Hard Money Loan Calculator: Payments, Points & ROI

Running the numbers before you sign for a hard money loan can mean the difference between a profitable flip and a costly mistake. A hard money loan calculator helps you estimate monthly interest-only payments, upfront points, and overall costs, so you can determine whether a deal actually makes financial sense before committing capital.

As a mortgage broker and active real estate investor with over 25 years in the lending industry, I've funded more than $150 million in loans, including hard money products for fix-and-flip projects. I've seen investors rush into deals without calculating true costs, only to watch their margins evaporate at closing. The right calculator prevents that.

This guide breaks down how hard money loan calculators work, what inputs you need, and how to interpret the results for smarter investment decisions. You'll also find a straightforward formula to run the math yourself, plus guidance on when hard money financing makes sense, and when it doesn't. Whether you're evaluating your first flip or your fiftieth, understanding these numbers puts you in control of the deal.

Why hard money loan calculators matter

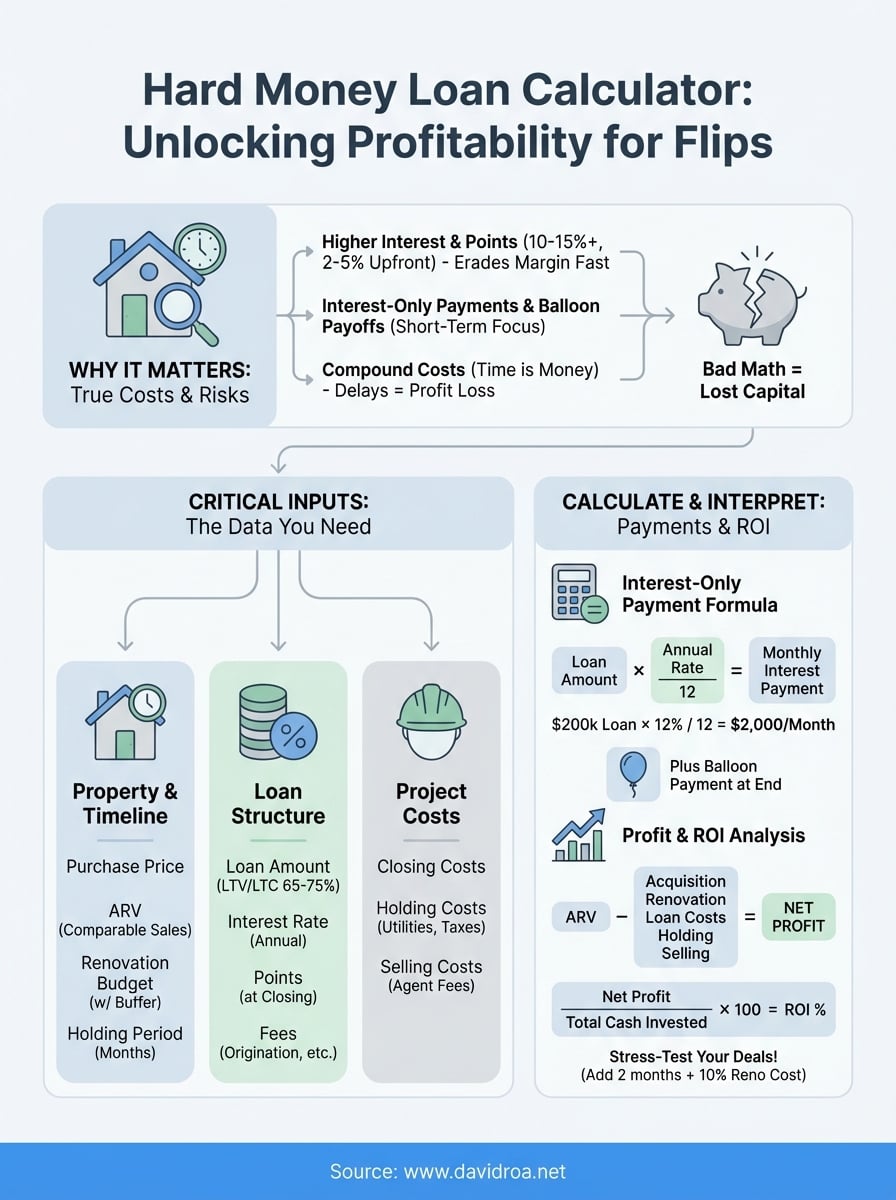

Hard money loans charge higher interest rates and upfront points that can quickly erode your profit margin if you don't calculate them accurately. Traditional mortgage calculators won't work here because they assume fully amortizing loans with principal and interest, while most hard money products require interest-only payments and balloon payoffs. You need a specialized tool that accounts for points, origination fees, exit fees, and short holding periods typical of fix-and-flip projects.

Hard money costs compound faster than traditional mortgages

You pay interest every month you hold the property, and at 10% to 15% annual rates, those payments add up fast. A $200,000 hard money loan at 12% costs you $2,000 per month in interest alone, before factoring in any construction expenses or holding costs. If your renovation takes four months instead of two, you've just added $4,000 to your project budget. A hard money loan calculator shows you exactly how much each additional month costs, so you can build realistic timelines and buffer your budget accordingly.

Most lenders also charge 2 to 5 points upfront, which means you pay $4,000 to $10,000 just to access that same $200,000 loan. Some add exit fees or extension penalties if you need more time. Calculating these costs before you make an offer tells you whether the deal leaves enough room for profit after renovations, closing costs, and resale expenses.

You need to know your break-even point before closing

Every flip has a minimum sale price that covers your acquisition cost, loan fees, interest, renovation budget, and selling costs. If you don't calculate this break-even number before you close, you're investing blind. A hard money loan calculator helps you reverse-engineer your offer price based on the after-repair value (ARV) and your target profit margin.

For example, if a property has an ARV of $350,000 and you want a $50,000 net profit, you need to work backward. Subtract your profit, then subtract 8% to 10% for selling costs ($28,000 to $35,000), then subtract your renovation budget and holding costs. What's left is your maximum all-in cost, including the purchase price, loan fees, and interest. Running these numbers through a calculator before you submit an offer keeps you from overpaying.

Running the numbers first protects you from deals that look profitable on paper but fail in reality.

Bad math turns profitable flips into losses

Investors who skip the calculator stage often underestimate their true cost of capital. You might assume your hard money loan will cost $15,000 total, but if you didn't factor in loan origination fees, appraisal costs, and title insurance, your actual out-of-pocket could hit $20,000 or more. That $5,000 difference wipes out a significant chunk of your expected profit, especially on lower-priced properties where margins are already thin.

I've worked with investors who budgeted for a three-month flip but took six months due to permit delays or contractor issues. Their monthly interest payments doubled, and they burned through their profit before they even listed the property. A hard money loan calculator would have shown them the cost of a delayed timeline, prompting them to either negotiate a lower purchase price or walk away entirely.

Accurate calculations also prevent you from overleveraging. If your numbers show you need to sell at $380,000 just to break even, and comparable properties are selling at $360,000, the deal doesn't work. Identifying that mismatch early saves you from tying up capital in a project that can't deliver returns.

The inputs you need before you run the numbers

You can't run accurate calculations without specific data points that define both the property and the loan structure. Gathering these numbers before you open a hard money loan calculator saves time and ensures your projections reflect reality. Missing even one input, like origination fees or the actual loan-to-value ratio, can throw off your entire budget and make an unprofitable deal look attractive.

Property acquisition and value numbers

You need your purchase price and the after-repair value (ARV) to determine how much capital you'll borrow and what your exit price needs to be. The purchase price is straightforward, but the ARV requires comparable sales data from recently sold properties in similar condition. Pull at least three to five comps that closed within the last 90 days and match your property's square footage, bedroom count, and location.

Your renovation budget should include materials, labor, permits, and a 10% to 20% contingency buffer for unexpected repairs. Don't estimate this casually. Walk the property with a contractor, get line-item bids, and add costs for utilities, insurance, and property taxes during the renovation period. These holding costs compound your total project expense and directly impact your profitability.

Loan terms and fee structure

Hard money lenders structure deals differently, so you need the exact interest rate, points charged, and loan-to-value (LTV) ratio your lender offers. Most hard money loans range from 65% to 75% LTV on the purchase price, though some lenders include renovation costs in the loan amount (loan-to-cost or LTC). Confirm whether your lender funds the full renovation budget upfront or releases it in draws as work progresses.

Points typically range from 2 to 5 points of the loan amount, paid at closing. Some lenders also charge origination fees, processing fees, or exit fees if you pay off the loan early or request an extension. List every fee your lender discloses so your calculator captures the true cost of capital.

Knowing the exact fee structure prevents surprises at closing that drain your working capital.

Project timeline and exit strategy

Your holding period determines how many months of interest you'll pay, so estimate conservatively. If you think renovations will take two months, budget for four. Most hard money loans run 6 to 12 months, and extending beyond that term often triggers penalty rates or extension fees. Calculate interest for your expected timeline, then add two months as a safety margin to see how delays impact your numbers.

How to calculate hard money payments

Hard money loans typically require interest-only payments each month, with the full principal balance due at the end of the loan term. This structure keeps your monthly costs lower than traditional mortgages but creates a balloon payment that you must satisfy through refinancing or property sale. Calculating your monthly payment requires only three numbers: the loan amount, the annual interest rate, and the number of months you'll hold the loan.

The interest-only payment formula

You calculate your monthly payment by multiplying your loan amount by the annual interest rate, then dividing by 12 months. For a $200,000 hard money loan at 12% annual interest, the formula looks like this: $200,000 × 0.12 = $24,000 annual interest, divided by 12 = $2,000 per month. That $2,000 covers only interest, so your principal balance stays at $200,000 throughout the entire loan term.

Most hard money loan calculators automate this formula, but understanding the math helps you verify results and adjust projections quickly. If your lender quotes you 11.5% interest instead of 12%, you can immediately see your monthly payment drops to $1,917, saving you $83 per month. Over a six-month flip, that difference adds up to $498 in reduced carrying costs.

Running the interest-only calculation yourself confirms your lender's numbers and prevents billing errors that inflate your costs.

Factor in the loan term and balloon payment

Your loan term determines how many months you'll make interest payments before the balloon payment comes due. Most hard money loans run 6 to 12 months, though some lenders offer 18 or 24-month terms for larger projects. Each month you hold the loan adds another interest payment to your total cost, so accurate timeline estimates directly impact your profitability.

Calculate your total interest expense by multiplying your monthly payment by the number of months you'll carry the loan. Using the $2,000 monthly payment example, a four-month flip costs $8,000 in interest, while a six-month project costs $12,000. Add your balloon payment (the full loan amount) to see your total repayment obligation at the end of the term. For that $200,000 loan held for six months, you'll pay $212,000 total: $12,000 in interest plus the $200,000 principal.

If you can't sell or refinance before the term ends, extension fees typically add 1 to 3 points and may increase your interest rate. Budget for at least one potential extension when you calculate payments, so you don't get trapped in a deal that bleeds cash while you wait for the right buyer.

How to calculate points, fees, and cash to close

Points and fees hit your budget before you even start renovations, so calculating your upfront cash requirement separates viable deals from capital traps. A hard money loan calculator shows you the total amount you need at closing, including the down payment, origination points, and various lender fees that don't appear in your monthly payment calculation. These costs reduce your working capital and must fit within your available funds without forcing you to cut corners on renovations.

Calculate origination points and lender fees

Hard money lenders charge points as a percentage of the loan amount, not the purchase price. Each point equals 1% of what you borrow, so 3 points on a $150,000 loan costs you $4,500 at closing. Some lenders advertise low interest rates but compensate with higher points, while others reverse that structure. Calculate the total cost of both to compare offers accurately.

Beyond points, lenders add origination fees, processing fees, underwriting fees, and document preparation charges that range from $500 to $2,000 combined. Some charge appraisal fees separately ($400 to $800), while others bundle them into closing costs. Request a full fee schedule from each lender you're considering, then add every line item to see your true cost of capital. A loan that appears cheaper based on rate alone might cost more once you account for all fees.

Calculate every fee upfront to avoid closing-day surprises that drain your renovation budget.

Total your upfront cash requirement

Your cash to close includes your down payment plus all fees and points, so start with your purchase price and subtract the loan amount to find your equity requirement. If you're buying a $200,000 property with a 70% LTV hard money loan, you borrow $140,000 and contribute $60,000 as your down payment. Add your points ($4,200 at 3 points) and fees ($1,500 estimated), bringing your total cash to close to $65,700 before accounting for title insurance, recording fees, and property taxes.

Most investors underestimate this number because they forget closing costs that exist outside the loan structure. Title insurance, escrow fees, and transfer taxes typically add 2% to 3% of the purchase price ($4,000 to $6,000 on a $200,000 property). Plugging these figures into a hard money loan calculator before you make an offer confirms you have sufficient liquid capital to close the deal and fund initial renovations without depleting your reserves entirely.

How to estimate profit and ROI on a flip

Calculating your net profit and return on investment (ROI) determines whether a flip meets your investment criteria before you commit capital. A hard money loan calculator helps you project these numbers by factoring in your total acquisition cost, renovation budget, carrying costs, and expected sale price. Running these calculations early in your deal analysis prevents you from overpaying or underestimating expenses that destroy your margins.

Calculate your net profit after all costs

Your net profit equals your after-repair value (ARV) minus all acquisition costs, renovation expenses, hard money loan fees and interest, holding costs, and selling expenses. Start with your ARV, which you determine from comparable sales data. Subtract your purchase price, then subtract every dollar you'll spend to close, renovate, carry, and sell the property. What remains is your net profit before taxes.

For a concrete example, assume you buy a property for $200,000 using a hard money loan at 70% LTV ($140,000 borrowed), pay 3 points ($4,200), and hold the loan for five months at 12% annual interest ($7,000 total). Add a $40,000 renovation budget, $3,000 in holding costs (utilities, insurance, taxes), and 8% selling costs on a $300,000 ARV ($24,000). Your total cost breakdown looks like this: $200,000 purchase + $60,000 down payment + $4,200 points + $7,000 interest + $40,000 renovation + $3,000 holding + $24,000 selling = $278,200 all-in cost. Subtract that from your $300,000 sale price to net $21,800 profit.

Run your profit calculation with an extra two months of interest and 10% higher renovation costs to stress-test the deal.

Use ROI to compare deals and measure performance

ROI measures how efficiently your capital works by dividing your net profit by your total cash invested, then multiplying by 100 to get a percentage. Your cash invested includes your down payment plus all upfront fees and your renovation budget. Using the previous example, you invested $60,000 down payment + $4,200 points + $40,000 renovation = $104,200 total cash. Divide your $21,800 profit by $104,200, then multiply by 100 to get 20.9% ROI on this flip.

Annualizing your ROI helps you compare deals with different timelines. Divide your ROI by the number of months you held the property, then multiply by 12. A 20.9% ROI over five months equals 4.18% per month, which annualizes to 50.2% annual ROI. This metric shows you how your capital performs relative to other investment opportunities and helps you prioritize deals that maximize returns per dollar invested. Properties with lower profit but faster turnaround times often generate better annualized returns than higher-profit deals that tie up capital for longer periods.

Conclusion section

Running a hard money loan calculator before you commit to a flip protects your capital and prevents deals that look profitable but fail in execution. The calculator shows you your true monthly costs, total fees, and net profit after accounting for every expense that traditional mortgage calculators miss. You need accurate numbers on points, interest payments, renovation budgets, and holding costs to determine whether a property delivers acceptable returns on your invested capital.

Calculate your break-even price and annualized ROI for every deal you evaluate, then compare those numbers against your investment criteria before making offers. Properties that pencil out on paper sometimes fail in reality when timelines extend or unexpected costs emerge, so stress-test your projections with conservative assumptions. If you need financing for your next fix-and-flip project or want guidance on structuring deals that maximize returns, connect with our lending team to discuss hard money options tailored to your investment strategy.