What Is A Cash Out Refinance? How It Works & Pros/Cons

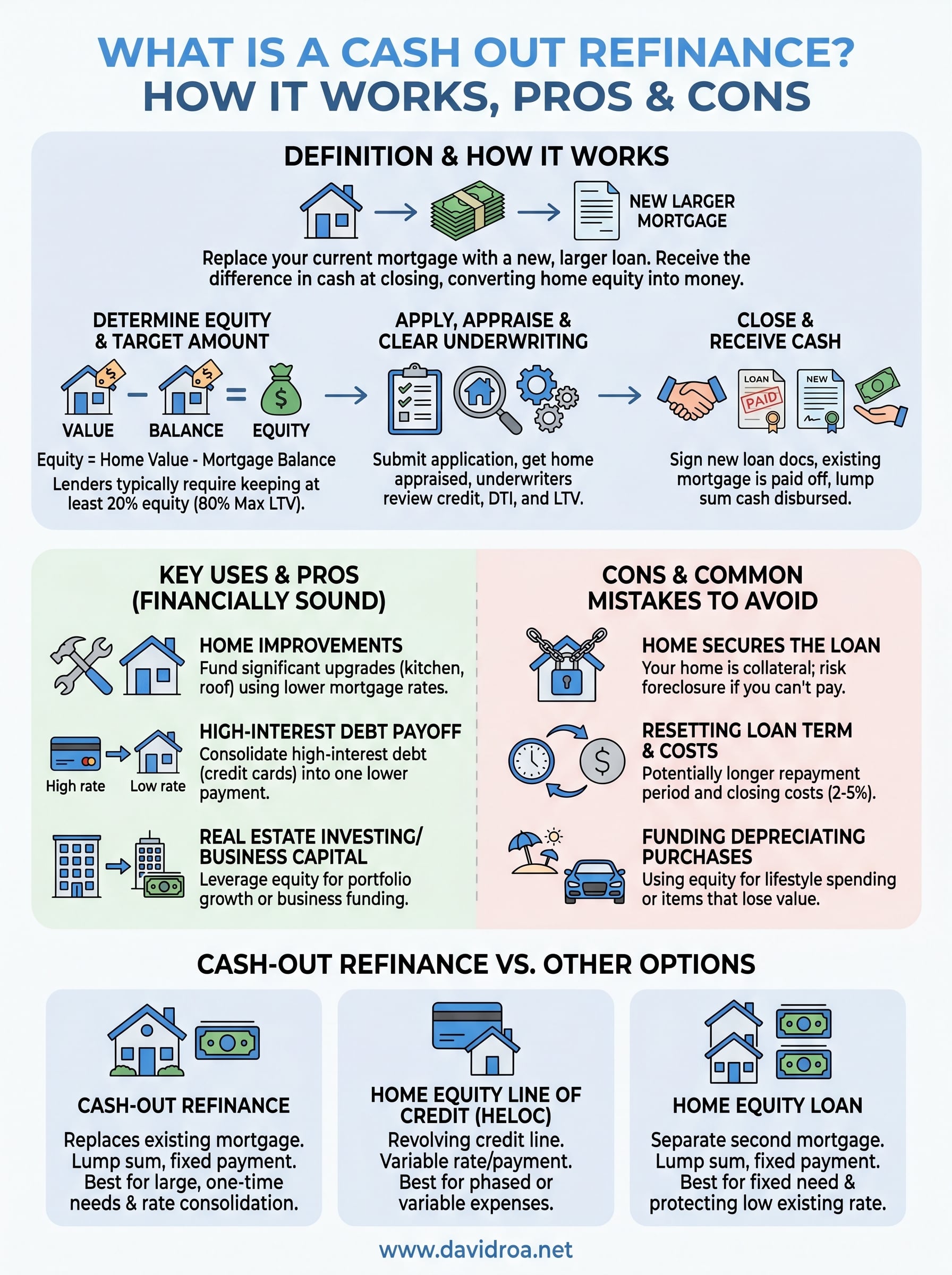

Your home has been building equity for years, maybe through rising property values, maybe through consistent mortgage payments. A cash out refinance lets you convert a portion of that equity into actual money you can use. It replaces your current mortgage with a new, larger loan and hands you the difference as cash at closing.

It sounds straightforward, but the details matter. How much equity do you need? What are the costs involved? Is it smarter than a home equity loan or a HELOC? These are the questions that trip people up, and getting them wrong can cost thousands.

At David Roa, we've helped homeowners and investors navigate refinancing decisions across over $150 million in funded loans. With more than 25 years in mortgage lending, and hands-on experience as a real estate investor, David understands both the numbers and the strategy behind pulling equity from a property.

This guide breaks down exactly how a cash out refinance works, who qualifies, and the real pros and cons you should weigh before moving forward.

Why homeowners use a cash-out refinance

Understanding what is a cash out refinance is one thing. Knowing why it makes sense for your specific situation is another. Homeowners tap into their equity for different reasons, and the right reason can make the transaction genuinely worthwhile. The wrong reason, or poor timing, can leave you with a larger loan balance and not much to show for it. Below are the most common and financially sound uses.

Home improvements and renovations

One of the most popular uses for cash-out refinancing is funding significant home improvements. Kitchen remodels, roof replacements, additions, and HVAC upgrades all carry high upfront costs that most homeowners can't cover from savings alone. By pulling equity through a refinance, you spread that cost over the life of the loan at mortgage interest rates, which are typically far lower than personal loans or credit cards.

There's also a financial logic to this approach. Improvements like updated kitchens, bathrooms, and energy-efficient systems tend to increase your home's value. You're using existing equity to potentially generate more equity, which works in your favor as long as you're not over-improving for your neighborhood.

Renovations funded through a cash-out refinance can increase your home's appraised value, which may benefit you in future refinances or sales.

Paying off high-interest debt

Credit card balances and personal loans routinely carry interest rates between 18% and 30%. Your mortgage, by comparison, is one of the lowest-cost borrowing tools available to you. Rolling high-interest debt into a cash-out refinance can reduce your monthly obligations and the total interest you pay over the life of the debt.

Discipline after the consolidation is the critical piece. Homeowners who use a cash-out refinance to pay down credit cards and then run those balances back up end up worse off than before. They now carry the same consumer debt plus a larger mortgage balance. If you treat debt consolidation through a refinance as a genuine reset and not a license to borrow more, it can meaningfully improve your financial position.

Real estate investing and business capital

Real estate investors frequently use cash-out refinancing as a tool for portfolio growth. You pull equity from one property and use it as a down payment on the next. Done correctly, this approach lets you scale your portfolio without waiting years to accumulate fresh capital from income alone. David Roa applies this same strategy in his own investment work, which is why he understands what makes it viable versus what makes it reckless.

Business owners represent another significant group who benefit from this approach. If you own your home and need working capital, equipment financing, or startup funds, a cash-out refinance can provide a lump sum at a rate far better than most business loans. The tradeoff is real: you're securing business risk against your home, so the business case needs to be solid and well-researched before you commit to this route.

A cash-out refinance works best when the money you pull out earns more than it costs in interest over time. Home improvements, high-interest debt payoff with renewed spending discipline, and well-researched investments all meet that standard. Funding vacations or depreciating purchases generally does not.

How a cash-out refinance works step by step

Once you understand what is a cash out refinance conceptually, seeing the mechanics in sequence helps you know what to expect and where the critical decisions happen. The process shares most steps with a standard refinance, but there are specific points where your equity position and loan-to-value ratio determine how the deal shapes up.

Step 1: Determine your equity and target loan amount

Your starting point is knowing how much usable equity you have. Subtract your current mortgage balance from your home's estimated market value. Most lenders require you to keep at least 20% equity in the property after the cash-out, so you're working with what's available above that threshold. For example, if your home is worth $400,000 and you owe $250,000, you have $150,000 in equity. With a 20% reserve requirement, your maximum new loan would be $320,000, leaving you with up to $70,000 in cash before closing costs are factored in.

Calculating your equity range before you apply prevents surprises when the official appraisal comes back and sets realistic expectations from the start.

Step 2: Apply, get appraised, and clear underwriting

You submit a full mortgage application with income documentation, tax returns, credit history, and property details. Your lender orders an independent appraisal, which establishes the official market value the entire loan is built around. Underwriters then review your debt-to-income ratio, credit score, and loan-to-value ratio to determine approval and final loan terms. This stage typically runs two to four weeks, though complex files or high-volume periods at the lender can extend the timeline.

Step 3: Close on the new loan and receive your cash

At closing, you sign the new loan documents and your existing mortgage gets paid off and replaced by the larger loan amount. Federal law grants you a three-business-day right of rescission on refinances secured by a primary residence, so your funds are disbursed after that window closes. Cash proceeds arrive as a lump sum by wire transfer or check. From that point forward, you make monthly payments on the new, higher loan balance at the rate locked in during your application.

Cash-out refinance requirements and limits

Before you apply, you need to know where you stand against the qualification thresholds lenders use. Part of understanding what is a cash out refinance is recognizing that the approval criteria are stricter than a standard rate-and-term refinance because you're increasing your loan balance and the lender carries more risk. Meeting the baseline numbers before you apply saves time and protects your credit from unnecessary hard inquiries.

Credit score and debt-to-income ratio

Your credit score sets the floor for what's available to you. Most conventional lenders want a minimum score of 620, though you'll access better rates and terms at 680 or higher. FHA cash-out refinances allow scores down to 600 in some cases, but the mortgage insurance costs associated with FHA loans affect your total cost of borrowing.

Your debt-to-income (DTI) ratio measures your total monthly debt payments against your gross monthly income. Most lenders cap DTI at 43% to 50% for cash-out refinances, and a lower ratio improves your rate. Factor in the new, higher mortgage payment when running your own numbers before applying.

Loan-to-value limits by loan type

The maximum cash you can pull out depends on your loan type and how much equity you're required to retain in the property after closing. Here's how the main programs compare:

| Loan Type | Max LTV (Loan-to-Value) | Equity You Must Retain |

|---|---|---|

| Conventional | 80% | 20% |

| FHA | 80% | 20% |

| VA (eligible veterans) | 90% | 10% |

| Jumbo | 70-75% (varies by lender) | 25-30% |

VA loans offer the most favorable LTV ceiling for eligible borrowers, which can unlock significantly more cash compared to conventional programs.

Seasoning requirements and property type

Seasoning rules determine how long you must own the property before a lender will approve a cash-out refinance. Most conventional lenders require 12 months of ownership before you can pull equity. Investment properties and second homes face tighter LTV caps than primary residences, typically 70% to 75% depending on the lender. Your property type and how long you've held it directly shape what's available to you, so confirm both factors early in the process.

Pros, cons, and common mistakes to avoid

Deciding whether a cash-out refinance is right for you requires an honest look at both sides. The benefits are real, but so are the costs and risks. Understanding what is a cash out refinance means going beyond the definition and examining what it actually does to your financial picture over time.

The real advantages

A cash-out refinance gives you access to large sums of capital at mortgage interest rates, which are consistently lower than credit cards, personal loans, or most business financing. You consolidate your borrowing into one structured monthly payment rather than juggling multiple obligations. For homeowners with significant equity, it can unlock funds for improvements, investments, or debt payoff that would otherwise take years to accumulate through savings alone.

The lower interest rate is only an advantage if you use the funds productively and don't extend your loan term longer than necessary.

The real drawbacks

The most significant risk is straightforward: your home secures the loan. If your financial situation changes and you can't make payments, the lender can foreclose. You're also resetting your mortgage term in most cases, which means paying more interest over the life of the loan even if your rate stays flat. On top of that, closing costs on a cash-out refinance typically run 2% to 5% of the new loan amount, which directly reduces the net cash you walk away with at the table.

Beyond the numbers, taking on a larger mortgage affects your overall debt load and monthly budget. You need to account for the higher payment alongside your other financial obligations, not just the immediate cash benefit you're receiving.

Common mistakes to avoid

Many borrowers treat cash-out proceeds as free money rather than borrowed capital. Pulling equity to fund lifestyle spending or depreciating purchases adds to your loan balance without building any financial position. A second costly mistake is ignoring the break-even point on your closing costs. If you plan to sell within two or three years, the costs of refinancing may easily outweigh any rate or cash benefit. Calculate how long you need to stay in the property for the transaction to make actual financial sense before you commit.

Cash-out refinance vs HELOC and other options

When you're deciding how to access your home equity, a cash-out refinance is one of three main options. Each product works differently, and choosing the wrong one for your situation adds unnecessary cost or risk. The right choice depends on how much you need, how long you plan to stay in the home, and whether you want a fixed or flexible structure.

Cash-out refinance vs HELOC

A Home Equity Line of Credit (HELOC) works more like a credit card backed by your home's equity. You draw from it as needed up to an approved limit, pay interest only on what you use, and repay over time. A cash-out refinance, by contrast, delivers one lump sum at closing and folds everything into a single monthly mortgage payment.

A HELOC suits variable, ongoing expenses like phased renovations, while a cash-out refinance suits large, one-time capital needs with a clear cost.

HELOCs typically carry variable interest rates, which means your payment can rise as rates increase. A cash-out refinance with a fixed rate locks your cost in for the life of the loan. If you're asking yourself what is a cash out refinance and whether it beats a HELOC, the honest answer is that it depends on how stable you need your monthly obligations to be.

Cash-out refinance vs home equity loan

A home equity loan is a separate second mortgage that sits on top of your existing loan. You receive a lump sum and repay it at a fixed rate over a set term, but your original mortgage stays in place. You end up managing two separate loan payments rather than one.

A cash-out refinance replaces your mortgage entirely, which simplifies your payment structure. The tradeoff is that you pay closing costs on the full new loan amount, not just the equity you're pulling out. If your current mortgage rate is meaningfully lower than today's rates, keeping it intact through a home equity loan or HELOC may cost you less over time than refinancing the entire balance at a higher rate.

When each option makes sense

Choose a cash-out refinance when you need a large lump sum, want a single fixed payment, and current rates are equal to or better than your existing rate. Choose a HELOC when your expenses are staggered or uncertain and you want flexibility. Choose a home equity loan when you need a fixed amount but want to protect a low rate on your current mortgage.

| Option | Structure | Best For |

|---|---|---|

| Cash-out refinance | Replaces existing mortgage | Large one-time needs, rate consolidation |

| HELOC | Revolving credit line | Phased or variable expenses |

| Home equity loan | Second mortgage, fixed | Fixed need, protecting existing rate |

Next steps

Now that you understand what is a cash out refinance, the gap between knowing the concept and making the right decision for your situation comes down to the specifics: your equity position, your current rate, your credit profile, and what you plan to do with the funds. Each of those variables shifts the math, and getting the calculation wrong can cost you thousands over the life of the loan.

Before you apply anywhere, run your numbers honestly. Know your home's approximate value, your remaining balance, and your target loan amount. Think through your exit timeline and whether closing costs make financial sense given how long you plan to stay in the property. If any part of the analysis feels unclear, working with an experienced lender saves you from costly missteps.

David Roa brings over 25 years of mortgage and investment experience to every conversation. Talk to David about your refinance options and get a clear picture of what's possible for your specific situation.