How To Qualify For An FHA Loan: Credit, DTI, Down Payment

FHA loans have helped millions of Americans become homeowners, even those turned away by conventional lenders. But before you can take advantage of lower down payments and more flexible credit requirements, you need to understand exactly how to qualify for an FHA loan.

The qualification process involves meeting specific thresholds for your credit score, debt-to-income ratio, and down payment. You'll also need to verify your income, maintain steady employment, and purchase a property that passes FHA appraisal standards. Each piece matters, and missing one requirement can delay or derail your application.

With over 25 years in mortgage lending and more than $150 million funded, I've guided thousands of borrowers through FHA qualification, including first-time buyers, those rebuilding credit, and ITIN holders who thought homeownership was out of reach. This guide breaks down every eligibility requirement so you know exactly where you stand before you apply.

Why FHA loans can be easier to qualify for

FHA loans consistently rank as the most accessible home financing option for buyers who don't fit the conventional lending mold. The Federal Housing Administration backs these mortgages, which allows lenders to accept lower credit scores, smaller down payments, and higher debt ratios than they would for uninsured conventional loans. This government guarantee means you can secure financing even if your financial profile has some rough edges that would typically trigger a denial from traditional banks.

Lower credit score acceptance

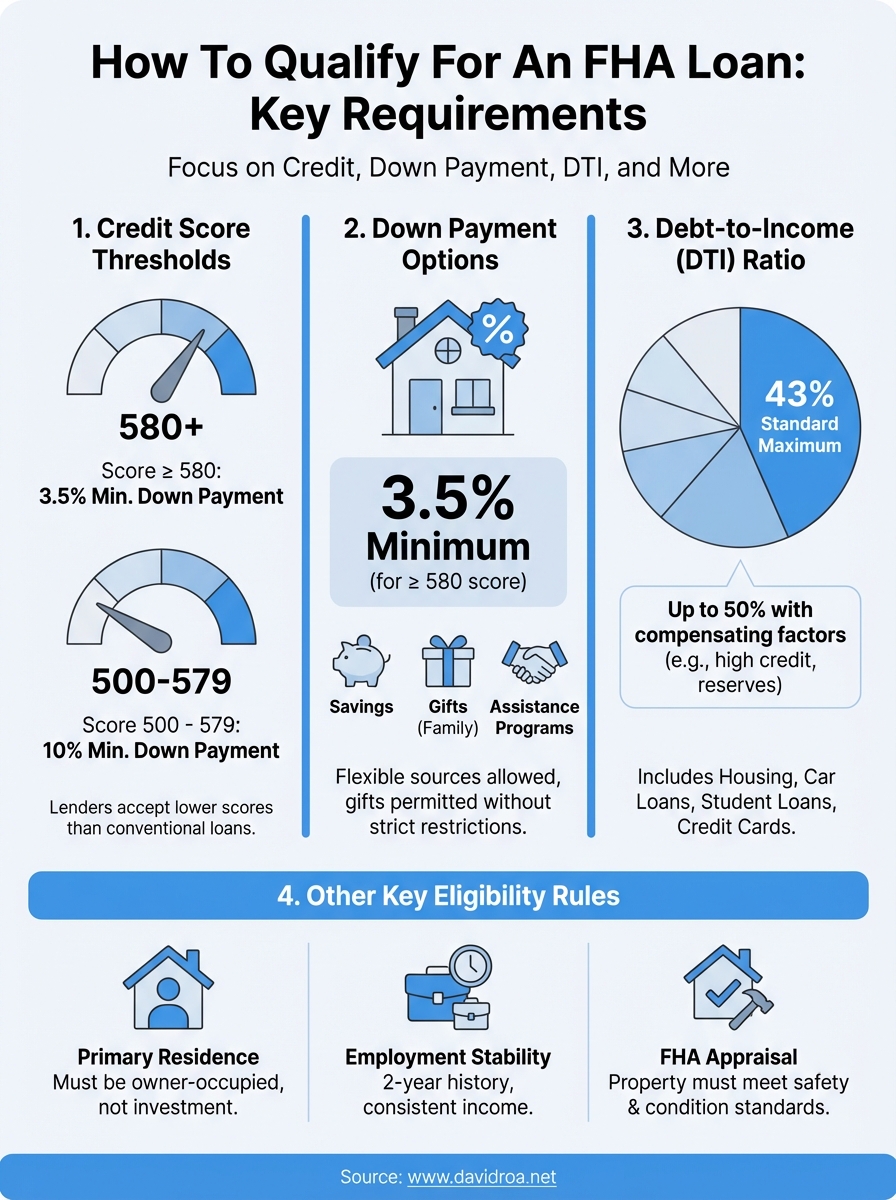

You can qualify with a credit score as low as 580 for the minimum 3.5% down payment, and some lenders will approve borrowers at 500 with a 10% down payment. Conventional loans typically require a 620 minimum, and the best rates start at 740 or higher. This 80 to 120-point difference represents thousands of buyers who would otherwise wait years to rebuild credit before applying.

FHA's flexibility on credit opens the door for recent immigrants, those recovering from medical debt, and anyone rebuilding after divorce or job loss.

Your credit history matters more than just the score itself. Lenders review your payment patterns over the last 12 months and look for stability rather than perfection. A few late payments from two years ago won't automatically disqualify you if you've maintained clean records recently. Many of my clients with past foreclosures or short sales qualify after meeting the mandatory waiting periods (three years for foreclosure, two for short sale with extenuating circumstances).

Smaller down payment options

The 3.5% minimum down payment requirement makes homeownership immediately achievable for buyers without massive savings. On a $300,000 home, you need just $10,500 compared to the $60,000 required for a conventional 20% down payment. Even with private mortgage insurance factored in, you're building equity in your own property instead of paying rent that builds nothing.

Down payment assistance programs stack with FHA loans in most states, which can reduce or eliminate your out-of-pocket cash requirement entirely. Your down payment can also come from gifts from family members without the restrictions conventional loans place on gifted funds. You'll need documentation showing the gift source and that the money doesn't require repayment, but this flexibility helps thousands of buyers who have strong income but limited savings.

Flexible debt-to-income tolerance

FHA guidelines allow your total monthly debts to reach 43% to 50% of your gross income, depending on compensating factors like high credit scores or cash reserves. Conventional loans typically cap at 43%, and many lenders prefer 36% or lower. This extra room means you can qualify even with student loans, car payments, or other obligations that would push you over conventional limits.

Understanding how to qualify for FHA loan approval with higher debt ratios requires you to strengthen other areas of your application. Lenders look at your employment stability, savings, and credit history to offset the risk of higher monthly obligations. A two-year job history in the same field, three months of reserves, and no recent credit issues can justify approval at the higher end of the DTI scale.

Government backing reduces lender risk

The FHA insurance premium you pay protects lenders if you default, which makes them more willing to approve borderline applications they would reject for conventional financing. This insurance costs you 1.75% upfront and an annual premium ranging from 0.55% to 0.80% depending on your loan amount and down payment. While this adds to your monthly cost, it's the trade-off that makes approval possible when you don't meet stricter conventional standards.

Basic FHA eligibility rules lenders check first

Before lenders evaluate your credit score or down payment, they verify you meet the foundational requirements that determine whether you can even apply for FHA financing. These basic eligibility rules act as the first filter in the approval process, and failing any one of them stops your application immediately. Understanding these requirements helps you avoid wasting time on an application you can't complete.

Legal residency and Social Security requirements

You must be a U.S. citizen or legal permanent resident with documentation proving your status. Green card holders qualify without restriction, and you can also apply with certain work visas that demonstrate your legal right to remain in the country for at least three years. Lenders verify this through your Social Security number, which must be valid for employment purposes and match your identification documents exactly.

ITIN holders face additional requirements that conventional loans don't accommodate, but FHA loans paired with specialized programs can work when you have tax history and alternative credit documentation. Your immigration status gets verified through federal databases during underwriting, so incomplete or expired documents will trigger an immediate denial before lenders review anything else about your financial profile.

Primary residence occupancy rule

FHA loans fund owner-occupied properties only, which means you must move into the home within 60 days of closing and live there as your primary residence for at least one year. You cannot use FHA financing to purchase investment properties or vacation homes, and lenders track occupancy through utility hookups, mail delivery, and tax filings. This restriction protects the program's goal of supporting homeownership rather than real estate speculation.

FHA's primary residence requirement ensures the program serves actual homebuyers instead of investors looking for low down payment rental properties.

You can own other properties while applying for an FHA loan, but your existing FHA loan must be paid off or satisfy specific circumstances like job relocation or family size changes. Understanding how to qualify for FHA loan approval when you already own property requires documentation proving you're not trying to build a portfolio through government-backed financing meant for individual homeowners.

Employment and income stability verification

Lenders require a minimum two-year employment history, preferably with the same employer or within the same industry. Gaps longer than six months require written explanations, and you'll need to show consistent income that covers your mortgage payment plus existing debts. Recent job changes don't automatically disqualify you if you stayed in the same field and maintained or increased your income level.

Self-employed borrowers face stricter documentation requirements, including two years of tax returns and year-to-date profit and loss statements. Your income gets averaged across both years, and lenders apply a 25% reduction if your business shows declining revenue trends. This stricter scrutiny reflects the higher risk lenders associate with variable income sources compared to W-2 wage earners.

Credit score and down payment requirements

Your credit score and down payment amount work together to determine your FHA loan eligibility and the specific terms lenders will offer. These two factors represent the most straightforward qualifications you need to meet, with clear numeric thresholds that tell you immediately whether you can proceed with an application. Unlike conventional loans that require near-perfect credit for competitive rates, FHA guidelines create multiple entry points based on your financial position.

Minimum credit score thresholds

Lenders approve borrowers with credit scores as low as 580 for the standard 3.5% down payment, which covers the vast majority of FHA applications. If your score falls between 500 and 579, you can still qualify but must increase your down payment to 10% of the purchase price. This sliding scale means you don't get rejected outright for lower credit, you just need more cash upfront to offset the additional risk lenders take on your application.

Understanding how to qualify for FHA loan approval with a lower credit score means preparing for higher upfront costs or spending months improving your score before applying.

Your middle credit score from all three bureaus determines your eligibility, not your highest or lowest score. Lenders pull reports from Experian, Equifax, and TransUnion, then use the median number for underwriting decisions. If you show scores of 590, 610, and 625, lenders evaluate you at 610, which qualifies you for the minimum down payment tier.

Down payment amounts by credit tier

You need $10,500 on a $300,000 purchase with a 580+ credit score, or $30,000 on the same property if your score sits below 580. This difference represents a significant barrier for buyers with damaged credit, which is why most applicants focus on reaching 580 before applying rather than saving the larger down payment amount. Your down payment can come from savings, gifts, grants, or approved assistance programs without restriction.

How to verify your credit readiness

Pull your credit reports from all three bureaus before you apply to identify any errors, collections, or late payments that could lower your score artificially. You can dispute inaccurate information directly with the credit bureaus, and successful disputes can raise your score quickly enough to qualify for better terms. Focus on paying down credit card balances below 30% of your limits and avoid opening new accounts in the six months before applying, as both actions will improve your middle score without requiring years of perfect payment history.

DTI and income rules that affect approval

Your debt-to-income ratio measures how much of your monthly income goes toward debt payments, and FHA lenders use this calculation to determine whether you can afford the mortgage alongside your existing obligations. Lenders divide your total monthly debts by your gross monthly income to produce a percentage, and FHA guidelines allow ratios up to 43% as a standard maximum, with some lenders approving up to 50% when you have compensating factors. This calculation includes your proposed mortgage payment, property taxes, insurance, HOA fees, student loans, car payments, credit cards, and any other recurring monthly obligations.

Maximum debt-to-income ratio limits

FHA guidelines split your DTI into two components: the front-end ratio (housing expenses only) should stay under 31%, while the back-end ratio (all debts combined) caps at 43% for most borrowers. Lenders can approve ratios between 43% and 50% if you have a credit score above 620, significant cash reserves, or minimal debt increase from your current housing payment. Understanding how to qualify for FHA loan approval at higher DTI levels requires you to strengthen other parts of your application with proof of financial stability.

Reducing your DTI by paying off small debts before applying can shift your application from marginal to strong approval status.

Income calculation methods for W-2 employees

Lenders verify your income through pay stubs covering the last 30 days, W-2 forms from the previous two years, and written employment verification from your employer. Your base salary counts as qualifying income without adjustment, and overtime or bonus income qualifies if you've received it consistently for at least two years with documentation showing it will continue. Lenders average variable income across 24 months to determine a stable monthly amount they can use for qualification purposes.

Self-employed and commission income requirements

You need two years of tax returns with all schedules if you own more than 25% of a business or work primarily on commission. Lenders review your Schedule C or business returns to calculate qualifying income, applying deductions that reduce your taxable income back into the calculation. Your net income after expenses determines approval, and if your business shows declining revenue year-over-year, lenders will use the lower figure or deny the application until you demonstrate income stability through updated financials.

Property rules, appraisals, and loan limits

The property you purchase with FHA financing must meet specific condition standards and fall within county-based loan limits that vary by location. These requirements protect both you and the lender by ensuring the home provides adequate security for the loan amount. Unlike conventional loans that may approve properties needing significant repairs, FHA underwriters will reject your application if the property fails inspection standards, regardless of how strong your financial profile looks on paper.

FHA appraisal standards and requirements

You must hire an FHA-approved appraiser from your lender's roster to evaluate the property's market value and condition before closing. The appraiser checks for safety hazards, structural integrity, and code compliance using standards stricter than typical home inspections. Properties with peeling paint, damaged roofing, faulty electrical systems, or foundation issues will fail appraisal until the seller completes repairs, and you cannot waive these requirements to expedite closing like you might with conventional financing.

FHA appraisals protect buyers from purchasing homes with hidden defects that could compromise safety or reduce property value below the loan amount.

Property condition minimums

Your property needs a functioning heating system, safe electrical wiring, adequate roofing, and accessibility to all areas the appraiser must inspect. Homes missing handrails on stairs, showing evidence of water damage, or lacking proper ventilation in bathrooms will receive repair requirements you must address before loan approval. Understanding how to qualify for FHA loan approval means either selecting move-in ready properties or negotiating repair credits with sellers who will fix issues before closing, as you cannot close with outstanding appraisal conditions.

County loan limits by property location

FHA caps your loan amount based on median home values in your specific county, with limits ranging from $498,257 in low-cost areas to $1,149,825 in high-cost markets for single-family homes in 2026. You can purchase properties above these limits, but you'll need to cover the difference with a larger down payment that conventional financing might handle more efficiently. Lenders provide exact limits for your target area during pre-approval, and these caps increase for multi-unit properties with two to four units you plan to owner-occupy.

How to apply and avoid common disqualifiers

You start the FHA application process by contacting an approved FHA lender who will pre-approve you based on your credit, income, and down payment capacity. Pre-approval gives you a clear budget and shows sellers you're a serious buyer with financing already secured. The actual application requires pay stubs, tax returns, bank statements, and employment verification, which your lender reviews to confirm you meet every requirement for approval before ordering the appraisal.

The FHA application process step by step

Your lender submits your complete application to underwriting within 48-72 hours after you provide all required documentation. Underwriters verify your employment, review your credit report for new inquiries or debts, and calculate your DTI ratio using your most recent pay information. You'll receive a conditional approval listing any outstanding requirements like additional documentation or explanations for specific credit items, which you must satisfy before final approval.

Once you satisfy all conditions, the lender orders your FHA appraisal and schedules closing after the property passes inspection. Understanding how to qualify for FHA loan approval means staying responsive during this process, as delayed documentation or new debts can restart underwriting review and push back your closing date by weeks.

Common disqualifiers that stop approval

New credit applications during underwriting represent the most frequent self-inflicted denial among approved borrowers. Opening a car loan, furniture financing, or new credit cards between pre-approval and closing changes your DTI ratio and credit score, which triggers re-evaluation of your entire application. Lenders must reverify your credit immediately before closing, and any new obligations that push you over DTI limits will cancel your approval regardless of how much work you've already completed.

Protect your approval by avoiding all new credit, major purchases, or job changes between application and closing, as any financial change requires complete underwriting review.

Recent bankruptcies or foreclosures create mandatory waiting periods you cannot waive regardless of your current financial strength. Chapter 7 bankruptcy requires a two-year wait from discharge date, while Chapter 13 needs one year of payments with court approval for early FHA financing. Foreclosures mandate a three-year waiting period, and you must demonstrate the financial hardship that caused the foreclosure rather than strategic default. These timelines protect the program from repeat defaults by ensuring you've rebuilt financial stability before qualifying again.

Next steps for getting an FHA loan

You now understand how to qualify for FHA loan approval, from the 580 credit score minimum and 3.5% down payment to the DTI calculations and property standards that determine your eligibility. These requirements create a clear roadmap for homeownership, even if your financial profile doesn't fit conventional lending standards.

Start by pulling your credit reports and calculating your current DTI ratio to identify any gaps between your current position and FHA minimums. Contact an FHA-approved lender for pre-approval once you meet the basic thresholds, as this gives you a firm budget and timeline for purchasing. Your pre-approval expires after 90 days, so time your application to align with your actual house hunting schedule rather than applying months before you're ready to make offers.

If you need guidance navigating FHA qualification requirements or want to explore specialized programs for ITIN holders and non-traditional income sources, contact our team to discuss your specific situation and develop an approval strategy.