FHA Bankruptcy Waiting Period: Chapter 7 vs Chapter 13

Filing for bankruptcy can feel like closing the door on homeownership, but that's rarely the full picture. The FHA bankruptcy waiting period exists specifically to give borrowers a second chance, and understanding exactly how long you need to wait is the first step toward getting back on track. Whether you filed Chapter 7 or Chapter 13, the timeline to qualify for an FHA loan differs significantly, and knowing these distinctions can save you months of frustration.

The good news? FHA loans remain one of the most accessible paths to homeownership after financial hardship. With over 25 years of experience as a mortgage broker and senior loan officer, I've helped countless clients navigate this exact situation, guiding them from discharge date to closing table. The waiting periods aren't arbitrary; they're designed to demonstrate financial recovery and responsible credit behavior, both of which lenders need to see before approving your application.

This guide breaks down the specific waiting periods for Chapter 7 and Chapter 13 bankruptcies, explains what exceptions exist, and outlines exactly what you need to do during the waiting period to strengthen your mortgage application. If you're wondering when you can realistically buy a home again, you're in the right place.

Why the FHA bankruptcy waiting period matters

The FHA bankruptcy waiting period isn't just a bureaucratic hurdle; it serves as proof that you've rebuilt your financial foundation. Lenders need to see that you can manage credit responsibly after a major financial setback, and the waiting period gives you time to demonstrate this through consistent payment history. Without this mandatory timeline, borrowers who haven't truly recovered might take on mortgage debt they can't sustain, leading to another foreclosure and deeper financial trouble.

Protection for both borrower and lender

You might view the waiting period as punitive, but it actually protects you from making a premature decision. Bankruptcy discharge doesn't erase the underlying financial habits or circumstances that led to the filing in the first place. The mandatory wait allows you to stabilize your income, address any lingering debt issues, and build an emergency fund before taking on a mortgage payment. Lenders benefit too because they reduce their risk of funding loans that might default within the first few years, which is exactly what happened during the housing crisis when qualification standards were too lenient.

The waiting period creates breathing room to fix what went wrong, not just to check boxes on a loan application.

Impact on your financial planning

Understanding the exact waiting period for your bankruptcy type lets you create a realistic timeline for homeownership rather than guessing or getting your hopes up too early. If you filed Chapter 7, you're looking at a two-year minimum from discharge before FHA approval, which means you can focus your energy during those 24 months on rebuilding credit and saving for a down payment. Chapter 13 filers who make 12 months of on-time payments might qualify earlier, which changes your strategic approach to financial recovery entirely. Knowing these timelines prevents you from wasting time applying too soon or, conversely, waiting longer than necessary because you assumed you couldn't qualify yet.

The cost of waiting versus rushing

Applying for an FHA loan before you've completed the full waiting period guarantees rejection, and that denial stays on your credit report. Each hard inquiry from a mortgage application can drop your credit score by several points, and multiple denials signal to future lenders that you're either desperate or uninformed about qualification requirements. The smart play is to wait until you clearly meet every requirement, then apply with confidence. During the waiting period, you can also improve your credit score significantly, which translates directly into lower interest rates. A borrower with a 640 credit score might pay 1.5% more in interest than someone with a 720 score, which means thousands of dollars over the life of a 30-year mortgage.

Patience during the FHA bankruptcy waiting period isn't about sitting idle. You should actively rebuild credit by opening a secured credit card, making all payments on time, and keeping credit utilization below 30%. Each month you demonstrate responsible financial behavior strengthens your eventual mortgage application and proves to underwriters that you've genuinely recovered from the bankruptcy. The waiting period matters because it separates applicants who've truly changed their financial habits from those who are simply trying to rush back into homeownership without addressing the root causes of their bankruptcy.

The dates that start the clock

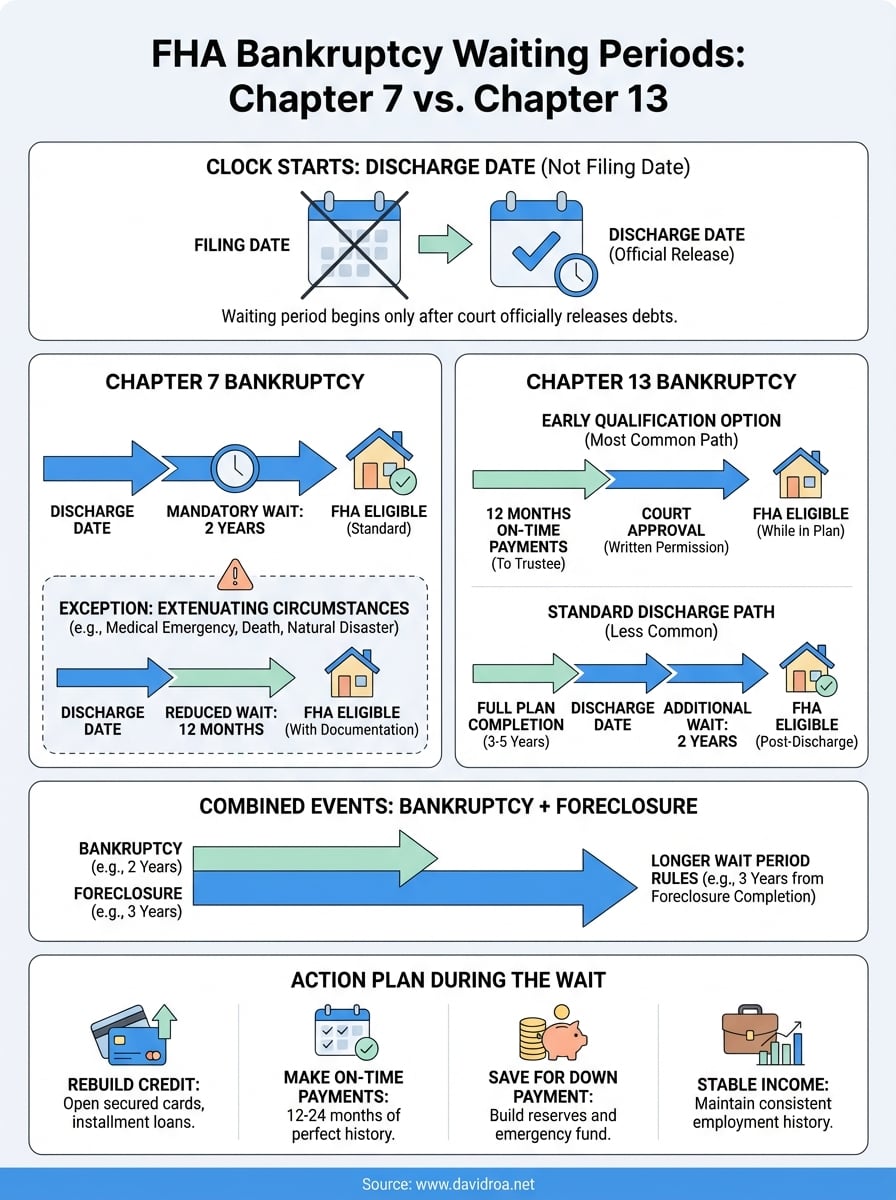

The FHA bankruptcy waiting period doesn't start when you file for bankruptcy; it starts from your discharge date or dismissal date, depending on the bankruptcy chapter. This distinction confuses many applicants because the gap between filing and discharge can span several months or even years, especially in Chapter 13 cases. You cannot begin counting down the waiting period until the bankruptcy court officially releases you from your debts, which means any time spent in active bankruptcy proceedings doesn't count toward your eligibility timeline.

Discharge date versus filing date

Your bankruptcy filing date only marks when you submitted paperwork to the court, not when your debts were legally discharged. For Chapter 7, discharge typically occurs 90 to 120 days after filing, but for Chapter 13, discharge happens only after you complete your entire repayment plan, which usually takes three to five years. The fha bankruptcy waiting period begins from discharge in most cases, though Chapter 13 has a special exception that allows you to qualify after 12 months of on-time plan payments. Confusing these dates can lead you to apply for a mortgage months or years too early, resulting in automatic denial and wasted application fees.

The discharge date is the only date that matters for calculating your FHA eligibility, not when you first filed.

Finding your official discharge date

You can locate your exact discharge date by reviewing the discharge order sent by the bankruptcy court, which is a legal document that formally releases you from debt obligations. If you've lost this paperwork, contact your bankruptcy attorney or request a copy directly from the court clerk's office where your case was filed. The discharge date appears clearly on the order, typically near the top of the document, and you should keep this paperwork in a safe place because mortgage underwriters will request it during the loan application process. Some bankruptcy trustees also provide online access to case documents, allowing you to download your discharge order immediately. You need this exact date to calculate when you'll become eligible for FHA financing, so tracking down the official documentation should be your first priority when planning your path back to homeownership.

Chapter 7 FHA waiting period and requirements

Chapter 7 bankruptcy involves complete liquidation of non-exempt assets to discharge your unsecured debts, and the FHA requires a minimum two-year waiting period from your discharge date before you can qualify for financing. This timeline applies regardless of the circumstances that led to your bankruptcy filing, though exceptions exist for situations involving extenuating circumstances beyond your control. The two-year period gives you enough time to rebuild credit while preventing borrowers who haven't truly stabilized from taking on mortgage debt prematurely.

The two-year mandatory timeline

You must wait exactly 24 months from your Chapter 7 discharge date before an FHA lender can approve your mortgage application. This waiting period is non-negotiable in standard cases, meaning you cannot apply at 20 months and hope for leniency. During these two years, you need to demonstrate that you've reestablished your credit profile by maintaining at least two active tradelines with perfect payment history. Most successful applicants open a secured credit card and an installment loan during this period, making every payment on time without exception.

The two-year clock starts ticking the day the bankruptcy court issues your discharge order, not when you filed or when your 341 meeting occurred.

Credit requirements after discharge

FHA guidelines require you to show responsible credit management throughout the entire waiting period, which means more than just avoiding late payments. You need to maintain credit accounts in good standing, keep your credit utilization below 30%, and avoid any new collections or charge-offs. Lenders will review your full credit report from discharge forward, looking for patterns that indicate financial recovery rather than continued instability. A credit score of 580 gets you the minimum down payment option of 3.5%, but scores between 500 and 579 require 10% down and significantly limit your lender options.

Income and employment stability

Your income situation during the two-year period matters almost as much as your credit behavior. FHA underwriters want to see stable employment history, ideally with the same employer throughout the waiting period or at least within the same field. You'll need to provide two years of W-2s, recent pay stubs, and potentially tax returns to verify your income capacity. Self-employed borrowers face additional scrutiny because lenders need to see consistent business income documented through tax returns, which becomes challenging if you launched your business shortly after bankruptcy discharge.

Chapter 13 FHA waiting period and requirements

Chapter 13 bankruptcy operates differently than Chapter 7 because it involves a court-approved repayment plan lasting three to five years rather than immediate debt discharge. The FHA bankruptcy waiting period for Chapter 13 offers a unique advantage: you can qualify for a mortgage after just 12 months of on-time payments to your bankruptcy trustee, provided you meet specific requirements and obtain court approval. This early qualification option makes Chapter 13 significantly more attractive for borrowers who need to purchase a home before their full repayment plan ends.

The 12-month early qualification option

You can apply for FHA financing after making 12 consecutive monthly payments to your Chapter 13 trustee without any late or missed payments. This timeline represents the absolute minimum waiting period for any bankruptcy type, but you cannot simply wait 12 months and apply on your own authority. You must obtain written permission from the bankruptcy court before your lender can process your mortgage application, which requires filing a motion explaining why you need to take on new debt while still in active bankruptcy proceedings.

The 12-month route offers the fastest path to homeownership after bankruptcy, but court approval is never guaranteed.

Your bankruptcy attorney must file the motion requesting permission to incur mortgage debt, and the trustee will review your current financial situation to determine whether adding a mortgage payment jeopardizes your ability to complete the repayment plan. The court typically approves these requests when you can demonstrate stable income, a legitimate need for housing, and that your proposed mortgage payment fits comfortably within your budget alongside your existing trustee payments. Some judges approve these motions routinely while others scrutinize them heavily, so your attorney's experience with local bankruptcy court procedures matters significantly.

Documentation and payment history requirements

Lenders will request complete payment records from your bankruptcy trustee showing every payment made during the 12-month period, along with confirmation that you remain current on your plan. You need to provide court documents proving your bankruptcy remains active and in good standing, plus the signed court order granting permission to incur mortgage debt. Your credit report must show zero late payments on any accounts during the 12-month period, including your trustee payments, any accounts not included in bankruptcy, and any new credit you've obtained since filing.

Alternative full discharge timeline

If you choose not to pursue early qualification or cannot obtain court approval, you follow the standard two-year waiting period from your Chapter 13 discharge date. This path requires completing your entire repayment plan, receiving your discharge order, and then waiting 24 additional months before applying for FHA financing. Most borrowers find this timeline less practical because Chapter 13 plans already span multiple years, making the total time from filing to mortgage approval stretch to five to seven years in many cases.

When you can shorten the wait

The FHA bankruptcy waiting period can be reduced to just 12 months from your Chapter 7 discharge date if you experienced extenuating circumstances that caused your bankruptcy filing. This exception recognizes that some bankruptcies result from events completely outside your control rather than irresponsible financial management. You cannot use this shortened timeline for poor spending habits, overleveraging on credit cards, or general financial mismanagement, but life-altering situations like medical emergencies or sudden unemployment may qualify you for earlier approval.

What qualifies as extenuating circumstances

FHA defines extenuating circumstances as events that were beyond your control and resulted in substantial loss of income or increased expenses. The death of a primary wage earner in your household qualifies, as does a catastrophic illness that generated massive medical bills while simultaneously preventing you from working. Job loss due to company-wide layoffs or business closure meets the definition, but getting fired for performance issues or quitting voluntarily does not. Natural disasters that destroyed your home or business also qualify if you can document the direct financial impact. Your circumstances must be both unexpected and unavoidable, meaning you took reasonable steps to prevent financial collapse but still ended up filing bankruptcy.

The key distinction is whether a reasonable person in your situation could have avoided bankruptcy through better financial planning.

Documentation requirements for reduced timeline

You need extensive documentation proving your extenuating circumstances directly caused your bankruptcy filing. Medical documentation includes hospital bills, treatment records, and doctor's statements explaining your inability to work during illness or injury. Employment-related circumstances require termination letters showing you lost your job through no fault of your own, along with unemployment benefit records and evidence of your job search efforts. You must also demonstrate that you've since recovered from the circumstances, typically through stable employment for at least 12 months after your bankruptcy discharge. Letters explaining your situation should come from you, your bankruptcy attorney, and potentially third parties like former employers or medical professionals who can corroborate your story. Underwriters scrutinize these exceptions carefully because approving too many early applications increases their default risk significantly.

Other events that can extend your timeline

Bankruptcy represents just one type of derogatory credit event that affects your FHA eligibility timeline, and combining bankruptcy with foreclosure creates a more complicated situation. If you lost your home to foreclosure either before or during your bankruptcy proceedings, you face separate waiting periods that run concurrently rather than sequentially. The FHA bankruptcy waiting period doesn't simply replace other waiting periods; instead, you must satisfy whichever timeline proves longer before you can qualify for financing.

Foreclosure combined with bankruptcy

Completing a foreclosure triggers its own three-year waiting period from the completion date, which typically extends well beyond the two-year bankruptcy requirement. You cannot start counting this timeline until the foreclosure fully concludes, meaning the property deed transfers back to the lender and all legal proceedings close. If your bankruptcy discharge occurred in January 2024 but your foreclosure didn't complete until March 2024, you must wait until March 2027 to apply for FHA financing because the foreclosure timeline supersedes the bankruptcy requirement. Deed-in-lieu transactions, where you voluntarily transfer property ownership to avoid formal foreclosure, follow the same three-year waiting period despite being technically different from foreclosure proceedings.

When bankruptcy and foreclosure overlap, the longer waiting period always controls your eligibility timeline.

Short sales and pre-foreclosure actions

Short sale completion requires waiting three years from the closing date before you qualify for FHA financing, matching the foreclosure timeline exactly. This waiting period applies even if you obtained full lender approval for the short sale and owed no deficiency balance afterward. Pre-foreclosure sales where you sold your property under duress to avoid foreclosure also trigger the three-year requirement because FHA views these transactions as evidence of mortgage default. You cannot shorten these timelines through extenuating circumstances exceptions unless the circumstances that caused both your bankruptcy and property loss meet FHA's strict criteria. Borrowers who filed bankruptcy but never owned property or lost property face only the standard fha bankruptcy waiting period without additional complications from real estate-related events.

Multiple derogatory events

Accumulating several credit problems during the same period creates overlapping waiting periods that you must satisfy individually. If you had a foreclosure in 2023, filed bankruptcy in 2024, and had a short sale on another property in 2025, you need to wait three years from each event's completion date before FHA approval becomes possible. Underwriters evaluate your entire credit history comprehensively rather than focusing solely on bankruptcy, which means any significant negative event extends your path back to homeownership.

How to get approved after bankruptcy

Getting approved for an FHA loan after bankruptcy requires more than simply waiting out the mandatory timeline. You need to actively rebuild your creditworthiness throughout the entire fha bankruptcy waiting period by establishing positive payment patterns and demonstrating financial stability. Lenders want evidence that you've addressed whatever caused your bankruptcy in the first place, not just proof that enough time has passed since your discharge date.

Rebuild your credit systematically

You should open at least two new credit accounts within three to six months after your bankruptcy discharge to begin rebuilding your credit profile. Secured credit cards work best for this purpose because approval is nearly guaranteed when you provide a cash deposit, and responsible use reports to all three credit bureaus just like traditional credit cards. Apply for a small installment loan through a credit union or online lender to diversify your credit mix, making monthly payments that demonstrate your ability to manage different types of debt responsibly. Keep your credit utilization below 30% on revolving accounts and pay every bill on time without exception. A single 30-day late payment during your waiting period can delay your mortgage approval by months or trigger outright denial.

Your credit behavior during the waiting period matters more to underwriters than your credit score before bankruptcy.

Maintain perfect payment history

Every payment you make after bankruptcy discharge appears on your credit report and influences your mortgage application outcome. You need 12 to 24 months of flawless payment history across all accounts, including utilities, rent, car payments, and any debts not discharged in bankruptcy. Set up automatic payments from your checking account to eliminate the risk of forgetting due dates, but monitor your accounts weekly to catch any processing errors before they become late payments. Underwriters scrutinize your post-bankruptcy behavior intensely because they're evaluating whether you've genuinely changed your financial habits and decision-making patterns.

Document your financial recovery

Start gathering documentation six months before you plan to apply for your mortgage to ensure you have everything underwriters will request. You need your bankruptcy discharge papers, two years of tax returns, recent pay stubs covering 30 days, and bank statements showing at least two months of reserves. Written explanations of your bankruptcy circumstances help underwriters understand your situation, particularly if extenuating circumstances caused your filing. Pull your credit reports from all three bureaus to identify and dispute any errors that might damage your application or reduce your credit score unnecessarily.

Next steps

The fha bankruptcy waiting period doesn't have to derail your homeownership plans if you approach it strategically. Start by marking your exact discharge date on your calendar and calculating your eligibility timeline based on your bankruptcy chapter and any additional credit events like foreclosure. You should immediately begin rebuilding credit through secured credit cards and small installment loans, making every payment on time while monitoring your credit reports for errors.

Your focus during the waiting period should center on creating stable employment history, building emergency savings, and documenting your financial recovery. Gathering your bankruptcy discharge papers, tax returns, and payment records now prevents scrambling when you're ready to apply. Understanding these requirements puts you months ahead of borrowers who wait until the last minute to organize their documentation.

Ready to explore your mortgage options after bankruptcy? Connect with an experienced loan officer who understands the FHA bankruptcy waiting period and can create a personalized timeline for your situation. Professional guidance ensures you apply at exactly the right moment with the strongest possible application.