What Is a DSCR Loan? How It Works, Pros, Cons, Requirements

Most real estate investors hit the same wall: banks want to see W-2s, tax returns, and personal debt-to-income ratios that don't reflect their actual ability to manage profitable properties. If you've ever lost a deal because your "on-paper" income didn't satisfy a traditional lender, you're not alone. That's exactly where a DSCR loan comes in, a financing option that qualifies you based on what the property earns, not what your tax returns show.

DSCR stands for Debt Service Coverage Ratio, and it's become one of the most practical tools for investors building rental portfolios or scaling into commercial real estate. At David Roa's lending practice, we've funded over $150 million in loans across residential, commercial, and investor-focused products, including DSCR financing for clients who need a smarter path to approval.

This guide breaks down how DSCR loans work, who they're designed for, and the specific requirements you'll need to meet. We'll also cover the real pros and cons so you can decide if this loan type fits your investment strategy.

How DSCR loans work

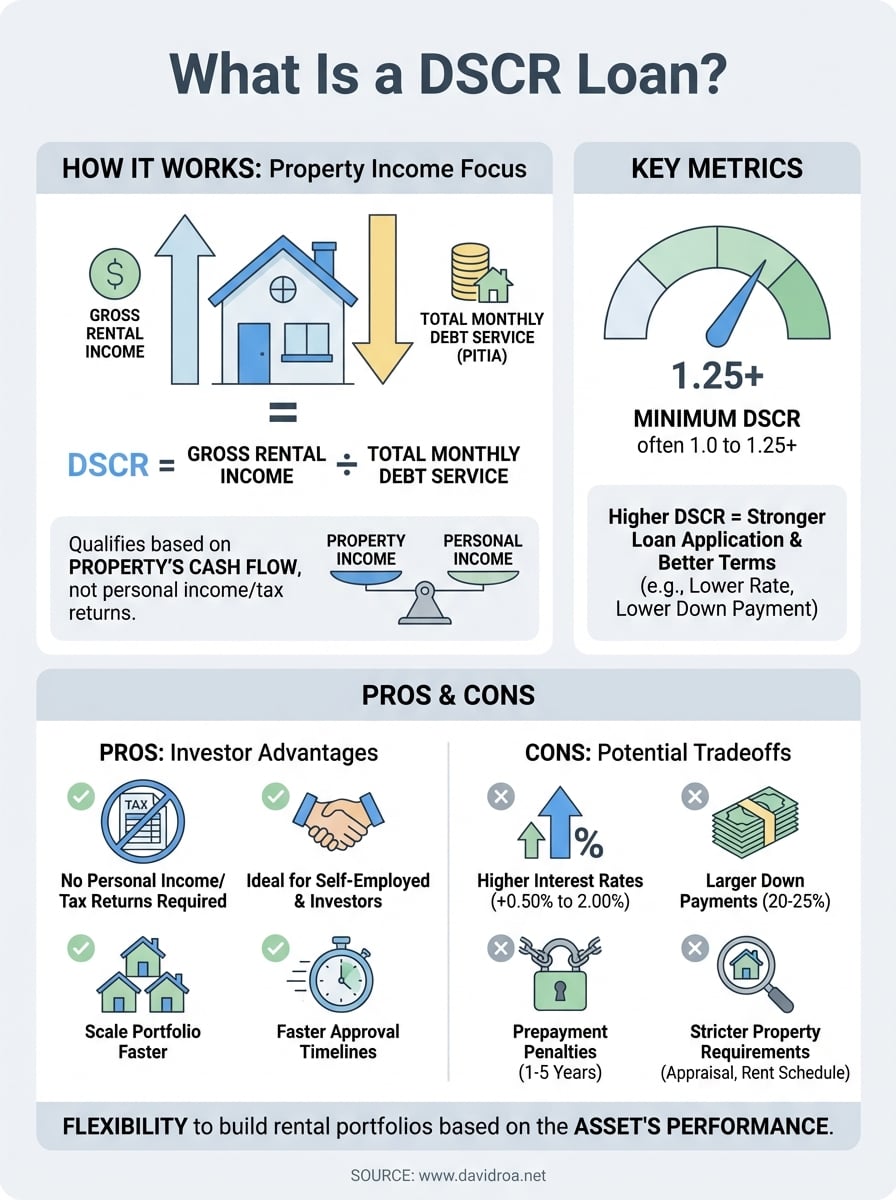

A DSCR loan shifts the qualification focus from your personal income to the property's rental income. Instead of digging through your W-2s or 1099s, lenders calculate whether the property generates enough monthly cash flow to cover its mortgage payment, taxes, insurance, and other expenses. If the property's income exceeds its debt obligations, you can qualify, even if your personal tax returns show low income or complex deductions that traditionally hurt your borrowing power.

The income-to-debt comparison

Lenders calculate your DSCR by dividing the property's gross rental income by its total monthly debt service. Gross rental income includes what you collect in rent each month, while debt service covers the principal, interest, taxes, insurance, and HOA fees (often called PITIA). If your property brings in $2,500 per month and the total debt service is $2,000, your DSCR is 1.25. Most lenders require a minimum DSCR of 1.0 to 1.25, meaning the property must generate at least as much income as the debt costs, or slightly more.

The property pays for itself, so your personal income becomes a secondary concern.

The qualification process

When you apply for a DSCR loan, you submit an appraisal and a rent schedule or lease agreement to document the property's income potential. If the property is vacant or you're purchasing it, lenders use a market rent analysis from the appraisal to project what it could earn. They don't ask for tax returns, paystubs, or employment verification in most cases. Instead, they focus on the asset itself: location, condition, market rent comparables, and the DSCR calculation. You'll still need to show sufficient down payment funds (typically 20 to 25 percent) and meet credit score minimums, but understanding what is a dscr loan means recognizing that the property's cash flow does the heavy lifting for approval.

DSCR ratio explained with examples

Understanding what is a dscr loan requires grasping the math behind the ratio itself. The calculation is straightforward: you take the property's monthly rental income and divide it by the monthly debt service (the full mortgage payment plus taxes, insurance, and HOA fees). The result tells lenders whether the property can sustain its own debt load without relying on your personal income.

Calculating the DSCR

You find your DSCR by dividing gross rental income by total monthly debt obligations. If a property generates $3,000 per month in rent and the total debt service is $2,400, your DSCR is 1.25 ($3,000 ÷ $2,400). Most lenders prefer a ratio of 1.20 or higher, which shows the property produces 20 percent more income than its debt costs. A DSCR of 1.0 means the property breaks even, while anything below 1.0 signals a cash flow shortfall.

A higher DSCR strengthens your loan application and can unlock better interest rates.

Real-world DSCR examples

Consider two properties: Property A earns $2,500 monthly with a $2,000 debt service, producing a DSCR of 1.25. Property B earns $2,200 monthly with the same $2,000 debt service, yielding a DSCR of 1.10. Lenders view Property A as the safer bet because it has more cash flow cushion. If Property B's rent drops or expenses rise, it could struggle to cover the mortgage. Lower DSCR ratios often result in higher interest rates or larger down payment requirements, so maximizing your property's rental income directly impacts your financing terms.

DSCR loan requirements and common terms

DSCR loans carry specific qualification standards that differ from conventional financing, but they're generally more flexible for investors. You won't need to provide tax returns or employment verification, which removes the documentation burden that traditional lenders impose. However, you'll still face requirements around credit scores, down payments, and property type that determine whether you qualify and what terms you receive.

Credit and down payment standards

Most lenders require a minimum credit score of 620 to 680, though higher scores unlock better rates and lower down payment options. You'll typically need to put down 20 to 25 percent of the purchase price, though some lenders offer programs with as little as 15 percent down if your credit and DSCR are strong. The property must be an investment property (single-family, multi-family, or small commercial), and lenders often cap the number of financed properties you can hold at once, usually between 5 and 10 properties depending on the lender's portfolio limits.

Interest rates and loan terms

DSCR loan interest rates run 0.50 to 2.00 percentage points higher than conventional mortgages because lenders view them as riskier without personal income verification. You'll find 30-year fixed, adjustable-rate, and interest-only options, depending on your investment strategy and cash flow needs. Prepayment penalties are common, often lasting 1 to 5 years, so you'll pay a fee if you refinance or sell early.

Higher DSCR ratios and larger down payments directly reduce your interest rate and improve your loan terms.

Pros and cons of DSCR loans

DSCR loans offer distinct advantages for real estate investors, but they come with tradeoffs that affect your financing costs and long-term strategy. You need to weigh the qualification flexibility against higher interest rates and stricter property requirements to determine if this loan type aligns with your investment goals. Understanding what is a dscr loan means recognizing both the benefits and the limitations before you commit to this financing path.

Key advantages for investors

You qualify based on property cash flow instead of personal income, which removes the documentation burden of tax returns, W-2s, and employment verification. This makes DSCR loans ideal if you're self-employed, own multiple businesses, or take significant tax deductions that reduce your reported income. You can also scale your portfolio faster because lenders evaluate each property independently rather than stacking personal debt-to-income ratios across your entire portfolio. Approval timelines typically run faster since underwriters focus on the asset, not your financial history.

The property's income does the work, so your personal finances stay separate from your investment strategy.

Potential drawbacks to consider

Interest rates run 0.50 to 2.00 percentage points higher than conventional loans, which directly increases your monthly payment and reduces your cash flow margin. You'll also face larger down payment requirements (typically 20 to 25 percent) and prepayment penalties that lock you into the loan for 1 to 5 years. Lenders impose stricter underwriting on the property itself, requiring strong market rent data, good condition, and desirable locations to approve your loan.

How to get a DSCR loan

Securing a DSCR loan follows a different path than traditional financing, but the process remains straightforward once you understand what lenders need. You'll focus on property selection and documentation that proves rental income potential rather than gathering personal financial statements. Most investors complete the process in 30 to 45 days, assuming the property meets underwriting standards and you provide accurate documentation upfront.

Find a DSCR-focused lender

You need to work with lenders who specialize in investor financing because traditional banks rarely offer DSCR products. Start by contacting mortgage brokers who maintain relationships with private lenders and portfolio lenders that fund investment properties. Ask about their minimum DSCR requirements, credit score thresholds, and property restrictions before you submit an application. Brokers often access multiple lenders simultaneously, which gives you better rate shopping power and faster approvals.

Prepare your property documentation

Lenders require an appraisal with a rent schedule that documents the property's income potential based on comparable rentals in the area. If the property already has tenants, you'll submit current lease agreements showing monthly rent amounts and lease terms. You'll also provide proof of down payment funds through bank statements or asset verification, along with property insurance quotes and title work.

Understanding what is a dscr loan means knowing that the property's numbers matter more than your personal financial history.

Submit and close your loan

Your lender reviews the DSCR calculation, orders the appraisal, and underwrites the file based on property cash flow and your credit profile. Approval typically takes 2 to 3 weeks, followed by a standard closing process where you sign loan documents and transfer funds.

Next steps

You now understand what is a dscr loan and how it uses property cash flow instead of personal income to qualify investors for financing. This loan type removes traditional documentation barriers and lets you scale your portfolio based on rental income performance rather than tax returns or W-2s. The tradeoff comes in higher interest rates and larger down payments, but the qualification flexibility often outweighs these costs if you're building a rental business or managing multiple properties.

Your next move depends on whether you have a property identified or you're still evaluating investment opportunities. If you've found a deal, contact a DSCR-specialized lender to verify the property meets minimum ratio requirements and run preliminary numbers. If you're still searching, focus on properties with strong market rent potential that will support a DSCR above 1.20.

At David Roa's lending practice, we help investors structure DSCR loans and other investor-focused financing products that align with your portfolio goals. Explore our real estate investment financing options to see how we can support your next acquisition.