Navy Federal VA Loan Rates: Today’s Rates, APR & Payments

If you're a veteran or active-duty service member exploring your home financing options, Navy Federal VA loan rates are likely on your radar. Navy Federal Credit Union is one of the largest credit unions in the country, and they're known for offering competitive VA loan products with some unique perks, no private mortgage insurance, flexible credit requirements, and a range of fixed and adjustable-rate terms.

But here's the thing most borrowers miss: the rate you see advertised isn't always the rate you'll get. Your credit profile, loan amount, occupancy type, and even the day you lock all play a role. That's why understanding how Navy Federal structures its VA rates and APRs matters before you commit. A difference of even a quarter percent can shift your monthly payment by hundreds of dollars over the life of the loan.

As a senior loan officer with over 25 years in the lending industry and more than $150 million in funded loans, I've helped countless VA-eligible borrowers at David Roa compare their options, including credit union offers like Navy Federal's, against the broader market. In this breakdown, we'll walk through today's Navy Federal VA loan rates, what drives them, and how to evaluate whether they're truly your best deal.

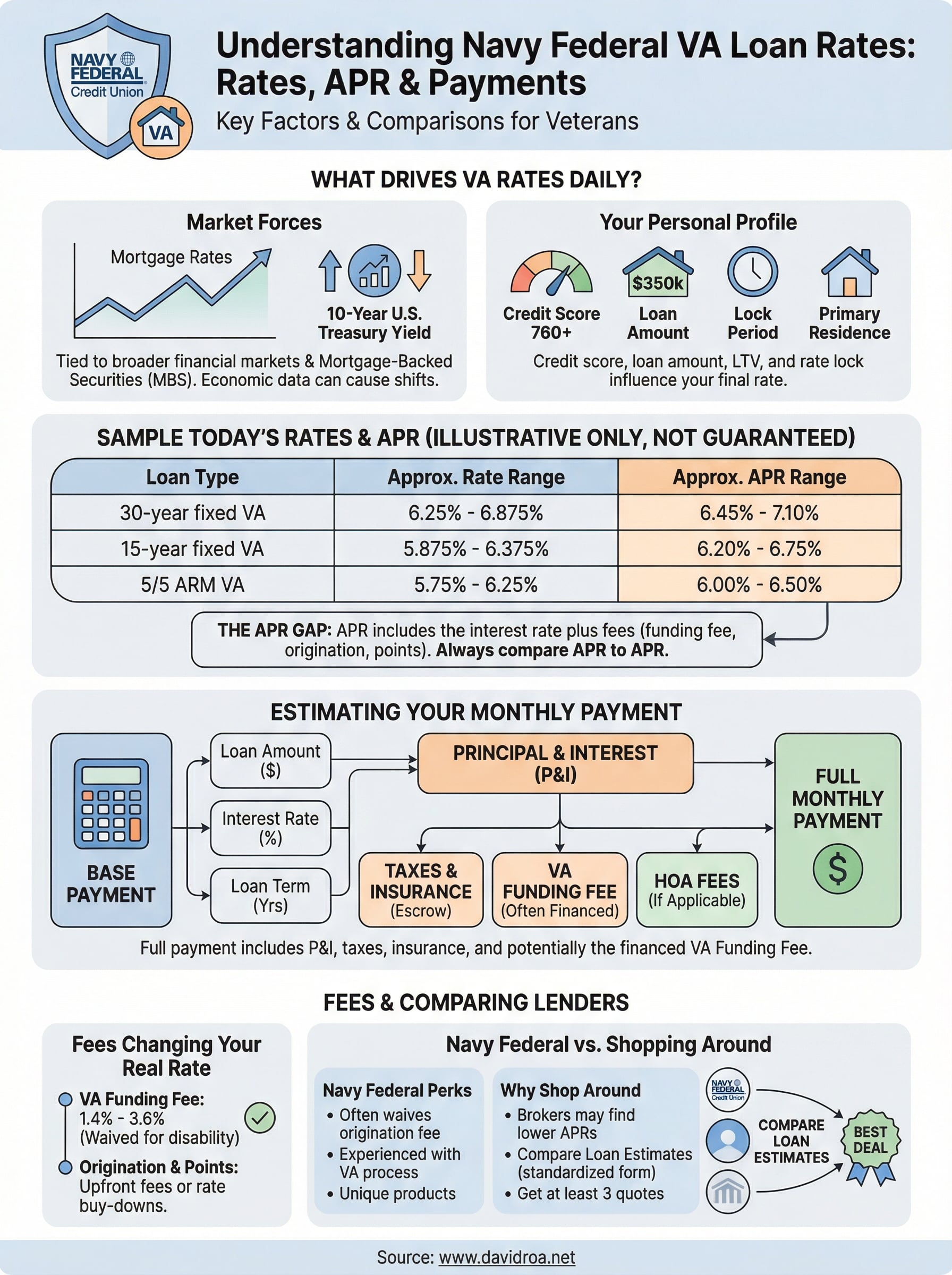

Why Navy Federal VA loan rates change daily

Navy Federal VA loan rates don't sit still, and that's not unique to this lender. Mortgage rates move every business day because they're tied to forces in the broader financial market. If you check the rate on Monday and wait until Thursday to call back, you may be looking at a different number entirely.

The bond market drives the baseline

Mortgage-backed securities (MBS) are the primary engine behind daily rate movement. When investors buy more MBS, lenders can offer lower rates. When investors sell, rates climb. The 10-year U.S. Treasury yield is the most widely watched proxy for this activity. Navy Federal, like every lender, monitors these movements and adjusts its rate sheets accordingly, sometimes more than once per day.

A Federal Reserve policy shift, a jobs report, or an inflation reading can swing rates by 0.125% to 0.25% in a single session, which adds up to thousands of dollars over a 30-year loan.

Economic data releases from sources like the Bureau of Labor Statistics and the Federal Reserve are the main triggers for these swings. On days when a major report drops, rates can move fast.

Your personal loan profile matters too

Beyond the market, your individual borrower profile shapes the rate Navy Federal actually quotes you. Lenders use a layered pricing model that adjusts for your credit score, loan amount, loan-to-value ratio, and property type. VA loans don't require a down payment, but a borrower with a 760 credit score will typically see a better rate than one with a 640.

Your lock period also factors in. A 60-day rate lock generally costs more than a 30-day lock because the lender carries more risk over a longer window.

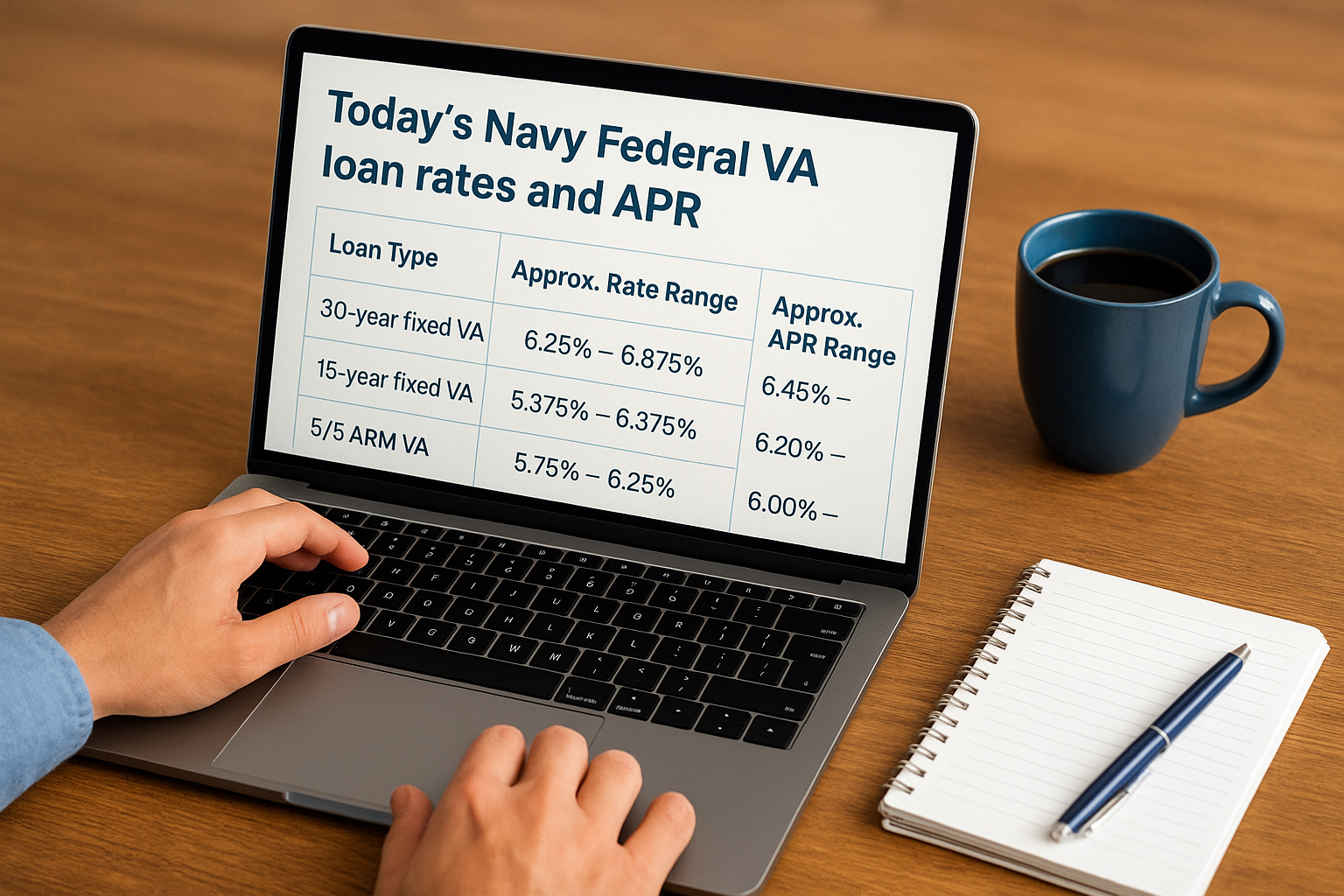

Today's Navy Federal VA loan rates and APR

Navy Federal publishes its current rate sheet on their website, but those numbers shift daily and depend on your specific loan profile. The table below reflects a sample range based on typical market conditions in early 2026 to give you a realistic starting point, not a guaranteed quote.

| Loan Type | Approx. Rate Range | Approx. APR Range |

|---|---|---|

| 30-year fixed VA | 6.25% - 6.875% | 6.45% - 7.10% |

| 15-year fixed VA | 5.875% - 6.375% | 6.20% - 6.75% |

| 5/5 ARM VA | 5.75% - 6.25% | 6.00% - 6.50% |

The APR is almost always higher than the stated rate because it folds in the VA funding fee, origination charges, and any discount points paid at closing.

The gap between rate and APR

Your interest rate tells you the borrowing cost on the principal balance. Your APR (Annual Percentage Rate) tells you the full cost of the loan because it absorbs fees into a single annualized figure. When you compare navy federal va loan rates against other lenders, always match APR to APR. A loan with a lower rate but heavier fees can cost you more over time than one with a slightly higher rate and minimal closing costs.

How to estimate your VA payment with Navy Federal

Before you call a loan officer, it helps to run a rough estimate yourself. Navy Federal's website includes a mortgage calculator, but understanding what goes into that number lets you cross-check the output and avoid surprises at closing.

Start with the principal and interest

Your base monthly payment depends on three inputs: the loan amount, the interest rate, and the loan term. For example, a $350,000 VA loan at 6.5% on a 30-year fixed term produces a principal and interest payment of roughly $2,213 per month. Adjust the rate up or down by 0.25% and that figure shifts by about $55 to $60 each month, which adds up to over $700 per year.

Running multiple scenarios side by side is the fastest way to see how even small rate changes affect your real monthly cost.

Factor in taxes, insurance, and the funding fee

Your full monthly payment will include property taxes, homeowners insurance, and possibly a VA funding fee rolled into the loan balance. Most borrowers who finance the VA funding fee (which ranges from 1.4% to 3.6% depending on your down payment and prior use) add roughly $30 to $80 per month to their payment depending on loan size.

Fees and costs that change your real rate

When you evaluate navy federal va loan rates, the interest rate is only part of the story. Several fees get layered on top that directly affect how much the loan actually costs you over time, and knowing them upfront prevents surprises at the closing table.

The VA funding fee

The VA funding fee is a one-time charge the Department of Veterans Affairs requires on most VA loans. It ranges from 1.4% to 3.6% of the loan amount, depending on your down payment and whether you've used your VA benefit before. Most borrowers roll it into the loan balance, which increases the principal you're paying interest on for the life of the loan.

If you have a service-connected disability rating, the VA waives the funding fee entirely, which can save you thousands of dollars.

Origination charges and discount points

Navy Federal may charge an origination fee, which typically runs around 1% of the loan amount. You may also have the option to buy discount points to lower your rate, where each point costs 1% of the loan amount and reduces your rate by roughly 0.25%. If you plan to stay in the home long-term, buying points can pay off. If you expect to sell or refinance within five years, paying points rarely makes financial sense.

How Navy Federal compares to other VA lenders

Navy Federal has real advantages for VA borrowers, but navy federal va loan rates don't automatically beat every lender on the market. Getting at least three loan estimates before you commit is the only way to know whether you're leaving money on the table.

Where Navy Federal holds an edge

Navy Federal often waives its origination fee for VA loans, which can save you $3,000 or more on a mid-sized loan. Their loan officers also deal with VA paperwork daily, which reduces the risk of documentation delays when you're under contract with a firm closing date.

Membership is a hard requirement. If you or an immediate family member don't qualify for Navy Federal, you'll need to look at other lenders regardless of how competitive their rates appear.

Where shopping around pays off

Independent mortgage brokers work with multiple investors and can sometimes source lower APRs, particularly for borrowers with credit scores above 740. Running a side-by-side comparison of origination costs, APRs, and lender fees on each estimate is the clearest way to confirm you're getting a competitive deal.

When you request a Loan Estimate, every lender must use the same standardized form required by federal law. That makes it straightforward to line up Navy Federal's numbers against any other lender's and see exactly where the cost differences lie.

Next steps

You now have a clear framework for reading navy federal va loan rates beyond the headline number. Check Navy Federal's current rate sheet, run a payment estimate using the inputs from this guide, and request at least two additional Loan Estimates from other lenders before you commit. Comparing APRs side by side on standardized forms is the fastest way to confirm whether Navy Federal's offer is genuinely competitive for your specific loan profile.

Getting pre-approved early also protects you. Rate locks expire, and waiting too long in a rising-rate environment can cost you more than any lender fee you tried to avoid. If you have a service-connected disability, confirm your VA funding fee waiver before your closing disclosure is issued.

When you're ready to explore your options with a lender who has worked through complex VA scenarios for over 25 years, connect with David Roa to get a straightforward comparison built around your numbers.