What Is Commercial Real Estate? Types, Examples, Differences

What is commercial real estate, and why should you care? If you're a business owner looking for space to operate, an investor building a portfolio, or simply exploring your options beyond residential property, understanding this category of real estate is the first step toward making smarter financial decisions.

Commercial real estate covers everything from office buildings and retail centers to warehouses and multifamily apartment complexes. It operates under different rules than residential property, different financing structures, different lease terms, and different ways to generate income. These distinctions matter, especially when you're putting real money on the line. With over 25 years in mortgage lending and commercial financing, I've helped business owners and investors across the Chicago area and nationwide secure funding for every type of commercial property you'll read about below.

This article breaks down the core types of commercial real estate, walks through real examples, and explains how commercial properties differ from residential ones. Whether you're evaluating your first commercial deal or comparing asset classes for your next investment, you'll walk away with a clear, practical understanding of the space.

Why commercial real estate matters

Commercial real estate touches nearly every part of daily life. The office where you work, the grocery store where you shop, the warehouse that stores goods before they ship to your door all fall under this category. When you understand what is commercial real estate and how it functions as an economic engine, you start to see why lenders, investors, and business owners treat it differently from a single-family home.

It drives the economy at every level

Commercial properties don't just sit there. They generate jobs, enable commerce, and create the physical infrastructure that businesses need to operate. Every lease signed in a retail strip mall means a business owner can open their doors. Every industrial building filled by a logistics company means goods move from point A to point B. The connection between commercial real estate and broader economic activity is direct and measurable.

Commercial real estate and the businesses that occupy it account for a substantial share of U.S. employment and GDP, which is why shifts in this market get attention from economists, lenders, and policymakers alike.

Business owners benefit from this understanding because knowing where the market is heading helps you decide whether to buy your business location outright or lease it. For investors, tracking commercial real estate activity gives you a clearer picture of where industries are expanding or pulling back.

It creates real income potential for investors

Residential properties can generate rental income, but commercial properties often take that potential to another level. Long-term leases, typically three to ten years, give commercial landlords a predictable revenue stream that residential landlords rarely see. Many commercial leases also shift operating costs, like property taxes, insurance, and maintenance, directly to the tenant, which protects the owner's net income without constant out-of-pocket expenses.

For investors evaluating asset classes, the yield on a well-positioned commercial property can outpace what most residential rentals produce. Appreciation in value over time, as the surrounding area develops or as tenant demand increases, adds another layer of return on top of current cash flow.

It opens doors that residential real estate doesn't

If your goal is to scale a real estate portfolio or build lasting wealth, commercial properties offer structures that residential simply cannot match. You can invest through syndications, real estate investment trusts, or direct ownership. You can use the income generated by the property itself, rather than your personal income, to qualify for financing through products like DSCR loans. You can hold multiple tenants in a single building, spreading your risk across several income sources instead of depending on one family to pay rent each month.

The financing options available for commercial real estate are also more varied than most people expect. SBA loans, hard money lending, and conventional commercial mortgages each serve a different type of buyer and a different type of deal. Understanding your options before you approach a lender puts you in a much stronger position to close on the right terms.

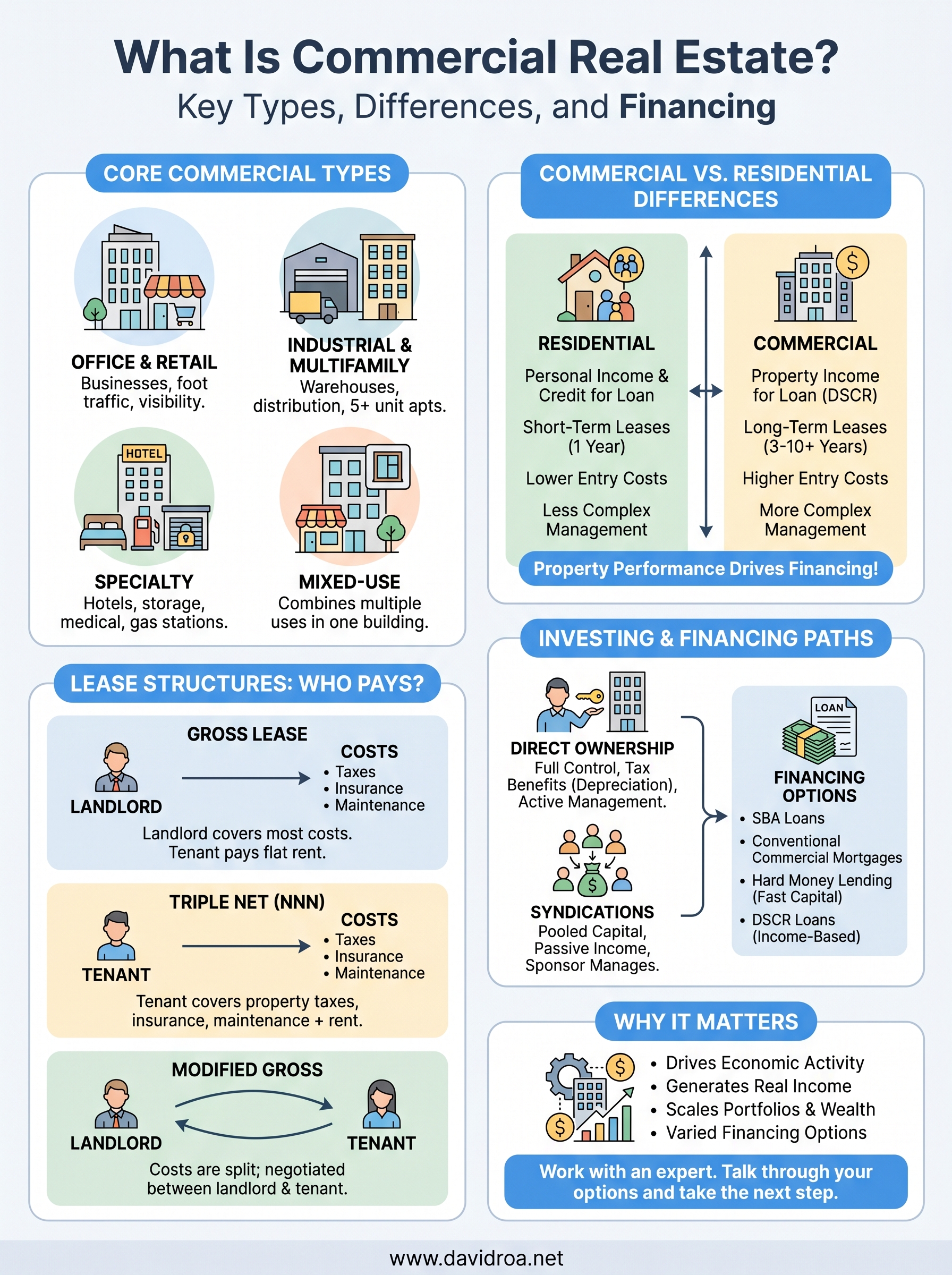

Types of commercial real estate and common examples

When people ask what is commercial real estate, the answer goes well beyond office buildings. Commercial property spans multiple asset classes, each with its own demand drivers, tenant base, and investment profile. Knowing the distinctions helps you identify which type fits your goals before you put capital to work.

Office and retail properties

Office buildings range from single-story suburban suites to high-rise downtown towers, and they typically lease space to businesses rather than individuals. Retail properties include strip malls, standalone storefronts, shopping centers, and big-box locations anchored by national brands. Both categories depend heavily on foot traffic, visibility, and the economic health of surrounding businesses.

Location drives value in retail and office properties more than in almost any other commercial category, which is why the same square footage can command very different rents depending on the street.

Industrial and multifamily properties

Industrial real estate covers warehouses, distribution centers, manufacturing facilities, and flex spaces that combine office and warehouse functions under one roof. Demand for industrial space has grown sharply with the rise of e-commerce and domestic manufacturing. Multifamily properties with five or more units, such as apartment complexes, also fall under the commercial umbrella because they are evaluated and financed on income potential rather than personal use. A 20-unit apartment building, for example, qualifies for commercial financing and is underwritten based on the rent it generates.

Specialty and mixed-use properties

Specialty commercial properties include hotels, self-storage facilities, medical offices, car washes, and gas stations. Each comes with its own operational complexity and underwriting approach. Mixed-use properties combine two or more uses in a single building, such as ground-floor retail with residential units above, and they have become increasingly common in urban and suburban redevelopment projects. If you own a restaurant or operate a business in a physical location, you may already occupy a specialty or mixed-use commercial property without having thought of it in those terms.

Commercial vs residential real estate differences

Understanding what is commercial real estate becomes clearer when you place it side by side with residential property. The two categories follow entirely different rules across financing, leasing, valuation, and risk, and blurring those distinctions is one of the most expensive mistakes new investors make when they first cross into the commercial space.

Financing and loan qualification

Residential mortgages rely heavily on your personal income, credit score, and debt-to-income ratio to determine what you can borrow. Commercial loans flip that equation. Lenders focus on the income the property itself generates, using metrics like the debt service coverage ratio to evaluate whether the property's cash flow can cover the loan payments. This shift means a strong, well-leased property can qualify for financing even when your personal income picture is complicated, which opens real opportunities for investors who operate through LLCs or rely on non-traditional income streams.

Because commercial lenders underwrite the deal based on property performance, a building with stable tenants can be easier to finance than a vacant one regardless of the borrower's personal financial profile.

Lease terms and tenant relationships

One-year lease agreements are the norm on the residential side, which gives landlords little visibility into future income. Commercial leases typically run three to ten years or longer, locking in revenue and making the investment significantly more predictable. Many commercial lease structures, including triple net leases, push property taxes, insurance, and maintenance costs directly to the tenant, which reduces the owner's ongoing out-of-pocket obligations. The landlord-tenant relationship in commercial real estate tends to be more formal, contract-driven, and operationally detailed than anything you encounter managing a single-family rental.

Risk and return profiles

Commercial properties carry higher entry costs and more complex management responsibilities than most residential investments. Vacancy can hit cash flow hard because a single tenant often occupies a large share of the building, and finding a replacement takes longer than placing a new residential renter. On the return side, cap rates and net operating income give you cleaner tools to measure performance, compare deals, and negotiate price based on the property's actual financial output rather than neighborhood comparable sales alone.

How commercial leases work

Commercial leases operate very differently from residential rental agreements, and understanding those differences protects you whether you're a business owner signing a lease for your first location or an investor evaluating a property's income stream. Before you can fully grasp what is commercial real estate and how it functions as an investment, you need to know how the lease structures that govern these properties actually work. The terms embedded in a commercial lease can make or break a deal's profitability for both the landlord and the tenant.

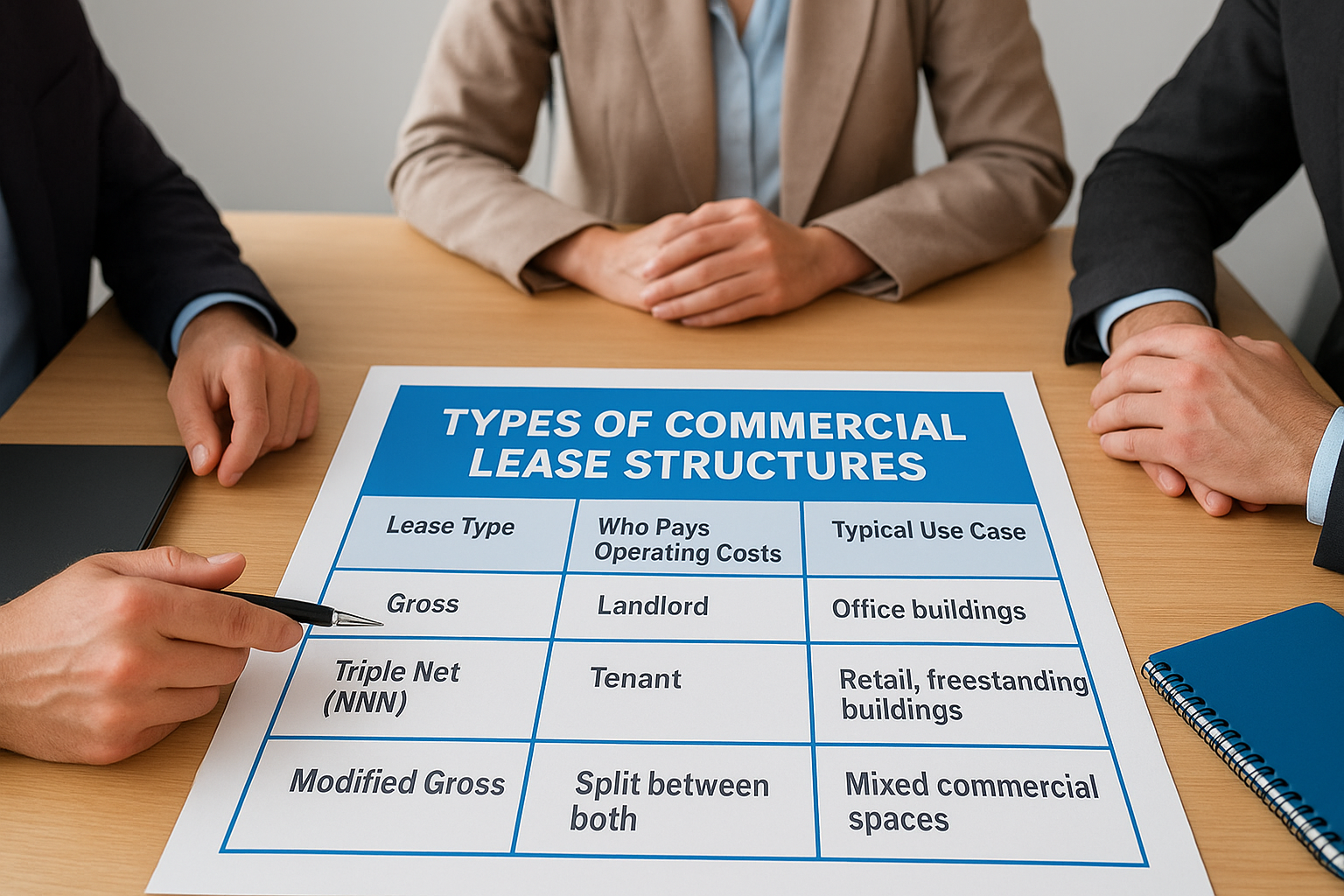

Types of commercial lease structures

The three most common commercial lease types are gross leases, net leases, and modified gross leases, and each one determines who pays for what during the tenancy. Under a gross lease, the landlord covers operating costs like taxes, insurance, and maintenance while the tenant pays a flat rent. Net leases, particularly the triple net structure, shift those costs directly to the tenant, which gives the property owner a cleaner, more predictable income stream. Modified gross leases split the costs somewhere in between, and the exact split is negotiated deal by deal.

In a triple net lease, the tenant handles property taxes, building insurance, and maintenance costs on top of base rent, which is why investors prize these structures for delivering stable, low-management income.

| Lease Type | Who Pays Operating Costs | Typical Use Case |

|---|---|---|

| Gross | Landlord | Office buildings |

| Triple Net (NNN) | Tenant | Retail, freestanding buildings |

| Modified Gross | Split between both | Mixed commercial spaces |

What to watch in lease negotiations

Every commercial lease includes rent escalation clauses and renewal options that have a direct impact on the property's long-term value. Rent escalations lock in annual increases, often tied to a fixed percentage or a cost-of-living index, which protects your returns against inflation over the lease term. You should also pay close attention to exclusivity clauses, permitted use language, and tenant improvement allowances, since these terms define what the tenant can do with the space and who funds any buildout required. Negotiating these details upfront saves both parties from expensive disputes down the road.

How people invest in and finance commercial real estate

Once you understand what is commercial real estate and how its lease structures work, the next question becomes how to actually get into the market. Your entry point depends on how much capital you have, whether you plan to operate the property directly, and which financing tools fit your situation. The good news is that commercial real estate offers more paths to ownership than most asset classes.

Direct ownership and syndications

Buying a commercial property outright gives you full control over leasing decisions, improvements, and sale timing. You take on the management responsibilities, but you also keep the full return. If you prefer a more passive role, commercial real estate syndications let you pool capital with other investors to purchase larger properties, with a sponsor handling operations while you earn a share of the income and appreciation. Both approaches have tax advantages, including depreciation deductions that can significantly offset your annual income from the property.

Depreciation allows commercial property owners to reduce taxable income each year even when the property's market value is rising, which is one of the most powerful wealth-building features of direct ownership.

Financing options for commercial properties

Your financing options range from conventional commercial mortgages and SBA loans to hard money lending and DSCR loans. SBA 7(a) and 504 loans work well for business owners purchasing the property they intend to occupy, offering competitive rates and longer terms than most conventional commercial products. DSCR loans evaluate the property's rental income rather than your personal income, which makes them a strong fit for investors who hold properties through LLCs or earn income in ways that traditional lenders underwrite poorly. Hard money loans provide fast, asset-based capital for time-sensitive acquisitions or fix-and-flip commercial projects where speed matters more than rate.

The financing structure you choose directly affects your cash flow, equity growth, and exit flexibility, so it pays to work with a lender who understands the full range of commercial products rather than one who only offers a single program. Matching the right loan to the right deal separates investors who build durable portfolios from those who struggle to close.

Next steps

You now have a solid foundation for understanding what is commercial real estate, from the core property types and lease structures to the financing tools that make deals work. Commercial real estate rewards people who take the time to learn the rules before they commit capital, and the knowledge you've built here puts you ahead of most first-time commercial buyers and investors.

Your next move is to match that knowledge with the right financing strategy for your specific situation. Whether you're a business owner looking to purchase your location, an investor evaluating a multifamily or retail property, or someone exploring DSCR loans for the first time, the details of your deal determine which loan product fits best. Working with a lender who understands the full range of commercial options makes that process faster and less frustrating. Reach out to David Roa, commercial mortgage expert to talk through your options and take the next step toward closing your deal.