FHA Streamline Refinance Requirements: Eligibility & Rules

If you already have an FHA loan and want a lower rate or payment, the FHA Streamline Refinance is one of the fastest paths to get there. But before you start the process, you need to know whether you actually qualify. The FHA streamline refinance requirements set specific rules around timing, payment history, and the benefit you'll receive from refinancing, and missing even one can stop your application cold. Understanding these eligibility criteria upfront saves you time, money, and frustration.

The Streamline program was designed by HUD to be simpler than a standard refinance. There's typically no appraisal required, and documentation is lighter than what you'd need for a full FHA refinance. But "streamlined" doesn't mean automatic. You still need to meet waiting periods, demonstrate a net tangible benefit, and stay current on your existing mortgage. The specific rules have also been updated over the years, so what applied when you first got your loan may not reflect current guidelines.

With over 25 years in mortgage lending and more than $150 million funded, I've helped hundreds of borrowers navigate FHA refinances, including the Streamline program. At David Roa, we handle FHA products daily and know exactly where borrowers run into issues with eligibility. This article breaks down every requirement you need to meet, from minimum seasoning periods to credit and income considerations, so you can determine whether the FHA Streamline Refinance is the right move for you.

Why FHA streamline requirements matter

The FHA Streamline Refinance sounds straightforward: swap your current FHA loan for a new one with a lower rate and skip the appraisal. But HUD built specific eligibility rules into the program for a reason, and those rules directly affect whether your application moves forward or lands in a denial. Knowing the fha streamline refinance requirements before you start the process means you avoid wasted time, unnecessary lender fees, and the frustration of a last-minute rejection after weeks of paperwork.

Why HUD set these rules in the first place

HUD created the Streamline program to reduce friction for existing FHA borrowers, but it also needed guardrails to prevent abuse of the system. Without requirements around payment history and loan seasoning, borrowers could refinance repeatedly without any real savings, and lenders could collect origination fees each time without delivering any value. The rules ensure that every refinance produces a measurable financial benefit for you and protects the FHA insurance fund from taking on unnecessary risk.

The net tangible benefit rule exists specifically to make sure you end up in a better financial position after the refinance, not just in a new loan with a new fee structure.

These rules also reflect HUD's broader responsibility to the borrowers who rely on FHA loans, a pool that includes first-time buyers, lower-income households, and people rebuilding credit. A refinance that increases your monthly payment or stretches your loan term without a clear financial upside could leave you worse off than before. The requirements function as a filter that prevents poorly structured deals from moving forward, which protects you even when it feels like an obstacle.

What's at stake if you miss an eligibility check

Applying without confirming your eligibility first puts you at risk of paying upfront costs you cannot recover. Many lenders collect application fees, credit report fees, or processing charges before they complete a full review. If your loan hasn't reached the required seasoning period, or your payment history shows a late payment inside the restricted window, the loan will not close. You end up out of pocket with nothing to show for it.

Beyond the financial cost, a failed refinance attempt can also create problems with your credit profile and your timeline. Multiple hard inquiries from lenders stack up, and restarting the process later means going through underwriting again when rates may have shifted. Your current servicer may also take note of the activity. Spending time upfront to check every eligibility box against the actual guidelines before submitting an application is the most efficient thing you can do when you're considering a Streamline refinance.

How to see if you meet the basic eligibility rules

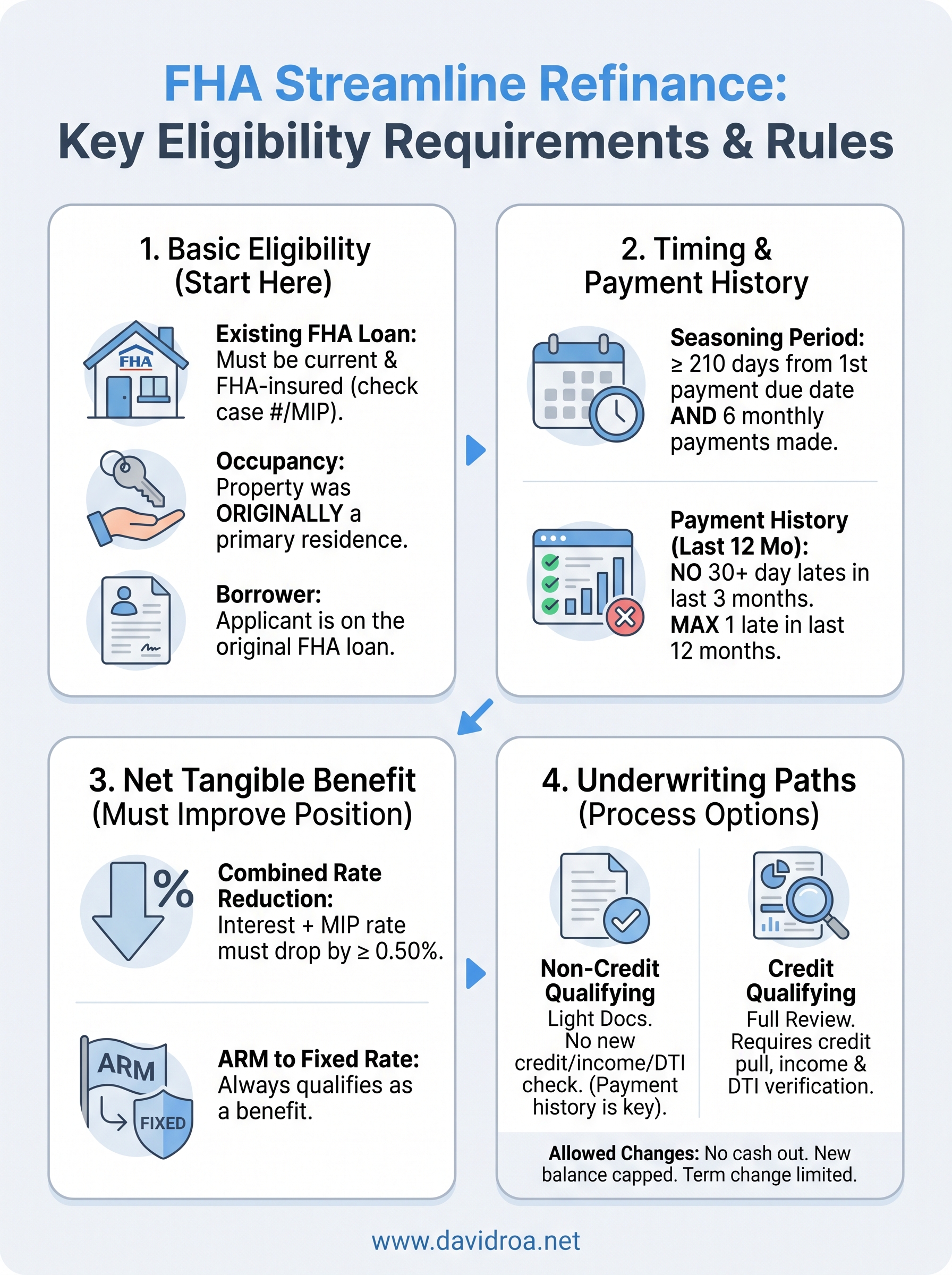

Before reviewing the full fha streamline refinance requirements, start with the foundational eligibility checks. These are the baseline conditions you must satisfy before anything else matters. If your loan or your current financial standing doesn't meet these basics, no amount of documentation or lender flexibility will change the outcome.

Your current loan must already be FHA-insured

The Streamline program is exclusively for existing FHA borrowers. You cannot use it to refinance a conventional loan, a VA loan, or a USDA loan into an FHA product. Your current mortgage must be insured by the Federal Housing Administration and must be in good standing with your servicer. You can verify your loan type by checking your original closing documents or your current mortgage statement, which will reference FHA case numbers or MIP (mortgage insurance premium) charges.

If your current loan doesn't carry FHA mortgage insurance, you need a standard FHA refinance or a conventional product, not the Streamline.

You must occupy or have occupied the property

The property tied to your FHA loan must have been your primary residence at some point. HUD guidelines allow you to use the Streamline even if you've since converted the home to a rental property, but the loan being refinanced must have originally been taken out on a primary residence. Investment properties purchased with FHA financing specifically for rental purposes from day one do not qualify. This rule catches many borrowers off guard, so check the purpose listed on your original FHA loan application if you're unsure.

Your name must be on the existing loan

You need to appear on the current FHA mortgage to refinance it through the Streamline program. If you were added to the title after closing but weren't on the original loan, you don't automatically qualify. The borrower of record on the existing FHA loan must be the one applying for the Streamline refinance.

Waiting periods and on-time payment requirements

Two of the most commonly overlooked fha streamline refinance requirements involve timing. You need to have held your current FHA loan for a minimum period before you can refinance it through the Streamline program, and your recent payment history must be clean. Both rules are firm, and no lender can waive them on your behalf. Getting clear on exactly where you stand on both counts before you apply saves you from a denial you could have avoided.

The seasoning period you must hit

Your existing FHA loan must have been open for at least 210 days before you can close on a Streamline refinance. HUD also requires that you've made at least six monthly payments on the current loan before the new loan closes. Both conditions must be satisfied, not just one. The 210-day clock starts from the first payment due date of your original loan, not from your closing date, so pull your mortgage statement and calculate from that specific date to confirm you're past the threshold.

If you're a few weeks short of the 210-day mark, waiting until you cross it is far better than rushing an application that HUD guidelines will reject outright.

Payment history rules that can disqualify you

Your most recent 12 months of payments will be reviewed, and no late payments are allowed in the 3 months immediately before your application date. Within the full 12-month window, you can have no more than one payment that was 30 or more days late. Even a single missed payment inside that restricted 3-month period is enough to stop the process entirely.

Lenders pull your payment history directly from your servicer records, not just from your credit report. That means disputed entries or delayed reporting won't work in your favor the way you might expect. If your record shows a recent late payment, waiting until you're safely past the restricted window is the most practical step before submitting your application.

Net tangible benefit and allowed loan changes

One of the core fha streamline refinance requirements is that your new loan must produce a net tangible benefit for you. This means the refinance has to result in a measurable financial improvement, not just move you from one loan to another with a new fee structure. HUD defines specific thresholds for what qualifies, and your lender must document that your new loan clears those thresholds before the file can close.

What counts as a net tangible benefit

HUD accepts several scenarios as valid net tangible benefits. The most common is a reduction in your combined rate (your interest rate plus your annual MIP rate) by at least 0.50 percentage points. If you're refinancing from an adjustable-rate FHA loan to a fixed-rate FHA loan, that move alone qualifies as a net tangible benefit regardless of rate change, because you're trading payment uncertainty for stability.

Moving from an ARM to a fixed rate qualifies on its own, even if your new interest rate is higher than your current rate.

You cannot use a lower monthly payment alone as the qualifying benefit if it's only lower because you're extending your loan term significantly. HUD looks at the combined rate reduction, not just what your statement shows due to re-amortization.

What changes the Streamline allows and restricts

The Streamline program limits the types of changes you can make to your loan at the same time as refinancing. You cannot take cash out. Your new loan balance is capped at your current unpaid principal balance plus allowable closing costs and prepaid items. You can change from a 30-year term to a 15-year term or keep the same term, but you cannot extend beyond your original loan term by more than 12 years. Any change to your loan structure must still satisfy the net tangible benefit test to move forward.

Documents, underwriting options, and costs to expect

The FHA streamline refinance requirements around documentation are lighter than a standard refinance, but they aren't zero. What you need to provide depends on the underwriting path your lender uses, so understanding both options before you apply helps you gather the right materials and avoid unnecessary delays.

Non-credit qualifying vs. credit qualifying underwriting

The Streamline program offers two underwriting tracks. Under the non-credit qualifying path, your lender does not pull a new credit report, verify your income, or calculate a debt-to-income ratio. Your payment history on the existing FHA loan carries most of the weight, and documentation requirements are minimal. Your lender will still need your current mortgage statement, proof of homeowner's insurance, and identification, but the file moves faster with fewer moving parts.

Choosing the non-credit qualifying path does not mean your lender skips the payment history review. That check still happens regardless of which track you're on.

The credit qualifying path requires a full credit pull, income verification, and a DTI calculation. Your lender may require this path if you're removing a borrower from the loan, if the payment history shows any issues, or if internal lender overlays demand it. In that case, expect to provide pay stubs, W-2s or tax returns, and bank statements similar to what you submitted on your original loan.

Costs to budget for

Even without an appraisal, a Streamline refinance still carries closing costs. You can expect lender fees, title charges, and prepaid items like your first year of homeowner's insurance or an escrow deposit. These costs typically run between 1% and 3% of the loan balance, and you generally cannot roll them into the new loan unless your lender structures a no-cost option with a slightly higher rate. Ask your lender for a full Loan Estimate within three business days of your application so you can compare the upfront cost against the monthly savings your new rate produces.

What to do next

Now that you understand the full fha streamline refinance requirements, the next step is to check your specific situation against each rule. Pull your current mortgage statement to confirm your loan type and payment history, then count back to your first payment date to verify you've cleared the 210-day seasoning period. If you've met the timing requirements and your last 12 months of payments are clean, you're in a strong position to move forward.

From there, the most valuable thing you can do is talk to a lender who works with FHA products regularly. A direct conversation about your current rate, remaining balance, and refinance goals will tell you quickly whether the net tangible benefit threshold is reachable and which underwriting path fits your file.

Ready to find out if you qualify? Talk to a mortgage expert at David Roa to review your FHA loan and get a clear answer on your refinance options.