VA Loan Eligibility Calculator: Estimate Entitlement & Limit

Figuring out your VA loan entitlement shouldn't require a finance degree. Yet most veterans and active-duty service members hit a wall when they try to determine exactly how much they can borrow, especially if they already have an existing VA loan and need to calculate remaining bonus entitlement. A reliable VA loan eligibility calculator takes the guesswork out of the equation and gives you a clear picture of your borrowing power in minutes.

At David Roa, we've helped veterans and military families secure VA financing as part of over $150 million in funded loans across more than 25 years in the lending business. VA loans are one of the most powerful homebuying tools available, but only if you understand how your entitlement actually works, and that's where most borrowers get tripped up.

This guide walks you through how to estimate your VA loan entitlement and county loan limits, what inputs you need, and how to use the numbers to make a confident buying decision. Whether you're a first-time VA buyer or purchasing a second property with partial entitlement, you'll leave here knowing exactly where you stand.

What the calculator is really estimating

Most online tools labeled as a VA loan eligibility calculator aren't calculating your eligibility in the traditional sense. You've already earned eligibility through your service. What the calculator is actually doing is estimating your entitlement, which is the dollar amount the VA guarantees to your lender if you default. That guarantee is what allows lenders to offer you a loan with no down payment and no private mortgage insurance.

Your entitlement is not a loan limit, it is the VA's financial guarantee to your lender, and understanding that distinction changes how you interpret every number the calculator produces.

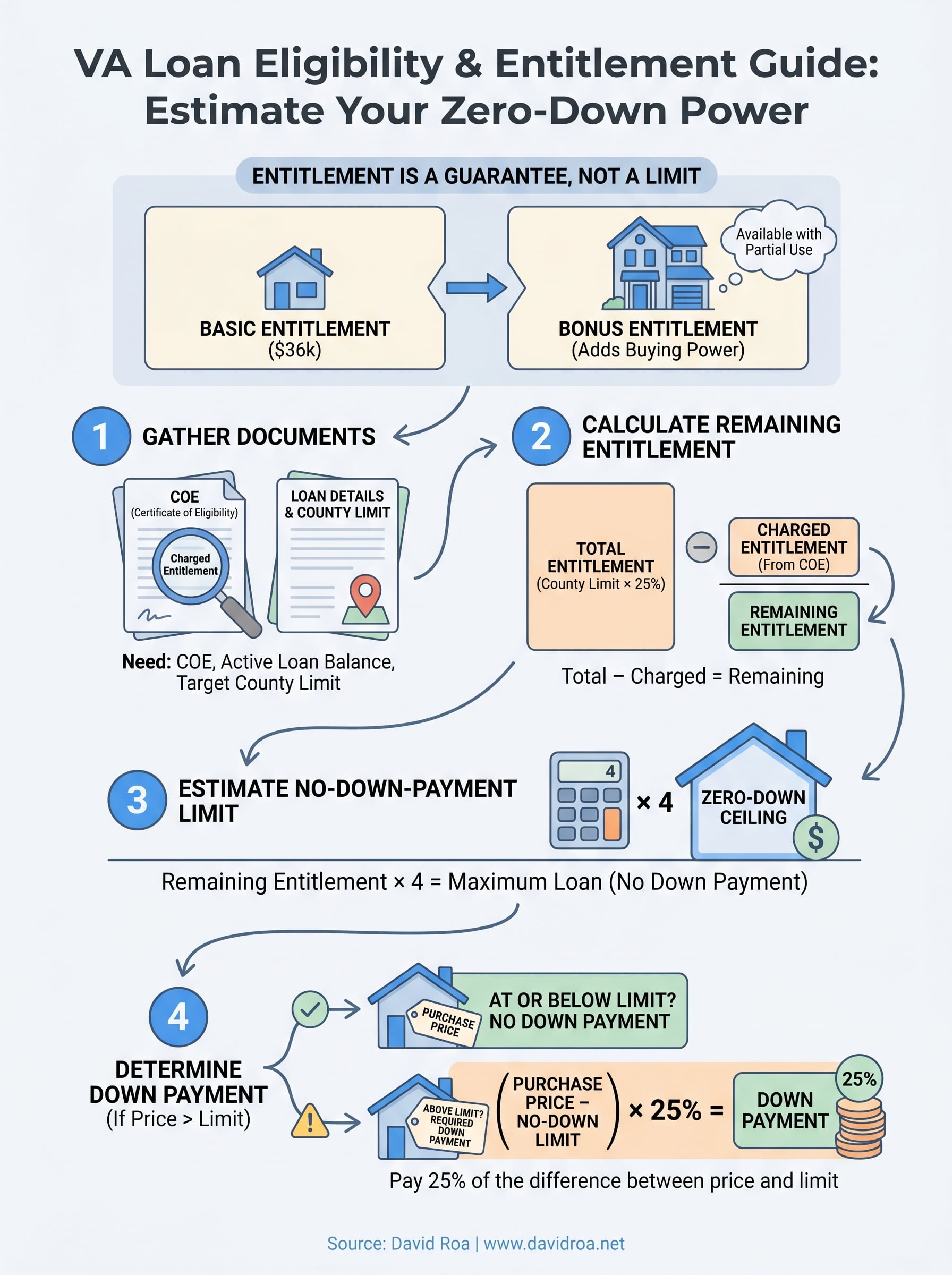

Basic entitlement vs. bonus entitlement

Every eligible borrower starts with basic entitlement of $36,000, but that number is misleading on its own. Lenders typically lend up to four times the available entitlement, so your real borrowing power comes from what the VA calls bonus entitlement (also known as second-tier or additional entitlement). For most counties in the U.S., the total entitlement available in 2025 is $127,600, which supports loans up to $766,550 with no down payment required.

If you've never used a VA loan before, your full entitlement is available and there is no county loan limit that caps your no-down-payment borrowing power under current VA rules. The calculator matters most when you've already used a portion of your entitlement and want to know what's left.

How your county loan limit factors in

Your county's conforming loan limit, set annually by the Federal Housing Finance Agency, becomes relevant when you have partial entitlement remaining from a prior VA loan. In that scenario, the calculator uses the local loan limit to determine the maximum loan you can take without a down payment. Higher-cost counties like those in the Chicago metro area carry higher limits, which directly expands your available buying power.

Step 1. Gather your COE and loan details

Before you run any VA loan eligibility calculator, you need two things in front of you: your Certificate of Eligibility (COE) and the details of any active or paid-off VA loans you currently hold. Without these documents, any number the calculator produces is an educated guess, not a reliable estimate.

Your COE is the official document that confirms your entitlement amount and shows exactly how much of it has already been used.

What your COE shows

Your COE lists your entitlement code and your charged entitlement, which is the portion already tied to an existing VA loan. You can request your COE directly through the VA's official portal or ask your lender to pull it through the VA's Automated Certificate of Eligibility system.

The loan details you need

If you carry an existing VA loan, gather the original loan amount and your current outstanding balance. You will also need your target county's conforming loan limit for the property you plan to buy. Here is what to collect before moving to the next step:

- COE with entitlement amount listed

- Original VA loan balance (if applicable)

- Current outstanding balance on any active VA loan

- Target county conforming loan limit for 2025

Step 2. Calculate remaining entitlement

The math behind remaining entitlement is straightforward once you have the numbers from Step 1. You subtract your charged entitlement (the amount tied to your existing VA loan) from the total entitlement available in your county to get what's left. That remaining figure is what any va loan eligibility calculator uses to determine your next loan's no-down-payment ceiling.

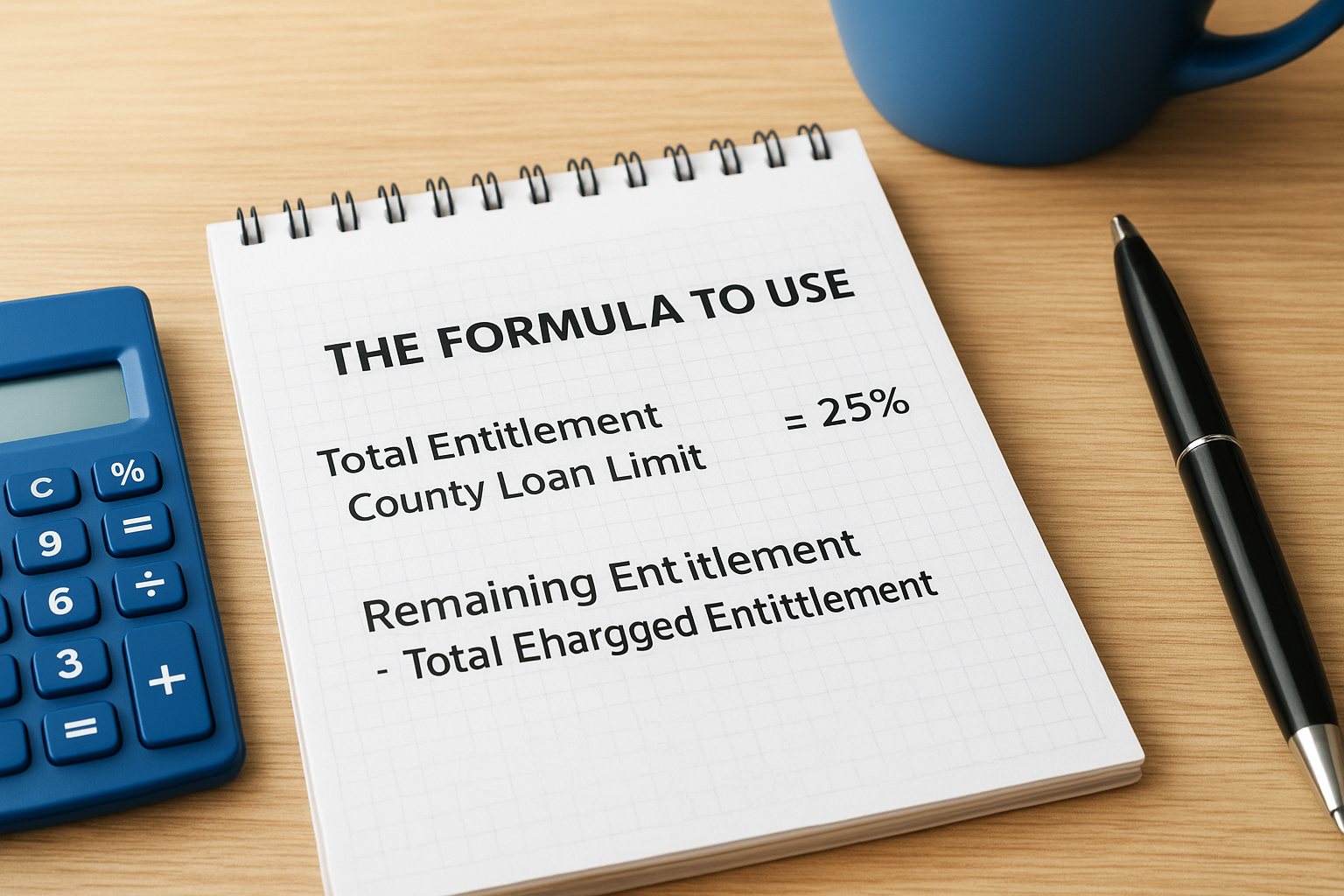

The formula to use

Use this calculation to find your remaining entitlement:

Total Entitlement = County Loan Limit × 25%

Remaining Entitlement = Total Entitlement - Charged Entitlement

For example, if your county loan limit is $766,550, your total entitlement equals $191,637. If your charged entitlement from a prior loan is $50,000, your remaining entitlement is $141,637.

Double-check your charged entitlement directly on your COE before plugging numbers into the formula, since an outdated figure will throw off every calculation that follows.

What the result tells you

Your remaining entitlement represents 25% of the maximum loan you can take with no down payment on the new property. Multiply it by four to get your actual no-down-payment loan ceiling for that county.

Using the example above, $141,637 × 4 gives you a borrowing ceiling of $566,548. Any purchase price above that number means you'll need to cover 25% of the difference as a down payment.

Step 3. Estimate your no-down-payment limit

Once you have your remaining entitlement from Step 2, converting it into a usable purchase ceiling takes one calculation. Multiply your remaining entitlement by four, and you get the maximum loan amount you can take on the new property without putting any money down. This number is the core output of any va loan eligibility calculator, and it tells you exactly where your zero-down threshold sits.

Your no-down-payment limit is tied to your remaining entitlement, not your income or credit score, so the math stays consistent regardless of your financial profile.

Applying the formula to real numbers

The table below shows how different remaining entitlement amounts translate into actual buying power based on a standard county loan limit of $766,550:

| Remaining Entitlement | Multiply by | No-Down-Payment Limit |

|---|---|---|

| $191,637 (full) | 4 | $766,550 |

| $141,637 | 4 | $566,548 |

| $91,637 | 4 | $366,548 |

| $50,000 | 4 | $200,000 |

If your target purchase price falls at or below your no-down-payment limit, you can move forward with zero down. Any amount above that ceiling requires a down payment equal to 25% of the difference between the purchase price and your estimated limit. Run these numbers before you start house hunting so you know your real budget before you ever sit across from a seller.

Step 4. Know when a down payment applies

A down payment only enters the picture when your purchase price exceeds your no-down-payment limit from Step 3. Understanding this threshold is the final output a va loan eligibility calculator delivers, and it tells you exactly how much cash to prepare before you make an offer.

A down payment on a VA loan is always smaller than what conventional financing would require for the same purchase price, even when you're working with partial entitlement.

The formula for your required down payment

When your target price sits above your no-down-payment ceiling, the math is direct. You owe 25% of the difference between your purchase price and your zero-down limit.

Down Payment = (Purchase Price - No-Down-Payment Limit) × 25%

For example, if your no-down-payment limit is $566,548 and you want to buy at $650,000, the difference is $83,452. Your required down payment is $83,452 x 25%, which equals $20,863. Compare that to the 20% down a conventional lender would require on the same $650,000 purchase, which would be $130,000. The VA benefit preserves a significant amount of your cash even when a partial down payment applies.

Your Move

You now have the complete framework to run your own VA loan eligibility calculator without guessing at any step. Start with your COE and charged entitlement, subtract from your total county entitlement, multiply the remainder by four, and you know your exact zero-down ceiling. If the purchase price sits above that number, calculate 25% of the difference to find your required down payment.

Those four steps cover every scenario, whether you're a first-time VA buyer with full entitlement or a veteran carrying a partial balance from a prior loan. The numbers stay consistent regardless of the lender or tool you use. Now you know how to read them before you ever make an offer.

When you're ready to move from calculation to closing, connect with David Roa for hands-on VA loan guidance backed by over $150 million in funded loans and more than 25 years of experience helping veterans and military families close.