What Is an SBA Loan? Types, Terms, and Who Qualifies in 2026

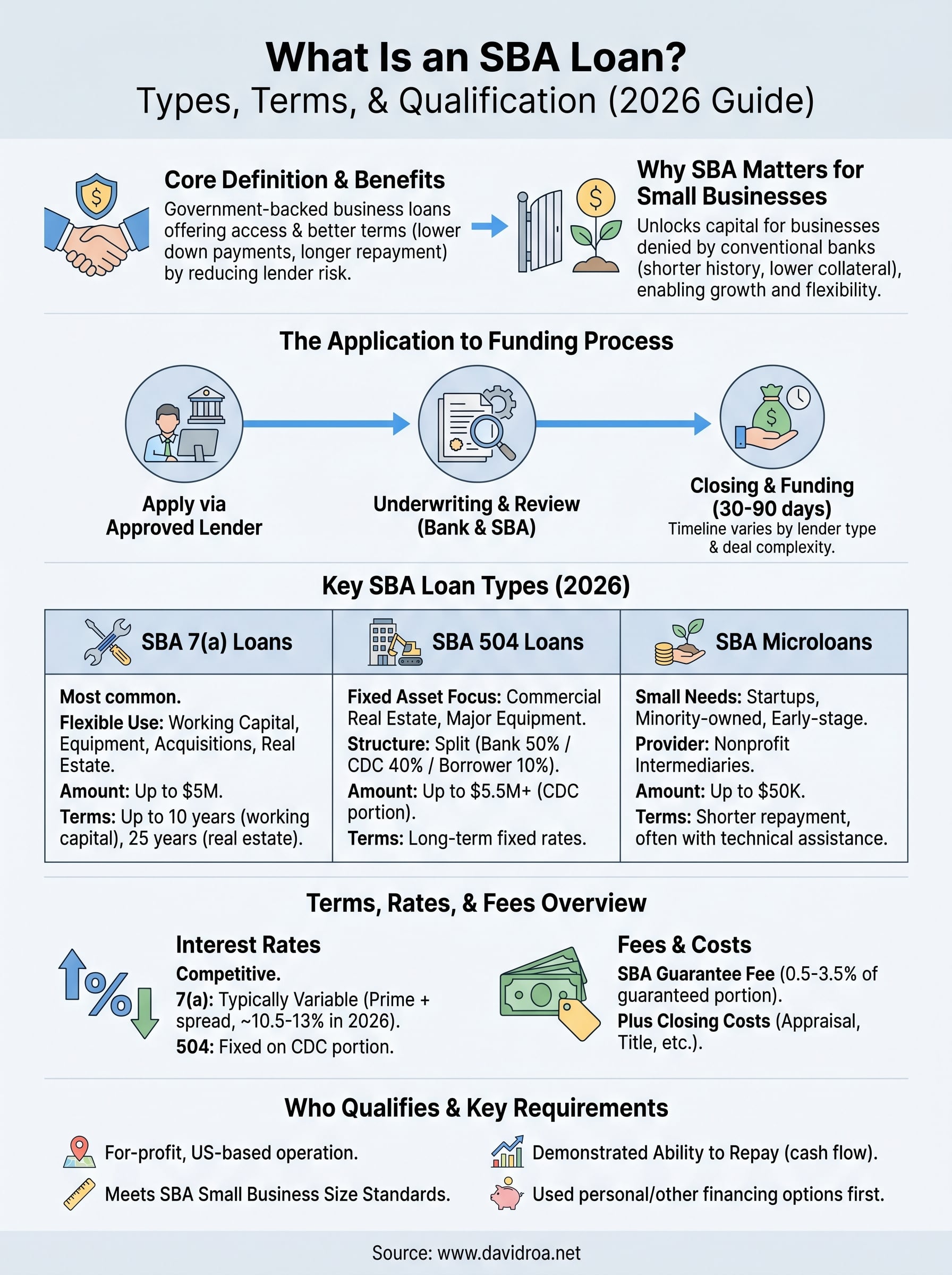

If you've ever asked what is an SBA loan, the short answer is this: it's a business loan partially guaranteed by the U.S. Small Business Administration, which reduces risk for lenders and opens the door for borrowers who might not qualify through conventional financing alone. That guarantee is the reason SBA loans carry lower down payments and longer repayment terms than most traditional commercial products.

But the full picture matters more than the summary. SBA loans come in several forms, 7(a), 504, microloans, each built for different purposes, funding amounts, and borrower profiles. Choosing the wrong one costs you time, money, or both. Understanding how each program works before you apply puts you in a stronger position to actually get approved and fund your business the right way.

Over the past 25-plus years, I've helped business owners across Chicago and nationwide secure SBA 7(a) and 504 loans for everything from equipment purchases to full commercial acquisitions. At David Roa, we work directly with borrowers to match them with the right program, not just the first one that comes up. This guide breaks down the types of SBA loans available in 2026, the terms you can expect, and exactly who qualifies so you can walk into the process informed and ready.

Why SBA loans matter for small businesses

When most business owners first encounter SBA programs, they focus on the interest rate. That's understandable, but the more important advantage is access. The SBA guarantee changes the math for lenders, which means businesses that get turned down by conventional banks often qualify for SBA financing through the same institution or a participating alternative lender. That shift matters enormously if you're trying to grow, acquire equipment, or purchase commercial property without having perfect credit or years of audited financials.

The guarantee changes what lenders will approve

The SBA doesn't lend money directly to you. Instead, it guarantees a portion of the loan to the approved lender, typically 75 to 85 percent depending on the program. That backstop reduces the lender's exposure, so they're more willing to approve borrowers with shorter operating histories, lower collateral, or non-traditional income documentation than a standard commercial loan would allow. Lenders still evaluate your credit and financials, but the bar shifts because their downside risk drops significantly.

When a lender knows the federal government covers most of their loss if a loan defaults, they extend credit to businesses they'd otherwise decline outright.

This is why understanding what is an SBA loan goes beyond just comparing interest rates. The guarantee is the mechanism that makes the entire program work for small business owners who don't fit the conventional mold. If your business has been operating for two years, earns steady revenue, but lacks the collateral a bank typically requires, SBA financing can be the difference between getting funded and being turned down flat.

Access to capital that conventional lending often blocks

Small businesses face a specific problem: banks price risk aggressively, and anything outside a clean balance sheet triggers automatic declines or heavy collateral demands. SBA programs exist to fill that gap directly. A restaurant owner, a contractor, a medical practice, or a retail operator with solid cash flow but limited hard assets often has no realistic path to growth capital through traditional channels.

SBA loans give you longer repayment terms, sometimes up to 25 years for real estate and 10 years for working capital, which lowers your monthly payment and keeps cash available for daily operations. That structure lets you invest in growth without strangling your cash flow. For business owners trying to scale without burning through reserves, the repayment flexibility alone makes SBA financing worth evaluating seriously.

How SBA loans work from application to funding

Once you understand what is an SBA loan and decide it fits your situation, the next step is understanding the process from start to close. The SBA does not take your application directly. Instead, you apply through an SBA-approved lender, which handles underwriting, collects your documents, and submits the loan package for SBA guarantee approval on your behalf.

Finding an SBA-approved lender

Your lender choice shapes how fast your loan moves. Preferred Lenders, those designated under the SBA's Preferred Lender Program, have authority to approve loans without waiting for SBA review on every file, which cuts weeks off the timeline. Working with a broker who already has relationships with multiple approved lenders gives you a better shot at matching your profile to the right institution quickly rather than starting over after a decline.

Choosing a Preferred Lender versus a standard participating lender can be the difference between closing in 30 days and waiting three months.

What happens after you apply

After you submit your application, the lender reviews your business financials, credit history, collateral, and business plan before packaging the file for SBA approval. Underwriting typically takes two to four weeks for standard lenders and as little as one to two weeks through Preferred Lenders. Once the SBA issues its guarantee commitment, the lender finalizes loan documents and closing conditions, which can add another one to three weeks depending on the deal complexity. From first conversation to funded loan, most SBA transactions close in 30 to 90 days depending on the lender type, deal size, and how quickly you supply documentation.

Types of SBA loans in 2026

When people ask what is an SBA loan, they're often thinking of a single product. In reality, the SBA administers several distinct programs, each targeting a specific business need and funding range. Picking the right program before you apply saves you weeks of back-and-forth and keeps your chances of approval high.

SBA 7(a) Loans

The 7(a) is the most widely used SBA program and the one most lenders default to when a business needs flexible capital. You can use 7(a) funds for working capital, equipment, business acquisition, refinancing existing debt, or commercial real estate. Loan amounts go up to $5 million, and repayment terms stretch to 10 years for working capital and 25 years for real estate, which keeps monthly payments manageable while you grow.

The 7(a) program's flexibility makes it the starting point for most small business financing conversations, but it still requires solid documentation and a bankable business profile.

SBA 504 Loans

The 504 program targets fixed asset purchases specifically, meaning commercial real estate and major equipment. It uses a split structure: a conventional lender covers roughly 50 percent, a Certified Development Company (CDC) covers up to 40 percent, and you bring in at least 10 percent as a down payment. Loan amounts through the CDC portion can reach $5.5 million for standard projects and higher for manufacturing or energy-related goals.

SBA Microloans

Microloans address the gap for early-stage businesses or smaller capital needs. The SBA funds nonprofit intermediaries who then lend up to $50,000 directly to qualifying borrowers. These loans work well for startups, minority-owned businesses, or any operation that needs a modest capital injection without meeting the full underwriting requirements of a 7(a) application.

Terms, rates, and fees to expect

SBA loans carry competitive rates compared to conventional commercial products, but knowing what you're actually agreeing to before you sign matters more than the headline number. When you ask what is an SBA loan truly worth, the answer depends on understanding interest rates, repayment terms, and upfront fees together rather than evaluating any one piece in isolation.

Interest rates on SBA loans

Your rate on an SBA loan depends on the program type and current market conditions, and the SBA sets maximum rate limits to keep lenders from overcharging. For 7(a) loans, variable rates typically tie to the prime rate plus a lender spread, and as of 2026, rates generally land between 10.5 and 13 percent depending on your credit profile and loan amount. The 504 program offers fixed rates on the CDC portion, which gives you predictable payments on long-term real estate deals.

Locking in a fixed rate through a 504 loan protects your payment from rising rate environments, which matters when you're planning a 20-year commercial real estate hold.

Fees you'll pay at closing

SBA loans come with guarantee fees charged by the SBA itself, separate from whatever origination or closing costs your lender adds. For 7(a) loans, the guarantee fee ranges from 0.5 to 3.5 percent of the guaranteed portion, scaled by loan size and term. Smaller loans under $150,000 often carry reduced or waived fees.

Common costs you'll typically budget for include:

- SBA guarantee fee: 0.5 to 3.5 percent of the guaranteed loan portion

- Appraisal and environmental reports: required for any real estate transaction

- Title insurance and closing fees: standard on property-secured deals

Budgeting 2 to 4 percent of the total loan amount for closing costs gives you a realistic starting point before you commit to a program.

Who qualifies and how to apply

Before spending time on an application, you need to know whether your business actually meets the SBA's baseline requirements. The core criteria apply across most SBA programs, though individual lenders may impose additional standards on top of what the agency requires. Understanding what is an SBA loan from a qualification standpoint means knowing both the federal rules and the lender overlays that shape real-world approvals.

Basic eligibility requirements

Your business must meet several foundational criteria to qualify for any SBA program. The SBA requires that your company operates for profit, conducts business in the United States, and falls within the agency's size standards for small businesses, which vary by industry and are measured by employee count or annual revenue. You also need to demonstrate that you've used personal assets or other financing options before seeking SBA help, and your credit profile and business finances need to show a realistic ability to repay the loan.

Lenders want to see that your business generates enough cash flow to service the new debt without relying on projections that assume dramatic growth.

How to prepare your application

Gathering your documentation before you approach a lender shortens your timeline significantly. Most SBA lenders request a consistent set of materials regardless of the specific program.

Core documents you'll typically need to provide:

- Business tax returns for the past two to three years

- Personal tax returns for all owners holding 20 percent or more

- Year-to-date profit and loss statement and balance sheet

- Personal financial statement for each owner

- Business plan with financial projections for startups or acquisitions

- Any existing business debt schedules

Organizing these materials in advance signals seriousness to lenders and prevents the back-and-forth that delays most deals.

Next steps if you want SBA financing

Now that you understand what is an SBA loan and how each program works, the most productive move is to assess your specific situation before you contact any lender. Pull together your last two years of business and personal tax returns, your current profit and loss statement, and a rough estimate of how much capital you need and what you'll use it for. That preparation alone separates borrowers who close quickly from those who stall in underwriting for months.

Your lender choice matters as much as your documentation. Working with someone who has direct experience structuring SBA 7(a) and 504 deals keeps you from wasting weeks on a program that doesn't fit your business or pushes you toward terms you can't sustain. If you're ready to explore your options or want a straightforward assessment of what you qualify for, connect with David Roa and get the process started.