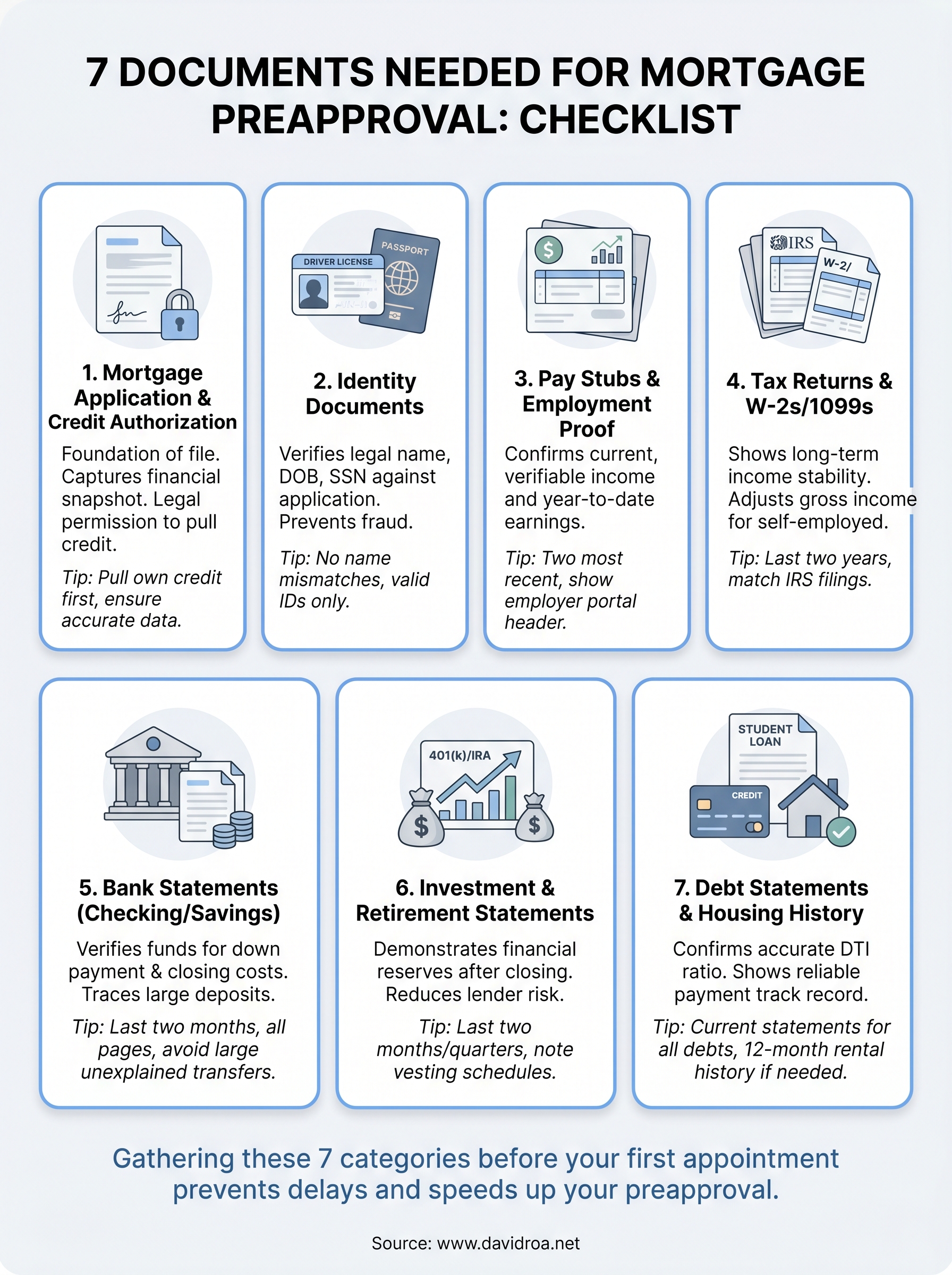

7 Documents Needed for Mortgage Preapproval: Checklist

Walking into a lender's office without the right documents needed for mortgage preapproval is one of the fastest ways to stall your home purchase before it even starts. Lenders need to verify your income, assets, and credit history before they'll issue a preapproval letter, and missing even one document can push your timeline back by days or weeks.

After 25+ years as a mortgage broker and over $150 million in funded loans, I've seen every version of the "I thought I had everything" conversation. At David Roa, we walk borrowers through this process daily, whether it's a first-time buyer gathering pay stubs or a self-employed entrepreneur pulling together tax returns and profit-and-loss statements. The paperwork requirements aren't complicated, but they are specific.

This checklist breaks down the seven core documents your lender will ask for, explains why each one matters, and gives you a clear path to getting your preapproval letter without unnecessary delays. Gather these before your first appointment, and you'll be ahead of most applicants from day one.

1. Mortgage application and credit authorization

The mortgage application, typically the Uniform Residential Loan Application (Form 1003), is the foundation of your entire preapproval file. Before a lender reviews a single pay stub or bank statement, they need your completed application and a signed credit authorization form giving them legal permission to pull your credit report directly from the bureaus.

What it proves to the lender

Your completed application gives the lender a full financial snapshot in one place. It captures your employment history, monthly income, current debts, and the property type you intend to purchase. The credit authorization then lets them verify the debt side of that picture so they can calculate your debt-to-income ratio and determine how much you qualify to borrow.

Without a signed credit authorization, your lender cannot issue a preapproval letter, full stop.

What to prepare before you apply

Before you sit down to complete the application, gather the specific details you'll need to fill it out accurately. Having this information ready shortens the process and reduces back-and-forth with your loan officer.

- Two-year employment history: employer names, addresses, and start/end dates

- Current monthly debts: car loans, student loans, credit cards, and any child support obligations

- Property details (if known): estimated purchase price and planned down payment amount

- Social Security number or ITIN for every borrower listed on the loan

Common issues that delay preapproval

One of the most frequent delays in the documents needed for mortgage preapproval process is a mismatch between what you write on the application and what appears on your credit report. If you list a debt as paid off but it still shows as an open account, your processor has to pause and request a written explanation before moving forward. Another common problem is a missing co-borrower signature on the credit authorization form, which requires a second round of paperwork and adds unnecessary days to your timeline.

Quick tips to keep your file clean

Getting the application right the first time saves everyone involved significant time. A few practical steps make a real difference in keeping your file moving.

- Pull your own credit report at AnnualCreditReport.com before applying so no open accounts catch you off guard

- Disclose all debts upfront, including informal payment arrangements, rather than hoping they won't surface

- Review every line of the completed application before signing to catch any typos in income figures or employment dates

2. Identity documents

Your lender needs to confirm you are who you say you are before issuing a preapproval letter. Government-issued identity documents are the starting point for verifying your personal information against what you submitted on your application, and lenders are legally required to collect them under federal Know Your Customer (KYC) regulations.

What it proves to the lender

Identity verification confirms your legal name, date of birth, and Social Security number match across your application, credit report, and supporting documents. Any inconsistency in your name or ID number flags a potential error or fraud risk, which freezes your file until the discrepancy is fully resolved.

Fixing a name mismatch after your file is already in review can add several business days to your timeline.

What to gather for US citizens and non-citizens

Being prepared means knowing which specific documents apply to your residency status. This is one area of the documents needed for mortgage preapproval process where requirements differ significantly depending on your situation.

- US citizens: valid driver's license or state-issued photo ID, plus your Social Security card if your name changed recently

- Permanent residents: green card (both sides) and a valid government-issued photo ID

- Non-US citizens: ITIN letter from the IRS, valid passport, and proof of legal residency status

Common issues that delay preapproval

The most common delay is a name mismatch between your ID and your loan application, typically caused by a recent marriage or legal name change. Your lender will require a certified legal name change document before the file can move forward.

Quick tips to keep your file clean

- Confirm your photo ID is not expired before your first appointment

- Bring any legal name change documentation if your current name differs from what appears on older financial records

3. Pay stubs and employment income proof

Your lender needs to see current, verifiable income before they'll commit to a preapproval letter. Pay stubs are the most direct evidence that money is coming in consistently, and most lenders require your two most recent pay stubs at a minimum.

What it proves to the lender

Pay stubs confirm that your reported income is real and ongoing, not just a number you wrote on the application. Lenders use your year-to-date earnings to verify that the monthly income you stated lines up with what your employer is actually paying you.

A significant gap between your stated income and your year-to-date figure on your pay stub will trigger an immediate request for a written explanation.

What to gather for salary, hourly, and commission

The documents needed for mortgage preapproval differ slightly depending on how you get paid. Knowing your income type ahead of time helps you pull the right paperwork without a second trip.

- Salaried workers: two most recent pay stubs showing year-to-date earnings and employer name

- Hourly workers: two most recent pay stubs plus documentation of your standard weekly hours

- Commission or bonus earners: two most recent pay stubs and a two-year history showing consistent commission income

Common issues that delay preapproval

A recently changed job title or pay structure is one of the most common triggers for additional documentation requests. If your income shifted from salary to commission within the past 24 months, your lender will need extra verification.

Quick tips to keep your file clean

- Download pay stubs directly from your employer's payroll portal to ensure they show the full official header

- If you changed jobs recently, have your offer letter and start date confirmation ready to accompany your stubs

4. Tax returns and W-2s or 1099s

Tax returns give lenders the clearest picture of your long-term income stability. Most lenders require your last two years of federal tax returns, along with corresponding W-2s from employers or 1099s from clients, to confirm your earnings are consistent year over year.

What it proves to the lender

Your tax returns verify that your reported income matches what you actually filed with the IRS. Lenders compare your adjusted gross income across both years to identify unusual swings or large write-offs that lower your qualifying income on paper.

If your income dropped significantly from one year to the next, your lender will average the two years or use the lower figure, which reduces your maximum loan amount.

What to gather for self-employed borrowers

Self-employed borrowers face the broadest set of requirements when it comes to the documents needed for mortgage preapproval. Your lender needs a fuller picture because your net income after deductions drives the qualifying calculation, not your gross revenue.

- Sole proprietors: two years of personal returns including Schedule C

- S-Corp or partnership owners: two years of personal and business returns (Form 1120S or 1065)

- Freelancers and contractors: two years of 1099s alongside personal tax returns

Common issues that delay preapproval

The most frequent delay for W-2 earners is a mismatch between income on your tax return and your pay stubs. For self-employed borrowers, large business deductions can push your qualifying income well below your actual take-home pay.

Quick tips to keep your file clean

- Request a tax transcript from the IRS at IRS.gov to give your lender a verified copy

- If you filed an extension, have your confirmation and completed return ready before you apply

5. Bank statements for checking and savings

Bank statements verify that the money you plan to use for your down payment and closing costs actually exists in your account. Most lenders require your two most recent monthly statements from every checking and savings account you intend to draw from during the transaction.

What it proves to the lender

Statements confirm that your funds are legitimate, accessible, and not secretly borrowed. Lenders review a 60-day account history and flag any large deposits that don't trace back to a regular paycheck or a clearly documented source.

An unexplained large deposit can freeze your file until you provide a full paper trail showing exactly where those funds came from.

What to gather for down payment and closing costs

This category in the documents needed for mortgage preapproval process is straightforward, but only if you bring complete statements. Partial pages are a common reason files stall mid-review.

- All account pages: every page the bank generates, including any blank pages at the end

- All contributing accounts: checking, savings, and any secondary accounts you plan to draw from at closing

- Gift fund documentation: a signed gift letter plus a bank statement from the donor if part of your down payment is a gift

Common issues that delay preapproval

Large unexplained deposits are the single most common problem lenders flag on bank statements. If you transferred money between accounts before applying, your lender will need statements from both accounts to trace the full transfer history.

Quick tips to keep your file clean

- Download statements directly from your bank's portal rather than exporting a transaction list, which lenders will not accept

- Avoid moving large sums between accounts in the 60 days before you apply

6. Investment and retirement account statements

Investment and retirement account statements show your lender that you have financial depth beyond your checking account. Most lenders request your two most recent monthly or quarterly statements from every brokerage, 401(k), IRA, or similar account you hold.

What it proves to the lender

These statements demonstrate that you have reserves available after closing, which reduces the lender's risk. Lenders want to confirm you can cover several months of mortgage payments if your income temporarily dips, and your account balances are the clearest proof of that cushion.

Strong reserves can sometimes offset a lower credit score or a higher debt-to-income ratio when underwriters evaluate your full file.

What counts as reserves and usable assets

Not every account balance qualifies equally when lenders calculate your usable assets as part of the documents needed for mortgage preapproval review. Knowing what counts helps you present the strongest picture of your financial position.

- Brokerage accounts: fully countable at current market value

- 401(k) and IRA accounts: typically counted at 60-70% of the vested balance to account for early withdrawal penalties and taxes

- Pension accounts: generally excluded unless you can document actual accessibility

Common issues that delay preapproval

Restricted stock units or unvested employer contributions frequently create confusion because they appear on statements but remain inaccessible. Your lender will exclude those amounts, which can lower your usable reserve figure unexpectedly and change your qualification picture late in the process.

Quick tips to keep your file clean

- Provide all pages of every statement, not just the summary page

- Note any vesting schedules in writing so your processor does not have to chase clarification

7. Debt statements and housing history

Your lender needs a complete picture of what you owe, not just what you earn. Debt statements and your housing payment history give underwriters the data they need to confirm your debt-to-income ratio is accurate and that you have a reliable track record of meeting financial obligations on time.

What it proves to the lender

Debt statements verify that every liability on your credit report has a current balance and monthly payment your lender can factor into your DTI calculation. Your rental or mortgage payment history shows whether you consistently meet housing obligations, which lenders treat as the strongest predictor of future repayment behavior.

Lenders give significant weight to housing payment history because it is the most direct parallel to the loan you are applying for.

What to gather for credit cards, loans, and rent

Knowing which specific documents needed for mortgage preapproval fall into this category helps you avoid last-minute scrambling before your appointment.

- Credit card statements: most recent statement for every open account showing current balance and minimum payment

- Auto and student loan statements: current statement with outstanding balance and remaining term

- Rental history: 12 months of canceled checks or bank transfer records if your landlord does not report to the credit bureaus

Common issues that delay preapproval

A debt not listed on your application but visible on your credit report is the most frequent trigger for an explanation letter. Lenders also flag deferred student loans because guidelines require them to count a percentage of the balance as a monthly payment even when the actual payment is zero.

Quick tips to keep your file clean

- Provide all account statements in full, including any accounts you plan to pay off before closing

- Keep written payoff confirmations on hand, since your credit report may not reflect a zero balance right away

Ready to apply

You now have a complete picture of every document needed for mortgage preapproval, from your signed credit authorization to your rental payment history. Gathering these seven categories before your first appointment puts you ahead of most borrowers and gives your loan officer everything required to issue a preapproval letter without unnecessary back-and-forth.

The difference between a smooth process and a stalled one almost always comes down to preparation. Borrowers who arrive with complete, organized files move from application to preapproval letter significantly faster than those who submit documents in pieces over several days. Treat this checklist as a one-time investment that protects your timeline and keeps your offer competitive when the right property appears.

When you're ready to take the next step, connect with David Roa for direct guidance on your specific situation, whether you're a first-time buyer, a real estate investor, or a business owner seeking financing.