First Deal To Scale: How To Build A Real Estate Portfolio

Most investors remember their first property, the nerves, the paperwork, the moment the keys finally landed in their hands. But that single deal is just the beginning. Learning how to build a real estate portfolio separates casual property owners from investors who generate lasting wealth. The difference lies in strategy, financing, and the discipline to treat each acquisition as one piece of a larger puzzle.

After funding over $150 million in real estate transactions and managing my own flipping portfolio, I've seen what works and what stalls investors at deal one or two. The path from your first rental to a diversified collection of income-producing properties isn't about luck, it's about understanding cash flow, leveraging the right loan products, and knowing when to scale. Whether you're eyeing single-family rentals, multifamily units, or mixed-use buildings, the fundamentals remain the same.

This guide walks you through each phase: setting your financial foundation, securing that critical first deal, and expanding strategically without overextending. You'll learn how financing options like DSCR loans and portfolio lending can accelerate growth when traditional banks say no. By the end, you'll have a clear roadmap to move from aspiring investor to portfolio owner.

What a real estate portfolio is and why it works

A real estate portfolio is a collection of investment properties owned by a single investor or entity, strategically acquired to generate income, appreciation, and tax benefits. Unlike owning a primary residence, building a portfolio means treating each property as a business asset that contributes to your overall wealth-building system. You might hold single-family rentals, multifamily buildings, commercial spaces, or a mix across different markets to spread risk and capture various income streams.

The mechanics of portfolio building

The process of learning how to build a real estate portfolio starts with acquiring properties that produce positive cash flow or offer strong appreciation potential. You purchase property one, stabilize its income, then use equity and cash reserves to fund property two. Banks and lenders evaluate each deal based on the property's ability to generate rent, not just your personal income, which is why products like DSCR loans (Debt Service Coverage Ratio) matter for scaling beyond three or four properties.

Each property becomes collateral and proof of your investing track record. Lenders view a successful rental history as evidence you can manage more, opening doors to portfolio loans that finance multiple properties under a single umbrella. This approach contrasts with traditional mortgages that require extensive personal income documentation for every deal.

Why multiple properties multiply returns

Your returns compound through four distinct channels: monthly rental income, property appreciation, mortgage paydown, and tax deductions. When you own multiple properties, each one contributes to all four categories simultaneously. A single rental might cash flow $400 per month, but ten properties at that same level generate $4,000, enough to cover unexpected repairs, vacancies, and still leave profit.

Diversification across property types and locations protects your portfolio when one market softens or a tenant leaves unexpectedly.

Leverage accelerates wealth creation in ways savings accounts never will. If you invest $50,000 as a down payment on a $250,000 property that appreciates 5% annually, you gain $12,500 in equity that first year, a 25% return on your actual cash invested. Multiply that across five properties, and your equity grows by $62,500 annually while tenants pay down your mortgages. The tax benefits through depreciation deductions further reduce your taxable income, keeping more cash available for the next acquisition.

Your first property teaches you systems for tenant screening, maintenance, and cash flow management. The second property refines those systems. By property five, you've built a repeatable acquisition and management process that lets you scale without reinventing the wheel each time. This operational efficiency is what separates successful portfolio builders from those stuck at one or two rentals.

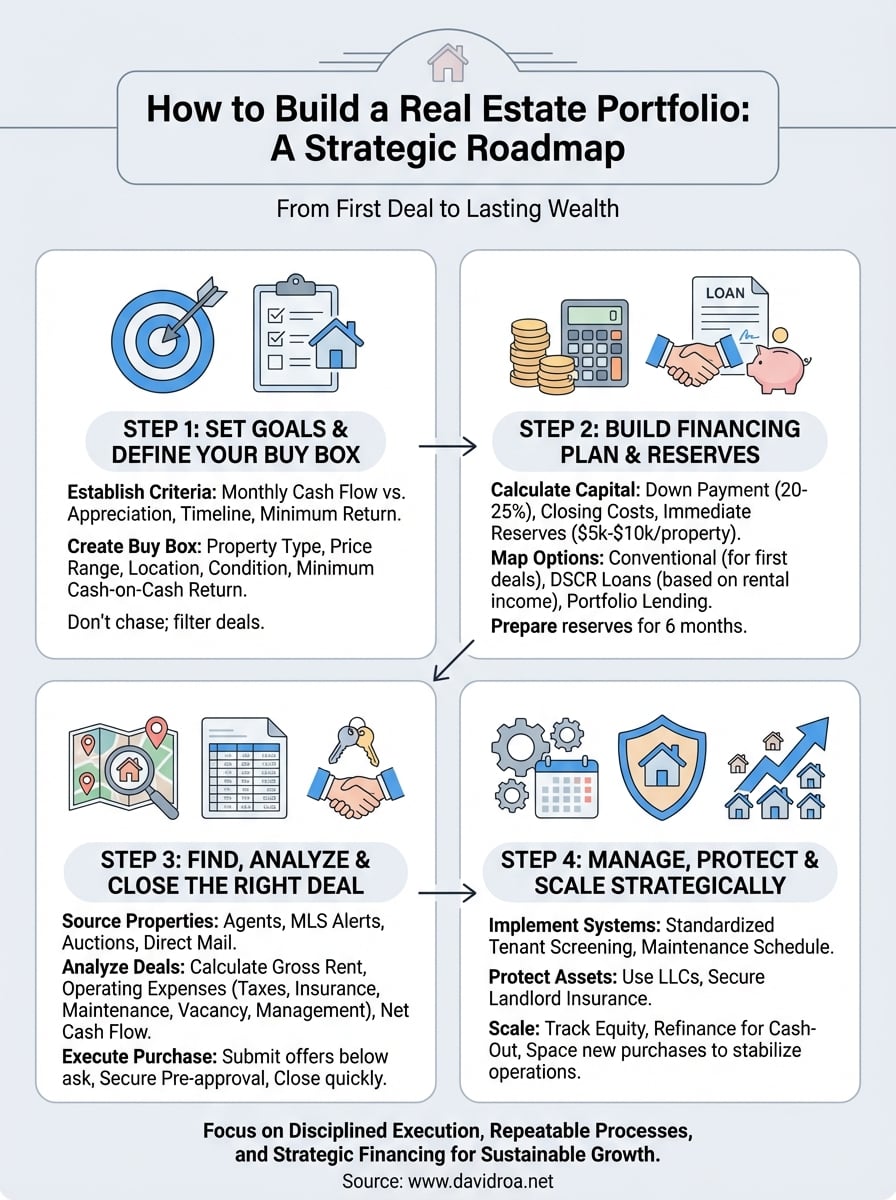

Step 1. Set goals and define your buy box

Before you analyze a single listing, you need to know what success looks like for your portfolio. Your financial goals and investment timeline determine which properties you pursue, which financing products you need, and how quickly you scale. Investors who skip this step waste months chasing deals that don't align with their actual objectives, learning how to build a real estate portfolio without direction leads to stalled momentum and capital tied up in the wrong assets.

Establish your investment criteria

Start by deciding whether you prioritize monthly cash flow or long-term appreciation. Cash flow investors target properties that generate immediate rental income, typically older single-family homes or small multifamily buildings in established neighborhoods. Appreciation investors accept lower or even negative cash flow in exchange for properties in high-growth markets where values increase rapidly. Your choice shapes everything from your financing strategy to your hold period.

Define your minimum acceptable return before you look at a single property, not after you fall in love with one.

Set concrete numbers for your five-year plan: how many properties you want to own, your target monthly cash flow (for example, $2,000 per property), and your acceptable equity position. If you're building toward financial independence, calculate the rental income needed to cover your living expenses, then work backward to determine how many properties at your target cash flow will get you there.

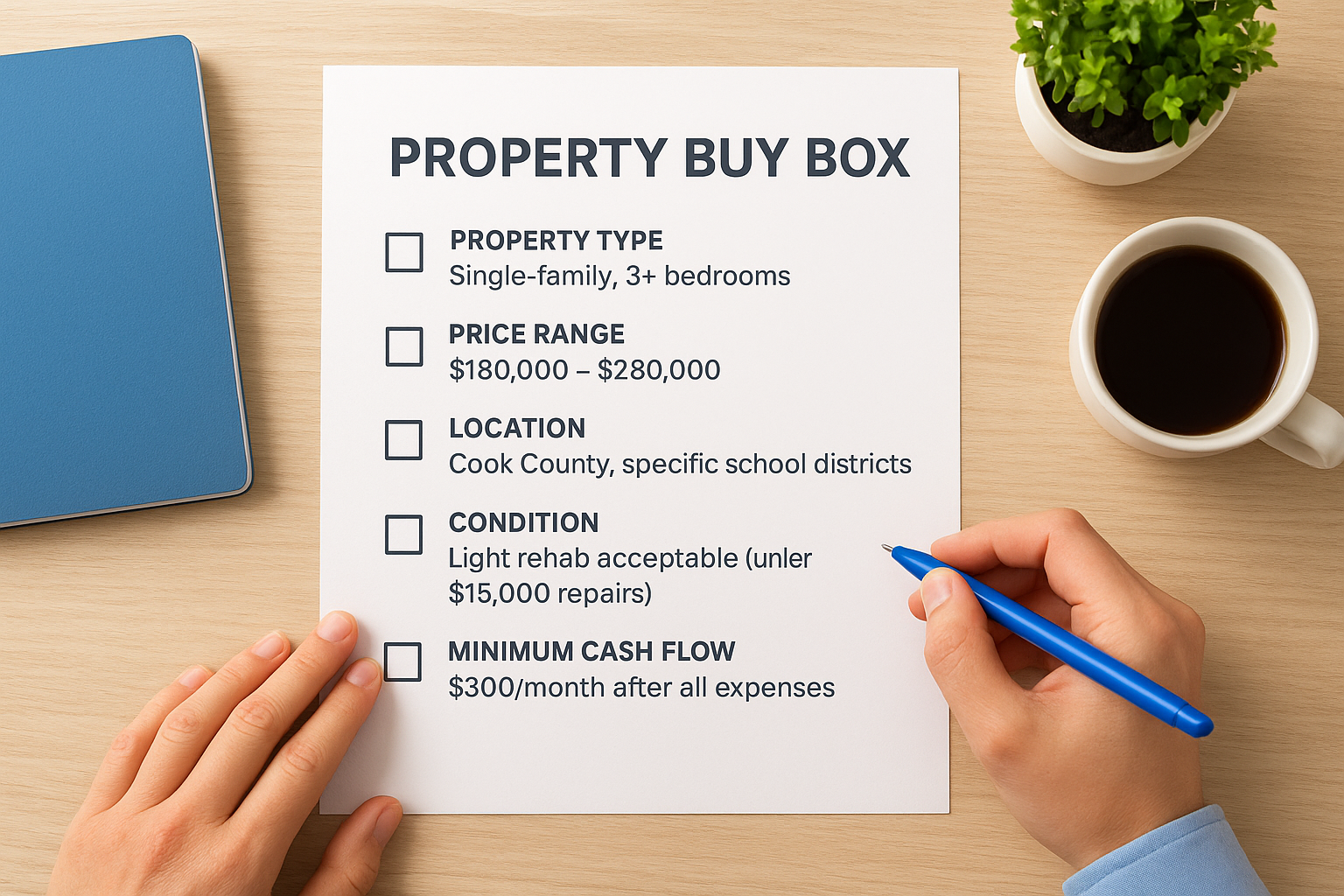

Create your property buy box

Your buy box is a written checklist of non-negotiable criteria that every potential property must meet before you make an offer. This document keeps you disciplined when emotions run high during competitive deals. Include specific parameters for property type (single-family, duplex, fourplex), price range ($150,000 to $300,000), location (within 50 miles of your home base or specific zip codes), condition (move-in ready versus fixer), and minimum cash-on-cash return (at least 8% annually).

Document your buy box in a simple template:

Property Type: Single-family, 3+ bedrooms

Price Range: $180,000 - $280,000

Location: Cook County, specific school districts

Condition: Light rehab acceptable (under $15,000 repairs)

Minimum Cash Flow: $300/month after all expenses

Target Cash-on-Cash Return: 10%+

This criteria sheet becomes your filter for every deal that crosses your desk.

Step 2. Build your financing plan and reserves

Your financing strategy determines how quickly you can acquire properties and whether you survive unexpected vacancies or repairs. Investors who fail to plan their capital requirements and loan products upfront get stuck after their first or second deal, unable to access the financing needed to scale. Understanding how to build a real estate portfolio means knowing exactly how much cash you need today and for your next three acquisitions.

Calculate your total capital requirements

Start by mapping the upfront costs for a typical deal in your buy box. You need 20-25% down payment for conventional investment property loans, plus 2-3% for closing costs, and another $5,000 to $10,000 in immediate reserves per property. If your target property costs $250,000, you're looking at $62,500 down payment, $6,250 in closing costs, and $7,500 in reserves, totaling roughly $76,250 for property one.

Build a capital deployment spreadsheet that tracks these costs across multiple properties:

| Property | Down Payment (25%) | Closing Costs | Initial Reserves | Total Capital | Target Timeline |

|---|---|---|---|---|---|

| Property 1 | $62,500 | $6,250 | $7,500 | $76,250 | Month 1 |

| Property 2 | $62,500 | $6,250 | $7,500 | $76,250 | Month 9 |

| Property 3 | $62,500 | $6,250 | $7,500 | $76,250 | Month 18 |

This template shows you need at least six months of operating reserves per property to cover unexpected vacancies, maintenance, and carrying costs while you search for the next deal.

Map your financing options and qualification criteria

Your loan type impacts your down payment, interest rate, and ability to scale beyond four properties. Conventional mortgages work for your first one to three deals but require full income documentation and cap you at four financed properties. DSCR loans qualify you based on the property's rental income instead of your W-2, making them ideal for portfolio growth beyond the conventional limit.

Understand your financing options before you submit your first offer, not when your earnest money is on the line.

Portfolio lenders bundle multiple properties under one loan, reducing closing costs and streamlining management. Research your qualification requirements now: minimum credit score (typically 680+), maximum debt-to-income ratio, and property performance metrics lenders evaluate.

Step 3. Find, analyze, and close the right deal

Your financing plan means nothing without deal flow. You need a consistent pipeline of properties that match your buy box, a system for evaluating each opportunity against your financial goals, and the confidence to move quickly when the numbers work. Investors who master how to build a real estate portfolio treat acquisition like a business process, not a treasure hunt.

Source properties through multiple channels

Build relationships with real estate agents who specialize in investment properties and understand your buy box criteria. Set up MLS alerts for new listings in your target areas, attend local auctions, and network with wholesalers who can deliver off-market deals before they hit public listings. Drive your target neighborhoods weekly to spot for-sale-by-owner signs and distressed properties that need quick sales.

Direct mail campaigns to absentee owners and pre-foreclosure lists generate leads other investors miss. Your goal is three to five qualified leads per month that meet your criteria.

Run the numbers before you fall in love

Analyze every property using a standardized formula that calculates cash-on-cash return and total expenses. Estimate monthly rent using comparable properties within half a mile, then subtract all operating costs: property taxes, insurance, maintenance (8-10% of rent), vacancies (5-8%), property management (8-10% if outsourced), and mortgage payment.

Use this quick analysis template:

| Line Item | Monthly Amount |

|---|---|

| Gross Rent | $1,800 |

| Property Tax | -$350 |

| Insurance | -$125 |

| Maintenance Reserve (8%) | -$144 |

| Vacancy Reserve (6%) | -$108 |

| Property Management (9%) | -$162 |

| Mortgage Payment | -$750 |

| Net Cash Flow | $161 |

Your analysis protects you from emotional decisions that drain cash flow for years.

Calculate cash-on-cash return by dividing annual cash flow ($161 × 12 = $1,932) by your total cash invested. Properties below your minimum acceptable return get rejected immediately, no exceptions.

Execute the purchase with confidence

Submit offers 10-15% below asking price on properties that meet your numbers, and negotiate repairs or closing cost credits during inspection. Secure your financing pre-approval before you make offers so sellers take you seriously. Close within 30 days to avoid extended carrying costs and lock in your financing terms.

Step 4. Manage, protect, and scale the portfolio

Your first property starts generating cash flow the moment a tenant moves in, but sustainable growth requires operational systems and legal protection that keep your portfolio performing through vacancies, repairs, and market shifts. Investors who treat property management as an afterthought lose months of rent to bad tenants or spend thousands on preventable maintenance issues. Understanding how to build a real estate portfolio means creating processes that protect your assets while you search for the next deal.

Implement systems for property operations

Create a standardized tenant screening process that includes credit checks, employment verification, and rental history from previous landlords. Set minimum criteria: credit scores above 620, income at least three times monthly rent, and positive references from the past two years. Document everything in a written application that protects you from discrimination claims while keeping unqualified applicants out.

Build a maintenance schedule that handles routine inspections every six months and tracks recurring costs like HVAC servicing, gutter cleaning, and water heater replacement timelines. Use a simple spreadsheet to log all repairs with dates, costs, and vendor contacts so you can budget accurately for future properties.

Protect your assets and cash flow

Establish an LLC or other legal entity for each property or group of properties to shield your personal assets from lawsuits. Secure landlord insurance policies that cover liability, property damage, and loss of rental income during repairs. Budget $800 to $1,500 annually per property for comprehensive coverage that protects against tenant lawsuits and natural disasters.

Your legal structure and insurance policies determine whether one bad tenant ruins your entire portfolio or just impacts a single property.

Scale strategically with equity and refinancing

Track your equity position in each property quarterly and identify candidates for cash-out refinancing once you reach 30% equity or more. Pull $50,000 to $75,000 from an appreciated property to fund down payments on your next two acquisitions. Space new purchases six to nine months apart to maintain cash reserves and give yourself time to stabilize each property's operations before adding complexity.

Your next move

You now have the framework for how to build a real estate portfolio from your first property to a collection of income-generating assets. The difference between investors who scale and those who stall comes down to disciplined execution of the steps outlined here: defining your buy box criteria, securing the right financing, analyzing deals with consistent metrics, and protecting your growing portfolio through systems and legal structures.

Your timeline starts today. Calculate your capital requirements for properties one through three, research DSCR lenders who qualify you based on rental income rather than W-2 earnings, and set up your deal pipeline through agents and direct marketing. Each property you acquire builds your track record and opens access to better financing terms for faster scaling.

If you need financing that traditional banks can't provide or want guidance on structuring your portfolio for maximum growth, connect with an experienced lender who understands investor needs and has closed over $150 million in real estate transactions.