8 Best Jumbo Loan Lenders To Compare Rates And Fees (2026)

Not every lender is built to handle jumbo-sized financing. When your loan amount exceeds conforming limits, currently $806,500 in most U.S. counties, you need jumbo loan lenders that actually specialize in high-balance mortgages. The difference between a good and bad fit here can mean tens of thousands of dollars in interest over the life of your loan.

With over 25 years in mortgage lending and more than $150 million funded, I've originated jumbo loans for buyers across a wide range of situations, from straightforward high-income earners to self-employed borrowers with complex financials. That hands-on experience gives me a clear picture of what separates strong jumbo lenders from those that just check the box.

Below, I've put together a list of eight jumbo loan lenders worth comparing in 2026. For each one, I break down their rates, fees, eligibility requirements, and where they tend to stand out. Whether you're purchasing a high-value primary residence or expanding a real estate portfolio, this guide will help you narrow down your options and choose with confidence.

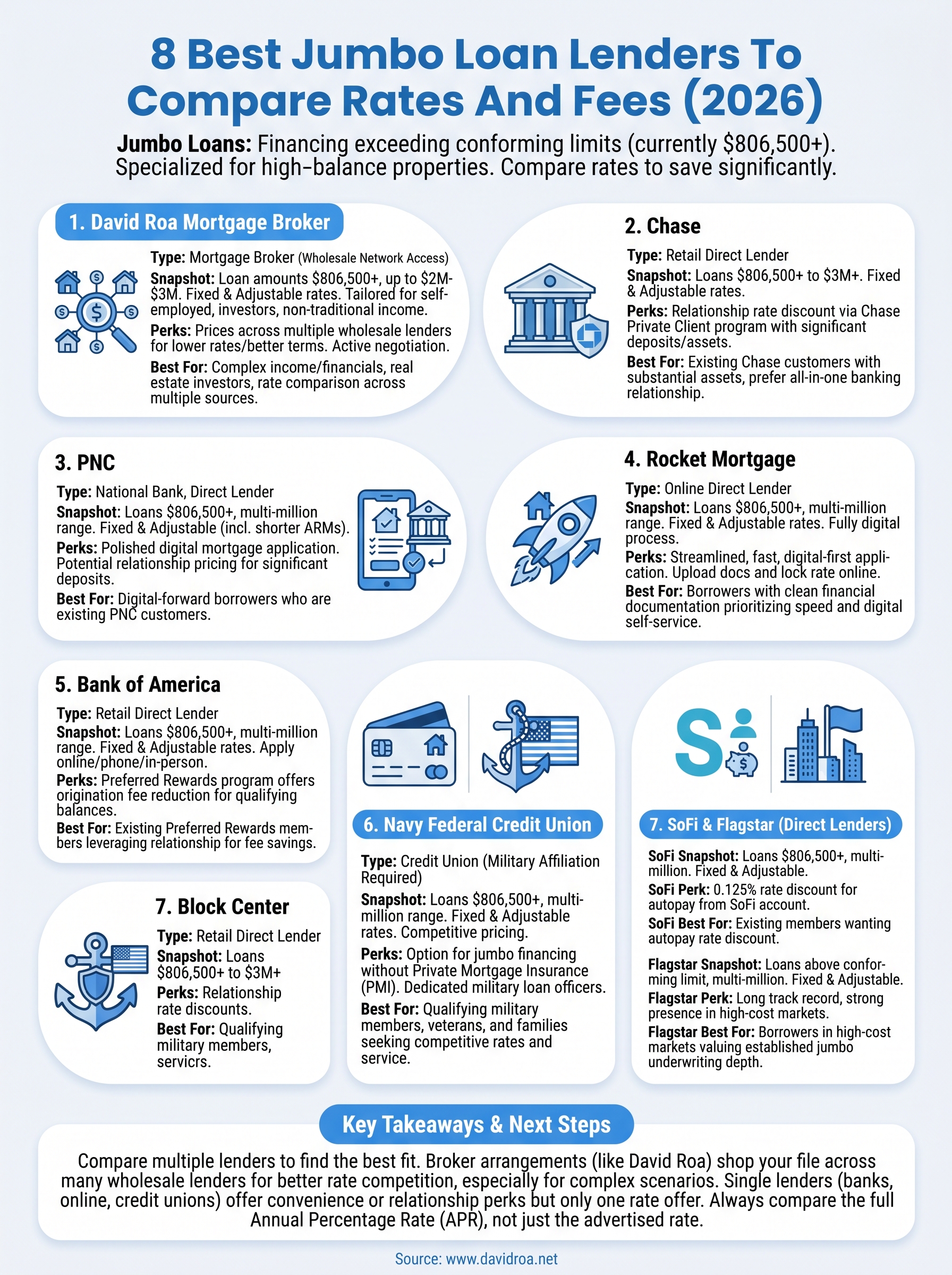

1. David Roa Mortgage Broker

As a mortgage broker rather than a direct lender, I work with a network of wholesale lenders to find you the most competitive jumbo terms available. That independence matters more on jumbo loans than on almost any other product, because rate differences of even 0.25% on a $1.5 million loan translate to significant money over a 30-year term.

Jumbo loan snapshot

I originate jumbo loans starting above the conforming limit of $806,500, with loan amounts that routinely reach into the $2 million to $3 million range. Borrowers get access to fixed and adjustable-rate options, and I work with programs tailored for self-employed buyers, real estate investors, and borrowers with non-traditional income documentation.

How David shops jumbo rates across lenders

Working with a broker means your application gets priced across multiple wholesale lenders at once, not just one institution's in-house menu. That competitive process consistently surfaces lower rates and better terms than a single bank can offer. When you work with me, I actively negotiate on your behalf, using your complete financial profile to position your file where it earns the best pricing.

Shopping your jumbo loan across multiple lenders through a broker is one of the most reliable ways to cut your rate and avoid overpaying on fees.

Typical jumbo requirements to expect

Most jumbo loan lenders in my network require a minimum credit score of 700, though stronger scores unlock meaningfully better pricing tiers. You'll typically need to document 12 to 24 months of cash reserves, a debt-to-income ratio under 43%, and a down payment of at least 10% to 20% depending on loan size. Self-employed borrowers can qualify using bank statement programs in place of traditional tax returns.

Fees and rate levers that matter most

Origination fees, discount points, and lender credits are the three variables that most directly shape your total cost. As your broker, I walk you through each trade-off so you can decide whether buying down your rate makes sense for your actual timeline. Full fee transparency is something I cover from the first conversation, not buried in a disclosure on closing day.

Best for

This option works well for borrowers who want rate comparisons across multiple lenders rather than a single bank's take-it-or-leave-it offer. It is especially strong for:

- Self-employed borrowers with complex income documentation

- Real estate investors using DSCR or asset-based qualification

- High-value purchases requiring a hands-on, strategic approach

Potential drawbacks

Processing timelines can vary depending on which wholesale lender handles your loan, since each has its own underwriting speed. Not every niche jumbo program is available through every lender in my network, so some highly specialized scenarios may require additional sourcing time before locking a rate.

2. Chase

Chase is one of the largest retail mortgage lenders in the U.S. and originates jumbo loans directly through its own channel. Buyers who already have a banking relationship there often explore it as a first stop for high-balance mortgage financing.

Jumbo loan snapshot

Loan amounts at Chase start above $806,500 and can reach $3 million or higher depending on your profile and property type. Both fixed and adjustable-rate products are available on jumbo loans.

Notable perks

Existing customers may qualify for a relationship rate discount through the Chase Private Client program. If you carry significant deposits or investment assets with the bank, that relationship can work in your favor when pricing a jumbo loan.

Chase's relationship pricing is one of the more concrete rate benefits a large bank offers jumbo borrowers, but you need substantial assets on deposit to see a meaningful difference.

Typical requirements

A minimum credit score of 700 is standard for most Chase jumbo products, along with a down payment of at least 20%. Debt-to-income ratios are typically capped around 43%, and reserve requirements scale with loan size.

Fees and rate notes

Sample rates are published online, but your actual rate depends on your credit score and loan-to-value ratio. Origination fees and discount points are standard, so always compare APR rather than the advertised rate alone.

Best for

This option suits buyers who carry a strong existing banking relationship with Chase and prefer the convenience of keeping their deposits and jumbo mortgage under one roof.

Potential drawbacks

Being a single lender means you receive one rate offer rather than competing bids from multiple sources. Borrowers with complex or non-traditional financials may find Chase's underwriting less flexible than what a broker or specialty jumbo loan lender can arrange.

3. PNC

PNC is a major national bank that offers jumbo loan products directly to borrowers. It operates as a full-service lender with both an in-person branch network and a digital mortgage application platform, giving you options for how you want to manage the process.

Jumbo loan snapshot

PNC originates jumbo loans above the conforming limit of $806,500, and its high-balance products extend into the multi-million dollar range depending on your financial profile and property location. Both fixed-rate and adjustable-rate structures are available, including shorter ARM terms that appeal to buyers who plan to sell or refinance within a set window.

Notable perks

PNC's online mortgage experience is more polished than many traditional banks, letting you track your application and submit documentation digitally. Existing PNC customers may also qualify for relationship-based pricing benefits, which can trim your rate slightly if you carry significant deposit balances at the bank.

PNC's digital tools make the jumbo process more transparent than a typical large bank, but that convenience does not replace the rate competition you get by working with multiple jumbo loan lenders at once.

Typical requirements

You generally need a minimum credit score of 700 and a down payment of at least 10% to 20%, depending on loan size. PNC also evaluates debt-to-income ratios and reserve requirements in line with standard jumbo guidelines.

Fees and rate notes

Published rates are a starting point, and your final rate and origination fees will reflect your specific credit score, LTV, and loan amount. Always compare the APR across lenders rather than the headline rate.

Best for

PNC fits borrowers who want a digital-forward experience within a traditional bank structure and already maintain accounts there.

Potential drawbacks

Like any single lender, PNC gives you one pricing offer, and its underwriting guidelines may be less accommodating for self-employed borrowers or those with non-traditional income documentation.

4. Rocket Mortgage

Rocket Mortgage is one of the most recognized names in online mortgage lending, operating as a direct lender with a fully digital application process. Its platform is built around speed and self-service, which appeals to borrowers who prefer to manage the loan process on their own schedule.

Jumbo loan snapshot

Rocket originates jumbo loans above the conforming limit of $806,500, with loan amounts that can extend into the multi-million dollar range. Both fixed-rate and adjustable-rate products are available, and the platform allows you to get a rate quote and submit your full application without speaking to anyone in person.

Notable perks

The biggest draw is the streamlined digital experience. You can upload documents, track your loan status, and lock your rate entirely online. For borrowers who have straightforward financials, this approach keeps the process moving quickly.

Speed and convenience are real advantages with Rocket, but they are no substitute for the rate competition you get by comparing multiple jumbo loan lenders side by side.

Typical requirements

Rocket typically requires a minimum credit score of 700 and a down payment of at least 10% to 20% depending on loan size. Standard debt-to-income and reserve thresholds apply, consistent with conventional jumbo guidelines.

Fees and rate notes

Origination fees and rate options vary by borrower profile. Compare the APR rather than the advertised rate to capture the true cost.

Best for

Rocket suits borrowers with clean financial documentation who prioritize a fast, digital-first experience over rate shopping across multiple sources.

Potential drawbacks

As a single lender, Rocket gives you one rate offer. Borrowers with complex income situations or investment-focused needs may find its guidelines more rigid than a broker arrangement.

5. Bank of America

Bank of America operates as a direct retail lender with a national footprint and a dedicated jumbo loan program. Borrowers with existing accounts there often consider it a convenient starting point when shopping high-balance mortgage financing.

Jumbo loan snapshot

Bank of America originates jumbo loans above the conforming limit of $806,500, with amounts that extend into the multi-million dollar range. Both fixed-rate and adjustable-rate products are available, and you can apply online, by phone, or in person at a local branch.

Notable perks

The Preferred Rewards program is the standout benefit here. If you hold qualifying deposit and investment balances with the bank, you may qualify for a mortgage origination fee reduction, which on a large jumbo loan can represent meaningful savings at closing.

The Preferred Rewards discount is one of the few concrete fee benefits a major bank offers jumbo borrowers, but it requires you to already hold substantial assets with the institution.

Typical requirements

You generally need a minimum credit score of 700 and a down payment of at least 20%. Standard debt-to-income and reserve thresholds apply in line with jumbo guidelines.

Fees and rate notes

Published rates are a baseline. Your final rate and origination costs adjust based on your credit score, LTV, and total loan amount. Review the APR across multiple jumbo loan lenders before committing.

Best for

Bank of America suits borrowers who are already enrolled in Preferred Rewards and want to leverage existing banking relationships to reduce fees at closing.

Potential drawbacks

As a single lender, Bank of America gives you one rate offer. Borrowers with complex income documentation or investment-focused needs may find the underwriting guidelines less accommodating than a broker arrangement.

6. Navy Federal Credit Union

Navy Federal Credit Union is the largest credit union in the U.S. and serves active military members, veterans, Department of Defense employees, and their immediate family members. If you qualify for membership, it is one of the strongest options among jumbo loan lenders for high-value purchases.

Jumbo loan snapshot

Navy Federal originates jumbo loans above the conforming limit of $806,500, with loan amounts that can reach into the multi-million dollar range depending on your financial profile. Both fixed-rate and adjustable-rate products are available, and the credit union consistently prices its jumbo products competitively relative to large retail banks.

Notable perks

Members can access jumbo financing without private mortgage insurance (PMI) on certain loan structures, which reduces your monthly carrying cost on a high-balance loan. Navy Federal also offers dedicated loan officers who specialize in serving the military community, which tends to mean more personalized service than a large commercial bank provides.

Avoiding PMI on a jumbo loan is a meaningful cost advantage, especially when your loan balance pushes into seven figures.

Typical requirements

You need active or retired military affiliation to become a member, which is the primary eligibility gate. Standard jumbo underwriting applies from there, including a minimum credit score around 700 and sufficient reserves and income documentation.

Fees and rate notes

Rate and fee structures are competitive with or below what major retail banks advertise, particularly for qualifying military borrowers. Always compare the full APR rather than the base rate alone.

Best for

Navy Federal works best for military-affiliated borrowers who qualify for membership and want strong jumbo pricing with attentive service.

Potential drawbacks

Membership eligibility is restricted, so most civilian borrowers cannot access this option regardless of how strong their financial profile is.

7. SoFi and Flagstar

Both SoFi and Flagstar operate as direct jumbo loan lenders with distinct advantages worth comparing before you lock a rate. Neither one is a broker arrangement, so you get a single offer from each, but both bring competitive pricing and useful borrower-specific perks to the table.

SoFi jumbo loan snapshot

SoFi originates jumbo loans above $806,500, with amounts extending into the multi-million dollar range on both fixed and adjustable-rate structures.

SoFi notable perks

Members receive a 0.125% rate discount when they set up autopay from a SoFi checking or savings account, which adds real savings on a large balance.

SoFi typical requirements

You need a minimum credit score of 700 and a down payment of at least 10%, with standard debt-to-income and reserve thresholds applying.

SoFi fees and rate notes

SoFi posts sample rates online, but your final APR reflects your specific credit score and LTV. Always compare the full cost, not just the advertised number.

SoFi best for

SoFi suits existing members who want to use their banking relationship to capture a rate discount on a high-balance loan.

SoFi potential drawbacks

As a single lender, SoFi offers one pricing tier with limited flexibility for complex or non-traditional income scenarios.

Flagstar jumbo loan snapshot

Flagstar originates jumbo loans above the conforming limit, extending into the multi-million dollar range with both fixed and adjustable options available.

Flagstar notable perks

Flagstar carries a long track record in jumbo lending and maintains a strong presence in high-cost markets across the country.

Flagstar's established jumbo experience makes it a more reliable option than newer digital lenders for complex high-balance transactions.

Flagstar typical requirements

Standard guidelines apply: a minimum credit score of 700, at least 10% to 20% down, and documented reserves scaled to your loan size.

Flagstar fees and rate notes

Origination fees and rate structures follow standard jumbo conventions. Compare the full APR across multiple lenders before you commit.

Flagstar best for

Flagstar fits borrowers in high-cost markets who want a lender with proven jumbo underwriting depth and experience closing large transactions.

Flagstar potential drawbacks

Like any single-lender option, Flagstar cannot match the multi-lender rate competition you access by working through a broker.

Next Steps

You now have a clear picture of eight jumbo loan lenders worth comparing in 2026, from large retail banks with relationship discounts to a broker arrangement that shops your file across multiple wholesale sources at once. The right choice depends on your income structure, loan size, and how much flexibility you need during underwriting.

Working with a broker consistently produces stronger outcomes for borrowers with complex financials or large loan amounts, because competing lenders bid for your business rather than presenting a single take-it-or-leave-it rate. Your final cost comes down to how aggressively your file gets positioned in the market.

If you want to see what multiple lenders would actually offer on your specific jumbo scenario, connect with David Roa for a direct consultation. With over 25 years of experience and $150 million funded, the goal is to find you the best terms available, not just the first ones on the table.