When Should You Refinance Your Mortgage? 7 Key Signs & Math

Refinancing sounds straightforward, swap your current mortgage for one with better terms, but the timing makes or breaks the deal. Knowing when should you refinance your mortgage comes down to real numbers, not gut feelings. Get it right, and you save tens of thousands over the life of your loan. Get it wrong, and you're paying closing costs for a move that barely moves the needle.

The challenge is that there's no single universal trigger. Your break-even point, your remaining loan term, your credit profile, and where rates currently sit all factor into the equation. What works for your neighbor might cost you money. That's why a clear framework, not a vague rule of thumb, matters here.

Over 25 years of funding residential mortgages at David Roa, I've walked hundreds of homeowners through this exact decision. With more than $150 million in loans closed, I've seen when refinancing pays off handsomely and when clients are better off staying put. Below, I'll break down seven specific signs it's time to refinance, the math behind each one, and the real-world scenarios where the numbers actually work in your favor.

What refinancing changes and why timing matters

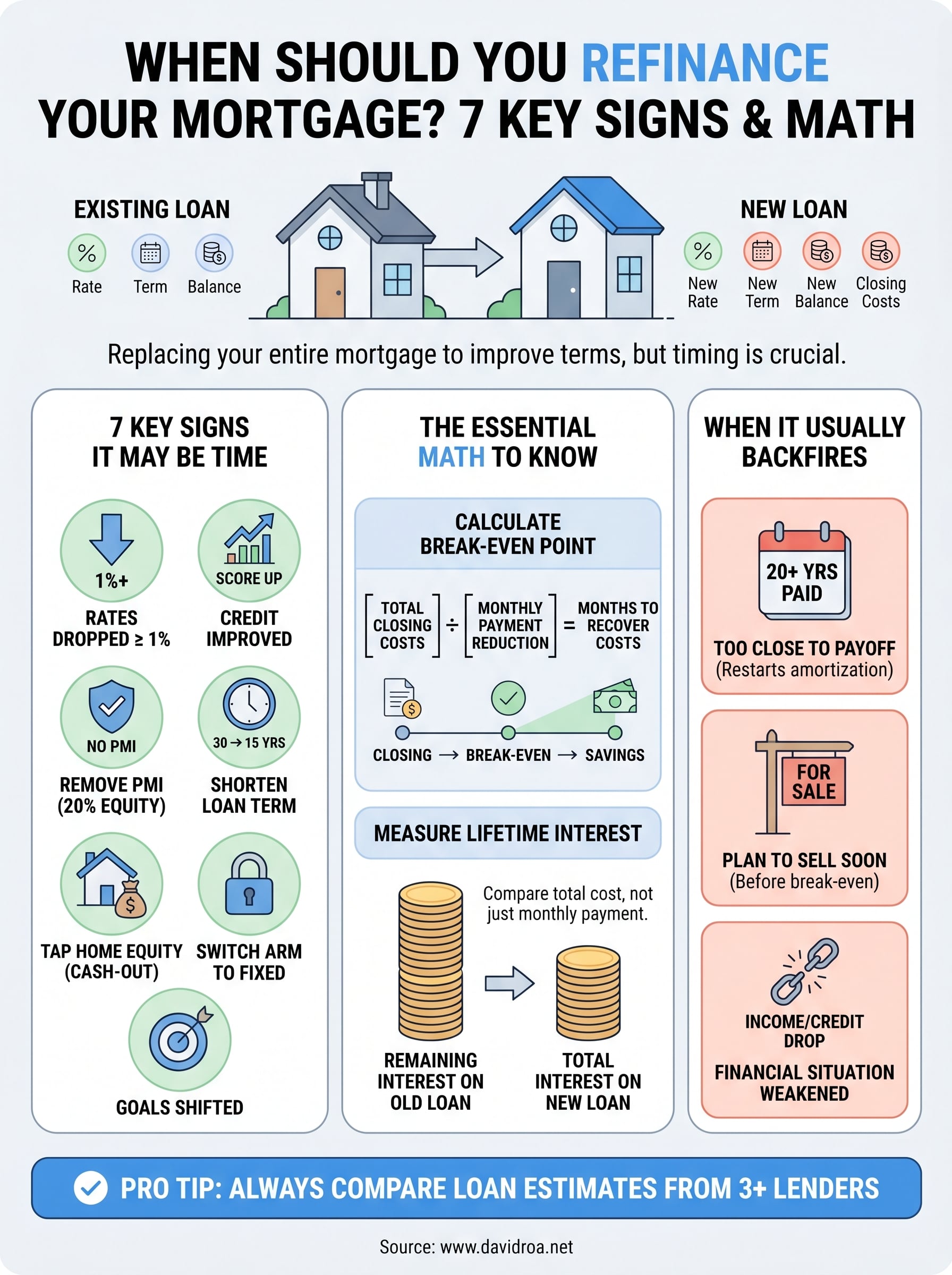

When you refinance, you're not simply swapping one rate for another. You're replacing your entire existing mortgage with a brand-new loan that carries its own interest rate, loan term, principal balance, and closing costs. Each of those components shifts simultaneously, which means a refinance that looks attractive on the surface can still hurt you if the timing doesn't line up with your financial situation.

The four components that shift in a refinance

Most homeowners focus on the rate drop and stop there. But your monthly payment is the output of at least four inputs working together: the new interest rate, the loan term, the principal balance (which may include rolled-in closing costs), and the amortization schedule that restarts from day one. Ignore any one of these, and you can easily misjudge whether the deal actually benefits you.

Here's how each component plays out:

- Interest rate: A lower rate directly reduces your monthly payment and the total interest you pay over the life of the loan.

- Loan term: Resetting to a new 30-year term lowers your monthly payment but extends how long you carry debt and increases lifetime interest paid.

- Principal balance: If you roll closing costs into the loan, you borrow more, which offsets some of the savings from a lower rate.

- Amortization schedule: Early loan payments are heavily weighted toward interest. If you refinance mid-loan, you restart that interest-heavy portion of the schedule.

Resetting a 10-year-old mortgage back to a 30-year term often costs more in total interest than keeping the original loan, even when the new rate is a full percentage point lower.

Why the timing of a refinance changes everything

The same rate drop can produce very different outcomes depending on where you are in your current loan term. If you refinanced last year and rates dip again today, a second refinance might not cover the new round of closing costs before you hit break-even. On the other hand, if you bought your home when rates were significantly higher and your credit score has improved since then, even a moderate rate reduction can translate to hundreds of dollars in monthly savings.

Timing also depends on how long you plan to stay in the home. Refinancing carries upfront costs, typically between 2% and 5% of the loan amount according to the Consumer Financial Protection Bureau. If you sell before your monthly savings exceed those closing costs, the refinance produced a net loss. That break-even point is the most important number in the entire decision, and you need to calculate it before you apply.

How market conditions factor into the decision

Mortgage rates don't move on a predictable schedule, and waiting for a perfect low is a strategy that costs many homeowners real money. Rather than trying to time the market, the smarter approach is evaluating whether today's rate creates a clear, calculable benefit given your specific loan balance, remaining term, and credit profile. Rates respond to Federal Reserve policy decisions, Treasury yield movements, and broader economic conditions, all of which can shift within a single quarter.

Understanding when should you refinance your mortgage starts here: know precisely what your current loan structure looks like, then measure every proposed change against that baseline. A refinance is only valuable when the numbers support it, not when the headlines suggest rates are dropping.

The math to know before you refinance

Before you submit a single application, you need three specific calculations. These numbers tell you whether a refinance actually improves your position or simply moves costs around. Skipping this step is the most common reason homeowners end up disappointed after closing.

Calculate your break-even point

Your break-even point is the number of months it takes for your monthly savings to recover the upfront closing costs. To find it, divide your total closing costs by your monthly payment reduction. If closing costs run $6,000 and your new payment is $200 lower per month, your break-even point is 30 months. If you plan to sell or refinance again before month 30, you lose money on this transaction, full stop.

A refinance only makes financial sense when you're confident you'll stay in the home long enough to pass the break-even point.

Here's the formula laid out simply:

- Break-even (months) = Total closing costs / Monthly payment reduction

- Closing costs typically range from 2% to 5% of your loan balance

- Monthly savings = Current payment minus new proposed payment (principal and interest only)

Measure the lifetime interest difference

Monthly savings get most of the attention, but total interest paid over the life of the loan is often a larger number and a more important one. Pull out your current amortization schedule and compare the remaining interest you owe against what you'd pay under the new loan's full term. If you reset a 30-year loan at year 10, you restart interest-heavy payments that you've already partially worked through.

Use this comparison to make a complete decision. Knowing when should you refinance your mortgage means looking at two timelines simultaneously: how quickly you recover closing costs month-to-month, and whether the new loan's total cost beats your original loan's remaining cost. A shorter loan term, such as moving from a 30-year to a 15-year mortgage, often reduces total interest dramatically even if the monthly payment rises. Run both scenarios with your actual numbers before committing to any refinance offer.

Seven signs it may be time to refinance

Knowing when should you refinance your mortgage gets clearer with a concrete checklist. Each sign below represents a scenario where the financial math typically works in your favor, though you still need to run your specific numbers before committing to any new loan.

- Rates have dropped at least 1% below your current rate: A full percentage point reduction usually generates enough monthly savings to justify closing costs within a reasonable break-even window.

- Your credit score has improved significantly: Moving from a 640 to a 740+ score can unlock much better rate tiers, even in a stable rate environment.

- You want to switch from an ARM to a fixed rate: If your adjustable-rate mortgage is approaching its reset period, locking in a fixed rate protects you from future payment increases.

- You need to remove private mortgage insurance: Once you've built 20% equity, refinancing into a conventional loan eliminates PMI and reduces your monthly payment.

- You want to shorten your loan term: Refinancing from a 30-year to a 15-year mortgage builds equity faster and cuts total interest paid dramatically.

- You need to tap home equity: A cash-out refinance lets you access accumulated equity for renovations or debt consolidation, provided the new rate and payment still make financial sense.

- Your financial goals have shifted: If your income has grown or your priorities changed, restructuring your mortgage can align your largest monthly expense with your current plan.

When multiple signs apply at once

When several signs apply simultaneously, your case for refinancing strengthens considerably. If rates have fallen and your credit score has improved, you might qualify for a rate two full percentage points below your current one, and that combination cuts your break-even timeline dramatically, often from 36 months to under 18.

If two or more signs apply to your situation, treat that as a strong signal to get a formal rate quote before the window closes.

| Signs present | Likely break-even range |

|---|---|

| Rate drop only | 24-36 months |

| Rate drop + credit improvement | 12-24 months |

| Rate drop + shorter term | Varies by equity |

| Three or more signs | Under 18 months |

When refinancing usually backfires

Refinancing isn't automatically a smart move just because rates have dipped. Several specific scenarios consistently produce outcomes where homeowners pay more than they would have by staying with their original loan. Understanding when should you refinance your mortgage also means knowing when the math clearly doesn't support it.

You're too close to paying off your loan

If you've been paying your mortgage for 20 or more years, the math rarely favors a refinance. Most of your current payments go toward principal now, not interest, because that's how amortization works. Resetting to a new 30-year loan means you restart the interest-heavy phase of repayment all over again, and the total cost comparison almost always shows you'd pay more over time, even with a lower rate.

A shorter term like a 15-year option might still make sense here, but only if the monthly payment fits your budget and your break-even window falls under two years. Always run the full lifetime interest comparison, not just the monthly payment difference, before you commit to anything.

You plan to sell the home soon

Closing costs on a refinance typically run between 2% and 5% of your loan balance, and you need enough time in the home to recover those costs through monthly savings. If you're planning to sell within the next two to three years, you likely won't reach your break-even point before the home changes hands.

Refinancing into a lower rate six months before listing your home almost always costs you money rather than saving it.

Your credit or income situation has weakened

Lenders price loans based on risk at the time of application. If your credit score has dropped, your debt-to-income ratio has climbed, or your employment situation has changed since you got your original mortgage, the rate you'll qualify for today may be no better than your current one, and possibly worse. Refinancing in that condition only adds closing costs without improving your terms. Rebuild your financial profile first, then revisit the decision from a stronger position.

How to refinance step by step

Once you've confirmed the math supports a refinance, the process moves in a predictable sequence. Knowing exactly what to expect at each stage helps you move efficiently and avoid the common mistake of accepting the first offer you receive, which is precisely where many homeowners trying to answer when should you refinance your mortgage end up leaving the largest savings on the table.

Pull your financial documents together first

Before you contact any lender, gather the core documents every underwriter will request: two years of tax returns, recent pay stubs, and bank statements from the last two to three months, along with your current mortgage statement. Having these ready before you start comparing offers speeds up the process and gives lenders a complete picture of your financial position from the first conversation.

Your credit report matters just as much as your income documents. Pull a free copy through the Annual Credit Report service authorized by federal law, review it for errors, and dispute anything inaccurate before you apply. A corrected error can shift your score enough to qualify you for a meaningfully better rate tier.

Compare offers from at least three lenders

Shopping multiple lenders is where most homeowners leave real money on the table. Each lender sets its own pricing, and the spread between the best and worst offer in a given week can be meaningful. Request a Loan Estimate from each lender, which federal law requires within three business days of your application, and compare the same line items across every quote.

Comparing Loan Estimates side by side is the single most effective step you can take to reduce your total refinance cost.

Review these specific items on each Loan Estimate:

- Interest rate and APR

- Total closing costs

- Loan term

- Prepaid items and escrow setup costs

Lock your rate and move through underwriting

Once you select a lender, lock your interest rate in writing with a specific expiration date, typically 30 to 60 days. The rate lock protects you from market movement while underwriting proceeds. During this phase, the lender verifies your income, assets, employment, and property value through a formal appraisal. Respond to any document requests within 24 to 48 hours to avoid delays that push you past your lock expiration.

Closing follows a successful underwriting review. At the closing table, you sign the new loan documents and cover any remaining closing costs, your old mortgage gets paid off and replaced, and your first payment on the new loan typically comes due 30 to 45 days after closing.

Next steps

Knowing when should you refinance your mortgage gives you a real advantage, but the knowledge only pays off when you act on it with accurate numbers. Start by calculating your break-even point using your current loan balance and the rate you'd likely qualify for today. If that window falls under 24 months and two or more of the seven signs apply to your situation, you have a strong case to move forward.

Your next concrete step is comparing at least three lender quotes side by side using the Loan Estimate documents each lender is required to provide. Do not accept the first offer on the table. The difference between offers can represent thousands of dollars over your loan term.

Experience and access to multiple loan programs make a measurable difference in the outcome you get. If you want a direct review of your current mortgage and a clear picture of your options, connect with David Roa today.