Fannie Mae Conforming Loan Limit: 2026 Baseline Vs High-Cost

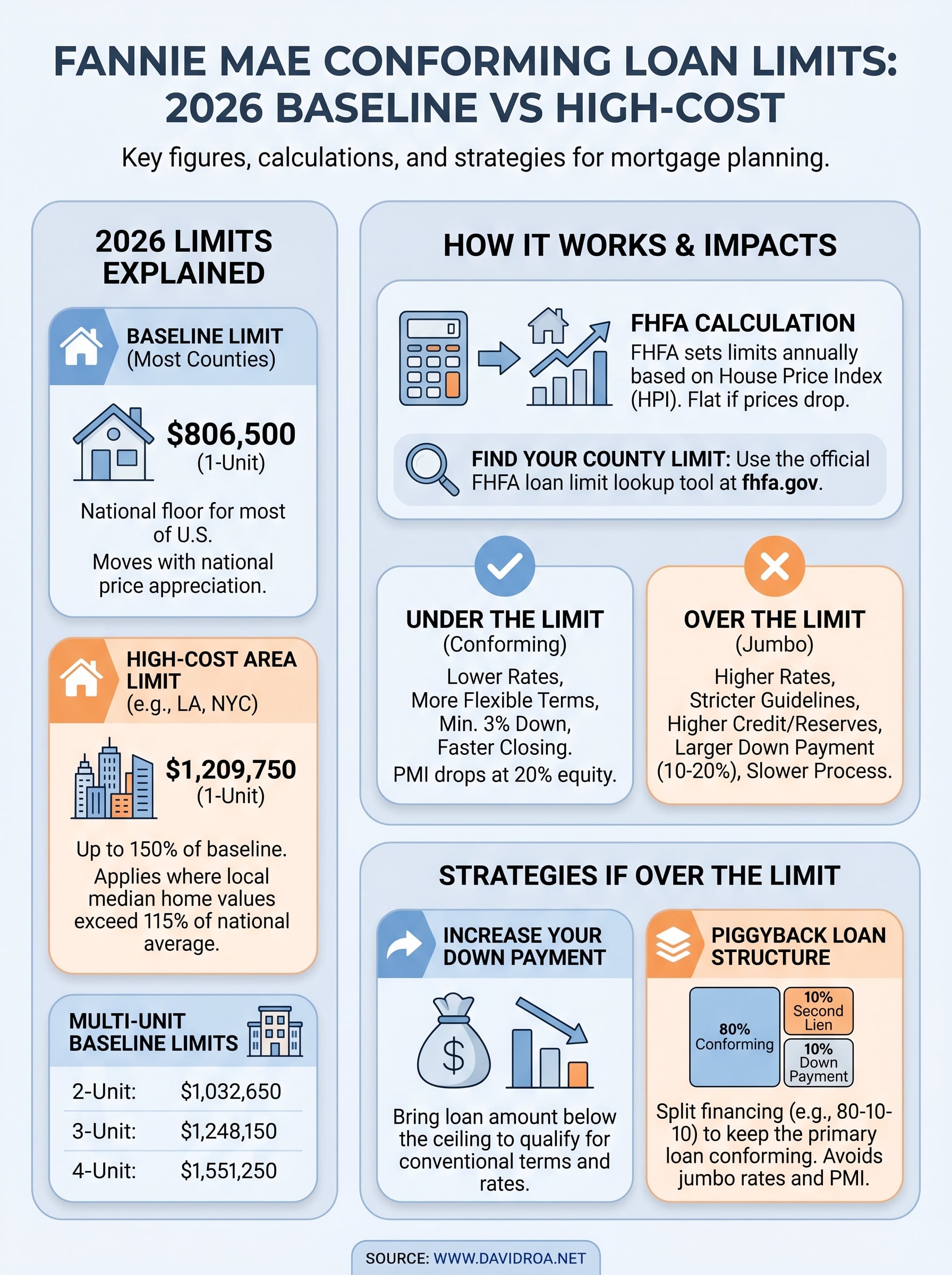

The Fannie Mae conforming loan limit determines the maximum mortgage amount you can borrow before your loan gets classified as a jumbo product, which typically means stricter qualification requirements and higher interest rates. For 2026, the baseline limit sits at $806,500 for most counties across the United States, while high-cost areas allow borrowing up to $1,209,750 on a single-unit property.

These numbers matter more than most buyers realize. A few thousand dollars above the limit can push you into a completely different loan category, changing your rate, your down payment, and your closing timeline. Whether you're purchasing your first home or adding to an investment portfolio, knowing exactly where your county falls on the conforming scale helps you structure a smarter deal.

With over 25 years originating residential mortgages and more than $150 million funded, I've walked clients through every version of these annual limit changes. Below, I break down the 2026 baseline and high-cost figures, explain how FHFA calculates them by county and property type, and show you how to use this information when planning your next purchase.

What the 2026 conforming loan limits are

The 2026 Fannie Mae conforming loan limit sets the ceiling on what Fannie Mae and Freddie Mac can buy from lenders on the secondary market. The baseline limit for a single-unit property is $806,500, which applies to the majority of counties across the contiguous United States. Alaska, Hawaii, Guam, and the U.S. Virgin Islands get higher baseline figures because of elevated construction and land costs that have applied to those areas for decades.

Baseline limits by property type

Your limit doesn't just depend on your county. It also scales based on how many units the property has. If you're buying a duplex, triplex, or four-unit building as an owner-occupant, your conforming ceiling jumps considerably above what a single-family buyer gets.

| Property Type | 2026 Baseline Limit |

|---|---|

| 1-Unit | $806,500 |

| 2-Unit | $1,032,650 |

| 3-Unit | $1,248,150 |

| 4-Unit | $1,551,250 |

These figures represent the floor for most U.S. counties, not the ceiling for every buyer. Where you purchase matters as much as what you purchase.

High-cost area limits

In counties where home prices run well above the national median, the FHFA raises the conforming ceiling to 150% of the baseline, which brings the 2026 cap to $1,209,750 for a single-unit property. Markets like Los Angeles, San Francisco, New York City, and parts of the Seattle and Denver metros all fall under this higher threshold.

In a high-cost county, you may qualify for a conforming loan at an amount that would be classified as jumbo in most other parts of the country, which can mean a meaningfully lower rate.

Multi-unit properties in these high-cost designated counties receive proportionally higher limits as well, giving investors and owner-occupants in expensive markets significantly more room before crossing into jumbo territory.

How FHFA sets limits and why counties vary

The Federal Housing Finance Agency (FHFA) publishes updated conforming loan limits each November, with new figures taking effect the following January. The agency uses its own House Price Index (HPI) to measure how much national home values changed over the prior four quarters, then applies that percentage increase to the existing baseline. If home prices drop nationally, the limit holds flat rather than decreasing.

The fannie mae conforming loan limit moves in direct proportion to national price appreciation, not local market swings at the baseline level.

Why your county's limit may be higher

Individual counties receive elevated limits when local median home values exceed 115% of the national baseline. The FHFA calculates this county-by-county using local price data, which is why a county in coastal California can carry a $1,209,750 ceiling while a neighboring inland county stays at $806,500.

Metropolitan statistical areas sometimes get treated as a single unit, meaning one high-priced county can pull its neighbors into the high-cost designation. Checking your specific county before you assume you fall under the baseline limit is worth the two minutes it takes, because the difference can be hundreds of thousands of dollars in borrowing room.

How to find your county limit fast

The fastest way to check your county's ceiling is to go directly to the FHFA's official loan limit lookup tool at fhfa.gov. You enter your state and county, and the tool returns the current conforming limit for one- through four-unit properties in a single view. No registration required, no calculation needed.

Checking your specific county limit before you start shopping saves you from structuring an offer around a loan amount that pushes you into jumbo territory at the last minute.

Using the FHFA lookup tool

The FHFA updates this tool each November after publishing the new figures. You select your state and county from dropdown menus, and the result appears immediately with limits broken out by property type.

The fannie mae conforming loan limit numbers on that page are exactly what lenders reference when underwriting your file. This lookup takes about two minutes and gives you a precise number rather than a rough estimate based on where you think your market falls.

Confirming the number with your loan officer

Your loan officer can cross-reference the county figure against your loan amount and down payment to tell you right away whether you qualify under conforming guidelines. Sharing the FHFA result before you make an offer gives you and your agent the clarity to structure a competitive bid without surprises at underwriting.

How limits affect your loan options

Staying under the fannie mae conforming loan limit gives you access to the broadest range of mortgage products and competitive rates available. Lenders price conforming loans tighter because Fannie Mae and Freddie Mac absorb the secondary market risk, which means lower rates and more flexible qualification terms flow through to borrowers who qualify under that ceiling.

When you stay under the limit

Keeping your loan at or below your county's conforming ceiling opens up conventional programs including fixed 30-year, 15-year, and adjustable-rate options with standard underwriting guidelines. Your minimum down payment can be as low as 3% on a primary residence, and private mortgage insurance drops off automatically once you reach 20% equity in the property.

Conforming loans also tend to close faster than jumbo products because they follow standardized guidelines that most lenders process routinely.

When you cross the threshold

Borrowing even $1 above the limit immediately reclassifies your loan as jumbo financing, which carries a separate set of requirements. Most jumbo lenders require higher credit scores and larger cash reserves, along with a down payment that typically runs between 10% and 20% before they approve the file. Your rate will also likely be higher, which adds real cost over a 30-year term.

Strategies if your loan amount is over the limit

If your purchase price pushes your loan above the fannie mae conforming loan limit, you have real options that don't automatically mean accepting jumbo rates. The right move depends on how far over the limit you land and how much cash or flexibility you bring to the table.

Increase your down payment

Putting more money down is the most direct way to pull your loan amount back under the conforming ceiling. If you're $30,000 above the limit, adding that amount to your down payment keeps you in conventional territory and preserves access to lower rates and standard underwriting guidelines. This approach works best when you have liquid reserves that don't wipe out your post-closing cushion.

A larger down payment that keeps you conforming can cost you less over 30 years than carrying a smaller down payment at a jumbo rate.

Use a piggyback loan structure

A piggyback loan splits your financing into a primary conforming mortgage and a second lien, keeping the first loan under the county limit. Your lender structures an 80-10-10 or similar combination so you avoid both jumbo classification and private mortgage insurance at the same time. Ask your loan officer about current second-lien pricing before you commit to this structure, since the blended rate needs to beat what a single jumbo loan would cost you.

Where to go from here

You now have the 2026 baseline and high-cost figures, the logic behind how the FHFA calculates county-level limits, and a set of practical strategies to work around the ceiling when your loan amount runs over. The fannie mae conforming loan limit isn't a wall, it's a threshold you can plan around with the right structure and the right lender in your corner.

Your next step is simple: look up your county's specific limit on the FHFA tool, match it against your target purchase price and expected down payment, and bring both numbers to a conversation with your loan officer before you start writing offers. That sequence takes less than an hour and eliminates most of the surprises that slow deals down at underwriting.

If you want a direct answer on where you stand, reach out to David Roa and get your loan options mapped out before you make your next move.