Jumbo Loan Calculator: Estimate Monthly Payment & PITI Fast

When you're shopping for a home that exceeds conforming loan limits, even a small difference in interest rate or down payment can shift your monthly obligation by hundreds of dollars. A jumbo loan calculator gives you a clear picture of what you'll actually owe each month, principal, interest, taxes, and insurance included, before you ever sit down with a lender. That clarity matters when you're dealing with loan amounts above $766,550 (the 2024 conforming limit in most U.S. counties).

I'm David Roa, a mortgage broker and senior loan officer with over 25 years in the lending business and more than $150 million funded across residential, commercial, and investment deals. Jumbo loans are a core part of what I do, and I've walked hundreds of borrowers through the exact calculations you're about to learn. The numbers aren't complicated, but understanding what drives them makes a real difference in your buying power.

This guide breaks down how to estimate your monthly jumbo loan payment step by step, what goes into each piece of your PITI breakdown, and how to use that information to make confident financing decisions. Whether you're buying a high-value primary residence or upgrading to a property that pushes past conforming limits, you'll leave with a practical framework for running the numbers yourself.

What counts as a jumbo loan in 2026

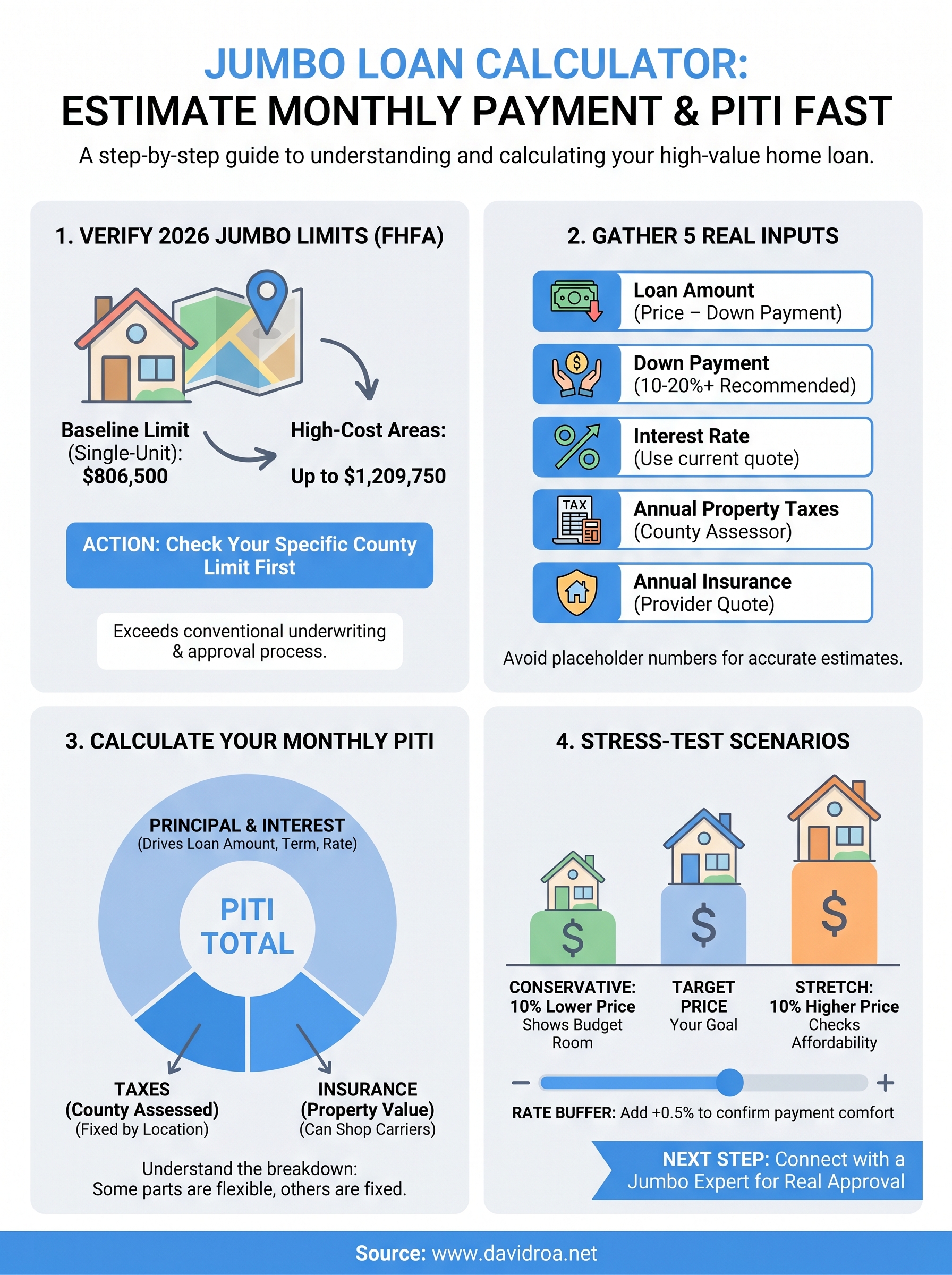

A jumbo loan is any mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These limits define what Fannie Mae and Freddie Mac can purchase on the secondary market, and anything above them falls outside conventional underwriting. For 2026, knowing exactly where that line sits in your target county is the first step before you run any numbers through a jumbo loan calculator.

The baseline limit for most counties

In standard-cost counties across the country, the 2026 baseline conforming loan limit sits at $806,500 for a single-unit property. Borrow one dollar more than that threshold and you're in jumbo territory, no exceptions. That also means a different approval process, stricter reserve requirements, and underwriting guidelines that vary by lender rather than following Fannie or Freddie rules. Multi-unit properties carry higher conforming ceilings: a two-unit property has a higher limit than a single-family home, and four-unit properties have the highest baseline. If you're purchasing a duplex or small apartment building, check the FHFA's published table before assuming you need a jumbo product.

Confirm the exact limit for your specific county on the FHFA website before you calculate anything, because being even slightly below the threshold changes your loan options entirely.

High-cost area limits and what they mean for you

Not every county uses the baseline figure. High-cost metros, including many counties in California, New York, Colorado, and Washington, receive a higher conforming ceiling that can reach up to $1,209,750 for a single-unit property in 2026. Buying in one of these areas means you won't enter jumbo territory until your loan amount exceeds that higher limit. The practical impact is significant: staying below the local ceiling often means lower rates, easier qualification, and less documentation. Always verify your county's specific limit directly on the FHFA site before you decide whether a jumbo product is actually what you need.

Gather the inputs you need before you calculate

Before you open any jumbo loan calculator, you need five specific numbers ready to enter. Running the tool with placeholder figures gives you a misleading estimate that can throw off your entire budget. Spend ten minutes pulling the real numbers from your documents and your county's public records first.

Loan amount and down payment

Your loan amount is the purchase price minus your down payment. Most jumbo lenders require at least 10 to 20 percent down, though some programs allow less with stronger cash reserves. For example, on a $900,000 purchase with 20 percent down ($180,000), your loan amount is $720,000. Confirm your target figure before entering anything.

Rate, taxes, insurance, and reserves

Your interest rate depends on your credit score, loan-to-value ratio, and current market conditions. For taxes and insurance, check your county assessor's site for the annual property tax bill and get a homeowner's insurance quote based on the purchase price. Here is a quick reference for every input you need:

| Input | Where to find it |

|---|---|

| Purchase price | MLS listing or signed offer |

| Down payment | Your savings plan |

| Interest rate | Lender quote or current averages |

| Annual property taxes | County assessor website |

| Annual insurance | Insurance provider quote |

Accurate inputs before you calculate will always produce a more useful estimate than round numbers you guess at later.

Enter your numbers into a jumbo loan calculator

With your inputs ready, open the calculator and work through each field in order. Start with the loan amount, then move to the interest rate, loan term, property taxes, and insurance. Skipping around or leaving fields at default values produces a useless estimate.

Set your loan term and rate first

Most jumbo loan calculators default to a 30-year fixed term, but you can also model a 15-year or adjustable-rate option. Enter the exact rate from your lender quote rather than a rounded number. A difference of 0.125 percent on an $800,000 loan changes your monthly principal and interest by roughly $65, which adds up to $780 per year.

Run the same loan amount with both a 30-year and 15-year term side by side to see how much total interest you save by shortening the payoff period.

Add taxes and insurance to complete the picture

Enter your annual property tax figure divided by 12 in the monthly tax field, then do the same for your insurance premium. Some calculators accept annual totals directly. Check which format the tool expects before entering anything so your PITI total accurately reflects your real monthly housing cost.

Understand your estimate and monthly PITI breakdown

Once the jumbo loan calculator returns a total, resist the urge to look only at the bottom line. Each component of your PITI tells you something different about where your money goes and which parts of the payment you can actually control before you commit to a purchase price.

What each PITI component tells you

Principal and interest are directly shaped by your loan amount, rate, and term, which means they respond to decisions you make before closing. Taxes and insurance are driven by your county's assessment and the property's replacement value, making them harder to move. Knowing which components are flexible tells you exactly where to focus when the total feels out of reach.

| PITI Component | What drives it | Can you reduce it? |

|---|---|---|

| Principal | Loan amount, term | Yes, larger down payment or shorter term |

| Interest | Rate, loan amount | Yes, better credit score or rate negotiation |

| Taxes | County assessment | Rarely, appeals process only |

| Insurance | Property value, coverage | Yes, shop multiple carriers |

When your total looks too high

If your PITI exceeds 28 to 36 percent of your gross monthly income, most jumbo lenders will flag your debt-to-income ratio as a risk before approval.

Increasing your down payment is the fastest fix because it cuts both your loan amount and your monthly interest charge immediately. Stretching your term from 15 to 30 years also lowers the monthly figure, though you will pay significantly more in total interest over the life of the loan.

Stress-test scenarios to pick a price and loan that works

Running a single estimate and stopping there gives you an incomplete picture. The real power of a jumbo loan calculator comes from running multiple scenarios back to back, comparing how different purchase prices, down payments, and rate assumptions shift your monthly payment before you commit to any offer.

Run three price points side by side

Pick your target purchase price, then model it 10 percent lower and 10 percent higher as well. This three-scenario approach shows you exactly how much room you have if negotiations push the price up, or if a better property comes in below your ceiling. Track each run in a simple table like this:

| Scenario | Purchase Price | Down Payment | Loan Amount | Est. PITI |

|---|---|---|---|---|

| Conservative | $850,000 | 20% | $680,000 | Calculate |

| Target | $950,000 | 20% | $760,000 | Calculate |

| Stretch | $1,050,000 | 20% | $840,000 | Calculate |

Factor in rate changes before you commit

Never anchor your purchase decision to today's quoted rate alone; run the same scenario with a rate 0.5 percent higher to confirm the payment still fits your budget comfortably.

Rate movement between the day you make an offer and your closing date is common, and building that buffer into your stress test now prevents you from overextending into a payment that becomes unsustainable if rates tick up before you lock.

Quick wrap-up and what to do next

You now have a repeatable process for estimating your monthly payment on a high-value property. Verify your county's 2026 conforming limit first, gather your five real inputs, run the calculator, then stress-test at least three price points before you settle on a target. That sequence keeps your budget grounded in actual numbers rather than assumptions that collapse once you're under contract.

Knowing your estimated PITI is a strong starting point, but a jumbo loan calculator only reflects the inputs you give it. Real approval depends on your credit profile, reserves, and debt-to-income ratio, which vary by lender and loan structure. Getting a personalized quote from an experienced jumbo lender closes the gap between an estimate and a firm offer you can act on.

When you're ready to move from numbers on a screen to an actual loan, connect with a jumbo mortgage expert who can review your full picture and find the right product for your situation.