FHA Debt-To-Income Ratio Limits: 31/43, 50%+ Exceptions

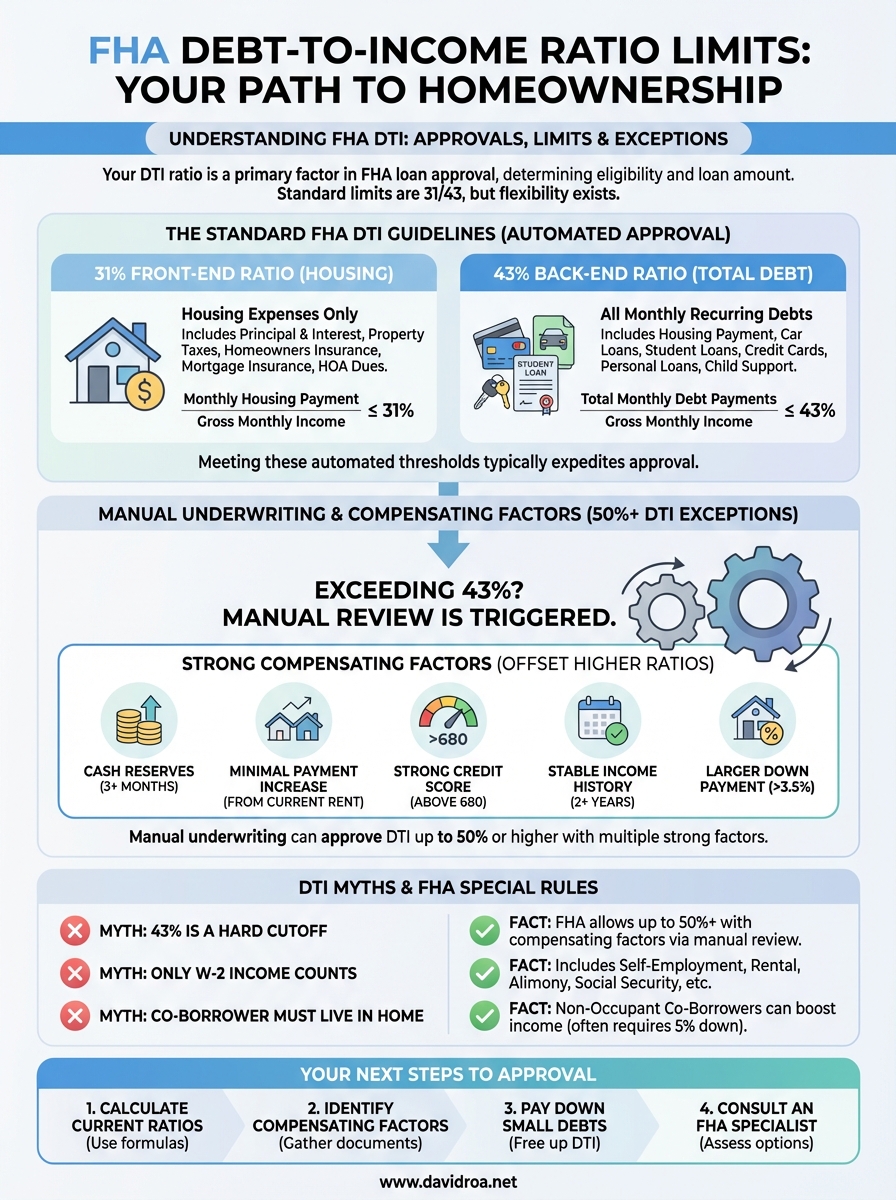

Your monthly debt payments directly determine whether you qualify for an FHA loan. Lenders use FHA debt-to-income ratio limits to measure how much of your income goes toward housing costs and total debts, and these numbers carry real weight in approval decisions. The standard guidelines set caps at 31% for housing expenses and 43% for total monthly debt, but the actual picture is more flexible than most borrowers realize.

With over 25 years funding residential mortgages, including hundreds of FHA loans at David Roa, I've seen qualified buyers get discouraged by DTI concerns before understanding the full rules. The truth is that compensating factors can push your allowable ratio to 50% or higher in certain situations. Knowing where these thresholds stand, and what exceptions apply, gives you a clearer path to homeownership.

This guide breaks down the front-end and back-end ratio calculations, explains the 31/43 baseline and when lenders can exceed it, and shows you exactly what compensating factors underwriters look for when approving higher DTI loans.

Why FHA DTI limits matter for approval

Your debt-to-income ratio serves as the primary gatekeeper in FHA underwriting. Lenders check your DTI before evaluating credit scores, down payment size, or employment history because this single metric shows whether you can afford the monthly payment. If your ratios exceed the standard thresholds, your file moves from automated approval through the FHA TOTAL Scorecard to manual underwriting, which adds time, documentation, and approval uncertainty.

Your approval odds depend on DTI first

Automated underwriting systems process most FHA applications in minutes, but they screen applicants by fha debt to income ratio limits before issuing a decision. When your front-end ratio stays at or below 31% and your back-end ratio stays at or below 43%, the system typically approves your loan without human review. Lenders favor this path because it reduces processing delays and documentation requirements on both sides.

Exceeding these benchmarks triggers manual underwriting, where a human examiner reviews your full financial profile. You can still get approved, but underwriters request additional documents like pay stub history, rent payment records, or explanations for any recent credit inquiries. The process takes longer and approval depends on whether you present strong compensating factors that offset the higher debt load.

Manual underwriting doesn't mean denial, but it does mean you need a stronger overall file to compensate for elevated debt ratios.

How DTI affects your loan amount and payment

Your allowable debt-to-income ratio directly caps the maximum monthly mortgage payment lenders will approve. If your gross monthly income totals $6,000 and you carry $1,200 in existing debt, a 43% back-end ratio allows total debt payments of $2,580. Subtracting your $1,200 in existing obligations leaves $1,380 available for your housing payment, which includes principal, interest, taxes, insurance, and HOA fees.

This cap shrinks your purchasing power when rates rise or when you carry higher existing debt. For example, at a 7% interest rate, that $1,380 payment supports roughly a $205,000 loan amount. Drop your car payment or pay off a credit card before applying, and you free up hundreds more per month for a larger mortgage. Small debt reductions create meaningful room in your DTI calculation and can push you from manual underwriting back into automated approval territory.

Lenders also evaluate your stability and ability to handle financial stress through DTI. A borrower at 30% DTI has more cushion for unexpected expenses than one at 48%, so lower ratios signal less default risk even when compensating factors allow higher thresholds.

FHA DTI limits: 31/43 and what counts

The 31/43 benchmark represents two separate calculations that measure different slices of your monthly budget. Your front-end ratio of 31% covers housing expenses only, while your back-end ratio of 43% includes all recurring debts. These fha debt to income ratio limits set the baseline approval standard for automated underwriting, though manual review can approve higher ratios when your file shows compensating strengths.

The 31% front-end housing ratio

Your front-end DTI divides your total monthly housing payment by gross monthly income. This payment includes your principal and interest on the mortgage, property taxes, homeowners insurance, mortgage insurance premiums, and HOA or condo fees if applicable. Lenders call this bundle PITIA (principal, interest, taxes, insurance, association dues), and every dollar in this category counts against your 31% threshold.

For example, if you earn $7,000 per month gross, your front-end limit sits at $2,170. You need to fit your entire housing payment under that cap to meet the standard guideline. Property taxes in high-cost areas often push buyers over this limit even when the base mortgage payment seems affordable.

The 43% back-end total debt ratio

Your back-end calculation adds all recurring monthly obligations to your housing payment. This includes car loans, student loans, credit card minimum payments, personal loans, child support, alimony, and any other debt that appears on your credit report. You divide this combined total by your gross monthly income to reach your back-end percentage.

Back-end DTI captures your full debt picture, which is why paying off small balances before applying creates immediate room in your approval calculation.

Using the same $7,000 monthly income, a 43% back-end ratio allows $3,010 in total monthly debt. If your housing payment takes $2,170, you have $840 left for other obligations before hitting the standard limit.

How to calculate your FHA front-end and back-end DTI

You can calculate both ratios yourself before applying by gathering your gross monthly income and listing all monthly debt obligations. Lenders use your income before taxes and deductions, so pull your most recent pay stubs or tax returns to find the right baseline number. These fha debt to income ratio limits become clear when you work through the math with your actual financial numbers.

Calculate your front-end housing ratio

Divide your total proposed housing payment by your gross monthly income, then multiply by 100 to get a percentage. If your estimated housing payment totals $1,800 (including principal, interest, taxes, insurance, and HOA fees) and you earn $6,500 gross per month, your calculation looks like this: $1,800 ÷ $6,500 = 0.277, or 27.7%. That result sits comfortably below the 31% guideline.

Your front-end ratio focuses exclusively on housing costs, so non-housing debts don't affect this calculation.

Calculate your back-end total ratio

Add your housing payment to all recurring monthly debts, then divide by gross monthly income. Using the same $1,800 housing payment and $6,500 income, add a $350 car payment, $150 in student loans, and $80 in credit card minimums. Your total monthly debt equals $2,380, which divides into $6,500 for a ratio of 36.6%. This clears the 43% back-end threshold.

What debts lenders count and exclude

Lenders include any obligation reporting to credit bureaus with ten or more months of payments remaining. Car loans, student loans, personal loans, and revolving credit all count. Child support, alimony, and co-signed loans also appear in your back-end calculation even when they don't show on your credit report. Utilities, cell phone bills, car insurance, and debts with fewer than ten payments remaining don't count toward your DTI.

When FHA allows 50%+ DTI and why

FHA guidelines permit debt ratios above the 31/43 standard when you present compensating factors that demonstrate financial strength despite higher monthly obligations. Manual underwriters can approve ratios reaching 50% or higher if your file shows multiple offsetting strengths that reduce default risk. These exceptions exist because FHA recognizes that raw DTI percentages don't capture your full financial picture, and rigid cutoffs would exclude qualified borrowers who can handle the payment.

Compensating factors that override standard limits

You need at least one strong compensating factor to justify exceeding 43% DTI in manual underwriting. The most powerful factors include cash reserves exceeding three months of mortgage payments, minimal increase from your current rent to your proposed housing payment, strong credit scores above 680, and documented income stability over multiple years. Lenders also credit significant down payments above the 3.5% FHA minimum and proven payment history on previous mortgages.

A borrower at 48% DTI with six months of reserves and a 720 credit score presents less risk than someone at 40% DTI with zero savings and marginal credit.

Each compensating factor adds weight to your application, and presenting two or three together significantly improves approval odds. For example, combining a 10% down payment with twelve months of reserves and minimal rent increase creates a strong case for approving a 49% back-end ratio.

Manual underwriting paths to 50%+ approval

Your file moves to manual review automatically when automated systems flag DTI above standard thresholds. Underwriters evaluate your complete financial profile rather than relying on algorithm-driven decisions, which opens approval paths that fha debt to income ratio limits would otherwise block. You submit additional documentation proving compensating factors, including bank statements showing reserves, rental history demonstrating payment reliability, and employment verification confirming income stability.

Ratios exceeding 50% require multiple strong factors and typically apply to borrowers with substantial assets, minimal debt payment increases, or professional income documentation showing career growth trajectory.

Common DTI myths and special FHA rules

Borrowers often misunderstand how lenders apply fha debt to income ratio limits, leading to unnecessary confusion during the application process. You might hear conflicting advice from friends, online forums, or even loan officers who don't specialize in FHA products. The reality involves several special calculation rules and approval exceptions that contradict common assumptions about what counts as debt and how underwriters evaluate your income.

The 43% limit isn't a hard ceiling

Many borrowers believe 43% creates an absolute approval cutoff, but manual underwriting regularly approves ratios reaching 50% or higher when compensating factors exist. You can exceed standard thresholds by demonstrating cash reserves, minimal payment increase from current housing costs, or strong credit history. This flexibility exists by design in FHA guidelines, though automated systems will refer your file to manual review rather than issuing instant approval.

FHA designed these thresholds as starting points, not absolute barriers, which is why compensating factors can override standard percentages.

Income calculation includes all stable sources

You don't need W-2 employment to qualify for FHA financing. Lenders count self-employment income, rental property cash flow, alimony, child support, Social Security, disability payments, and pension income when calculating your gross monthly total. Part-time work qualifies if you show two-year history in that role, and seasonal income works when documented across multiple years. Each income source requires specific documentation, but FHA guidelines accept diverse earnings that traditional conforming loans might reject.

Non-occupant co-borrowers don't live in the property

You can add a non-occupant co-borrower to your FHA application to boost qualifying income and lower your debt ratios. This person signs the loan and shares responsibility but doesn't live in the home, making them different from traditional co-borrowers. Their income counts toward your application, though FHA requires higher down payments (typically 5% minimum instead of 3.5%) when using non-occupant co-borrowers.

Next steps

Understanding fha debt to income ratio limits gives you clear benchmarks for qualifying, but knowing the rules doesn't replace working with an experienced lender who can evaluate your specific situation. You now know the 31/43 standard thresholds, how compensating factors extend approval beyond 50%, and which debts count in your calculation. The difference between automated approval and manual underwriting often comes down to small adjustments you can make before applying.

Calculate your current ratios using the formulas outlined above, then identify which compensating factors strengthen your file. Paying down small debts or increasing your down payment creates immediate room in your DTI calculation. Strong reserves and stable income history matter more than perfect ratios when underwriters review your application manually.

Ready to explore your FHA options with someone who has funded over $150 million in residential mortgages? Contact David Roa for a practical assessment of your approval odds and actionable steps to strengthen your DTI position before applying.