HUD FHA Handbook: What It Is and Key 4000.1 Policies Today

Every FHA loan approval traces back to one source: the HUD FHA Handbook. Officially known as Handbook 4000.1, this document contains the complete rules that lenders, underwriters, and appraisers must follow when processing FHA-insured mortgages. Whether you're buying your first home or refinancing, the policies in this handbook directly affect your eligibility and loan terms.

After funding over $150 million in loans, including countless FHA transactions, I've seen how understanding these guidelines gives borrowers a real advantage. Knowing what the handbook requires helps you prepare the right documentation, avoid delays, and set realistic expectations before you even apply.

This guide breaks down what Handbook 4000.1 covers, the key policies you should know about, and how these rules translate into practical requirements for your mortgage. If you're working toward an FHA loan, this is where the answers live.

What the HUD FHA Handbook covers

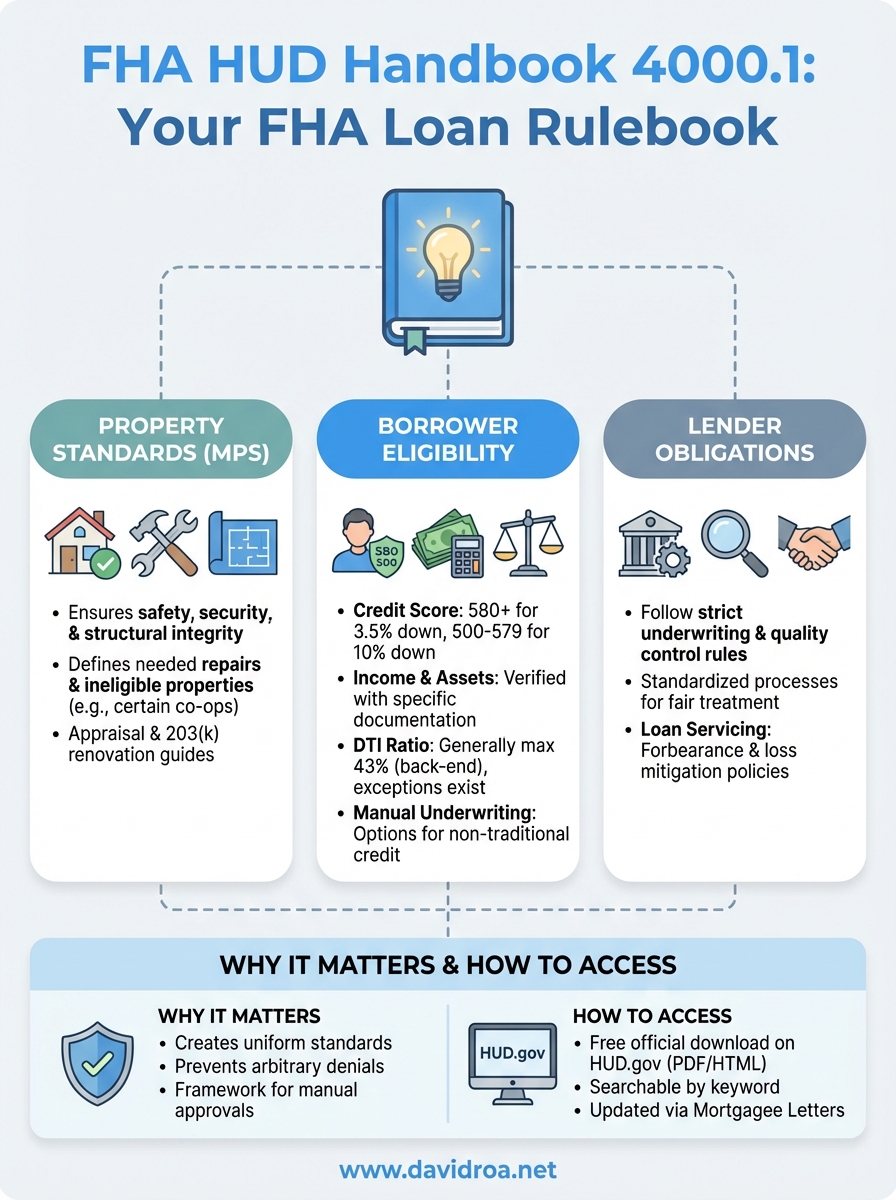

The HUD FHA Handbook functions as the complete rulebook for every step of the FHA loan process. It consolidates policies for lenders, requirements for borrowers, and standards for properties into one authoritative document. Before this handbook existed, FHA guidelines lived across hundreds of separate mortgagee letters and policy updates, creating confusion and inconsistencies across the industry.

Handbook 4000.1 organizes these rules into four main sections that address origination, underwriting, property requirements, and loan servicing. Each section drills down into specific scenarios you'll encounter during your loan application. The document tells lenders exactly what documentation they must collect, how to verify your income and assets, and which property conditions make a home ineligible for FHA financing.

Property and appraisal requirements

Your property must meet minimum property standards (MPS) outlined in the handbook before FHA will insure your loan. These standards cover structural integrity, safety hazards, and basic livability requirements. The appraiser uses the handbook to determine whether deficiencies need repair before closing or if the property fails to qualify entirely.

The handbook specifies acceptable property types, from single-family homes to condominiums, and lists ineligible properties like co-ops or properties with certain HOA restrictions. It also defines how appraisers must handle properties with accessory dwelling units, properties on leased land, and homes requiring 203(k) renovation financing.

Understanding property requirements before you make an offer saves you from delays or deal-breaking discoveries during the appraisal.

Borrower eligibility standards

Handbook 4000.1 defines the credit, income, and debt ratio requirements that determine your FHA loan eligibility. You'll find specific rules for minimum credit scores, acceptable debt-to-income ratios, and how lenders must document non-traditional credit. The handbook also addresses special circumstances like recent bankruptcies, foreclosures, and employment gaps.

Income verification follows detailed protocols in the handbook, including how to calculate self-employment income, verify overtime and bonuses, and handle non-occupant co-borrowers. If you're using gift funds for your down payment, the handbook outlines exactly what documentation the donor must provide and which relationships qualify as acceptable gift sources.

Lender obligations and processes

Lenders must follow the handbook's underwriting standards and quality control requirements to maintain their FHA approval status. The document specifies which automated underwriting systems they can use, how to manually underwrite loans that don't receive automated approval, and what compensating factors can offset risk indicators in your application.

The handbook also governs how lenders handle loan modifications, loss mitigation, and servicing requirements after you close. This includes forbearance policies, requirements for communicating with borrowers facing hardship, and procedures for handling insurance claims. Understanding these servicing rules matters if you ever face financial difficulty and need to work with your lender on payment solutions.

Why HUD Handbook 4000.1 matters to borrowers

The HUD FHA Handbook directly determines whether your loan application gets approved and what terms you'll receive. Every requirement your lender asks you to meet, every document they request, and every property standard they enforce comes from this handbook. When a lender tells you that you need a 580 credit score for minimum down payment or that your property needs specific repairs, they're following mandatory policies spelled out in Handbook 4000.1.

Understanding these rules gives you practical advantages during your home purchase. You'll know which documentation to prepare before applying, which property issues will require attention before closing, and what alternative solutions exist when you don't meet standard requirements. This knowledge prevents surprises that delay your closing or force you to restart your home search.

How the handbook protects your interests

Handbook 4000.1 creates uniform standards that every FHA-approved lender must follow. This standardization prevents arbitrary denials and ensures you receive consistent treatment regardless of which lender you choose. The handbook requires lenders to consider compensating factors when one part of your application shows weakness, rather than automatically rejecting your loan.

The document also establishes clear guidelines for manual underwriting when automated systems don't approve your loan. These guidelines give underwriters a framework for approving borrowers with non-traditional credit histories or unique income situations. Without these standardized rules, lenders would apply inconsistent criteria that make the approval process unpredictable.

Knowing the handbook's requirements lets you prepare a complete application the first time and avoid unnecessary back-and-forth with your lender.

What happens when lenders ignore handbook rules

Lenders who violate the hud fha handbook risk losing their FHA approval and facing penalties from HUD. This enforcement matters to you because it creates accountability. If your lender denies your application based on requirements not found in the handbook, you have grounds to question that decision and potentially work with a different lender who follows the actual rules.

Quality control audits and HUD reviews regularly check whether lenders comply with handbook standards. These oversight mechanisms protect borrowers from improper denials or unreasonable requirements that exceed FHA's actual policies.

Where to find the official handbook and updates

HUD publishes the complete Handbook 4000.1 on its official website at no cost. You can access, download, and search the document directly without creating an account or paying subscription fees. The handbook lives on HUD's single-family housing policy portal, where you'll also find supplemental resources like mortgagee letters, administrative memos, and frequently asked questions.

Accessing the handbook gives you the same information your lender uses to evaluate your application. You can reference specific policy numbers when discussing your loan with your loan officer and verify that requirements they mention actually exist in the official documentation.

Accessing Handbook 4000.1 directly

The HUD.gov website hosts the current version of Handbook 4000.1 in multiple formats. You'll find the full document as a searchable PDF and as individual HTML chapters organized by topic. The HTML format works better when you need to quickly locate specific requirements using keyword searches or when reading on mobile devices.

Each chapter in the online version includes a table of contents that jumps you to relevant sections. You can bookmark specific policy sections for quick reference later. The PDF version lets you download the entire handbook for offline access, which matters if you're reviewing requirements during property showings or discussions with real estate agents.

The official HUD.gov portal remains your most reliable source for current FHA policies, avoiding outdated information from third-party sites.

Tracking policy changes and mortgagee letters

HUD issues mortgagee letters throughout the year to announce policy changes, clarifications, and temporary guidelines that affect the hud fha handbook. These letters often modify specific handbook requirements or introduce new procedures before the handbook itself receives formal updates. You'll find an archive of recent mortgagee letters on the same HUD policy portal where the handbook lives.

Subscribing to HUD's email notifications keeps you informed when new mortgagee letters publish. Your lender should follow these updates immediately, but understanding recent changes yourself prevents confusion when requirements shift between when you start researching and when you actually apply for your loan.

How to use the handbook without getting lost

The hud fha handbook spans over 1,000 pages, but you don't need to read it cover to cover. Most borrowers only need to reference specific sections that apply to their unique situation. Learning to navigate the handbook efficiently saves you hours of reading policies that won't affect your loan application.

Your loan officer handles most handbook compliance automatically, but understanding how to find relevant information yourself gives you confidence during the process. When questions arise about specific requirements, you can verify the answer directly instead of relying solely on secondhand explanations.

Start with the table of contents

Each chapter in Handbook 4000.1 covers a distinct loan phase or topic area. Chapter II addresses property requirements and appraisals, while Chapter III focuses on borrower eligibility and underwriting standards. The table of contents shows you exactly which chapter contains the information you need.

Reading just the relevant chapter introduction gives you context before diving into detailed requirements. These introductions explain the chapter's purpose and how policies connect to your overall loan approval.

Targeting specific chapters based on your questions prevents wasting time reading unrelated policies.

Use the search function strategically

The PDF version of the handbook includes full-text search that lets you find specific terms or policy numbers instantly. Searching for keywords like "gift funds," "self-employment," or "appraisal conditions" takes you directly to relevant policy sections without scrolling through hundreds of pages.

When your lender mentions a specific requirement, ask them for the policy number or section reference. You can then search that exact reference in the handbook to read the complete policy context and understand any exceptions or alternative approaches.

Focus on relevant chapters for your situation

Chapter III addresses borrower credit and income requirements that affect your initial eligibility. If you're evaluating properties, Chapter II covers the minimum property standards your home must meet. Chapter IV becomes relevant after closing if you need loan modification or face payment difficulties.

Bookmark sections that apply to your specific circumstances, like non-traditional credit documentation or ITIN borrower requirements. This targeted approach lets you reference exact policies when discussing your application with your loan officer.

Key 4000.1 rules that affect your FHA loan

Several specific policies in the hud fha handbook directly determine your loan approval and terms. Understanding these core requirements helps you prepare documentation correctly and set realistic expectations before applying. These rules affect your minimum down payment, acceptable debt levels, and credit standards that lenders must follow.

Credit score minimums and exceptions

You need a minimum 580 credit score to qualify for FHA's standard 3.5% down payment option. Borrowers with scores between 500 and 579 can still obtain FHA financing, but the handbook requires a 10% down payment for this lower credit tier. Lenders can impose overlays that require higher scores, but they cannot approve loans below these handbook minimums.

The handbook also addresses manual underwriting requirements for borrowers without traditional credit scores. If you lack three tradelines on your credit report, your lender can document alternative credit sources like rent payments, utility bills, and insurance payments to establish your creditworthiness.

Manual underwriting provisions in Handbook 4000.1 give you approval options even when automated systems deny your application.

Down payment and upfront costs

Your down payment requirement depends on your credit score tier, with 3.5% representing the minimum for borrowers scoring 580 or higher. The handbook permits down payment funds from gifts, employer assistance programs, or grants from approved nonprofits. You can also use funds from retirement accounts without penalty when buying your first home.

FHA charges an upfront mortgage insurance premium equal to 1.75% of your loan amount, which you can finance into your loan rather than paying at closing. Annual mortgage insurance continues for the life of your loan when you put down less than 10%, or for 11 years when you make a larger down payment.

Debt-to-income ratio limits

The handbook establishes 43% as the maximum back-end ratio for most FHA loans, though automated underwriting systems can approve ratios up to 50% or higher when compensating factors exist. Your front-end ratio, which includes only housing expenses, should stay below 31% for standard approvals.

Manual underwriting requires stronger compensating factors when your ratios exceed these thresholds. Acceptable compensating factors include minimal debt history, significant cash reserves, or demonstrated ability to save money while meeting current obligations.

Next steps for your FHA loan

The hud fha handbook gives you the blueprint for every requirement your lender must follow. Understanding these policies helps you prepare complete documentation and avoid approval delays that derail your timeline.

Start by reviewing the specific chapters that apply to your situation, whether that's credit requirements, property standards, or income verification rules. Knowing what the handbook requires before you apply puts you ahead of most borrowers who discover requirements only after problems arise.

Working with a loan officer who knows Handbook 4000.1 thoroughly makes the difference between smooth approvals and frustrating delays. I've funded over $150 million in loans, including complex FHA scenarios involving ITIN borrowers, manual underwriting, and properties requiring repairs. Get expert guidance on your FHA loan to ensure your application meets every handbook requirement from day one.