing power to close on homes that conventional loans simply can't reach. But they come with stricter requirements, different rate structures, and underwriting standards that catch many borrowers off guard.

With over 25 years in mortgage lending and more than $150 million funded, I've guided buyers through the jumbo loan process across a wide range of scenarios, from primary residences to investment properties. In this article, I'll break down exactly what a jumbo loan is, the 2026 conforming loan limits that trigger it, current rate expectations, and what lenders actually look for when you apply.

What counts as a jumbo loan in 2026

A loan becomes a jumbo loan the moment it exceeds the conforming loan limit set each year by the Federal Housing Finance Agency (FHFA). That limit determines how large a mortgage Fannie Mae and Freddie Mac can purchase. Once your loan amount crosses that line, conventional financing no longer applies, and you move into jumbo territory with different rules, different underwriting, and different lender expectations. Understanding where that line sits in 2026 is the first step in knowing whether a jumbo product is what you actually need.

The baseline conforming loan limit

For most counties across the United States, the 2026 baseline conforming loan limit sits at $833,750 for a single-unit property. Any mortgage you take out above that number falls under the jumbo loan definition and must be funded through lenders who hold or privately sell those loans rather than packaging them for the government-sponsored enterprises. If your target home is priced at $900,000 with a 10% down payment, your loan amount would be $810,000, which puts you firmly in jumbo range.

The FHFA adjusts this limit annually based on changes in average U.S. home prices. Because home values have continued rising through 2025 and into 2026, the baseline has moved upward from previous years, but it still falls short of what homes in expensive metros actually cost. That gap is exactly why jumbo loans remain a critical product for buyers in high-demand markets.

Any loan that exceeds $833,750 in a standard U.S. county is considered a jumbo loan in 2026, regardless of the property type or your credit profile.

High-cost area exceptions

Not every county uses the same baseline limit. The FHFA designates certain counties as high-cost areas where local home prices significantly exceed the national average. In these markets, the conforming loan limit rises to as much as $1,250,750 for a single-family home in 2026. That means a $900,000 loan in San Francisco County would still qualify as a conforming loan, while that same loan amount could be a jumbo loan in a mid-tier market like parts of Illinois outside Chicago's designated high-cost zones.

To find the exact limit for a specific county, you can check the FHFA conforming loan limit map, which is updated each year following the official announcement. Knowing your county's specific threshold before you shop for a home saves you from being surprised when a lender flags your loan as non-conforming.

Multi-unit property limits

If you're buying a multi-unit property rather than a single-family home, the conforming loan limits scale up with the number of units. The table below shows the 2026 limits for standard-cost counties:

| Units | 2026 Conforming Loan Limit (Standard) |

|---|---|

| 1 | $833,750 |

| 2 | $1,067,750 |

| 3 | $1,290,800 |

| 4 | $1,603,600 |

Real estate investors often miss this point. If you're financing a duplex or triplex, your loan can go significantly higher before it becomes a jumbo product. This distinction matters because conforming multi-unit loans carry different qualification standards than jumbo multi-unit loans, and the rate difference between the two can affect your cash flow calculations on an investment property.

How jumbo loans differ from conforming loans

Understanding the jumbo loan definition only goes so far unless you also understand what changes once you cross the conforming limit. The core difference comes down to who ultimately holds the risk on your loan. Conforming loans get purchased by Fannie Mae or Freddie Mac after closing, giving lenders a guaranteed buyer for that debt. Jumbo loans have no such backstop, so the lender either holds the loan on its own books or sells it to private investors who set their own guidelines.

Who backs the loan matters for your terms

Because no government-sponsored enterprise stands behind a jumbo loan, every lender sets its own standards. Two lenders can have completely different credit score minimums, reserve requirements, and documentation demands for the exact same loan amount. With a conforming loan, Fannie Mae and Freddie Mac publish clear guidelines that most lenders follow closely, giving you more predictability from one lender to the next. With a jumbo product, you need to shop carefully and compare actual terms rather than assuming consistency.

The lender carries the full risk on a jumbo loan, which is why qualification standards often feel more demanding than what you'd face with a conventional mortgage.

Qualification standards shift significantly

Conforming loans allow debt-to-income ratios up to 45-50% in many cases, and some programs accept credit scores as low as 620. Jumbo loans typically require a credit score of 720 or higher, a DTI closer to 43% or below, and verified cash reserves covering 6 to 24 months of mortgage payments depending on loan size. Lenders also scrutinize income documentation more heavily, especially when earnings come from self-employment, commissions, or business ownership.

Down payment and mortgage insurance

Most jumbo lenders require at least 10% down, and many push that to 20% or more for loan amounts above $1.5 million. One offsetting factor is that jumbo loans rarely carry private mortgage insurance requirements, even when your down payment falls below 20%. Conforming loans typically trigger that insurance cost the moment you put down less than 20%, so the absence of PMI on a jumbo loan can reduce your monthly payment more than you'd expect.

How jumbo loans work from offer to closing

The jumbo loan process follows the same basic stages as any mortgage, but each step carries more scrutiny and longer timelines than you'd see with a conforming loan. Lenders treat these transactions as higher-stakes decisions because they're holding the full risk on the loan, so expect more documentation requests, more detailed underwriting, and occasionally additional appraisals before you reach the closing table.

Getting pre-approved before you make an offer

Serious sellers in the luxury market will not entertain offers from buyers who lack a jumbo loan pre-approval letter in hand. Before you start touring homes above the conforming limit, gather your last two years of tax returns, recent pay stubs or proof of income, bank statements covering the past two to three months, and documentation on any investment accounts. Lenders will verify every source of income and look closely at asset reserves to confirm you can cover several months of payments beyond your down payment.

A pre-approval for a jumbo loan carries more weight than for a conforming loan because lenders complete more thorough income and asset checks upfront.

Underwriting and the appraisal stage

Once you go under contract, the file moves to underwriting, where a lender's team reviews everything in detail. Jumbo underwriting often includes a second appraisal requirement for higher loan amounts, typically loans above $1.5 million. This protects the lender's investment by confirming the property value through an independent third-party opinion. The appraisal itself can take longer on luxury properties because comparable sales in high-price neighborhoods are harder to find and require more analysis from the appraiser.

From conditional approval to the closing table

After underwriting issues a conditional approval, you'll need to satisfy any outstanding conditions, which often include additional letters of explanation for large bank deposits, updated statements, or confirmation of employment. Once all conditions clear, the lender issues a clear to close, and your closing date gets scheduled. Plan for 45 to 60 days from application to closing on a jumbo loan, compared to the 30-day timeframe many conforming borrowers expect.

Jumbo loan requirements lenders usually look for

Meeting the jumbo loan definition threshold is only the starting point. Once your loan amount crosses the conforming limit, you face a completely different set of qualification standards than what a conventional borrower encounters. Because lenders hold the full risk on these loans, they apply more rigorous scrutiny to your credit history, income stability, and financial reserves before they commit to funding a transaction of this size.

Credit score and debt-to-income ratio

Most jumbo lenders set a minimum credit score of 720, and some push that to 740 or higher for loan amounts above $2 million. Your credit history needs to be clean across the full window lenders review, meaning no recent late payments, no collections, and limited hard inquiries from new credit accounts. Even one missed payment in the past 12 months can shift your rate or trigger a denial from lenders who have no flexibility to make exceptions on non-conforming products.

Your debt-to-income ratio, or DTI, needs to stay at or below 43% in most jumbo programs. Lenders calculate this by adding your proposed housing payment to all recurring monthly debt obligations, then dividing that total by your gross monthly income. If you carry significant student loans, car payments, or credit card balances, reducing those obligations before applying can make the difference between qualifying and not.

Lenders evaluate your full financial picture on a jumbo application, not just your credit score, so address any weak spots in your profile before you submit.

Income documentation and cash reserves

You need to document every dollar of income you intend to use for qualification. Salaried borrowers typically provide two years of W-2s, recent pay stubs, and employment verification. Self-employed borrowers and business owners submit two years of personal and business tax returns, year-to-date profit and loss statements, and sometimes a CPA letter confirming income continuity.

Beyond income, lenders want to see liquid reserves covering 6 to 24 months of your total mortgage payment after closing. These reserves must sit in accounts you can access without penalty, which means retirement accounts often count at a reduced percentage while checking and savings accounts count in full.

Rates, costs, and smart ways to structure the deal

The jumbo loan definition carries a common misconception: that jumbo rates are always higher than conforming rates. That was true for years, but the relationship has shifted. Because jumbo loans attract well-qualified, high-credit borrowers, lenders compete aggressively for this business, and the rate difference between conforming and jumbo products is often smaller than most buyers expect, sometimes even in the jumbo product's favor.

How jumbo rates compare to conforming rates

Jumbo rates move independently from conforming rates because they're not tied to Fannie Mae or Freddie Mac pricing. Instead, private capital markets and individual lender portfolios drive where jumbo rates land on any given day. In 2026, jumbo rates for a 30-year fixed mortgage have generally tracked within 0.25% to 0.50% of comparable conforming rates for well-qualified borrowers with credit scores above 740 and substantial reserves.

Borrowers with strong credit profiles and large down payments often qualify for jumbo rates that rival or beat conforming loan pricing.

Adjustable-rate mortgages, or ARMs, are particularly common in the jumbo space. A 10/1 ARM gives you a fixed rate for the first ten years before it adjusts annually, and many high-value buyers choose this structure when they plan to sell or refinance before the adjustment period begins. If your plans have a defined timeline, an ARM can reduce your rate by a meaningful margin.

Costs to build into your budget

Beyond the interest rate, your closing costs on a jumbo loan will run higher in raw dollar terms simply because they're calculated as a percentage of a larger loan amount. Expect origination fees, appraisal costs (sometimes two appraisals), title insurance, and prepaid interest to add up to 2% to 3% of the loan amount at closing. On a $1.2 million loan, that's $24,000 to $36,000 in closing costs you need to plan for alongside your down payment.

To structure the deal intelligently, consider making a larger down payment if you're close to a round number like 20% or 25%. Lenders tier their pricing at these benchmarks, and crossing one can reduce your rate enough to offset the additional capital deployed at closing.

Wrap-up and next steps

The jumbo loan definition comes down to one core fact: any mortgage that exceeds the conforming loan limit set by the FHFA requires a different lending approach, different documentation, and a lender who knows how to close these transactions efficiently. In 2026, that limit starts at $833,750 in standard counties and reaches $1,250,750 in high-cost markets. Qualifying means bringing strong credit, documented income, and liquid reserves to the table before you make your first offer.

You now have a clear picture of what separates jumbo loans from conforming products, what lenders look for during underwriting, and how to structure the deal to get competitive terms. The next move is finding a lender with direct jumbo experience rather than one learning the process on your transaction. If you're ready to talk through your specific situation and loan amount, connect with a jumbo loan specialist who has over 25 years of experience funding complex mortgage scenarios.