Commercial Real Estate Definition: Types, Examples, And More

The commercial real estate definition is straightforward, but the category itself covers a lot more ground than most people realize. It goes well beyond office buildings and shopping centers, and understanding exactly what qualifies as commercial property matters when you're making buying, leasing, or financing decisions that involve serious capital.

Whether you're a business owner looking for your first storefront, an investor evaluating a multifamily deal, or a real estate agent guiding a client through an SBA loan scenario, the distinctions between commercial and residential property affect everything from loan structure to tax treatment. Having funded over $150 million in loans across residential, commercial, and investment deals over 25+ years, I've seen firsthand how a clear understanding of these categories helps people make smarter moves with their money.

This article breaks down what commercial real estate actually is, walks through the main property types and real-world examples, and explains how it differs from residential real estate, so you can move forward with clarity and confidence.

Why commercial real estate matters

Commercial real estate drives a significant portion of the U.S. economy. Whether you own a building, lease space inside one, or finance its acquisition, the decisions you make within this asset class carry larger financial consequences than most residential transactions. Understanding the commercial real estate definition is not just academic; it changes how you approach loans, leases, tax planning, and investment strategy from the very beginning. Getting clear on what qualifies as commercial property helps you avoid mismatched financing, prepare the right documentation, and negotiate from a position of knowledge rather than confusion.

The financial scale involved

The numbers in commercial real estate are simply larger across the board. A single strip mall, office building, or apartment complex can represent millions of dollars in value, and the financing structures that support those deals look nothing like a standard 30-year mortgage. Lenders evaluate commercial properties based on income potential, not just appraised value, which means your ability to secure capital depends heavily on how well the property performs or is projected to perform.

If a property generates strong, documented income, lenders will often work with you even when other factors are less than perfect.

This income-based approach shifts the entire conversation. Before you walk into a lender's office, you need to understand debt service coverage ratios (DSCR), net operating income (NOI), and cap rates, because those are the metrics that determine whether your deal gets funded and on what terms. The stronger your grasp of these figures, the better positioned you are to negotiate and close.

What it means for your borrowing options

The type of property you are dealing with directly shapes which loan products are available to you. Residential loans fall under consumer protection laws and follow guidelines from entities like Fannie Mae and Freddie Mac. Commercial loans operate under a different framework, with terms negotiated more directly between borrower and lender. That flexibility can work in your favor, but it also means you carry more responsibility for understanding exactly what you are agreeing to before you sign.

If you are a business owner buying your own building, an SBA 504 or SBA 7a loan may give you favorable rates and longer terms than a conventional commercial mortgage. If you are an investor buying a rental property with five or more units, you are already in commercial territory regardless of what the building looks like from the street. Knowing which category your deal falls into before you apply saves you time and prevents costly surprises at the closing table.

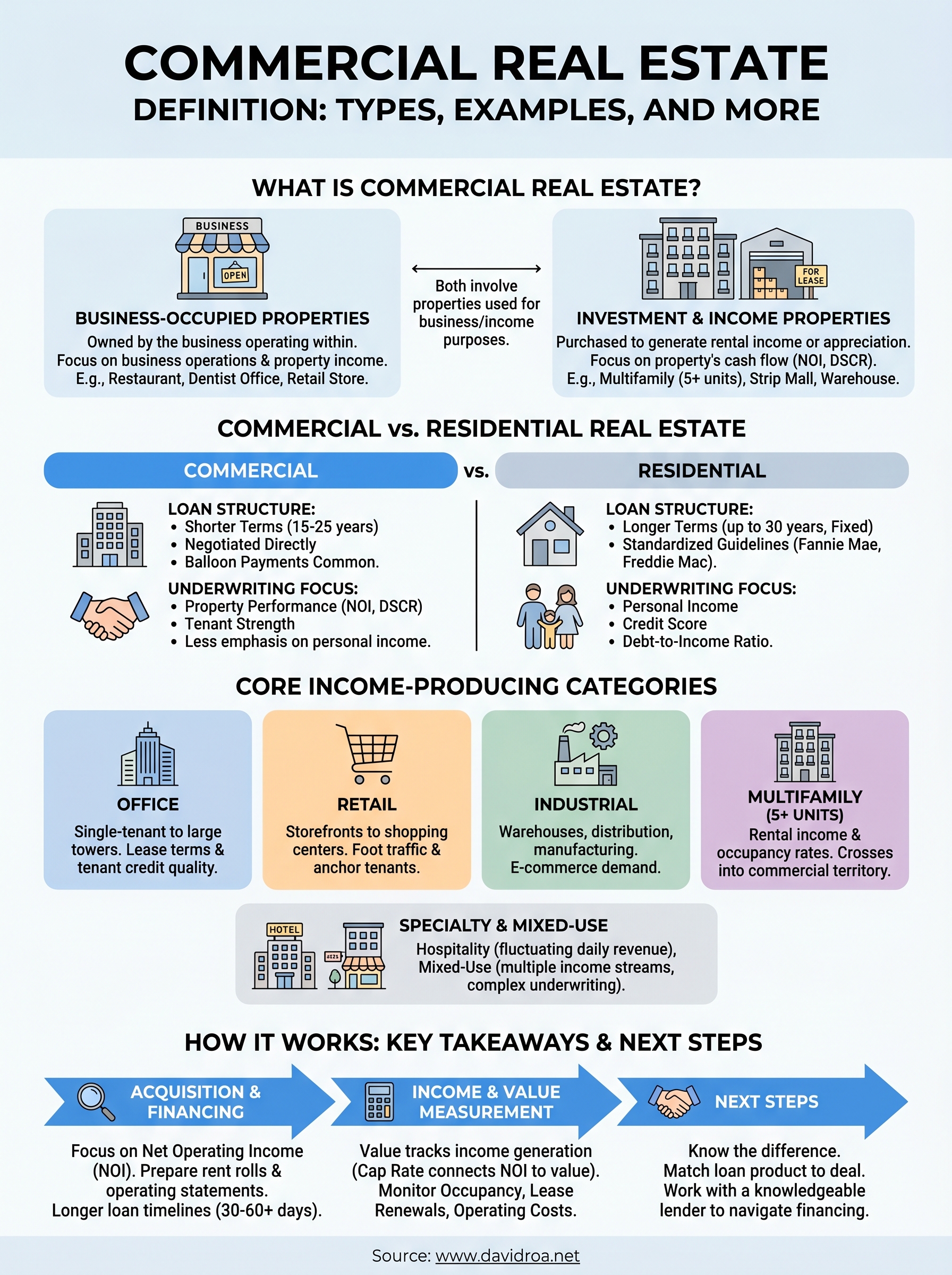

Types of commercial real estate

The commercial real estate definition covers several distinct property categories, each with its own financing requirements and risk profile. Knowing which type you are dealing with helps you match the right loan product to the right deal and set accurate expectations before you ever contact a lender.

Income-producing property categories

The four core categories most lenders and investors reference are office, retail, industrial, and multifamily (five or more units). Each carries its own underwriting standards and tenant structures that directly shape how lenders evaluate the deal you bring to them.

- Office: Single-tenant buildings to large downtown towers, evaluated on lease terms and tenant credit quality

- Retail: Storefronts to shopping centers, assessed on foot traffic patterns and anchor tenant strength

- Industrial: Warehouses, distribution centers, and manufacturing facilities, all driven by sustained e-commerce demand

- Multifamily: Apartment buildings with five or more units, underwritten primarily on rental income and occupancy rates rather than the owner's personal income

Once a multifamily property reaches five units, it crosses into commercial territory and requires commercial financing, not a standard residential mortgage.

Specialty and mixed-use properties

Hospitality properties, such as hotels and motels, operate on a different income model because revenue fluctuates daily rather than through fixed leases. Lenders apply extra scrutiny to these deals and typically require stronger cash reserves plus a documented operating history before approving financing.

Mixed-use properties combine two or more of the categories above into a single building or development, such as ground-floor retail with apartments directly above. These assets offer multiple income streams from one location but add complexity to the underwriting process because each use carries its own risk profile that lenders evaluate separately before issuing a decision.

Commercial real estate examples by use

Walking through real examples makes the commercial real estate definition concrete rather than abstract. The same property can serve completely different purposes depending on how it's used and who occupies it, which directly affects how a lender evaluates the deal and what financing options you can access.

Business-occupied properties

These are properties where a business operates directly from the space. A restaurant owner purchasing the building where they cook and serve customers owns a business-occupied commercial property. The same applies to a dentist buying their own office suite, a mechanic purchasing a repair shop, or a retailer acquiring a storefront rather than leasing one. In each case, the property's value to the owner ties directly to business operations, and lenders often evaluate both the property's income potential and the strength of the underlying business when underwriting these deals.

SBA loans work especially well for business-occupied commercial properties because they help owner-operators build equity instead of paying rent indefinitely.

Investment and income properties

These are properties you buy specifically to generate rental income or long-term appreciation, not to operate your own business inside. A 10-unit apartment building, a strip mall with multiple retail tenants, a self-storage facility, and a warehouse leased to a logistics company all fall into this category. What ties them together is that the property itself produces the income, and lenders underwrite the deal based on that cash flow rather than your personal earnings. This is where DSCR loans become particularly useful, since your qualification depends on whether the property's income covers the debt payment rather than on your W-2 or tax returns. For investors managing multiple properties, that distinction opens doors that traditional income documentation would otherwise keep closed.

Commercial vs residential real estate

The commercial real estate definition draws a clear line between properties used for business or investment purposes and those used as personal residences. That line matters enormously when you apply for financing, because the loan products, qualification criteria, and legal frameworks on each side of that line are fundamentally different. Treating them as interchangeable leads to mismatched applications, wasted time, and sometimes a deal that falls apart entirely.

Loan structure and terms

Residential loans follow standardized guidelines set by agencies like Fannie Mae and Freddie Mac, which keeps rates competitive and terms predictable, often stretching to 30 years with fixed interest. Commercial loans operate on shorter amortization schedules, typically 15 to 25 years, and lenders negotiate terms directly with borrowers based on property performance and borrower financial strength rather than a uniform checklist. That flexibility is useful, but it also puts more responsibility on you to understand the numbers before you sign.

The shorter terms and balloon payments common in commercial lending mean you need to plan your exit or refinance strategy from day one, not after the fact.

Property use and income requirements

Residential underwriting centers on your personal income, credit score, and debt-to-income ratio. Commercial underwriting shifts the focus to the property itself, specifically its ability to generate income sufficient to cover the debt obligation. A strong net operating income and favorable DSCR carry more weight than your pay stubs when a lender evaluates a commercial deal. This is why two borrowers with identical credit profiles can face completely different approval outcomes depending on whether they are buying a single-family home or a six-unit apartment building. Knowing which category your property falls into before you apply keeps the process moving in the right direction.

How commercial real estate works

Understanding the commercial real estate definition is the starting point, but knowing how transactions actually move from interest to closing gives you a real advantage. Commercial real estate deals follow a distinct process that differs from residential purchases in timeline, documentation, and due diligence requirements. Most transactions involve an acquisition phase, a financing phase, and an ongoing management or exit phase that you need to plan for before you ever make an offer.

The acquisition and financing process

When you identify a commercial property, your first step is evaluating the financials, not just the location. Lenders and experienced buyers focus on net operating income (NOI), which is the property's gross income minus operating expenses. That figure tells you whether the property can sustain itself and service the debt. Before you submit a loan application, you will typically need rent rolls, operating statements covering at least two years, and a current rent lease review.

The stronger your property's documented income history, the more leverage you have when negotiating financing terms with a lender.

Loan approval timelines in commercial deals run longer than residential, often 30 to 60 days or more, because underwriters evaluate the property's performance as thoroughly as they evaluate your financials. Appraisals also differ since commercial valuations rely heavily on the income approach rather than comparable sales alone.

How income and value are measured

Once you own a commercial property, its value tracks closely with its ability to generate consistent income. Investors and appraisers use the capitalization rate, or cap rate, to connect NOI to market value. A lower cap rate signals stronger demand and lower perceived risk in that market. Tracking your occupancy rates, lease renewal terms, and operating costs on a regular basis keeps you positioned to refinance, sell, or expand your portfolio from a place of informed decision-making.

Key takeaways and next steps

The commercial real estate definition covers any property used for business purposes or income generation, from retail storefronts and office buildings to industrial warehouses and multifamily properties with five or more units. Each category carries distinct financing requirements, underwriting criteria, and income metrics that determine which loan products fit your deal and what documentation you need to bring to the table.

Knowing the difference between commercial and residential real estate saves you time, prevents mismatched applications, and positions you to negotiate from a place of real knowledge rather than guesswork. Whether you are buying your first commercial building, evaluating a rental portfolio, or exploring an SBA loan for your business, the fundamentals covered here apply directly to every decision you make.

Your next step is working with a lender who understands these deals from the inside out. Connect with David Roa to talk through your specific situation and find the right financing path forward.