Real Estate Investing for Beginners: A Step-By-Step Guide

You've heard the stories, regular people building wealth through rental properties, house flipping, or strategic real estate deals. But when you're starting from zero, real estate investing for beginners can feel overwhelming. Where do you even begin? How much money do you actually need? What strategies make sense for your situation?

These are questions I hear constantly. With over 25 years in mortgage lending and hands-on experience as an active real estate investor myself, I've helped hundreds of first-time investors secure the right financing to close their first deal. The path to property investing isn't as complicated as it seems, but it does require solid knowledge and a financial partner who understands investor needs.

This guide breaks down everything you need to get started: from understanding different investment strategies like rental properties, REITs, and house hacking, to calculating your financial requirements and taking concrete steps toward your first purchase. Whether you have $10,000 or $100,000 to work with, there's an entry point that fits your budget, and a loan product designed for your specific situation.

How real estate investing works and what to expect

Real estate investing isn't rocket science, but it operates differently from stocks or bonds. You put money down on a property (or control it through various financing structures), and that asset generates returns through appreciation, rental income, or both. Unlike paper investments, real estate gives you a tangible asset you can improve, refinance, or leverage to acquire more properties. The fundamentals haven't changed in decades: buy at the right price, manage the asset properly, and either hold for long-term wealth or exit strategically for profit.

The basic mechanics of property investment

When you invest in real estate, you're acquiring physical property that can produce income. Most beginners start by purchasing a property with financing (typically 20-25% down for investment properties), then either rent it out or improve and resell it. Your returns come from two primary sources: equity buildup as you pay down the mortgage, and property value appreciation over time. If you rent the property, monthly rental income covers your mortgage payment, taxes, insurance, and ideally leaves cash flow in your pocket.

Leverage is what separates real estate from other investments. You can control a $300,000 property with $60,000 down, meaning your returns calculate based on your actual cash invested, not the full property value. When that property appreciates by 5% annually, you're earning $15,000 on a $60,000 investment, which equals a 25% return on your money. This principle applies whether you're buying a single-family rental, a multi-unit building, or a fix-and-flip project.

Income streams you can expect

Rental income represents the most straightforward return for real estate investing for beginners. You collect monthly rent checks that cover your expenses and, ideally, generate positive cash flow. A $1,500 monthly rent payment might cover a $1,100 mortgage, $150 in property taxes, $100 in insurance, and leave $150 in your pocket. That's $1,800 per year in cash flow, plus the equity buildup from mortgage principal payments and any appreciation.

"Real estate creates wealth through multiple channels simultaneously: cash flow, appreciation, loan paydown, and tax advantages that stocks simply cannot match."

Appreciation builds your net worth passively. Properties in strong markets typically increase 3-5% annually, though this varies by location and economic conditions. Tax benefits also boost your effective returns. Depreciation deductions allow you to write off a portion of the property's value each year, and expenses like repairs, property management, and mortgage interest reduce your taxable income.

Timeline and commitment level

Expect your first investment to take 3-6 months from education to closing. You'll spend time analyzing deals, securing financing, and conducting due diligence. Once you own the property, involvement depends on your strategy. Rental properties demand ongoing management, whether you handle tenant issues yourself or hire a property manager for 8-10% of monthly rent.

Fix-and-flip projects require intense but shorter-term commitment, typically 4-6 months of active renovation management. Passive investments like REITs or syndications need minimal involvement but offer less control and lower returns. Your first deal will consume more time as you learn the process, but subsequent purchases become significantly faster once you understand financing options, market analysis, and due diligence procedures.

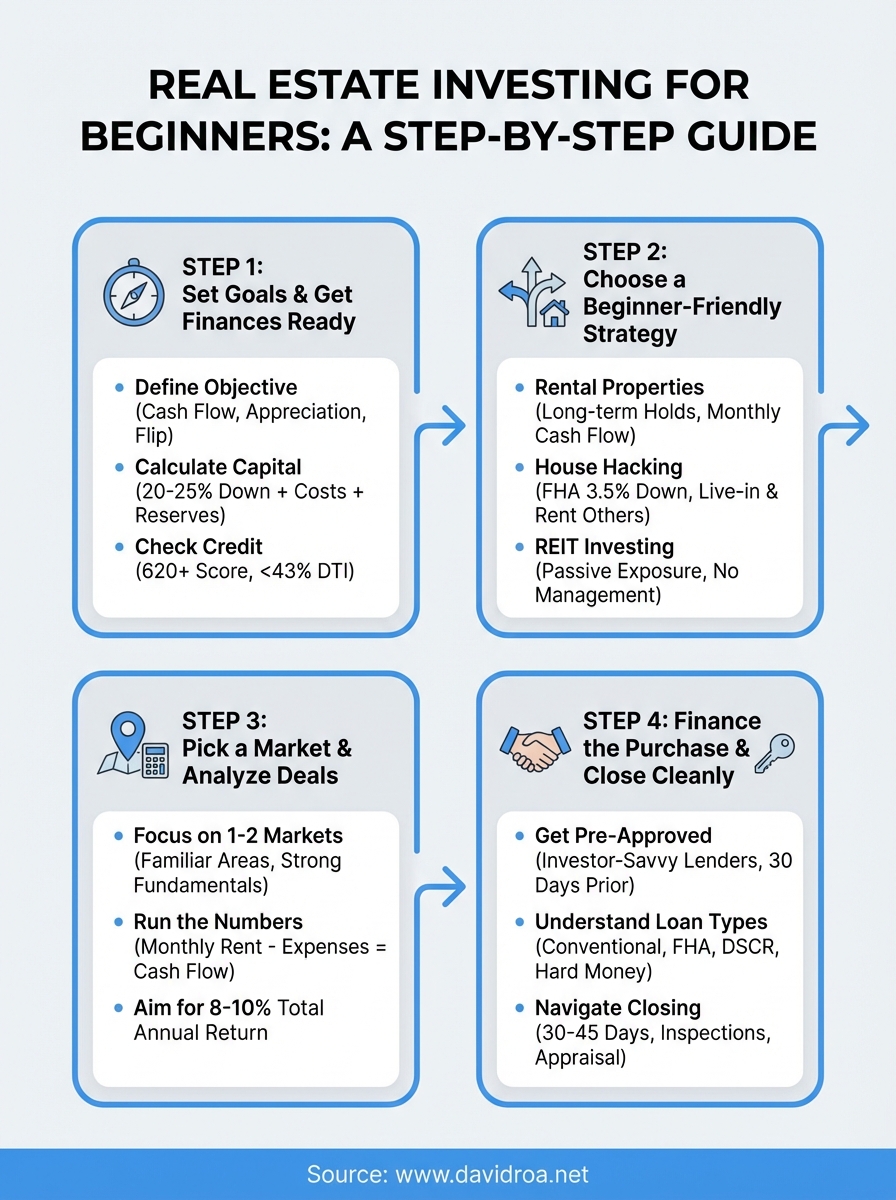

Step 1. Set goals and get your finances ready

Your first move in real estate investing for beginners starts with clarity about what you want and an honest assessment of your financial position. You need to know whether you're targeting monthly cash flow, long-term appreciation, or quick profits from flipping. This decision shapes everything: the properties you pursue, the financing you need, and the timeline you operate on. Skip this step and you'll waste months chasing deals that don't align with your actual situation.

Define your investment objective

Write down a specific goal that includes numbers and timeframes. "I want to build wealth through real estate" doesn't cut it. Instead, try "I want to acquire two rental properties within 18 months that generate $400 per month in cash flow each." This clarity helps you filter opportunities and stay focused when attractive but misaligned deals surface.

Your objective should reflect your personal circumstances and risk tolerance. If you need income now, prioritize cash-flowing rentals or house hacking strategies. If you can wait 5-10 years for returns, appreciation-focused properties in emerging markets make sense. Consider time commitment too: flipping demands active management, while REITs require almost no involvement but offer smaller returns.

"Setting a concrete investment goal with measurable targets transforms your search from browsing properties to executing a strategic plan."

Calculate your starting capital

You need to know exactly how much cash you can deploy without jeopardizing your financial stability. Most lenders require 20-25% down on investment properties, plus closing costs of 2-3% and reserves of 3-6 months of property expenses. For a $250,000 rental property, expect to bring $50,000-$62,500 for the down payment, $5,000-$7,500 for closing costs, and $4,500-$9,000 in reserves. That's $59,500-$79,000 total to get started.

Alternative strategies require less capital. House hacking allows you to live in one unit while renting others, qualifying for owner-occupied financing with just 3.5-5% down. DSCR loans (Debt Service Coverage Ratio) evaluate the property's income rather than your personal finances, opening doors for investors with cash but irregular income. Partnership structures let you contribute knowledge and sweat equity while a partner provides capital, splitting profits based on your agreement.

Document your available funds, credit score, and debt-to-income ratio. Most investment property loans require a credit score of 620-640 minimum, though better rates come with 740+. Your debt-to-income ratio should stay below 43% to qualify for conventional financing, though some portfolio lenders offer flexibility.

Step 2. Choose a beginner-friendly strategy

You don't need to master every real estate strategy before making your first investment. Pick one approach that matches your capital, time availability, and risk tolerance, then execute it competently. The three strategies below work particularly well for real estate investing for beginners because they offer clear entry points, manageable learning curves, and proven track records of success.

Rental properties with long-term holds

Buy a single-family home or small multi-unit property, rent it out, and hold it for years while tenants pay down your mortgage. This strategy builds wealth through monthly cash flow, appreciation, and equity buildup simultaneously. You target properties where rent covers your mortgage payment plus expenses, leaving $200-$400 monthly in your pocket.

Start with single-family homes in stable neighborhoods where rents run 1% or higher of the purchase price monthly. A $200,000 property should generate at least $2,000 in monthly rent to work. Factor in vacancy (8% annually), maintenance (10% of rent), property management (8-10% if you hire out), and your actual expenses to calculate real cash flow.

House hacking for minimal capital

Move into a 2-4 unit property using an FHA loan with just 3.5% down, live in one unit, and rent out the others. Your tenants cover most or all of your mortgage payment while you build equity and learn property management with minimal risk. After one year of occupancy, you can repeat the process with another property while keeping the first as a pure rental.

"House hacking cuts your entry cost by 75% compared to traditional investment properties while giving you hands-on experience managing tenants and properties."

Look for duplexes or triplexes in decent neighborhoods where individual units rent for $800-$1,200 monthly. Your 3.5% down payment on a $300,000 triplex equals just $10,500, compared to $60,000 for a traditional investment property.

REIT investing for passive exposure

Buy shares of Real Estate Investment Trusts through your brokerage account if you want property exposure without property management. REITs own and operate income-producing real estate, distributing 90% of taxable income as dividends. You invest with any amount, gain instant diversification, and skip tenant calls entirely. Returns average 8-12% annually but offer no leverage benefits or tax advantages that direct ownership provides.

Step 3. Pick a market and analyze deals

You can't invest everywhere, so focus your energy on one or two markets where the numbers actually work. This step separates successful investors from perpetual researchers. You need to identify areas with strong rental demand, reasonable property prices relative to rent, and economic fundamentals that support growth. Then you run specific calculations on individual properties to determine if each deal generates acceptable returns.

Pick your target market

Start with markets you know personally or can visit easily. Investing in your hometown or nearby cities cuts travel costs and lets you inspect properties without flying across the country. Look for areas with population growth, job diversity, and landlord-friendly laws. Check local rent-to-price ratios: you want markets where monthly rent equals at least 0.8-1% of the purchase price.

Use free resources to evaluate market fundamentals. Search "City Name economic development" or "City Name population growth" to find municipal data showing job creation and demographic trends. Real estate platforms display median home prices and rental rates by ZIP code. Cross-reference three neighborhoods in your target city, comparing average rents against property prices to spot the best opportunities for real estate investing for beginners.

"The right market gives you built-in advantages through strong fundamentals, while the wrong market forces you to fight uphill regardless of how well you manage the property."

Run the numbers on specific properties

Calculate potential cash flow before making any offer. Use this formula: Monthly Rent - (Mortgage + Taxes + Insurance + Maintenance + Vacancy + Property Management) = Cash Flow. A $200,000 property with $1,600 monthly rent, $1,100 mortgage, $150 taxes, $100 insurance, $160 maintenance (10%), $128 vacancy (8%), and $144 property management (9%) leaves $18 monthly cash flow. That's marginal but acceptable for appreciation-focused markets.

Calculate cash-on-cash return by dividing annual cash flow by your total cash invested. If you put $50,000 down plus $7,000 in closing costs ($57,000 total) and net $2,400 annually in cash flow, your return equals 4.2%. Add equity paydown and appreciation to see your total return. Properties should deliver at least 8-10% total annual returns to justify the time commitment and risk.

Verify rent estimates by checking actual listings for comparable units in the same neighborhood. Call three property management companies asking what similar properties rent for currently. Their answers will be more accurate than online estimates.

Step 4. Finance the purchase and close cleanly

Financing separates serious buyers from browsers, and getting your loan secured properly determines whether you close on time or lose the deal. You need to understand which loan products match your investment strategy, get pre-approved before making offers, and manage the closing process without surprises. This step requires working with lenders who understand investment property financing, not residential mortgage officers who primarily handle primary residences.

Secure pre-approval with investment-savvy lenders

Contact lenders who specialize in investor financing at least 30 days before making your first offer. Explain your investment strategy clearly: are you buying a rental property, house hacking, or flipping? Each requires different loan products. Traditional investment property loans need 20-25% down with 620+ credit scores, while FHA house hacking works with 3.5% down if you occupy the property.

DSCR loans (Debt Service Coverage Ratio) evaluate the property's rental income instead of your personal income, which works perfectly for real estate investing for beginners with cash but irregular W-2 income. Hard money loans fund flips quickly (5-10 days) but charge 10-12% interest and require 20-30% down. Bring your tax returns, bank statements, and credit reports to your pre-approval meeting. Lock your rate once approved to protect against increases during your property search.

"Pre-approval with the right lender gives you credibility with sellers and speeds up closing by 2-3 weeks compared to starting from scratch after your offer gets accepted."

Navigate closing without delays

Once your offer gets accepted, you enter a 30-45 day closing period filled with inspections, appraisals, and final loan processing. Order your inspection within 5 days and negotiate repairs or price reductions based on findings. Your lender orders the appraisal, which must support your purchase price or renegotiation becomes necessary.

Review your Closing Disclosure three days before closing to verify loan terms, interest rate, and closing costs match your expectations. Wire funds to the title company 24 hours before closing and bring your driver's license to the signing appointment. Most closings take 45-90 minutes of signing documents before you receive keys and officially own investment property.

Your next move

You have the framework for real estate investing for beginners: set clear goals, pick a strategy that matches your capital, identify strong markets, analyze deals properly, and secure financing from lenders who understand investment properties. The difference between reading this guide and building wealth comes down to taking action on your first deal.

Start by calling three lenders this week to discuss your specific situation and available loan products. Review properties in your target market and run the cash flow calculations on at least five listings. The numbers will tell you which deals work and which don't.

When you're ready to move forward with financing that fits your investment strategy, connect with an experienced lender who has closed over $150 million in transactions and actively invests in real estate themselves. That combination of lending expertise and investor perspective makes the difference between smooth closings and deals that fall apart.