DSCR Loan Requirements: Credit Score, Down Payment & DSCR

Real estate investors have a problem: traditional mortgage lenders want W-2s, tax returns, and proof of personal income. But what if your strategy relies on rental cash flow, not a paycheck? That's exactly where DSCR loans come in, and understanding the DSCR loan requirements before you apply can save you time, money, and frustration.

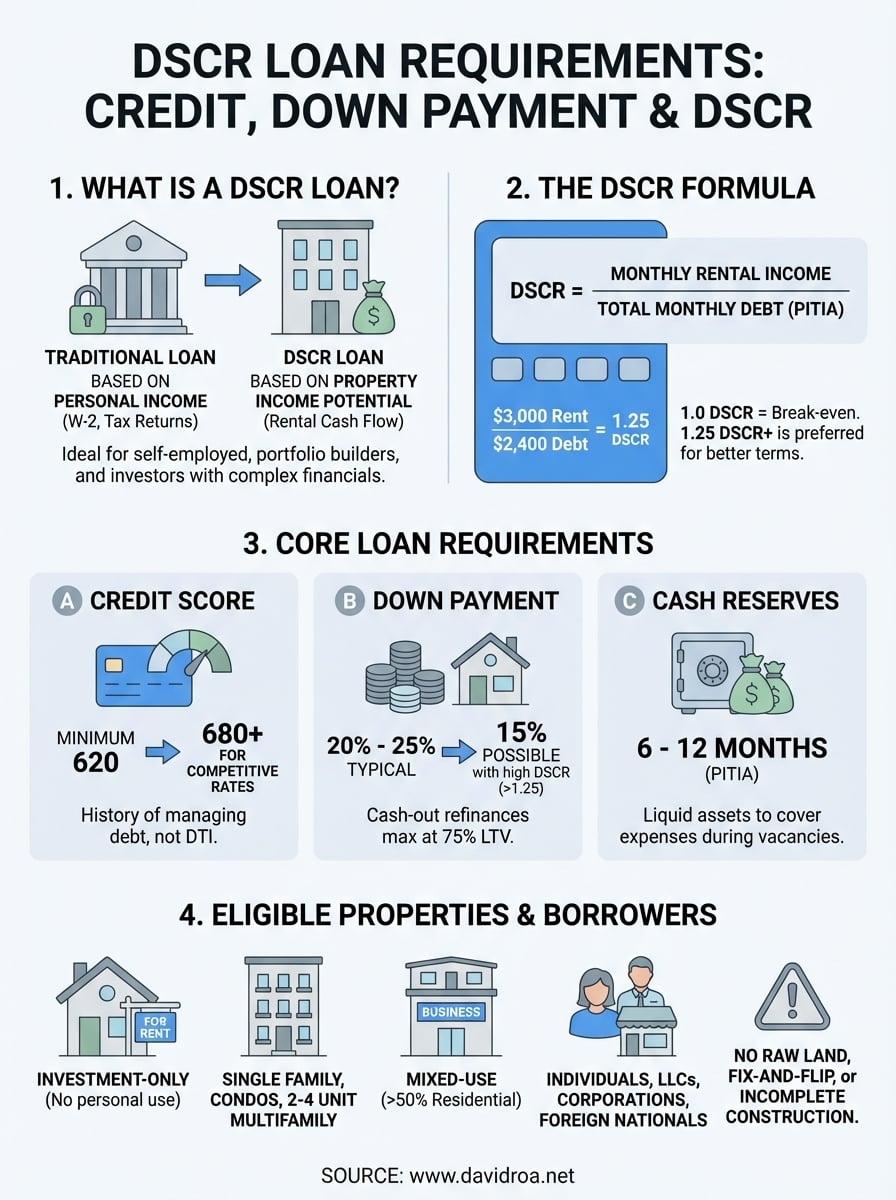

A DSCR (Debt Service Coverage Ratio) loan qualifies you based on the property's income potential, not your personal financials. This makes it a go-to option for investors building portfolios, self-employed borrowers, or anyone whose tax returns don't reflect their true buying power. But these loans aren't a free pass, lenders still have specific criteria around credit scores, down payments, and the ratio itself.

With over 25 years in lending and $150 million funded, I've helped hundreds of investors secure DSCR financing for rentals, mixed-use properties, and portfolio expansions. This guide breaks down exactly what you need to qualify, no guesswork, no fluff. Whether you're eyeing your first investment property or adding to an existing portfolio, you'll walk away knowing precisely where you stand and what lenders expect.

Why DSCR loans matter for investors

Traditional mortgage underwriting forces you into a box that doesn't fit real estate investors. Banks want two years of tax returns showing consistent W-2 income, stable employment history, and debt-to-income ratios that cap out around 43%. If you're self-employed, write off business expenses aggressively, or your strategy involves scaling a portfolio quickly, you're often disqualified before you start. That's the fundamental problem DSCR loans solve.

Traditional lending creates investor roadblocks

Conventional lenders evaluate you as a homeowner, not an investor. They calculate your personal income, subtract all your existing debts (including mortgages on other properties), and determine if you personally can afford the new loan. This approach ignores one critical fact: your rental properties generate their own income. A fourplex pulling in $6,000 monthly might easily cover its $4,200 mortgage, but if your personal debt-to-income ratio is maxed out, traditional underwriting rejects the deal. You're penalized for portfolio growth instead of rewarded for it.

DSCR loans flip the script by qualifying properties based on their cash flow, not your paystubs.

Who benefits most from DSCR financing

You'll find DSCR loans particularly valuable if you're a self-employed investor whose tax returns show minimal income after deductions. Real estate agents, contractors, and business owners often write off legitimate expenses that tank their qualifying income on paper. DSCR financing looks past those returns and focuses on what the property earns, not what you reported to the IRS. Portfolio investors building multiple properties within a year also benefit since traditional lenders typically cap you at four to ten financed properties, while DSCR programs allow unlimited investment properties. Foreign nationals and ITIN holders face even steeper barriers with conventional loans, but DSCR lenders evaluate the asset's performance, making citizenship status irrelevant. Understanding the basic dscr loan requirements upfront helps you position your deal correctly and avoid wasted applications.

DSCR loan requirements at a glance

DSCR lenders evaluate you differently than traditional banks, but you still need to meet specific benchmarks. The core dscr loan requirements center on three pillars: the property's cash flow ratio, your credit profile, and your down payment capacity. Most programs require a minimum 1.0 DSCR, meaning the property's rental income equals or exceeds the monthly mortgage payment, though some lenders accept ratios as low as 0.75 with compensating factors like larger down payments or stronger credit.

Credit and down payment minimums

You'll typically need a credit score of at least 620 to qualify, though competitive rates start around 680. Lenders view your credit history as proof you manage debt responsibly, even if they're not scrutinizing your personal income. Down payments generally range from 20% to 25% for investment properties, with some programs allowing 15% if your DSCR exceeds 1.25. Cash reserves matter too, expect lenders to verify you have six to twelve months of property expenses (PITIA: principal, interest, taxes, insurance, and association fees) sitting in liquid accounts.

Lower DSCR ratios require higher down payments and better credit scores to offset lender risk.

Property and documentation basics

Your property must be a completed, habitable investment property, no fix-and-flips or properties under construction. Single-family homes, condos, townhomes, and small multifamily units (two to four units) all qualify. Lenders require a current appraisal and lease agreements or rent schedules proving the property generates income. If the property is vacant, they'll use market rent analysis from the appraisal to calculate DSCR.

How lenders calculate DSCR and rent

Lenders use a straightforward formula to determine if your property qualifies: they divide the monthly rental income by the total monthly debt obligation (mortgage payment plus taxes, insurance, and HOA fees). This ratio tells them whether the property generates enough cash flow to cover its expenses. A DSCR of 1.25 means the property earns $1.25 for every $1.00 of debt, giving the lender a 25% cushion against vacancies or market shifts.

The DSCR formula explained

You calculate DSCR by taking the gross monthly rent and dividing it by your PITIA (principal, interest, taxes, insurance, and association dues). If your property rents for $3,000 monthly and your total payment is $2,400, your DSCR equals 1.25 ($3,000 ÷ $2,400). Lenders typically multiply your monthly rent by 0.75 to account for vacancy and maintenance, so that $3,000 becomes $2,250 in adjusted income, dropping your DSCR to 0.94. This adjustment varies by lender, some use 80% or skip it entirely for long-term leases with established tenants.

The vacancy adjustment can make or break your loan approval, so confirm your lender's exact calculation method upfront.

How rental income gets verified

Lenders verify rent through existing lease agreements showing current market rates and tenant occupancy. If the property sits vacant or you're refinancing, they'll use the appraisal's rent schedule, which compares your property to similar units in the area. Some aggressive dscr loan requirements allow you to use projections for properties under renovation, but most programs stick to documented income or appraised market rents. Short-term rental income from platforms requires 12 to 24 months of documented earnings to qualify.

Credit score, down payment, and cash reserves

Your financial profile determines not just approval, but the interest rate you'll pay and the loan terms you'll receive. DSCR lenders tier their pricing based on credit scores, down payments, and liquid reserves, meaning stronger qualifications translate directly into lower rates and more flexible options. These three components work together as your personal risk profile, separate from the property's DSCR calculation.

Credit score thresholds and pricing

Most DSCR programs accept credit scores as low as 620, but you'll pay premium rates at that level. Competitive pricing starts around 680, with the best terms reserved for scores above 720. Lenders pull your credit to verify payment history on existing mortgages, credit cards, and installment loans, but they won't calculate debt-to-income ratios like traditional banks. If you're sitting between 620 and 679, expect rate adjustments of 0.5% to 1.5% compared to higher-score borrowers.

Down payment and equity requirements

Standard dscr loan requirements call for 20% to 25% down on investment properties, though some lenders drop to 15% if your DSCR exceeds 1.25. Refinances require at least 25% equity in the property based on current appraised value. Cash-out refinances typically max out at 75% loan-to-value, leaving you with 25% equity after pulling funds. Larger down payments can offset weaker credit or lower DSCR ratios, giving you flexibility to structure deals around your strengths.

Cash reserves prove you can weather vacancies, repairs, or market downturns without defaulting on the loan.

Documented cash reserves

Lenders require six to twelve months of property-specific reserves in liquid accounts (checking, savings, money market funds). They calculate this by multiplying your monthly PITIA payment by the required months of reserves. A $2,400 monthly payment requires $14,400 to $28,800 in documented funds. Retirement accounts like 401(k)s typically count at 60% to 70% of their value since early withdrawals carry penalties.

Property, borrower, and entity eligibility

DSCR lenders care about three things: property type, occupancy status, and ownership structure. Your investment property must meet specific criteria before any lender evaluates your DSCR ratio or credit profile. These dscr loan requirements exclude properties lenders consider speculative, incomplete, or difficult to liquidate if the loan defaults.

Property type restrictions

You can finance single-family homes, condos, townhomes, and two-to-four unit multifamily properties with DSCR loans. Mixed-use buildings qualify if the residential portion exceeds 50% of the total square footage. Lenders reject raw land, properties under construction, and active fix-and-flip projects requiring permits or major renovations. Your property must be completed, habitable, and generating rental income (or ready to rent within 30 days). Warrantable condos in projects with HOA approval meet guidelines, but non-warrantable units in buildings with commercial litigation or incomplete construction don't qualify.

Properties must be investment-only, you cannot occupy a DSCR-financed property as your primary residence or second home.

Borrower and ownership structures

DSCR lenders accept individual borrowers, married couples, and business entities like LLCs, corporations, and trusts. Holding properties in an LLC protects your personal assets from liability, and most DSCR programs allow this without requiring personal guarantees beyond your credit check. Foreign nationals and ITIN holders qualify since lenders focus on the property's cash flow rather than citizenship status. You'll need a U.S.-based property and bank accounts for loan servicing, but your residency doesn't disqualify you. Partnerships and multi-member LLCs work, though some lenders cap the number of borrowers at four per loan.

Next steps

You now understand the complete picture of dscr loan requirements: credit scores starting at 620, down payments of 20% to 25%, and cash reserves covering six to twelve months of expenses. More importantly, you know how lenders calculate your DSCR ratio and what property types qualify. This knowledge puts you ahead of most investors who waste time applying for loans they don't qualify for or accepting terms they could have negotiated better.

Your immediate action depends on where you stand. If you're evaluating a specific property, calculate its DSCR using the rental income divided by total monthly debt. Pull your credit report to confirm your score meets minimum thresholds. Gather documentation for your cash reserves and organize existing lease agreements or market rent data. Contact me directly if you need a lender who understands investor financing, I've funded over $150 million in investment properties and can tell you within 24 hours if your deal qualifies.