What Is Equipment Financing? Loans vs Leases Explained

Every business reaches a point where growth depends on having the right machinery, vehicles, or technology, but paying for it all upfront can drain your cash reserves fast. That's where what is equipment financing becomes a critical question, especially for small and medium business owners trying to scale without putting their operations at risk. Whether you're opening a restaurant, expanding a construction crew, or upgrading your office infrastructure, how you fund that equipment shapes your cash flow for years to come.

Equipment financing lets you acquire what you need now and spread the cost over time, either through a loan or a lease. Each option works differently, carries distinct tax implications, and fits different business situations. A loan gives you ownership. A lease gives you flexibility. Choosing the wrong structure can cost you thousands in unnecessary expenses, or lock you into terms that don't match how your business actually operates. Understanding the mechanics of both options puts you in a stronger position before you sign anything.

At David Roa, we work directly with business owners on commercial financing solutions, including equipment loans and SBA programs like the 7(a) and 504. With over 25 years in lending and firsthand experience running businesses, David brings an operator's perspective to every deal, not just a broker's. This article breaks down exactly how equipment financing works, the real differences between loans and leases, and what to consider based on your specific situation so you can make a confident, informed decision.

Why equipment financing matters for businesses

Most business owners treat equipment as a capital expense, something you save up for or put on a business credit card. But that approach ties up cash you need for payroll, inventory, and daily operations. Understanding what is equipment financing means recognizing it as a tool that lets you match the cost of an asset to its productive life, rather than draining your reserves all at once.

Cash flow is your most important lever

When you pay for equipment outright, you trade liquid capital for a fixed asset immediately. That might work if you're sitting on significant reserves, but for most small and medium businesses, it creates a dangerous gap between what you have available and what you need to operate. Equipment financing keeps your cash in your account and spreads predictable monthly payments across the useful life of the asset, which makes budgeting far more manageable.

Preserving cash flow is not just a convenience. It is a structural advantage that lets you respond to unexpected costs, seasonal slowdowns, or new opportunities without scrambling for funds.

The practical benefit shows up fast. A restaurant owner who finances a commercial oven at $800 per month instead of paying $30,000 upfront keeps that capital available for staffing, food costs, and marketing. The cash working inside the business generates more value than the interest cost on a well-structured equipment loan.

Access equipment that drives revenue now

Waiting until you have saved enough to buy equipment outright means delaying your revenue-generating capacity. If a construction company needs a new excavator to take on larger contracts, waiting six months to accumulate the full purchase price means six months of turned-down jobs. Financing lets you put the equipment to work immediately and let the revenue it generates cover the payments.

Your competitive position depends on this timing. Clients notice when your equipment is outdated or when your capacity falls short of what they need. Financing gives you the ability to upgrade on a schedule tied to business growth, not just cash availability, which keeps you relevant and capable in markets where standing still means falling behind.

How equipment financing works step by step

Understanding what is equipment financing at a mechanical level helps you prepare before you approach a lender. The process moves faster than most people expect, and knowing what to bring to the table from the start can cut your approval timeline significantly. Most equipment financing deals close within a few days to two weeks, depending on the lender, the loan size, and how complete your documentation is.

From application to funding

You start by identifying the equipment you need and getting a quote or invoice from the vendor. That document becomes the foundation of your application because lenders tie the loan directly to the asset being purchased. You submit your application along with basic business financials, and the lender underwrites the deal based on your creditworthiness and the collateral value of the equipment itself. Once approved, the lender pays the vendor directly, and you begin making scheduled payments immediately.

The equipment you're financing typically serves as its own collateral, which means lenders often move faster and require less documentation than they would for an unsecured business loan.

What lenders evaluate

Lenders look at a combination of factors to determine your terms and approval odds. Your personal and business credit scores carry significant weight, especially for smaller deals. For larger transactions, lenders also review business revenue, time in operation, and the type of equipment being financed, since assets that hold value well, like commercial vehicles or heavy machinery, reduce the lender's risk and often result in better rates.

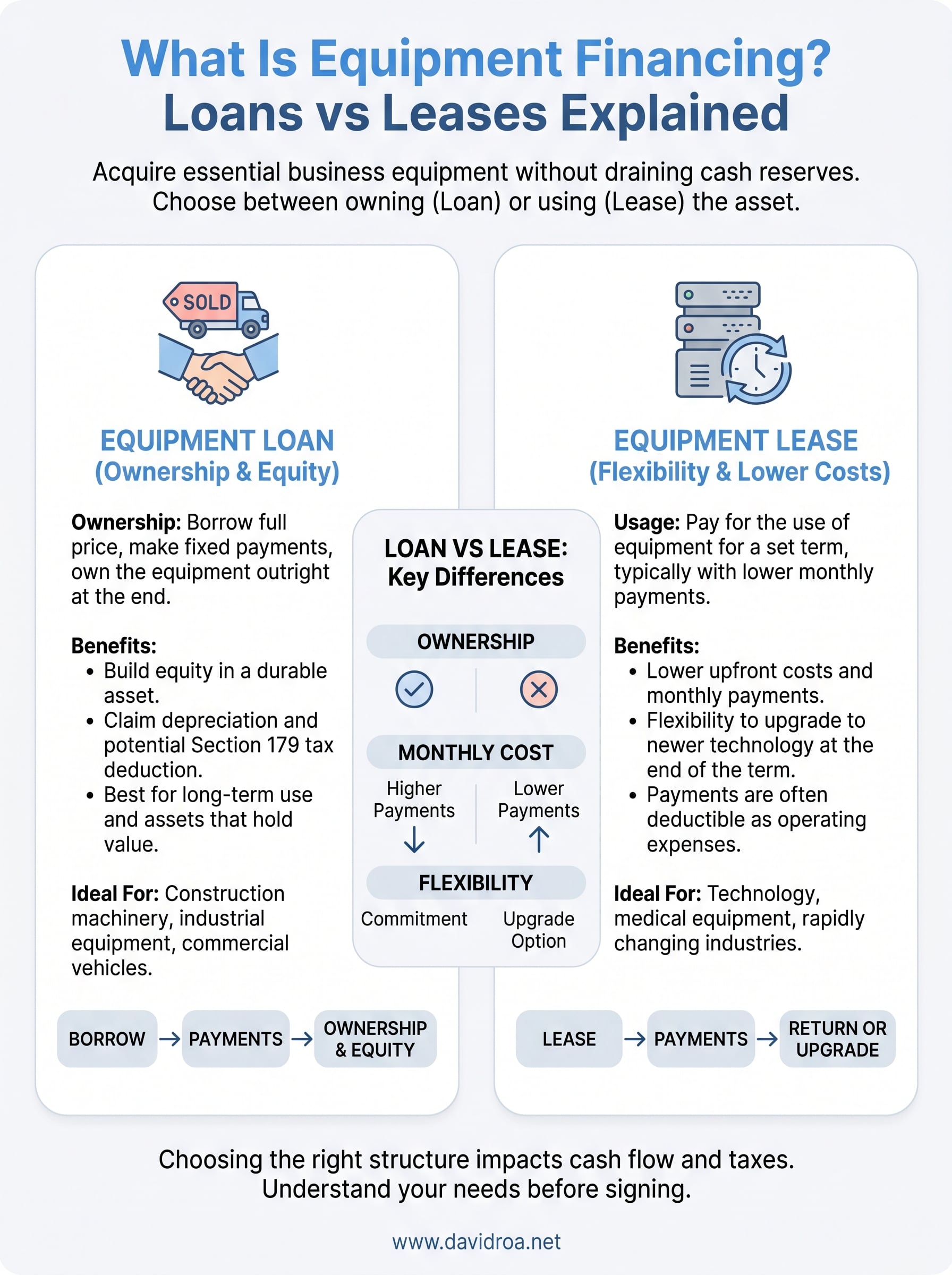

Equipment loan vs equipment lease

When you understand what is equipment financing, the most important decision comes down to one question: do you want to own the asset or simply use it? Both structures let you acquire equipment without a large upfront payment, but they produce very different financial and operational outcomes. Getting this choice wrong means paying more over time or locking yourself into a structure that doesn't fit your business model.

Equipment loans

With an equipment loan, you borrow the full purchase price and make fixed monthly payments until the loan is paid off. At that point, you own the equipment outright. The asset appears on your balance sheet immediately, and you can claim depreciation as a tax deduction over its useful life.

Loans work best when you plan to use the equipment for many years and want to build equity in a durable asset. Commercial vehicles, heavy construction machinery, and industrial kitchen equipment are common examples where ownership delivers the strongest long-term value.

If the equipment holds its value well and has a long useful life, an equipment loan almost always delivers better long-term value than a lease.

Equipment leases

A lease lets you use the equipment for a set term in exchange for monthly payments, without taking ownership at the end. You typically get lower monthly costs compared to a loan covering the same asset, and you can upgrade to newer models when the lease expires.

Leases make sense when your industry moves fast, technology changes frequently, or you need flexibility to scale your equipment mix without being tied to aging assets.

Costs, rates, terms, and tax basics

Understanding what is equipment financing also means knowing the real numbers before you commit. Equipment loan interest rates typically range from 4% to 20%, depending on your credit profile, business financials, and the type of equipment. Lease rates vary too, and the monthly payment you see doesn't always reflect the true cost over the full term. You need to look at the total repayment amount, not just the monthly figure, to make an accurate comparison between options.

What rates and terms look like

Most equipment loans carry fixed monthly payments over terms ranging from 24 to 84 months. Shorter terms mean higher payments but less total interest paid. Longer terms reduce your monthly burden but increase the overall cost of the asset. Lenders set your rate based on your credit score, time in business, and the collateral value of the equipment itself. If you have strong financials and the equipment holds value well, you have real leverage to negotiate better terms.

Comparing the annual percentage rate across multiple lenders, not just the monthly payment, is the most reliable way to evaluate your true borrowing cost.

Tax advantages to know

Both loans and leases offer tax benefits worth factoring into your decision. With a loan, you can deduct depreciation on the equipment, and Section 179 of the IRS tax code lets many businesses deduct the full purchase price in the year it was placed in service, up to current annual limits. Lease payments are generally deductible as a business operating expense, which can simplify your accounting significantly.

Qualifying and choosing the right option

Once you understand what is equipment financing, the next step is figuring out where you stand as a borrower and which structure actually fits your business. Approval requirements vary by lender, but most look at a consistent set of factors that you can prepare for well before you apply.

What lenders want to see

Lenders evaluate your application based on a combination of personal and business factors. Your credit score, revenue history, and time in business carry the most weight for most deals, but the type of equipment also influences how aggressively a lender prices the deal.

Here are the key factors most lenders review:

- Personal credit score: 650 or above opens more options; 700+ gets better rates

- Time in business: Most lenders prefer at least 2 years of operating history

- Annual revenue: Lenders want to see that payments fit comfortably within your cash flow

- Equipment type: Assets that hold value well reduce lender risk and improve your terms

- Down payment: Some lenders require 10-20% down, others finance the full amount

Preparing your last two years of tax returns and three to six months of bank statements before you apply dramatically speeds up the approval process.

Matching the option to your situation

If you plan to use the equipment for many years and it holds its value, a loan gives you ownership and better long-term cost. If your industry changes quickly or you want lower monthly payments with upgrade flexibility, a lease is the stronger fit. The right choice comes down to your cash flow needs, how long the asset stays useful, and your tax situation.

Next steps

Now that you understand what is equipment financing and how loans compare to leases, you can approach lenders with a clear picture of what you need and why. Knowing your credit score, revenue figures, and the type of equipment you're financing before you apply puts you ahead of most borrowers and speeds up the process significantly. The difference between a loan and a lease is not just structural; it shapes your cash flow, tax position, and long-term asset strategy for years after the deal closes.

Start by pulling your last two years of tax returns and three to six months of bank statements. Review your monthly cash flow to determine what payment amount fits comfortably within your budget. Then talk to a lender who understands both the equipment market and how business financing decisions affect your operations overall. If you're ready to move forward, connect with David Roa to discuss your equipment financing options directly.