What Is a Bank Statement Loan? Requirements & How It Works

If you're self-employed, you already know the frustration: your business is profitable, your bank account proves it, but a traditional lender won't approve you because your tax returns tell a different story. Write-offs that save you thousands in taxes can cost you a mortgage approval. A bank statement loan solves that problem by using your actual deposits as proof of income instead of W-2s or tax returns.

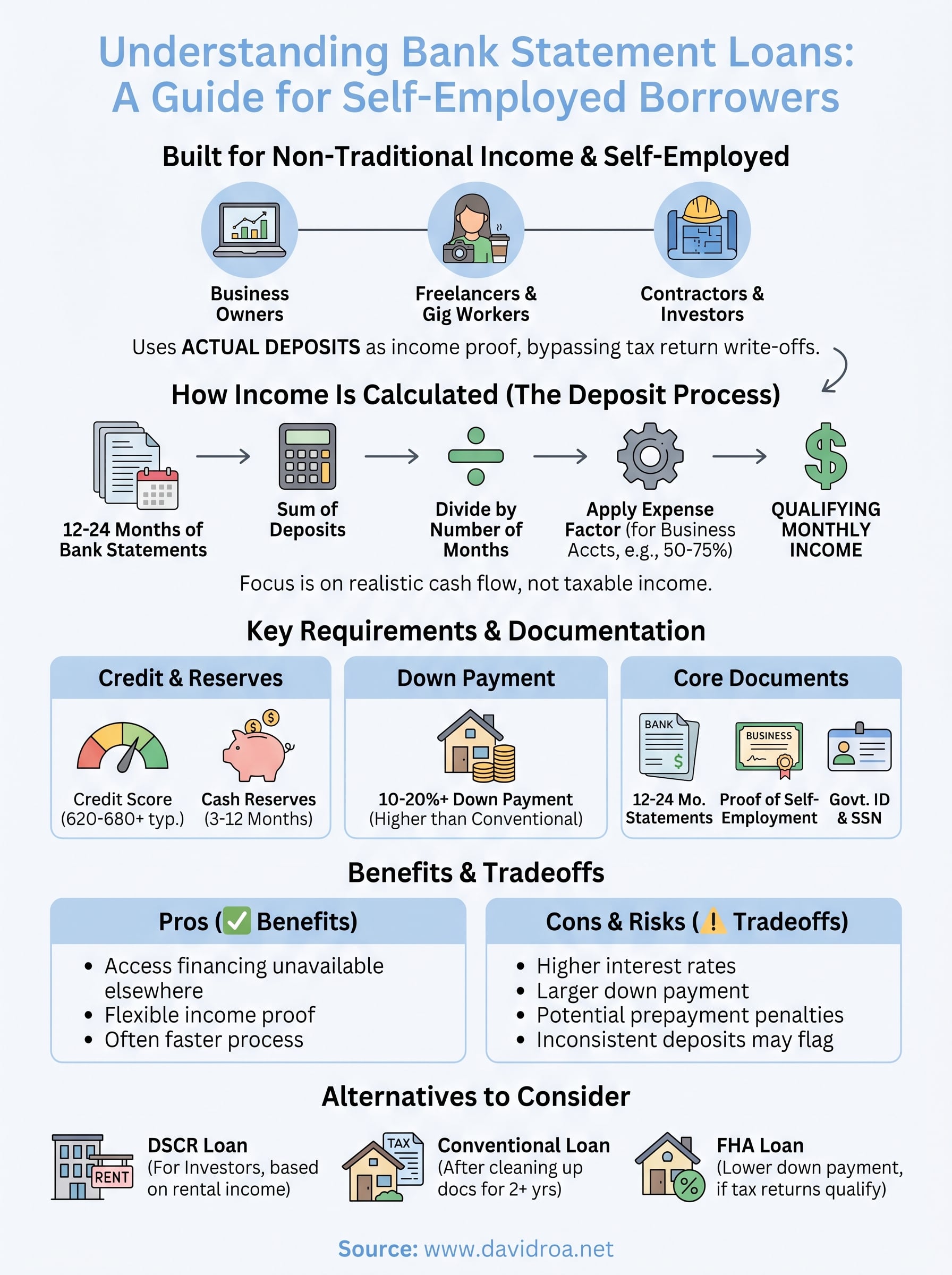

This loan type was built for borrowers whose financial picture doesn't fit neatly into a conventional underwriting box, business owners, freelancers, gig workers, and 1099 contractors who earn well but document income differently. Instead of penalizing you for smart tax strategy, bank statement loans reward real cash flow, making homeownership and investment purchases accessible without jumping through impossible hoops.

At David Roa, we've spent over 25 years helping self-employed borrowers and investors find the right financing, including bank statement programs that traditional banks rarely offer. With more than $150 million funded across residential, commercial, and investment deals, we understand how these loans work from the inside.

This guide breaks down exactly how bank statement loans function, who qualifies, what lenders look for, and how to position yourself for approval. Whether you're buying your first home or adding to a real estate portfolio, you'll walk away knowing if this loan type fits your situation, and what steps to take next.

Why bank statement loans exist and who they help

The conventional mortgage system was built around a simple assumption: salaried employees with steady paychecks are the most reliable loan candidates. Lenders designed their underwriting models to verify income through W-2s, pay stubs, and tax returns. That system works fine if you report to a single employer. But if you run a business, freelance full-time, or work as a contractor, your income documentation looks completely different, and traditional underwriting often penalizes you for it, even when your actual cash flow is strong.

The tax write-off trap that blocks conventional approval

Self-employed borrowers face a specific problem that salaried workers rarely encounter. Business write-offs reduce your taxable income, which is exactly what your accountant wants. Deducting home office expenses, vehicle use, equipment, travel, and other legitimate costs can drop your reported income significantly. For tax purposes, that's a win. For a conventional mortgage underwriter, it looks like you don't earn enough to qualify.

The IRS and your mortgage lender look at the same tax return with opposite goals: one wants your income low, and the other needs it high.

This conflict is the core reason bank statement programs were developed. Instead of relying on what you reported to the IRS, these programs let lenders evaluate your real financial activity. They review your actual deposits over a set period, typically 12 or 24 months, to calculate what you genuinely bring in. That single shift in verification method changes everything for borrowers who manage taxes aggressively but run healthy, profitable operations.

Who these loans are built for

When people ask what is a bank statement loan, the honest answer starts with understanding the borrowers it was designed to serve. Self-employed business owners are the most common users, whether they run a single-person LLC, own a restaurant, or operate a construction company. If your business income flows through personal or business bank accounts rather than a corporate payroll, this loan type fits your situation.

Beyond traditional business owners, bank statement loans also serve:

- Freelancers and independent contractors who receive 1099 income from multiple clients and can't point to a single employer's W-2

- Gig economy workers who earn through platforms and accumulate deposits across multiple accounts

- Real estate investors who own rental properties and show depreciation losses on returns that reduce reported income

- Seasonal business owners whose income fluctuates month to month but averages out to strong annual totals

Each of these borrower types earns real income. The core issue is how that income appears on paper compared to how it actually moves through their accounts. Bank statement loans close that gap by shifting the verification method, not lowering the standard.

Why this matters more than ever

The number of self-employed Americans has grown consistently over the past decade, and alternative documentation loan programs have expanded alongside that trend. According to the U.S. Bureau of Labor Statistics, millions of Americans work as independent contractors or run their own businesses, and that group faces structural barriers in traditional mortgage markets. Bank statement programs exist because the lending industry recognized that creditworthy borrowers shouldn't be locked out of homeownership simply because their documentation doesn't match a model built for 9-to-5 employees.

For borrowers in that position, this isn't just a niche product. It's often the only realistic path to approval when a conventional loan door closes. Understanding how the loan works under the hood, which is what the next section covers, puts you in a much stronger position to move forward with confidence.

How a bank statement loan works in underwriting

The underwriting process for a bank statement loan follows a different path than a conventional mortgage, but the goal stays the same: verify that you can repay the loan. Instead of reviewing W-2s or tax returns, the lender collects your bank statements and calculates your average monthly deposits over a set review period. That deposit average becomes your qualifying income, and everything else in the file is evaluated against it.

The deposit calculation process

Lenders typically request 12 or 24 months of statements, either personal, business, or both, depending on the program you qualify for. The underwriter adds up all deposits across that period and divides by the number of months to arrive at your average monthly income. From there, they calculate your debt-to-income ratio and determine what loan amount your cash flow can support.

Not every deposit counts toward that total. Underwriters exclude transfers between your own accounts, large one-time deposits that don't reflect regular business activity, and any funds you can't document as income-related. What remains after that filtering is a realistic picture of your consistent cash flow, free of distortions that could inflate or misrepresent your actual earning pattern.

Business bank statement programs often apply an expense factor, typically between 50% and 75%, to account for operating costs your business carries before arriving at a usable income figure.

How the expense factor affects your qualifying income

If you use business bank statements, most lenders apply an expense ratio to your gross deposits. This percentage represents what the lender assumes you spend to run your business. For example, if your statements show $20,000 in average monthly deposits and the lender applies a 50% expense factor, your qualifying income becomes $10,000 per month. That adjusted number drives your approval amount, not the gross figure.

Personal bank statements usually receive more favorable treatment because lenders treat those deposits as take-home income rather than gross business revenue. Choosing the right account type and finding lenders with competitive expense factors can meaningfully change what you qualify for, which is why working with an experienced broker matters in this loan category.

How lenders evaluate overall risk

Beyond income, underwriters also weigh your credit score, loan-to-value ratio, and available cash reserves. Borrowers researching what is a bank statement loan often focus only on the income side, but your credit history and down payment still carry real weight. A stronger credit profile and larger down payment give the lender more confidence and often unlock better rates, even when income documentation is non-traditional.

Bank statement loan requirements and common documents

Understanding what is a bank statement loan also means knowing exactly what lenders expect from you before approving one. These programs are more flexible than conventional mortgages, but they still carry firm qualification standards. Lenders take on more risk by accepting non-traditional documentation, so they offset that risk through tighter requirements in other areas, particularly your credit score, down payment, and cash reserves.

Credit, down payment, and reserves

Most bank statement loan programs set a minimum credit score between 620 and 680, though borrowers with scores above 700 access better rates and more favorable terms. Your credit profile signals repayment reliability when your income documentation takes a non-traditional form, so lenders weigh it heavily in their decision.

A higher credit score doesn't just improve your odds of approval; it directly reduces the interest rate you'll pay over the life of the loan.

Down payment requirements typically start at 10% and often range up to 20% or more, depending on the loan amount and your credit tier. Larger down payments reduce the lender's exposure and can offset a lower credit score or shorter bank statement history. Beyond the down payment, most programs require cash reserves equivalent to three to twelve months of mortgage payments sitting in your account after closing. This reserve requirement confirms that you can handle payments through slower business months without defaulting.

What documents you'll need to prepare

Gathering your paperwork before you apply speeds up the process and prevents last-minute delays. Most bank statement programs require a consistent set of core documents, though specific lenders may ask for additional items depending on your loan size or business structure.

You can expect to provide:

- 12 or 24 months of personal or business bank statements, depending on which account type you're using to qualify

- Proof of self-employment, such as a business license, CPA letter confirming your business is active, or formation documents for your LLC or corporation

- A profit and loss statement prepared by a licensed CPA, which some lenders require alongside or instead of business statements

- Government-issued photo ID and your Social Security number

- Documentation for any existing debts, including mortgage statements, auto loans, or credit card accounts that affect your debt-to-income ratio

Organizing these documents ahead of time puts you in a stronger position when you submit your application. Lenders move faster when your file is complete, and a clean, well-organized submission signals that you're a serious borrower prepared to close.

Pros, cons, and risks to watch for

Understanding what is a bank statement loan means looking at the full picture, not just the approval benefits. These programs open real doors for self-employed borrowers, but they also carry tradeoffs that affect your long-term cost and financial flexibility. Knowing both sides before you apply helps you decide whether this is the right move for your specific situation rather than finding out after you've committed.

The advantages that make this loan worth considering

The most obvious benefit is access to financing that would otherwise be unavailable to you. If your tax returns show depressed income due to legitimate deductions, a bank statement loan lets your actual cash flow do the talking. You don't have to choose between minimizing your tax bill and qualifying for a mortgage.

Beyond approval access, these programs offer genuine flexibility in how you document your income, whether through personal accounts, business accounts, or a combination. Lenders in this space also tend to move faster than traditional institutions because they've built their processes specifically around non-traditional borrowers. That speed can matter when you're competing for a property.

Bank statement loans give you approval based on how your business actually performs, not how your accountant needed it to look at tax time.

The tradeoffs you need to know upfront

Interest rates on bank statement loans run higher than conventional mortgages, typically by half a percentage point to one full point or more, depending on your credit profile and loan-to-value ratio. Lenders charge more because they accept documentation risk that conventional underwriting eliminates. That rate difference adds real cost over a 30-year loan, so you need to factor it into your monthly budget and long-term financial planning before you commit.

Down payment requirements are also steeper than what you'd find with FHA or standard conventional programs. Putting down 10% to 20% ties up more capital upfront, which can strain your liquidity if you're simultaneously running a business that needs working capital.

Risks that can catch borrowers off guard

The biggest risk most borrowers overlook is inconsistent deposit patterns that undermine your calculated income. If your statements show erratic deposits, large unexplained transfers, or gaps in business activity, underwriters may flag your file or reduce your qualifying income significantly below what you expected.

Prepayment penalties represent another exposure that surprises borrowers after closing. Some bank statement programs include prepayment clauses that limit your ability to refinance quickly if rates drop. Always ask your broker directly whether a prepayment penalty applies to your specific program before signing anything.

Alternatives and when another loan fits better

A bank statement loan fits a specific profile, but it isn't the right solution for every self-employed borrower or investor. Before you commit to this program, it's worth reviewing the other loan types available to you and understanding exactly when one of those alternatives delivers better terms, lower rates, or a simpler path to closing.

DSCR loans for real estate investors

If you're purchasing an investment property rather than a primary residence, a Debt Service Coverage Ratio (DSCR) loan may serve you better than a bank statement program. DSCR loans qualify you based entirely on the rental income the property generates, not on your personal income at all. The lender compares the property's projected or actual rental income against its monthly mortgage payment, and if that ratio clears their threshold (typically 1.0 or higher), you qualify.

For investors with strong rental properties but complex personal income, a DSCR loan removes personal income documentation from the equation entirely.

This makes DSCR lending a cleaner fit if you already understand what is a bank statement loan but your goal is building a rental portfolio rather than buying a home to live in. You avoid the deposit-calculation process altogether, and approval hinges on the asset rather than your tax returns or bank activity.

Conventional loans after cleaning up documentation

If your business has been operating for several years and your reported income has grown, a conventional loan may now be within reach even if it wasn't before. Conventional programs offer lower rates, smaller down payments, and no prepayment penalties in most cases. The tradeoff is that you need two years of tax returns showing sufficient net income to meet debt-to-income requirements.

Borrowers who reduced their write-offs strategically over the prior two filing years, or whose business grew enough to show qualifying income despite deductions, often find that switching to a conventional program saves them significantly over the life of the loan. It's worth running both scenarios with your broker before deciding.

FHA loans for qualifying first-time buyers

FHA loans carry minimum down payments of 3.5% and more flexible credit requirements than conventional programs, making them accessible for borrowers with thinner credit histories. If you can document your income through tax returns and your reported income is high enough to qualify, an FHA loan almost always beats a bank statement program on rate and upfront cost. The key question is whether your adjusted gross income after deductions clears the lender's minimum threshold for the loan amount you need.

Next Steps

Now that you understand what is a bank statement loan and how it works from application through closing, the next move is figuring out whether it fits your specific income picture and financial goals. Your bank statements, credit score, and down payment capacity are the three factors that will shape your approval odds and rate, so pulling those details together gives you a strong starting point before you speak with a lender.

Working with a broker who has real experience in non-traditional lending matters more here than in a conventional deal. David Roa brings over 25 years of experience and has funded more than $150 million across residential, commercial, and investment transactions, including bank statement and DSCR programs that most banks won't touch. If you're ready to find out what you qualify for, connect with David Roa today and get a direct answer about your options without the runaround.