Minimum Credit Score for Home Loans: 2026 Requirements

Your credit score is one of the first numbers lenders look at when you apply for a mortgage. It affects whether you qualify, what interest rate you'll pay, and how much home you can afford. Understanding the minimum credit score for home loans in 2026 can save you months of frustration, and potentially thousands of dollars over the life of your loan.

The truth is, there's no single magic number. Different loan programs have different requirements, and recent guideline updates have shifted the landscape for borrowers across the spectrum. Whether you're eyeing an FHA loan with a lower threshold or a conventional mortgage with more competitive rates, knowing where you stand matters.

With over 25 years in mortgage lending and more than $150 million funded, I've helped buyers at every credit level find the right path to homeownership. This guide breaks down the 2026 credit score requirements for FHA, conventional, VA, and USDA loans, plus practical steps you can take if your score needs work before you apply.

Why minimum credit scores matter in 2026

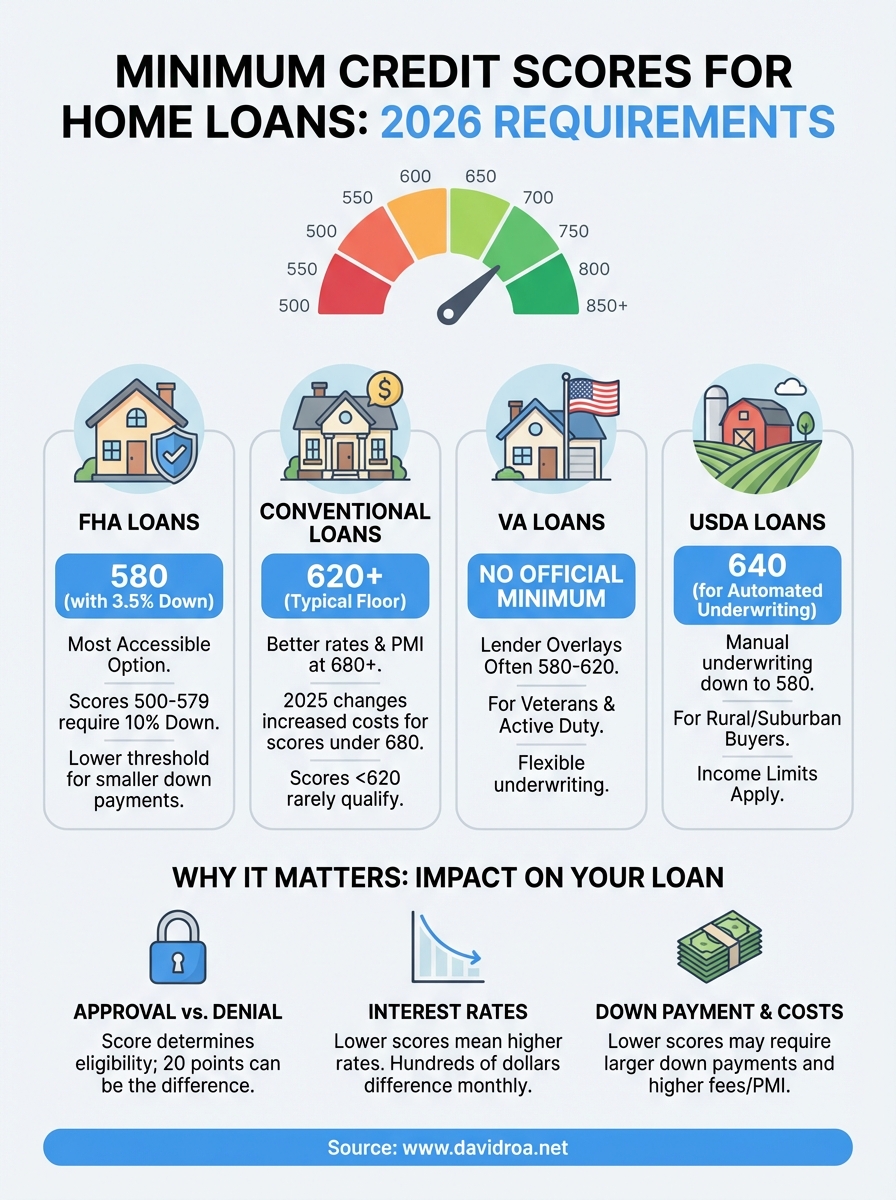

Your credit score acts as a gatekeeper in the mortgage process. Lenders use it to measure risk and decide whether to approve your loan, what interest rate to charge, and how much you'll need for a down payment. A difference of just 20 points can mean the gap between approval and denial, or thousands of dollars in extra interest over the life of your loan.

Your credit score determines your loan options

Each loan program sets its own floor for the minimum credit score for home loans. If you fall below that threshold, you won't qualify no matter how stable your income or how much you've saved. FHA loans historically accept borrowers at 580, while conventional programs typically require 620 or higher. VA and USDA loans fall somewhere in between, though individual lenders often set their own overlays above these minimums.

The practical effect is simple: a score of 575 locks you out of most programs entirely, while a 625 opens the door to conventional financing with competitive rates. Knowing where you stand helps you target the right loan type from the start instead of wasting time on applications that won't clear underwriting.

Interest rates swing by hundreds each month

Your credit score directly controls the interest rate you receive. Lenders price loans in tiers, with borrowers at 740 or above getting the best terms and those below 660 paying a premium. On a $350,000 loan, the difference between a 6.5% rate and a 7.2% rate costs you roughly $175 more per month, or over $63,000 in additional interest across a 30-year mortgage.

Even a small score improvement before you apply can save you significant money over the life of your loan.

Rate sheets change daily, but the spread between tiers remains consistent. If you're sitting at 655, pushing to 680 before you lock a rate can drop your monthly payment substantially. This isn't about perfection; it's about understanding where the cutoffs fall and positioning yourself on the right side of them.

Down payment requirements shift with your score

Lower scores often force you to bring more cash to closing. FHA borrowers with a 580 score need just 3.5% down, but if your score dips to 579 or below, that jumps to 10%. Conventional loans work differently but follow the same principle: stronger credit gives you access to programs with lower down payment requirements and better mortgage insurance rates.

Private mortgage insurance (PMI) also costs more when your score is weaker. A borrower at 680 might pay 0.5% of the loan amount annually, while someone at 630 could face 0.9% or higher. On a $300,000 loan, that's an extra $1,200 per year until you reach 20% equity. Your score doesn't just affect whether you can buy; it shapes how much you'll pay every month and how quickly you can build wealth through homeownership.

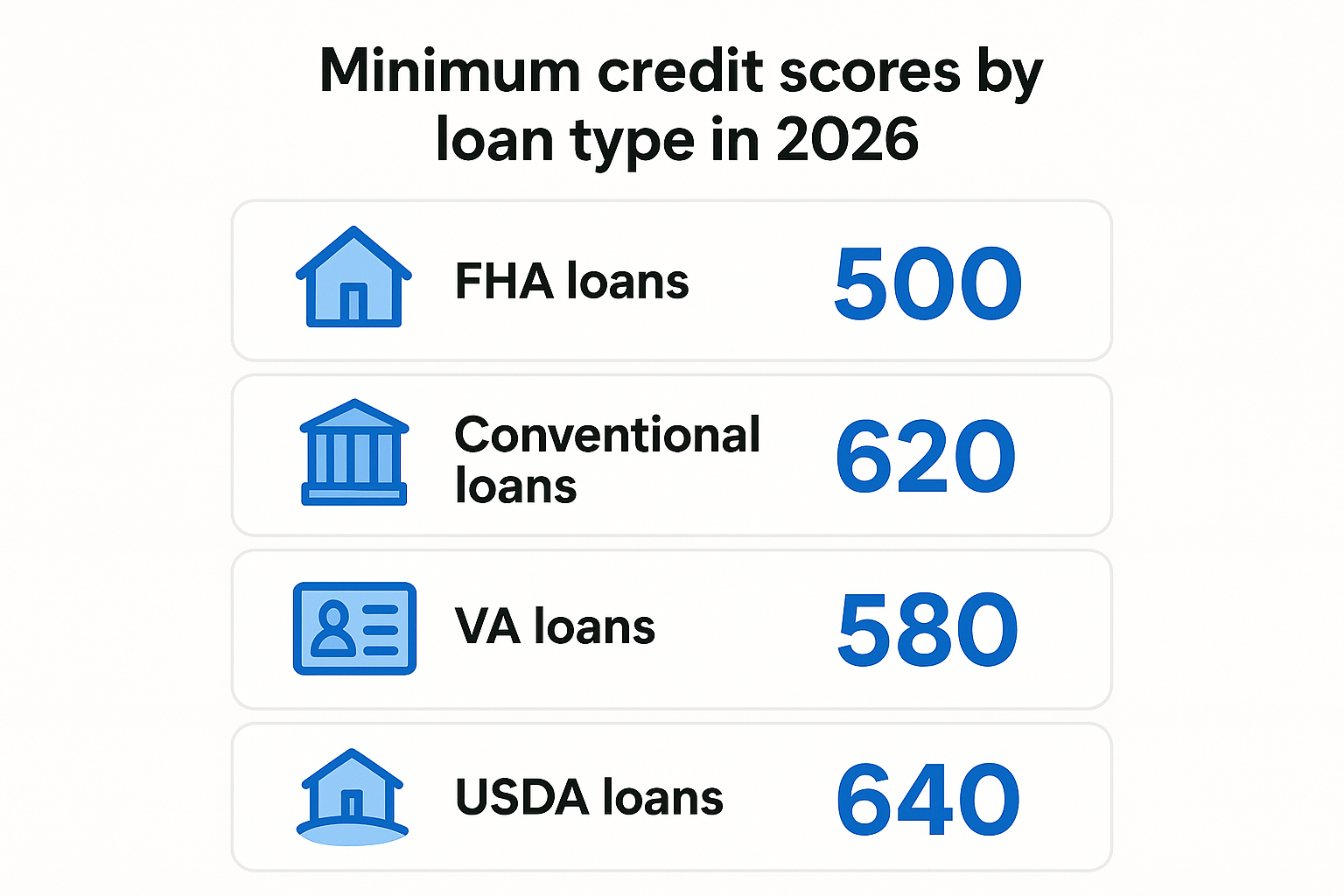

Minimum credit scores by loan type in 2026

The minimum credit score for home loans varies significantly depending on which program you choose. Each loan type serves a different borrower profile, and the credit requirements reflect that. Understanding these thresholds helps you focus your application on the program where you're most likely to succeed.

FHA loans

FHA loans remain the most accessible option for buyers with weaker credit. The official minimum is 500, but that number is misleading. If your score sits between 500 and 579, you'll need a 10% down payment to qualify. Most buyers prefer the lower threshold of 3.5% down, which kicks in at 580 or above.

Lenders often add their own requirements on top of FHA guidelines. You'll find many banks won't approve borrowers below 600 even though the program technically allows it. That's an overlay designed to reduce risk, and it's perfectly legal. Shop around if your score falls in that gap, because some lenders are more flexible than others.

Conventional loans

Conventional mortgages typically require a 620 credit score to qualify, though a handful of lenders will go as low as 580 with compensating factors. These loans offer better rates and lower mortgage insurance costs than FHA once your score reaches 680 or higher. If you're sitting at 615, it's worth the effort to push above 620 before you apply.

Conventional loans reward strong credit with significantly lower costs over the life of your mortgage.

VA loans

VA loans carry no official minimum credit score requirement from the Department of Veterans Affairs. In practice, most lenders set their floor at 580 to 620. If you're a veteran or active-duty service member with a 590 score, you'll have options that civilians at the same level won't.

USDA loans

USDA loans generally require a 640 credit score to use the automated underwriting system, though manual underwriting may accept scores as low as 580. These loans target rural and suburban buyers who meet income limits, so qualifying involves more than just your credit.

What changed for conventional loans in late 2025

Fannie Mae and Freddie Mac rolled out pricing adjustments in late 2025 that reset how lenders charge borrowers across the credit spectrum. The changes shifted costs away from higher-score borrowers with smaller down payments and toward those with weaker credit profiles, regardless of down payment size. If you're planning to use a conventional loan in 2026, these adjustments directly affect your upfront fees and monthly payments.

The new pricing adjustment for credit scores below 680

Borrowers with scores between 620 and 679 now face steeper loan-level price adjustments (LLPAs) than they did in 2024. These adjustments appear as a percentage of your loan amount and get added to your closing costs or rolled into your interest rate. A borrower at 665 putting down 10% might pay an additional 1.5% to 2.0% in fees compared to someone at 740 with the same down payment.

The practical effect is that the minimum credit score for home loans on the conventional side remains 620, but qualifying at that level costs significantly more than it did two years ago. Lenders price these adjustments into your rate, so a lower score translates directly to a higher monthly payment even if you bring the same amount of cash to closing.

If your score sits below 680, expect to pay more in fees or accept a higher rate to offset the lender's increased risk.

How the changes affect your closing costs

A $300,000 conventional loan at 640 credit score with 10% down now carries roughly $4,500 to $6,000 in additional LLPA fees compared to a 740 score. You can either pay that upfront or ask your lender to build it into your rate, which typically increases your monthly payment by $80 to $120 depending on the adjustment size.

These changes don't disqualify you, but they make conventional loans less competitive against FHA options for borrowers below 680. If your score falls in that range, run the numbers on both programs before you commit. The conventional route still wins for buyers above 700, but the gap narrowed considerably after the 2025 updates.

How lenders review credit beyond the score

Your credit score opens the door, but underwriters dig far deeper into your credit report before they approve your loan. They look at the patterns behind the number, examining how you've managed debt over time and whether recent financial behavior suggests risk. Meeting the minimum credit score for home loans gets you past the initial filter, but the details inside your report determine whether you actually close.

Payment history matters more than the number

Lenders scrutinize your payment timeline for the past 12 to 24 months. A 680 score with no late payments in two years looks stronger than a 700 score with three 30-day lates in the past year. Recent delinquencies carry more weight than older ones, and housing-related payments (rent, previous mortgages) get extra attention because they predict future behavior.

You can have a decent score but still face denial if your report shows a pattern of missed payments on installment loans or revolving accounts. Underwriters flag consecutive late payments as a red flag, even if your score recovered after you caught up. One isolated 30-day late from 18 months ago won't sink your application, but repeated lapses suggest ongoing financial instability.

Lenders care more about your recent payment behavior than your overall credit score when making final approval decisions.

Debt-to-income ratio and credit utilization

Your debt-to-income ratio (DTI) measures how much of your monthly income goes toward debt payments. Most conventional loans cap DTI at 43% to 50%, while FHA allows up to 57% in some cases. High credit card balances also hurt your application even if you pay on time, because utilization above 30% suggests you're overextended.

Underwriters calculate your total monthly obligations, including the new mortgage payment, property taxes, insurance, and all existing debts. If your score qualifies but your DTI exceeds program limits, you won't get approved until you pay down balances or increase income.

How to qualify or improve your odds with a low score

Meeting the minimum credit score for home loans doesn't guarantee approval, but specific actions can strengthen your application even if your score sits below ideal levels. Lenders evaluate your entire financial picture, and you can compensate for weaker credit by addressing other risk factors in your profile. The strategies below work whether you're six months away from applying or ready to submit an application tomorrow.

Pay down credit card balances first

Your credit utilization ratio affects both your score and how underwriters view your application. If you're carrying balances above 30% of your available limits, paying them down to 10% or lower can boost your score by 20 to 40 points within 30 to 60 days. Focus on cards close to their limits first, because maxed-out accounts hurt you more than evenly distributed balances.

Reducing your credit card utilization to below 10% often delivers the fastest score improvement you can achieve on your own.

Consider an FHA loan if you're below 620

Conventional loans penalize borrowers under 680 heavily after the 2025 pricing changes. FHA loans accept scores as low as 580 with 3.5% down, and they don't layer additional fees based on minor score differences. You'll pay mortgage insurance for the life of the loan in most cases, but the upfront qualification is easier and the monthly cost may still beat a conventional loan at your credit level.

Add a co-borrower with stronger credit

Lenders use the lower middle score when evaluating joint applications, but a co-borrower with better credit can help you qualify if their income offsets your higher debt ratios. If you're at 625 and your co-borrower sits at 720, the approval decision still hinges on your 625, but their income and payment history strengthen the overall file. This works best when you're borderline on debt-to-income limits rather than significantly below minimum score thresholds.

Conclusion section

Understanding the minimum credit score for home loans in 2026 gives you a clear target and helps you choose the right loan program for your situation. FHA loans accept borrowers at 580, conventional programs typically require 620 or higher, and VA and USDA options fall somewhere in between depending on lender overlays. The recent pricing changes make credit score differences more expensive than ever on conventional loans, but you have options regardless of where you stand.

Your score matters, but lenders evaluate your entire financial profile before making approval decisions. Payment history, debt-to-income ratios, and credit utilization all play a role. If you need help navigating these requirements or want to explore which loan type fits your credit level, reach out for a personalized consultation. With over 25 years of experience and $150 million funded, I've helped buyers at every credit level find the right path to homeownership.