VA Loan Eligibility Requirements: Who Qualifies and How

If you've served in the military, you've earned access to one of the most powerful home financing tools available, but understanding VA loan eligibility requirements can feel like reading another government manual. Between minimum service thresholds, discharge conditions, and the Certificate of Eligibility process, there's a lot to sort through before you even start shopping for a home.

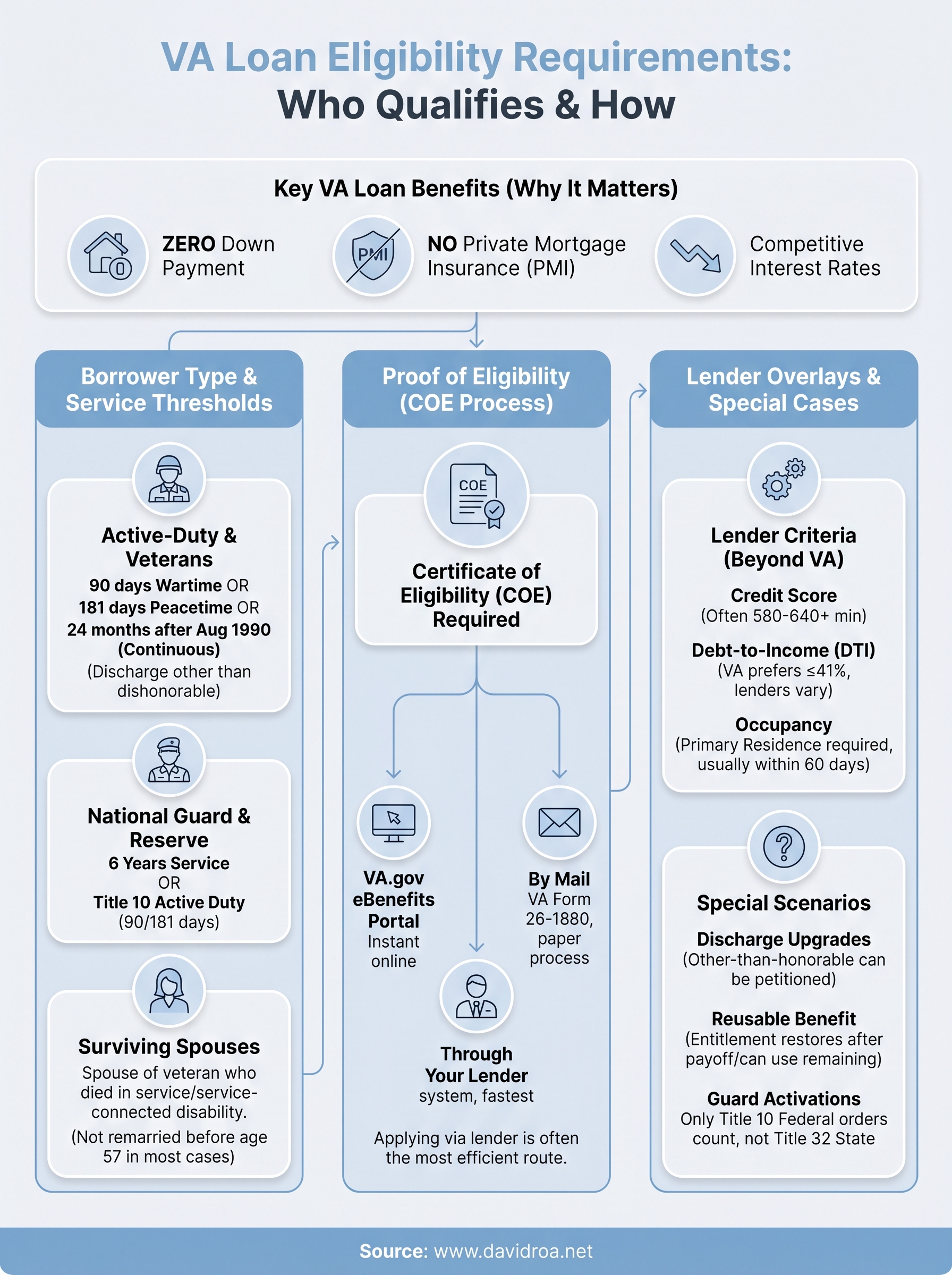

The good news: once you know where you stand, the path forward is straightforward. VA loans offer zero down payment, no private mortgage insurance, and competitive rates that most conventional products can't match. The catch is that not every veteran or service member qualifies automatically, and the specific criteria depend on when you served, how long you served, and your current financial profile. Credit scores, income verification, and entitlement limits all play a role.

At David Roa, we've spent over 25 years helping buyers, including veterans and active-duty service members, navigate exactly these questions. With more than $150 million in funded loans, we've guided hundreds of borrowers through the VA process from eligibility confirmation to closing day. This guide breaks down every qualifying factor so you can determine your eligibility with confidence and take the next step toward homeownership.

Why VA loan eligibility matters

Understanding your standing against VA loan eligibility requirements is worth doing before you tour a single property. The VA loan program offers a combination of benefits that no other mortgage product comes close to matching, and knowing you qualify gives you a real negotiating position in any market.

The financial advantage of VA loans

The numbers tell the story quickly. A conventional loan on a $400,000 home typically requires a 5% down payment, which means $20,000 out of pocket before you factor in closing costs. A VA loan brings that requirement to zero, keeping your savings intact and your buying power high. On top of that, you avoid private mortgage insurance entirely, a line item that can run $100 to $300 per month on a conventional loan and adds up to thousands over the life of the loan.

Eliminating both the down payment and PMI puts more cash in your pocket every month and accelerates the equity you build in your home.

Your VA loan also carries competitive interest rates that typically run lower than conventional and FHA products, because the VA guaranty reduces the lender's risk. That lower rate compounds over 15 or 30 years into significant long-term savings on total interest paid.

Why confirming eligibility early saves you time

Skipping the eligibility check and proceeding directly to house hunting creates a real problem. If a lender discovers a service gap or discharge status issue after you've made an offer, you lose time and potentially the property. Sellers work on timelines, and financing delays break deals that otherwise would have closed.

Confirming your eligibility upfront also gives you a clear picture of your entitlement amount, which determines how much the VA will back without requiring a down payment. That number matters when you're looking at higher-priced markets or purchasing a second property while retaining a previous VA loan. Starting the process with a confirmed eligibility status means every step after it moves faster and with fewer surprises.

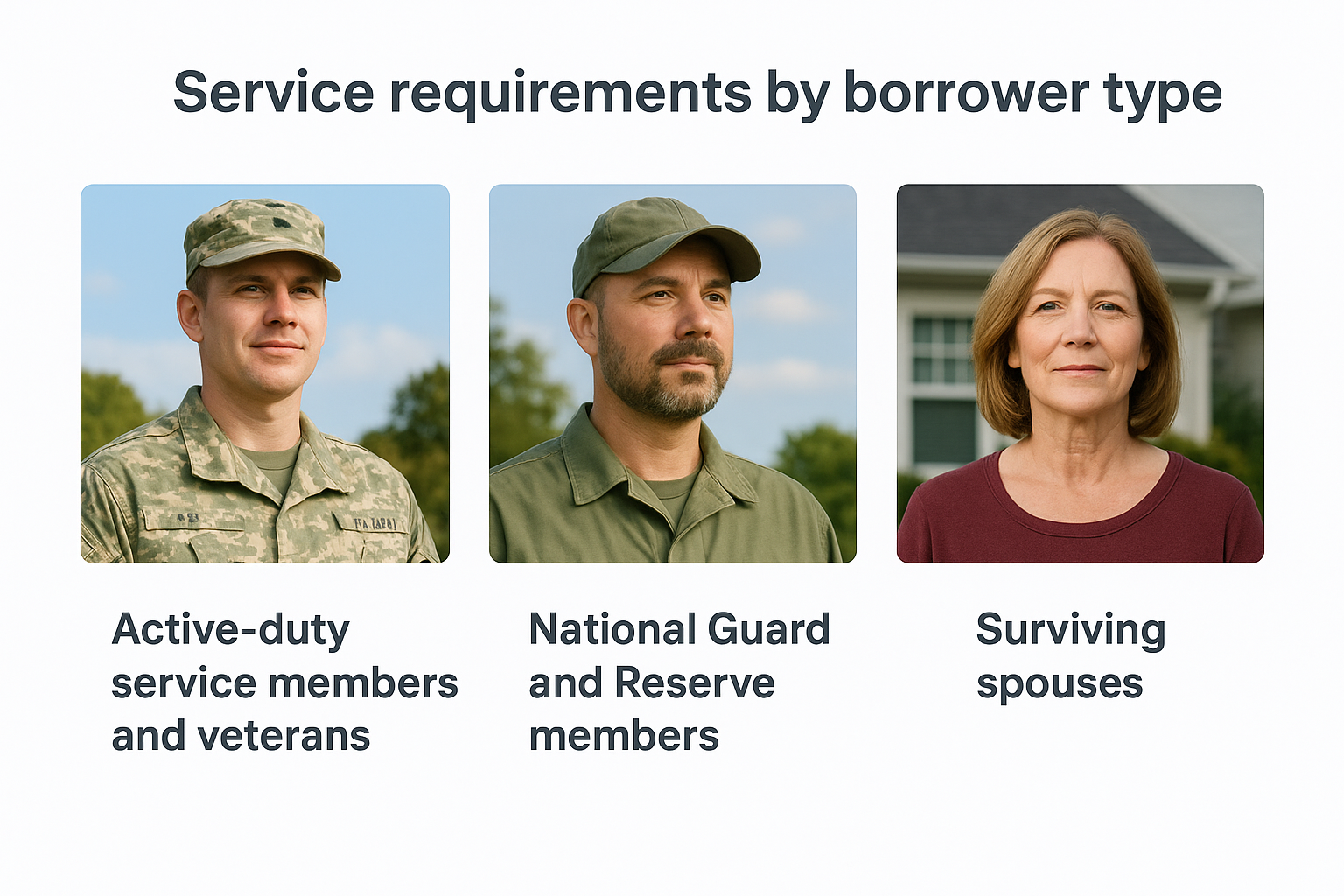

Service requirements by borrower type

The VA loan eligibility requirements for service differ based on which category you fall into. Your branch, era of service, and length of duty all factor into whether you meet the minimum threshold. The VA sets clear benchmarks for each borrower type, so there is no ambiguity once you know where you fit.

Active-duty service members and veterans

If you served on active duty, the minimum requirement is 90 continuous days during wartime or 181 days during peacetime. Veterans who served after August 1990 need 24 months of continuous active-duty service or the full period for which they were called. A discharge under any condition other than dishonorable keeps your eligibility intact.

Honorable, general, and other-than-honorable discharges all meet the VA's character of discharge standard in most cases.

National Guard and Reserve members

Guard and Reserve members must complete six years of service in their respective branch, or be called to active duty under Title 10 orders. If you were activated under Title 10, the standard 90-day wartime or 181-day peacetime thresholds apply instead of the six-year requirement.

Surviving spouses

Surviving spouses of veterans who died in service or from a service-connected disability may qualify for VA loan benefits. You must not have remarried before age 57 in most circumstances. Spouses of service members listed as missing in action or prisoners of war also retain eligibility.

Certificate of Eligibility and how to get it

The Certificate of Eligibility, or COE, is the document that proves to a lender that you meet VA loan eligibility requirements. Without it, no lender can process your VA loan application. Getting your COE is a required step, but it does not have to slow you down. Most borrowers can obtain one in minutes through the right channel.

Three ways to obtain your COE

You have three direct options for securing your COE, and each one fits a different situation depending on your access to technology and documentation.

- VA.gov eBenefits portal: Apply online through your eBenefits account for the fastest result. Many veterans receive their COE instantly.

- Through your lender: Most VA-approved lenders can pull your COE directly using the VA's Web LGY system, often within seconds during the loan application.

- By mail: Submit VA Form 26-1880 to your regional loan center if you prefer a paper process or have documentation issues that need manual review.

Applying through your lender is the most efficient route if you're already working with a VA-approved mortgage professional.

What to do if your COE shows an issue

Sometimes a COE comes back with a reduced entitlement or an error tied to a prior VA loan. This happens when a previous VA loan was not fully paid off or the prior property was not sold. Your lender can request a one-time restoration of entitlement in most cases, which resets your benefit for the new purchase.

Lender rules: credit, income, and occupancy

Meeting the VA loan eligibility requirements set by the VA itself is only part of the picture. Individual lenders apply their own overlays on top of the VA's baseline standards, covering credit scores, income documentation, and how you intend to use the property.

Credit score expectations

The VA does not set a minimum credit score, but most lenders impose a floor between 580 and 620. Some lenders work with scores below 600 on a case-by-case basis, while others require 640 or higher for streamlined approval. A stronger score gives you access to better rate pricing and a faster underwriting process.

Checking your credit report before applying gives you time to correct errors that could otherwise push your score below a lender's threshold.

Income and debt-to-income ratio

Lenders use your debt-to-income ratio (DTI) to confirm that your monthly obligations stay within manageable limits. The VA prefers a DTI at or below 41%, though lenders can approve higher ratios with compensating factors such as significant residual income or strong cash reserves. You'll need to document your income through W-2s, pay stubs, or tax returns depending on your employment type.

Occupancy requirements

Your VA loan must finance a primary residence, not an investment property or vacation home. You are required to occupy the home within 60 days of closing in most situations. Active-duty service members on deployment can designate a qualified family member to fulfill this requirement on their behalf.

Special cases and common eligibility questions

Some borrowers encounter specific scenarios that the standard VA loan eligibility requirements don't address directly. These situations come up more often than most applicants expect, and understanding them upfront saves you from stalled applications or missed opportunities.

Discharge status and upgrades

If your discharge was other-than-honorable, you are not automatically locked out of the program. You can petition your branch's Discharge Review Board to request an upgrade, and each case gets evaluated individually based on your service record and the circumstances surrounding your separation.

A successful upgrade restores your full entitlement and makes you eligible for all VA home loan benefits going forward. Your lender can help you understand the expected timeline before you submit your petition.

Using your VA benefit more than once

Your VA loan benefit is not a one-time option. After you sell a VA-financed home and pay off the loan, your entitlement restores automatically. Borrowers who still hold an active VA loan can use their remaining entitlement toward a second home, though a down payment may apply if the loan amount exceeds the county limit.

Your lender can pull your current entitlement status through the VA's system and confirm exactly how much remains available for your next purchase.

National Guard state activations

State-ordered activations do not count toward VA eligibility, regardless of how long the activation lasted. Only Title 10 federal orders meet the service threshold required for the program. If your orders fall under Title 32, review your DD-214 carefully before submitting an application.

Providing complete service documentation to your lender early prevents delays and ensures your eligibility gets assessed accurately from the start.

Next steps

You now have a complete picture of VA loan eligibility requirements, from minimum service thresholds to lender overlays and special discharge situations. The next move is to confirm your eligibility status, pull your COE, and connect with a lender who knows the VA process inside and out.

Working with an experienced VA-approved mortgage professional saves you time and prevents the documentation errors that stall applications. David Roa brings over 25 years of lending experience and a track record of more than $150 million in funded loans to every transaction, including complex VA scenarios that other lenders turn away.

Start your VA loan conversation with David Roa today and get a clear answer on your eligibility, your entitlement amount, and your buying power before you make your first offer.