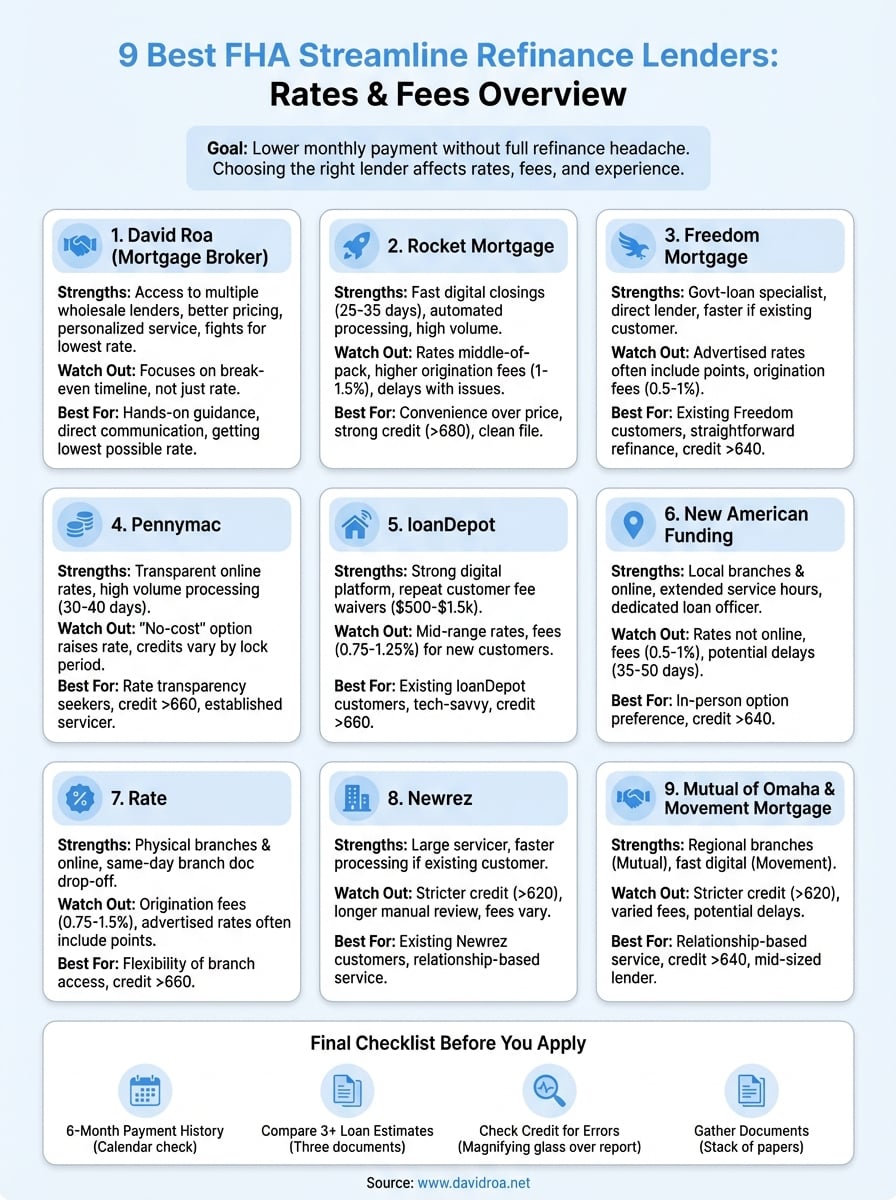

9 Best FHA Streamline Refinance Lenders: Rates & Fees

If you already have an FHA loan and want to lower your monthly payment without the headache of a full refinance, you're in the right place. The FHA streamline refinance lenders you choose can make a significant difference in your rates, fees, and overall experience, so picking the right one matters more than you might think. With over 25 years in the mortgage industry and more than $150 million funded, I've seen firsthand how the wrong lender can cost borrowers thousands.

This guide breaks down nine top lenders offering FHA streamline refinances in 2026, comparing their rates, fees, and what makes each one stand out. Whether you're looking for the lowest closing costs or the fastest turnaround time, you'll find options that fit your situation. Let's get into the details so you can refinance with confidence and start saving.

1. David Roa

Working with a dedicated mortgage broker like me gives you access to multiple FHA streamline refinance lenders instead of being locked into one bank's rates and fees. I've closed over $150 million in loans during my 25 years in the business, and that experience means I know which lenders offer the best terms for your specific situation. You get personalized service, direct communication, and someone who fights to get you the lowest rate possible.

What you get when you work with a mortgage broker

A mortgage broker acts as your advocate, shopping your loan across multiple wholesale lenders that typically offer better pricing than you'd find going direct. You avoid the runaround of calling five different banks yourself, and I handle the paperwork, follow-ups, and underwriting process from start to finish. Most importantly, brokers have access to lender overlays and pricing sheets that help us match you with the best fit for your credit profile and equity position.

You also get flexibility that single-lender operations can't match. If one lender hits a snag with your appraisal or documentation, I can pivot your file to another lender without starting from scratch. This saves you weeks and keeps your refinance on track even when unexpected issues pop up.

How to compare streamline offers across lenders

Start by looking at the annual percentage rate (APR), not just the interest rate. The APR includes lender fees, which can vary wildly between fha streamline refinance lenders even when their rates look identical. Ask every lender for a loan estimate within three days of applying so you can compare origination charges, discount points, and third-party costs side by side.

The lowest advertised rate almost always comes with higher upfront fees or points, so focus on your break-even timeline instead of just the monthly payment.

Pay attention to credit score requirements and whether the lender charges for rate locks beyond 30 days. Some lenders will waive origination fees entirely on streamline refinances, while others bake those costs into a slightly higher rate. You need to calculate which approach saves you more money over the time you plan to stay in the home.

Best fit borrower profile

You're a strong fit if you want hands-on guidance and access to wholesale pricing without the hassle of shopping lenders yourself. My clients typically value direct communication and appreciate working with someone who owns a business and invests in real estate, so I understand both the numbers and the real-world impact of your monthly payment. If you're in the Chicago area or prefer working with a broker who answers your calls personally, this option makes the most sense for your FHA streamline refinance.

2. Rocket Mortgage

Rocket Mortgage built its reputation on fast digital closings and automated processing, which translates well to FHA streamline refinances where minimal documentation is required. You can complete most of the application online without phone calls or branch visits, and their system updates you through each stage of underwriting. The company handles high volume and typically closes streamline refinances in 25 to 35 days, though some borrowers report longer timelines when appraisals or title issues arise.

Streamline refinance experience and speed

You'll work through their online platform for most tasks, uploading documents and tracking your loan status without waiting for callbacks. Rocket assigns you a mortgage banker who handles questions via phone or chat, though you may interact with different team members during closing. The company invests heavily in technology, so your application moves faster through automated underwriting compared to smaller fha streamline refinance lenders that rely on manual reviews.

Their speed advantage shows up most clearly when your credit and payment history are clean. Borrowers with recent late payments or disputed accounts often face delays as the file moves to manual underwriting, which slows the process considerably.

What to watch for on rates and lender fees

Rocket's rates sit near the middle of the pack rather than at the low end, and their origination fees typically run higher than broker or credit union options. You'll see charges for processing and underwriting that add up to 1% to 1.5% of your loan amount. Request a loan estimate early so you can compare their all-in costs against other lenders offering the same rate without points.

Advertised rates often require purchasing discount points, so confirm whether the quote you're seeing reflects zero-point pricing or includes upfront costs.

Best fit borrower profile

You're a good match if you value convenience over price and prefer managing your refinance through an app rather than phone conversations. Rocket works best for borrowers with strong credit scores above 680 and straightforward income documentation who don't need hand-holding through the process.

3. Freedom Mortgage

Freedom Mortgage specializes in government-backed loans and handles a high volume of FHA products, which means their underwriters see streamline refinances daily. The company operates as a direct lender rather than a broker, so you work with their in-house team from application through closing. They maintain relationships with many mortgage servicers and often refinance loans they already service, which can speed up documentation since they hold your payment history internally.

FHA streamline focus and process basics

You'll complete your application either online or over the phone with a loan officer who specializes in FHA products. Freedom's underwriting team processes streamline refinances in 30 to 45 days on average, though timelines stretch when third-party appraisals or title work hit delays. Their servicer relationships mean you might skip certain verification steps if they already service your existing FHA loan, cutting a week or more off standard processing times.

The company uses automated underwriting systems for most streamline refinances, which works well if your credit profile is clean. Manual review becomes necessary when credit disputes or payment gaps appear on your report.

What to watch for on rate quoting and add-on costs

Freedom's advertised rates often include discount points that aren't clearly disclosed upfront, so you need to ask specifically for zero-point pricing to compare against other fha streamline refinance lenders. Their origination fees run between 0.5% and 1% of the loan amount, with additional charges for processing and underwriting that can add several hundred dollars to your closing costs.

Always request an itemized fee breakdown within 48 hours of rate shopping so you catch hidden charges before you commit to an application.

Best fit borrower profile

You're a strong candidate if Freedom already services your current FHA loan and you want a straightforward refinance without shopping multiple lenders. Their process works best for borrowers with credit scores above 640 who don't need extensive guidance or rate negotiation.

4. Pennymac

Pennymac operates as both a servicer and direct lender, handling billions in FHA loans annually and offering streamline refinances through their retail and correspondent channels. You'll find their rates posted online with more transparency than most competitors, though actual pricing depends on your credit score and loan-to-value ratio. The company processes high volume and maintains dedicated FHA underwriting teams that move files through approval in 30 to 40 days on average.

Rate visibility and streamline options

You can check Pennymac's current rates online without submitting an application, which gives you a baseline for comparison against other fha streamline refinance lenders before committing your time. Their platform shows rates broken down by credit score tiers, so you know whether the advertised rate applies to your profile. Pennymac offers both standard streamline and credit-qualifying options if you want to cash out equity or roll closing costs into your new loan balance.

What to watch for on no-cost offers and credits

Pennymac advertises no-closing-cost refinances that eliminate upfront fees by raising your interest rate slightly, typically by 0.25% to 0.375%. Calculate your break-even point carefully because the higher rate costs you thousands over the loan term even though you save money at closing. Their lender credits vary based on rate lock periods, with shorter locks earning better pricing than extended 60-day or 90-day commitments.

A no-cost refinance makes sense only if you plan to move or refinance again within three to five years, otherwise you pay more in total interest than the closing costs you avoided.

Best fit borrower profile

You're a strong match if you want rate transparency upfront and prefer working with an established servicer that handles government loans daily. Pennymac works best for borrowers with credit scores above 660 who value convenience over the absolute lowest rate available in the market.

5. loanDepot

loanDepot operates as a direct lender with a strong digital platform designed for borrowers who want to manage their refinance through an app or website. The company processes thousands of FHA streamline refinances annually and offers repeat customer incentives that reduce fees if you've worked with them before. Their technology stack mirrors what you'll find at Rocket Mortgage, with automated updates and document upload features that keep you informed without requiring constant phone contact.

Digital process and repeat-refi perks

You'll complete your application through their online portal and track progress through automated status updates at each underwriting stage. loanDepot assigns you a loan officer who handles questions through their messaging system or by phone, and most streamline refinances close in 30 to 45 days. The company offers loyalty discounts that waive origination fees entirely if you're refinancing a loan they already service, which saves you between $500 and $1,500 compared to new customers.

Their mobile app lets you upload documents and review loan estimates from your phone, making the process faster than lenders that require email submissions or fax documents.

What to watch for on lender fees and pricing

loanDepot's rates typically fall in the mid-range compared to other fha streamline refinance lenders, and their origination fees run between 0.75% and 1.25% of your loan amount unless you qualify for repeat customer waivers. Processing and underwriting charges add several hundred dollars to closing costs, so request a detailed loan estimate within three days of applying. Their advertised rates often assume excellent credit scores above 700, with pricing adjustments for lower tiers that aren't always clear upfront.

Compare loanDepot's total closing costs against at least two other lenders before locking your rate, since their convenience premium may cost you thousands over cheaper alternatives.

Best fit borrower profile

You're a strong candidate if you already have a loan with loanDepot and want to take advantage of their loyalty fee waivers, or if you prefer managing your refinance through a digital platform rather than phone calls. Their process works best for tech-comfortable borrowers with credit scores above 660 who value convenience over securing the absolute lowest rate available.

6. New American Funding

New American Funding operates as a direct lender with both retail branches and online services, giving you flexibility in how you manage your FHA streamline refinance. The company handles government-backed loans across all 50 states and maintains local loan officers who work with borrowers through phone, email, or in-person meetings depending on your branch location. Their underwriting teams process streamline refinances in 35 to 50 days on average, with timelines varying based on documentation completeness and third-party vendor speed.

Support options and availability

You can choose between working with a local loan officer at one of their branches or completing your application entirely online through their digital platform. Branch-based officers provide more hands-on guidance and can meet face-to-face if you prefer discussing your refinance in person, while their online channel mirrors the self-service experience you'll find at larger digital lenders. New American Funding assigns you a dedicated loan officer regardless of which path you choose, and that person handles your file from application through closing.

Their customer service team operates extended hours including evenings and weekends, which helps if you work a standard schedule and can't call during business hours.

What to watch for on rate transparency and timelines

New American Funding doesn't post rates online without requiring contact information, so you'll need to speak with a loan officer before seeing actual pricing. Their rates fall in the mid-range compared to other fha streamline refinance lenders, and origination fees typically run between 0.5% and 1% of your loan amount. Processing times stretch longer than advertised when appraisals or title work hit delays, so build extra time into your planning if you're refinancing with a tight deadline.

Always confirm rate lock periods in writing since verbal agreements won't protect you if rates rise during underwriting delays.

Best fit borrower profile

You're a strong match if you want the option of in-person meetings with a local loan officer while still having access to digital tools for document uploads and status tracking. Their service works best for borrowers with credit scores above 640 who value relationship-based lending over purely price-driven competition.

7. Rate

Rate operates as a retail mortgage lender with physical branch locations and an online application platform, giving you the choice between face-to-face service and digital convenience. The company handles FHA streamline refinances across multiple states and maintains loan officers who work through their branch network or remotely depending on your location. Their underwriting process typically takes 35 to 45 days from application to closing, with standard timelines extending when documentation issues or third-party delays occur.

Branch access vs online streamline workflow

You can visit a Rate branch location to meet with a loan officer in person if you prefer discussing your refinance face-to-face, or handle everything through their online platform without stepping into an office. Branch-based officers provide personalized guidance through the FHA streamline process, answering questions and reviewing documents during scheduled appointments. Their digital workflow mirrors other online lenders with document uploads, automated status updates, and communication through email or phone rather than in-person meetings.

Local branches give you access to same-day document drop-offs and immediate answers when questions arise, while the online channel offers flexibility to work on your refinance outside traditional business hours.

What to watch for on origination charges and points

Rate's origination fees typically range from 0.75% to 1.5% of your loan amount, with additional processing and underwriting charges that add several hundred dollars to closing costs. Their advertised rates often include discount points that reduce your interest rate but increase upfront costs by thousands of dollars. Request zero-point pricing from your loan officer so you can compare Rate's costs against other fha streamline refinance lenders offering similar rates without purchasing points.

Always ask for an itemized breakdown of all lender fees within 24 hours of receiving a rate quote so you catch pricing adjustments before committing to an application.

Best fit borrower profile

You're a strong candidate if you want the flexibility of branch access while maintaining the option to handle parts of your refinance online. Rate works best for borrowers with credit scores above 660 who appreciate relationship-based lending but don't necessarily need the absolute lowest rates in the market.

8. Newrez, Mutual of Omaha Mortgage, and Movement Mortgage

These three lenders handle FHA streamline refinances with regional strengths and specific borrower profiles that differentiate them from national competitors. Newrez operates as a large servicer with correspondent lending channels, Mutual of Omaha brings decades of insurance-backed lending experience, and Movement Mortgage focuses on fast closings through their digital platform. Each offers competitive rates in specific scenarios, though you'll find less brand recognition compared to Rocket or Pennymac.

When these lenders make sense for streamline refinances

You benefit most from Newrez if they already service your existing FHA loan since their internal documentation access speeds up processing by one to two weeks. Mutual of Omaha works well when you want a traditional lender with physical branch access across the Midwest and South, offering face-to-face consultations that larger fha streamline refinance lenders don't provide. Movement Mortgage delivers faster digital closings than most regional competitors, typically completing streamline refinances in 25 to 35 days when your credit and payment history are clean.

What to watch for on credit overlays and underwriting speed

These lenders impose stricter credit score minimums than FHA's baseline requirements, often requiring 620 or higher when the program technically allows scores down to 580. Their underwriting timelines stretch longer than advertised when manual review becomes necessary, adding 10 to 15 days to standard processing. Origination fees vary widely between these three, so request detailed loan estimates within 48 hours of applying to compare their all-in costs against larger competitors.

Regional lenders often compensate for higher overhead with slightly elevated fees, so verify whether their rate advantage justifies any additional closing costs.

Best fit borrower profile

You're a strong candidate if you value relationship-based service over purely digital convenience or already have an existing loan with one of these servicers. Their approach works best for borrowers with credit scores above 640 who prefer working with mid-sized lenders that offer more personalized attention than national brands.

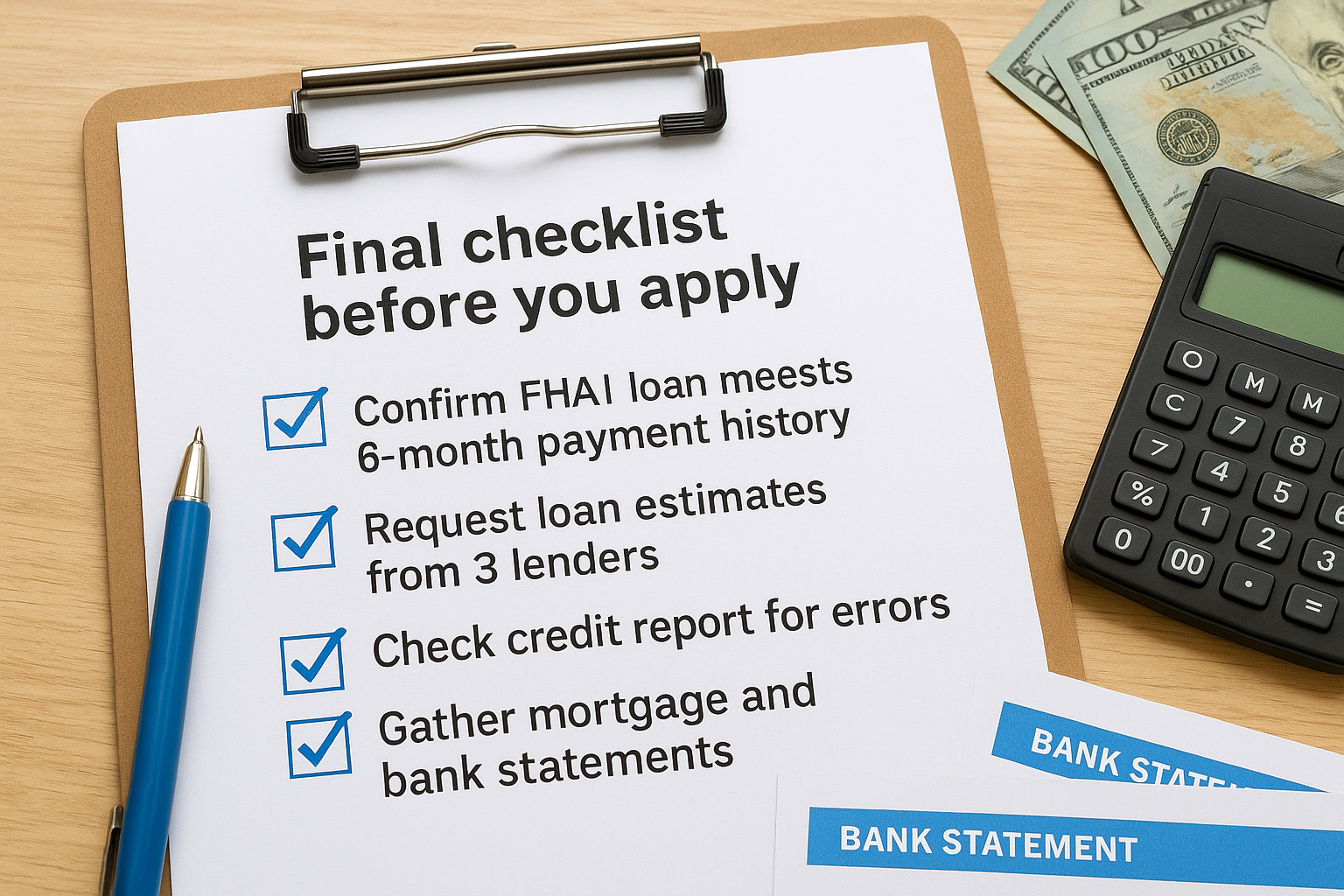

Final checklist before you apply

You now have a clear picture of which fha streamline refinance lenders offer the best combination of rates, fees, and service for your situation. Before you submit an application, confirm your current FHA loan meets the six-month payment history requirement and verify that refinancing will actually lower your monthly payment or annual costs. Request loan estimates from at least three lenders within the same 48-hour window so rate comparisons stay accurate, and review each estimate for hidden origination fees or discount points that inflate closing costs.

Check your credit report for errors that could delay underwriting, and gather your most recent mortgage statement along with two months of bank statements to speed up documentation. The right combination of low rates and responsive service makes your refinance faster and cheaper, but only if you start with accurate information about your current loan and financial profile.

Ready to move forward? Work with me directly to access multiple wholesale lenders and secure the best streamline refinance rate available for your situation.