Mortgage Pre Approval vs Pre Qualification: Key Differences

You found a home you love, and now the seller wants proof you can actually pay for it. That's when most buyers hear two terms thrown around: mortgage pre approval vs pre qualification. They sound similar, but they carry very different weight in a real transaction.

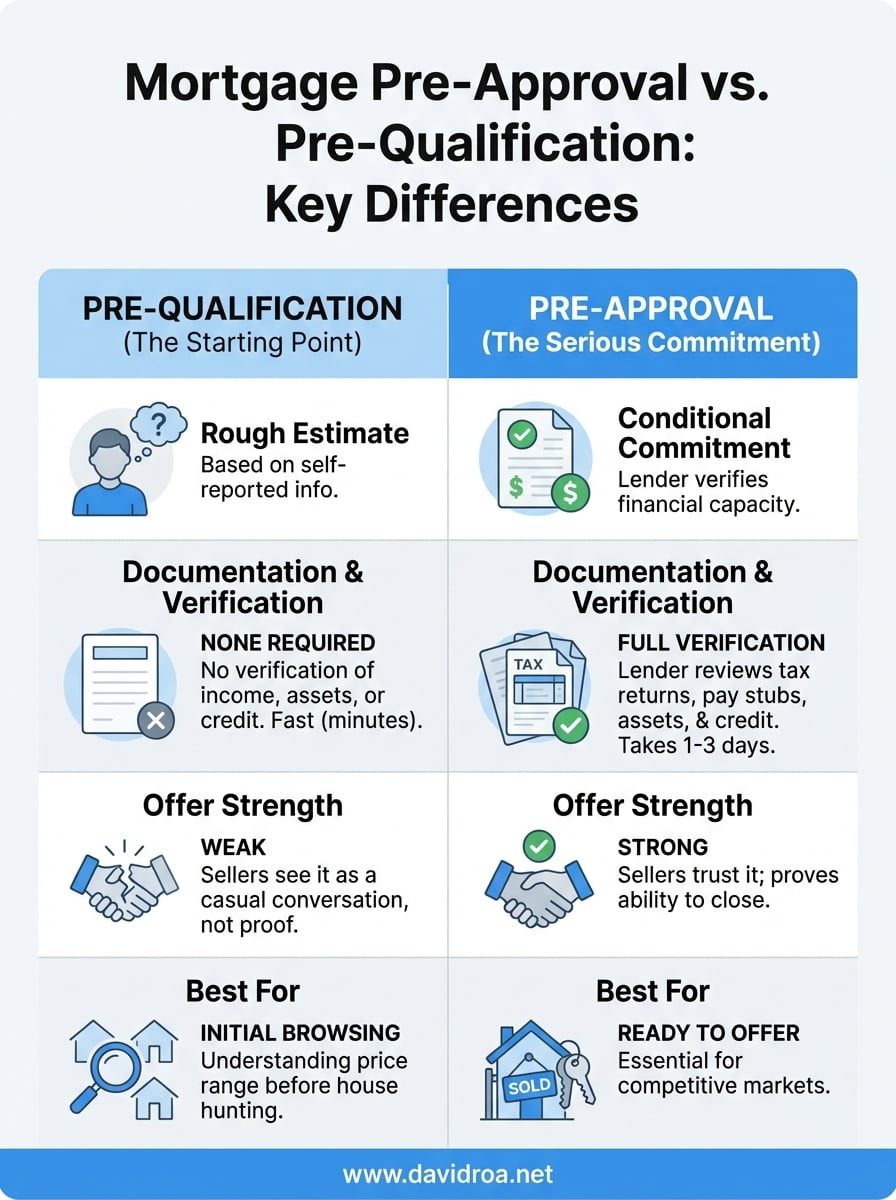

Pre-qualification gives you a rough estimate of what you might afford. Pre-approval, on the other hand, involves a lender verifying your income, assets, and credit, then issuing a conditional commitment to lend you a specific amount. One is a conversation; the other is documentation that sellers take seriously.

After 25 years in the mortgage industry and over $150 million funded, I've watched buyers lose out on properties simply because they showed up with the wrong letter. Understanding the distinction between these two steps can determine whether your offer gets accepted or passed over for someone who came better prepared.

This guide breaks down exactly what separates pre-qualification from pre-approval, what documentation each requires, and which one you actually need before house hunting. Whether you're a first-time buyer or adding to an investment portfolio, knowing where you stand financially before making an offer puts you in a stronger negotiating position.

Why the difference matters to your home offer

The listing agent receives three offers on the same property, all at the same price. Two buyers submit pre-qualification letters. One submits a pre-approval. The seller's agent will immediately recommend the pre-approved buyer because that offer carries verifiable backing from a lender who has already reviewed the financials.

Sellers want certainty. A pre-qualification is essentially a lender's educated guess based on whatever you told them over the phone or through an online form. Pre-approval means a loan officer has verified your income documentation, pulled your credit report, and confirmed you meet the lending criteria. When a deal falls through because financing fails, the seller loses time, money, and sometimes a backup buyer who moved on.

How sellers evaluate competing offers

Your offer strength goes beyond the purchase price. Sellers and their agents assess how likely you are to close based on the documentation you present. A pre-approval letter shows you've already cleared the most significant hurdle in the mortgage process.

In competitive markets, a pre-qualification letter can get your offer tossed aside immediately. Real estate agents know that pre-qualified buyers often discover problems later when they actually apply for the loan. Maybe the debt-to-income ratio doesn't work. Maybe the credit score was lower than initially stated. Those issues surface during underwriting, not during a casual phone call with a loan officer.

Pre-approval gives the seller proof that a lender has committed to funding your purchase, not just ballparked a number.

The financial credibility gap

Understanding mortgage pre approval vs pre qualification becomes critical when multiple buyers compete for the same home. Pre-approval demonstrates that you've already invested time in gathering tax returns, bank statements, and pay stubs. That effort signals serious intent.

Buyers who submit pre-qualification letters often find themselves asking for contract extensions later because underwriting uncovers unexpected issues. Sellers have no patience for that risk. They need confidence that you can perform, and a pre-approval letter provides exactly that assurance before they take their property off the market.

What mortgage prequalification really is

Pre-qualification is a preliminary estimate of how much you might be able to borrow based on information you provide to a lender. You typically complete this step through a phone conversation or an online application form. The lender asks about your income, debts, and assets, then uses that self-reported data to calculate a rough borrowing range.

No verification happens during pre-qualification. The loan officer takes your word on your salary, savings, and credit situation without requesting tax returns, pay stubs, or bank statements. This makes the process fast, often completed in minutes, but it also means the numbers can shift dramatically once a lender actually reviews your documentation.

Pre-qualification gives you a starting point for house hunting, but it doesn't guarantee the lender will actually fund your purchase.

What lenders evaluate during pre-qualification

Your stated income forms the foundation of the calculation. The loan officer divides your monthly debt payments by your monthly income to estimate a debt-to-income ratio. They also consider the down payment amount you mention and any other financial obligations you disclose.

Why pre-qualification comes first

Most buyers start with pre-qualification because it requires no financial documentation and provides an immediate answer. You can shop around between lenders quickly to compare rates and loan products. When comparing mortgage pre approval vs pre qualification, this initial step helps you understand what price range makes sense before you invest time gathering paperwork for a full application.

What mortgage preapproval really is

Pre-approval requires you to submit full financial documentation to a lender who then verifies everything before issuing a commitment letter. You provide tax returns, W-2s, pay stubs, bank statements, and authorization for a credit report pull. The lender's underwriting team reviews these documents to confirm your income, assets, debts, and creditworthiness match what you claimed.

The verification process behind pre-approval

A loan officer inputs your verified information into an automated underwriting system that evaluates your risk profile. This system checks your debt-to-income ratio, credit score, employment history, and available funds for closing. The result is a conditional approval that specifies exactly how much the lender will loan you, assuming the property meets their requirements and your financial situation doesn't change before closing.

Pre-approval transforms your house hunt from window shopping into serious negotiating because sellers know a lender has already committed to funding your purchase.

How long pre-approval stays valid

Your pre-approval letter typically remains valid for 60 to 90 days. After that period, lenders require updated documentation because your financial situation might have changed. Credit inquiries older than 90 days also need to be refreshed. When weighing mortgage pre approval vs pre qualification, remember that pre-approval demands more upfront effort but gives you immediate credibility with sellers who want to close quickly and avoid financing complications.

Prequalification vs preapproval side-by-side

The clearest way to understand mortgage pre approval vs pre qualification is to see them compared directly. Both steps aim to tell you how much you can borrow, but the process behind each number differs significantly. One relies on your word; the other requires verifiable proof of your financial capacity.

A pre-qualification gives you a number to start shopping with, while pre-approval gives you a number that sellers actually trust.

Key differences that affect your buying power

| Factor | Pre-Qualification | Pre-Approval |

|---|---|---|

| Documentation | None required | Tax returns, pay stubs, bank statements |

| Credit check | Soft inquiry or none | Hard inquiry that impacts credit score |

| Verification | Self-reported information | Lender verifies all details |

| Timeline | Minutes to hours | 1 to 3 business days |

| Validity period | Varies by lender | 60 to 90 days |

| Offer strength | Weak in competitive markets | Strong negotiating position |

| Underwriting | Not reviewed | Conditionally approved by underwriter |

Your choice between these two options depends on where you are in your home search. Pre-qualification works when you want a quick estimate before seriously looking at properties. Pre-approval becomes necessary when you're ready to submit an offer and compete against other buyers who have already completed their financial verification.

How to choose the right step for your timeline

Your timeline determines which option makes sense. If you're just starting to explore what you can afford and won't be making offers for several months, pre-qualification gives you enough information to browse listings and understand your price range. You avoid the credit inquiry that comes with pre-approval and can still gather financial documents at your own pace.

When pre-qualification makes sense

Start with pre-qualification when you're three to six months away from submitting an offer. This approach lets you compare lenders, understand different loan products, and refine your budget without the pressure of a time-sensitive approval letter. You can shop around freely and decide which lender offers the best terms before committing to a full application process.

Pre-qualification works when you're still figuring out whether buying makes sense for your financial situation.

When to get pre-approved instead

Move to pre-approval as soon as you're ready to tour properties seriously or when you find a home that meets your criteria. Competitive markets demand pre-approval letters because sellers won't wait while you scramble to verify your finances. The difference between mortgage pre approval vs pre qualification becomes critical once you're prepared to write an offer and need to stand out against other buyers who already completed their documentation.

Next steps

Understanding mortgage pre approval vs pre qualification puts you ahead of most buyers who walk into the process unprepared. You now know that pre-qualification gives you a starting estimate, while pre-approval provides verified credibility that sellers actually respect. The difference determines whether your offer gets accepted or ignored when competition heats up.

Start by gathering your financial documents now: two years of tax returns, recent pay stubs, bank statements, and a list of your current debts. This preparation lets you move straight to pre-approval when you find the right property, eliminating delays that cost you the deal.

Your next move depends on how soon you plan to submit offers. If you're actively house hunting or ready to compete in today's market, skip pre-qualification entirely and go straight to a lender who can verify your finances. Working with an experienced loan officer who understands both residential purchases and investment properties ensures you get accurate numbers and the strongest possible letter for your situation.