5 Down Payment Assistance Programs In Illinois (2026)

The median home price in Illinois has climbed past $260,000, and for many buyers, the biggest obstacle isn't qualifying for a mortgage, it's coming up with the cash to close. That's where down payment assistance programs Illinois offers through state and local agencies can make a real difference. These programs provide grants, forgivable loans, and subsidized financing that reduce or eliminate the upfront costs of buying a home.

With over 25 years in mortgage lending and more than $150 million funded, I've helped hundreds of Illinois buyers, including first-time purchasers and ITIN holders, structure their financing to take full advantage of these programs. At David Roa, we work directly with you to match the right assistance option to your specific loan type and financial situation, whether that's an FHA, VA, or conventional mortgage.

Below, you'll find five active programs available in 2026, broken down by eligibility requirements, income limits, and how to apply.

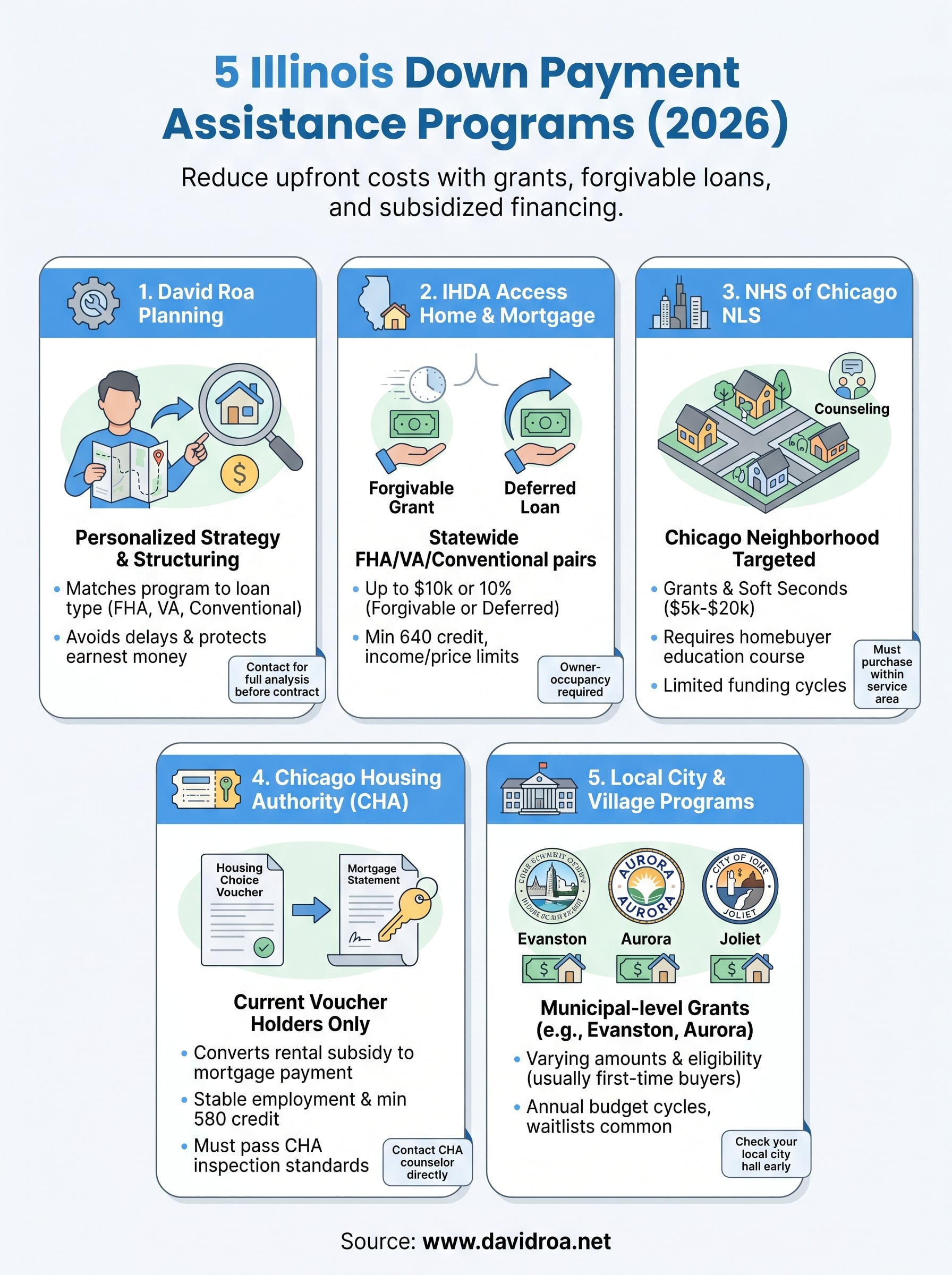

1. David Roa Down Payment Assistance Planning

Before applying to any state or municipal program, you need a clear picture of your full financing stack. At David Roa, we start by reviewing your complete financial profile before recommending which assistance programs fit your loan type, purchase price, and timeline.

What You Get and How It Works

Working with David Roa gives you a dedicated mortgage strategist who maps out your entire path to closing. We identify which down payment assistance programs Illinois offers that you actually qualify for, then build your loan structure around those programs so you maximize the benefit without jeopardizing your approval.

Getting assistance lined up before you go under contract protects your earnest money and keeps your timeline intact.

Who This Is For

This planning service is built for first-time buyers, ITIN holders, and real estate investors who need creative financing. If you earn within program income limits but lack enough cash to close, or if you are a non-U.S. citizen navigating an ITIN loan, David Roa's bilingual team can walk through every option with you in English or Spanish.

What to Bring to the First Call

Come prepared with your two most recent pay stubs and tax returns from the last two years, plus any self-employment income records and a government-issued ID. ITIN applicants should also bring their ITIN letter and supporting income documentation so David can assess your full qualification picture upfront.

How to Stack Assistance with Your Mortgage

Stacking programs means layering a forgivable second loan or grant on top of your primary FHA or conventional mortgage. David reviews each program's subordination requirements to confirm your primary lender will accept the assistance without triggering additional approval conditions.

Common Mistakes This Helps You Avoid

The most common error buyers make is applying for assistance after going under contract, which compresses your timeline and creates closing delays. David also flags programs that carry hidden repayment triggers that buyers often miss when reading the fine print.

2. IHDA Access Home and IHDA Mortgage Programs

The Illinois Housing Development Authority (IHDA) runs the most widely used down payment assistance programs Illinois buyers can access statewide. These programs pair directly with FHA, VA, and conventional loans through IHDA-approved lenders across the state.

What the Program Offers in 2026

IHDA's Access Forgivable and Access Deferred products provide either a forgivable grant or a deferred loan toward your down payment and closing costs, up to $10,000 or 10% of the purchase price, whichever is less.

How the Assistance Is Structured

The Access Forgivable option cancels the full balance after ten years of on-time occupancy. Access Deferred requires repayment only when you sell, refinance, or pay off your primary mortgage, with no separate monthly payment required on the assistance itself.

Choosing forgivable versus deferred depends on how long you realistically plan to stay in the home.

Eligibility Basics and Typical Limits

You need a minimum 640 credit score and must fall within county-specific income and purchase price limits, which typically cap household income around $102,000 and purchase prices around $420,680 depending on the area.

Step-by-Step Application Process

You apply through an IHDA-approved lender, not directly through the authority. Your lender packages and submits your complete file to IHDA alongside your primary mortgage application for simultaneous review.

When IHDA May Not Be the Best Fit

IHDA programs require owner-occupancy, so investment properties are automatically disqualified. If your income or purchase price exceeds the county cap, you will need to look at other local or municipal programs instead.

3. Neighborhood Housing Services of Chicago NLS

Neighborhood Housing Services (NHS) of Chicago offers one of the more targeted down payment assistance programs Illinois urban buyers can access. NHS focuses on underserved Chicago neighborhoods and pairs counseling services with direct financial aid to help buyers close the cash gap.

What the Grant Can Cover

NHS provides grants and soft second loans that cover down payment and closing costs, typically ranging from $5,000 to $20,000 depending on the specific product and how much funding remains in the current cycle.

Eligibility Basics and Service Area

You must purchase within specific Chicago community areas, and your household income must fall within HUD area median income limits, usually at or below 120% AMI. First-time buyer status is typically required for most NHS products.

How to Apply and Timing

You must complete an NHS-approved homebuyer education course before receiving any assistance. After finishing, a housing counselor reviews your full financial profile and connects you with available funding directly.

Start the education course early since funding can run out mid-year once the cycle's allocation is exhausted.

Combining This with Other Programs

NHS assistance can layer on top of an FHA or conventional loan and in some cases pairs with IHDA Access programs when all eligibility conditions align.

Key Tradeoffs to Understand

The geographic restriction is the biggest limitation here. If your target property falls outside NHS service boundaries, this option is unavailable regardless of your income qualification.

4. Chicago Housing Authority Down Payment Assistance

The Chicago Housing Authority (CHA) runs one of the more specialized down payment assistance programs Illinois offers, available exclusively to current voucher holders. If you receive a Housing Choice Voucher, you may redirect part of that subsidy toward your down payment and monthly mortgage costs instead of rent.

What CHA Offers and How It Works

CHA's Homeownership Program converts your rental voucher into mortgage payment support. Some participants also receive a down payment contribution to help cover upfront closing costs at the time of purchase.

Who Qualifies

You need to be a current CHA voucher holder in good standing for at least one year. You also need stable two-year employment, a minimum 580 credit score, and completion of a CHA-approved homebuyer counseling course.

This is not an open public program. Only active voucher holders are eligible to apply.

How to Apply and Required Steps

Start by contacting your CHA housing counselor directly. They confirm your eligibility and connect you with a lender experienced in voucher-to-mortgage conversion before you begin your home search.

How This Affects Your Mortgage Options

Your voucher converts into a mortgage assistance payment that most FHA lenders accept. Confirm your specific loan type is compatible with CHA's structure before signing a purchase contract.

Pitfalls and Deal-Killers to Watch for

Every home must pass CHA inspection standards tied to HUD housing quality requirements. This disqualifies many distressed or fixer-upper properties that buyers typically find at the lower end of Chicago's market.

5. Local City and Village Homebuyer Programs

Beyond Chicago, many Illinois suburbs and downstate municipalities run their own down payment assistance programs Illinois buyers frequently overlook. Cities like Evanston, Aurora, and Joliet operate independent homebuyer programs funded through federal Community Development Block Grants.

Examples to Check First in Your Area

Contact your city or village hall directly to ask about current homebuyer assistance. Rockford, Elgin, and Waukegan each run programs with varying grant amounts tied to local housing priorities and available federal funding.

Common Eligibility Rules Across Municipalities

Most programs require owner-occupancy and first-time buyer status, with income limits set between 80% and 120% of the area median income based on your household size.

How Funding Cycles and Waitlists Work

Municipal programs run on annual budget cycles and often exhaust allocations within weeks of opening. Getting on a waitlist early improves your position before the next funding round.

Check your local program's funding calendar before you begin your home search.

Documents You Usually Need

Expect to provide two years of tax returns, recent pay stubs, a government-issued ID, and proof of residency within the municipality's service boundaries.

How to Combine Local Help With IHDA or Other Aid

Many municipalities allow layering with IHDA Access programs, provided all parties confirm subordination in writing. Your loan officer must coordinate every program simultaneously to prevent closing delays.

Your Next Move

Illinois buyers have more down payment assistance programs Illinois offers than most people realize, but these programs move fast and funding disappears mid-year without warning. Every program covered here has specific income limits, property restrictions, and documentation requirements that can delay or derail your closing if you approach them in the wrong order.

Start by getting your full financial picture reviewed before you fall in love with a property. Knowing which programs you qualify for ahead of time gives you a real negotiating advantage and keeps your earnest money protected once you go under contract.

David Roa has helped buyers across Illinois structure FHA, conventional, and ITIN loans alongside state and local assistance so that every eligible dollar is captured at closing. Reach out today to schedule a call and find out exactly which programs fit your situation in 2026.