SBA Loan Down Payment Requirements: 7(a) Vs 504 Explained

Most business owners assume SBA loans require massive upfront capital, but the reality is more nuanced than that. SBA loan down payment requirements typically range from 10% to 20%, depending on which program you use and what you're using the funds for. That range can mean tens of thousands of dollars in difference, money that could stay in your business instead of tied up at closing.

The two most common SBA programs, the 7(a) and the 504, each come with their own down payment structures, eligibility rules, and exceptions that directly affect how much cash you need on hand. Whether you're acquiring an existing business, purchasing commercial real estate, or funding equipment, the program you choose changes the equation. Some borrowers even qualify for reduced or zero down payment options under specific circumstances.

At David Roa, we've structured SBA 7(a) and 504 financing for business owners across a wide range of industries, from restaurants to mixed-use properties, with over $150 million funded throughout 25+ years in lending. This article breaks down exactly what each program requires, where the requirements differ, and how to position yourself for the lowest possible down payment on your next SBA loan.

Why SBA down payments and equity injection matter

When you apply for an SBA loan, the lender and the SBA itself want to see that you have skin in the game. The down payment you bring to closing demonstrates financial commitment and directly reduces the lender's exposure if your business runs into trouble. Without a required contribution, the risk shifts entirely to the lender and the taxpayer-backed SBA guarantee, which is why both programs set minimum equity injection thresholds rather than leaving it to individual lender discretion.

Down payment vs. equity injection: understanding the distinction

These two terms get used interchangeably, but they carry a specific meaning in the SBA world. A down payment typically refers to the cash you put toward an asset purchase, such as commercial real estate or equipment. An equity injection is the broader term the SBA actually uses, covering any contribution you make to reduce the total amount borrowed. Your injection can come from personal savings, a family gift, or proceeds from selling an existing asset, as long as the source is not another loan.

Your lender will require you to document where the equity injection comes from. If you cannot trace the funds clearly through bank statements or other records, the lender will flag it before the file moves forward. Getting your documentation in order early prevents last-minute delays that can push back a closing by weeks. Borrowed funds cannot serve as your equity injection unless the SBA specifically approves an exception, which is rare and heavily scrutinized.

Why equity injection requirements exist

Shared risk is the foundation of how the SBA structures its guarantee program. When you put your own capital into a deal, the lender's potential loss shrinks proportionally, and the SBA's exposure on its guarantee decreases as well. This is why sba loan down payment requirements are not arbitrary percentages. They reflect decades of SBA performance data on which loan types and purposes carry the highest default rates.

Loans where borrowers contributed less equity historically show higher default rates, which is precisely why the SBA sets minimums rather than leaving the decision to individual lenders.

Business acquisitions typically require more equity than real estate purchases because the collateral is harder to liquidate. A commercial building holds independent value and can be sold to recover losses. An operating business, by contrast, often depends on the current owner to retain its value. Real estate also offers more predictable appraisal values, which makes lenders more comfortable with lower down payments. Knowing this distinction helps you plan your capital before approaching any lender.

SBA 7a down payment requirements by loan use

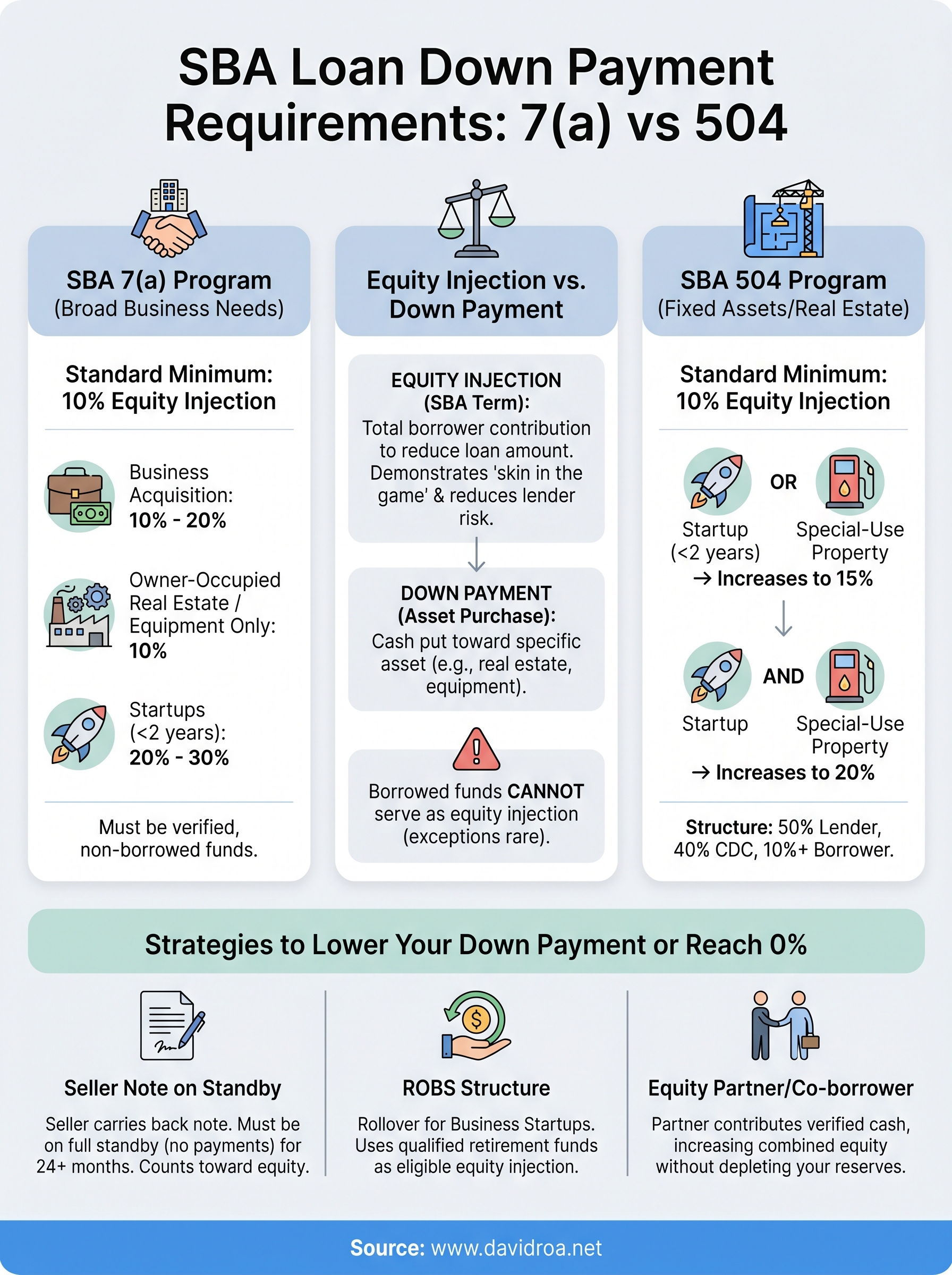

The SBA 7(a) program covers a broad range of business needs, which means sba loan down payment requirements vary depending on what you're actually funding. The standard minimum is 10% equity injection, but that floor shifts upward based on loan purpose, the strength of your application, and whether the deal involves a change of ownership.

Business acquisitions

When you use a 7(a) loan to buy an existing business, the SBA typically requires a 10% minimum equity injection. Lenders often push that number to 15% or 20% if the business has limited tangible assets, a short operating history, or if cash flow projections appear tight.

Your injection must come from verified, non-borrowed funds, documented through at least two to three months of bank statements. If a seller note helps cover part of your contribution, the SBA may allow it in certain cases, but the note must remain on full standby for at least 24 months before any payments can be made.

Lenders treat acquisition loans with more scrutiny than property-backed deals because the business's value often walks out the door with the previous owner.

Real estate and equipment purchases

For commercial real estate and equipment, the 7(a) loan still uses a 10% baseline, and lenders have more flexibility here because the collateral is tangible and independently appraisable. Below is how the requirement typically applies across common loan uses:

| Loan Use | Typical Down Payment |

|---|---|

| Business acquisition | 10% to 20% |

| Owner-occupied real estate | 10% |

| Equipment only | 10% (strong financials required) |

| Startup businesses | 20% to 30% |

Startup businesses draw the highest requirements because they lack the operating history that lenders use to assess repayment risk. If your business is under two years old, plan to bring 20% to 30% to the table regardless of how strong your personal credit profile looks.

SBA 504 down payment requirements and when they increase

The SBA 504 loan is built specifically for fixed asset purchases, which means commercial real estate and long-life equipment are its primary targets. The standard sba loan down payment requirement for a 504 loan sits at 10%, with the remaining financing split between a conventional lender covering 50% and a Certified Development Company (CDC) funding 40%. That structure keeps your upfront cash lower than most conventional commercial loans while still giving the SBA and lender adequate protection.

The 504's layered financing structure is one of the most borrower-friendly arrangements in small business lending, but the 10% baseline does not hold in every situation.

When the 504 down payment increases to 15%

Two specific circumstances push your required contribution from 10% to 15%. The first is a startup business, defined by the SBA as any company operating for less than two years at the time of application. The second is a special-use property, which includes buildings that serve a single purpose and have limited alternative uses, such as gas stations, car washes, hotels, and funeral homes.

Special-use properties carry a higher requirement because their resale value is narrower than a standard office building or warehouse. If your business defaults, the lender faces a much smaller pool of qualified buyers for that asset.

When it reaches 20%

Your down payment climbs to 20% when both conditions apply simultaneously, meaning you're a startup purchasing a special-use property. This combination represents the highest default risk in the 504 program, so the SBA increases your equity contribution accordingly to offset the lender's exposure from the start.

How to lower your SBA down payment or reach 0% down

Reducing your sba loan down payment requirements comes down to structuring the deal correctly before you submit your application. There are legitimate strategies that let you bring less cash to closing, and some buyers do reach 0% out-of-pocket, but each approach requires documentation and lender approval.

Use a seller note to cover part of your injection

When you buy a business using a 7(a) loan, the seller can carry back a note that counts toward your required equity injection. The SBA allows this under a specific condition: the seller note must go on full standby for at least 24 months, meaning no principal or interest payments during that period. Your lender needs to approve the standby agreement in writing before the loan closes.

A seller note on standby is one of the most effective ways to preserve cash at closing without violating SBA equity injection rules.

Not every seller will agree to standby terms, so negotiate this early in the purchase process rather than after you've already structured the deal.

Tap retirement funds through a ROBS structure

A Rollover for Business Startups (ROBS) arrangement lets you roll over qualified retirement account funds into a new business's corporation, which then invests in the business. Because the funds come from your own retirement account rather than a loan, the SBA treats them as eligible equity injection. This approach requires a plan document, a C-corporation, and a plan administrator, so work with a qualified ERISA attorney before using it.

Bring in a co-borrower or equity partner

Adding a business partner who contributes verified cash increases your combined equity injection without depleting your own reserves. Both parties become co-borrowers on the loan, sharing full personal liability for repayment.

What to prepare before you apply with a lender

Understanding sba loan down payment requirements is only the first step. Before you sit down with a lender, you need to organize your financial records so the application moves without delays. Lenders review a predictable set of documents at the start, and missing even one can push your timeline back by several weeks.

Financial documents your lender will request

Your lender will build a complete picture of your business and personal finances before recommending a program or confirming your equity injection amount. Gathering these materials ahead of time shortens the underwriting process significantly.

- Last three years of business and personal tax returns

- Year-to-date profit and loss statement and balance sheet

- Business debt schedule listing all current obligations

- Three months of business and personal bank statements

- Business plan with financial projections (required for startups)

Lenders rarely move forward without a complete file, so submitting a partial application typically adds weeks rather than days to your timeline.

Proof of your equity injection source

Documenting where your down payment funds are coming from is a non-negotiable part of the approval process. Pull together at least two to three months of bank statements showing the funds have been on deposit and are not the result of a recent large transfer without a clear explanation.

If you plan to use retirement funds or a seller note, coordinate with your lender before signing any purchase agreements. Structuring those arrangements after the fact creates complications that can unwind an otherwise approved deal. Aligning your documentation with your funding strategy from the start keeps your closing on schedule.

Final takeaways

SBA loan down payment requirements follow a clear logic once you understand the two programs. The 7(a) starts at 10% for most loan purposes, but climbs to 20% to 30% for startups or businesses with limited collateral. The 504 holds at 10% for established businesses buying standard properties, then rises to 15% or 20% when startup status or special-use properties enter the picture.

Your actual out-of-pocket cost depends heavily on how you structure the deal. A seller note on standby, retirement funds through a ROBS arrangement, or a qualified equity partner can all reduce what you bring to closing. Preparing your documentation early, from tax returns to bank statements, keeps underwriting from stalling at the last moment.

If you want a direct assessment of which program fits your situation and how much you actually need to bring to closing, connect with David Roa to review your options.