Calculate Monthly Mortgage Payment: Formula + PITI

Before you sign anything or fall in love with a listing, you need to calculate monthly mortgage payment costs down to the dollar. Not a rough guess, an actual number that accounts for principal, interest, taxes, and insurance. That full picture, known as PITI, is what determines whether a home fits your budget or stretches it past the breaking point.

Most online calculators give you a basic estimate, but they skip the details that actually move the needle. Escrow costs, PMI, HOA fees, these add up fast, and ignoring them leads to surprises you don't want at closing. After funding over $150 million in residential and investment loans, I've watched buyers get blindsided by numbers they didn't run properly beforehand.

This guide breaks down the exact mortgage payment formula, walks you through each PITI component, and shows you how to run the math yourself. Whether you're a first-time buyer or an investor analyzing a new deal, you'll walk away knowing precisely what your monthly obligation looks like, and what drives it up or down.

What your monthly mortgage payment includes

When you calculate monthly mortgage payment costs, most people focus only on the loan amount and interest rate. That's a mistake. Your actual monthly obligation is built from multiple components, and understanding each one prevents the shock of seeing a number at closing that's far higher than you expected.

Principal and interest

The principal is the portion of your payment that reduces your loan balance. The interest is the cost of borrowing that money, expressed as an annual percentage rate applied monthly. Early in your loan, most of your payment goes toward interest, not principal. This is how amortization works. A 30-year loan at 7% means your first payment might allocate roughly 80% to interest and only 20% to principal reduction.

As you pay down the balance over time, that ratio shifts, and more of each payment chips away at what you actually owe.

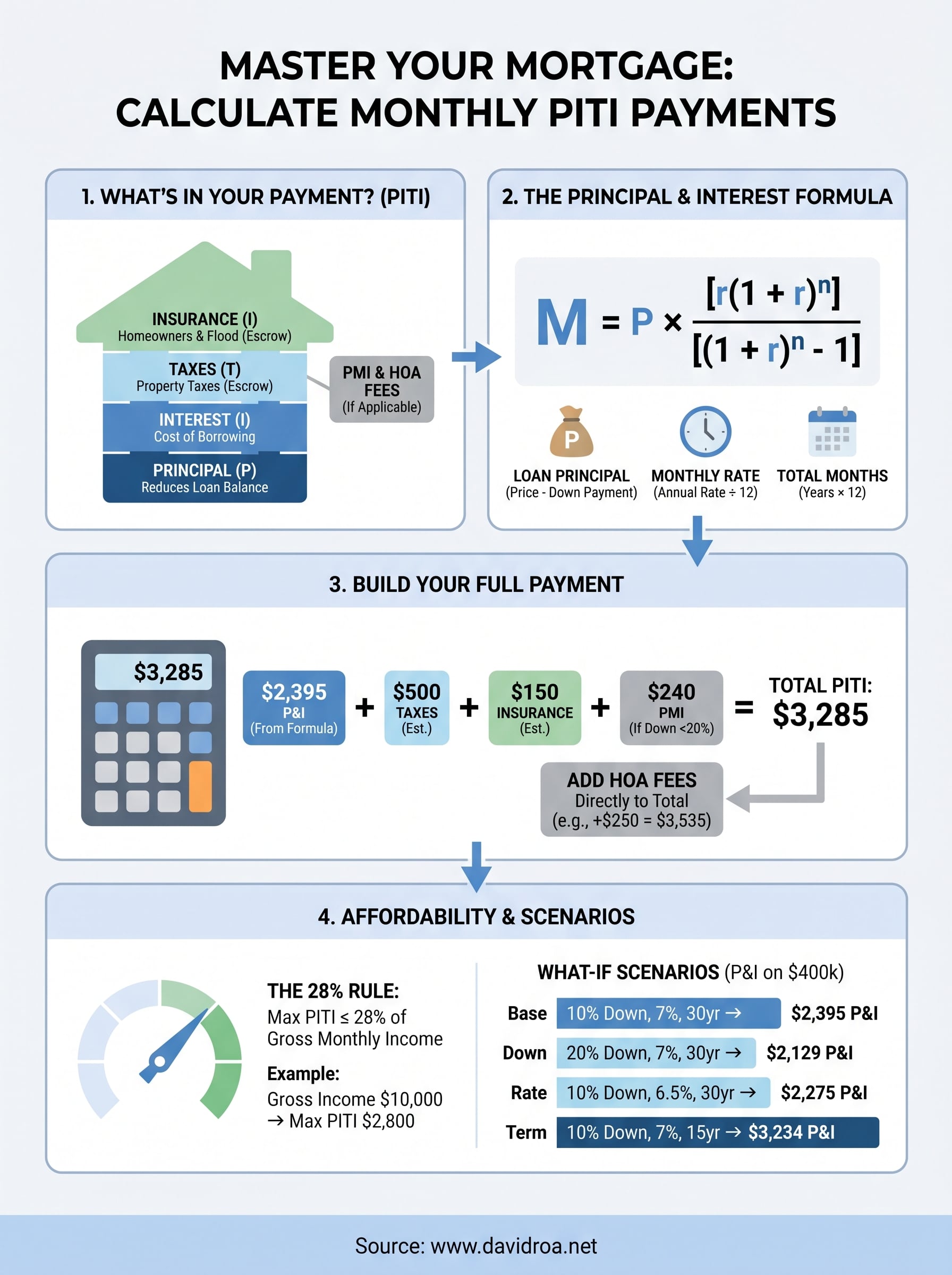

Taxes and insurance (escrow)

Property taxes and homeowners insurance are the two components most buyers underestimate. Your lender typically collects these as part of your monthly escrow payment, holds the funds, and pays the bills on your behalf when they come due. This protects their interest in the property and keeps you from falling behind on tax obligations.

Property taxes vary significantly by location. In high-tax states like Illinois, taxes can add $400 to $700 or more per month to a mid-range home purchase. Homeowners insurance depends on the home's value, location, and coverage level, but plan for $100 to $200 per month as a starting baseline. Your lender will require proof of coverage before closing.

Private mortgage insurance (PMI)

If your down payment is less than 20% on a conventional loan, your lender adds PMI to your monthly payment. PMI protects the lender, not you, in case of default. It typically runs 0.5% to 1.5% of the loan amount per year, split into monthly installments. On a $350,000 loan, that's roughly $146 to $438 added to your payment each month.

PMI is not permanent. Once your loan-to-value ratio drops to 80%, you can request cancellation. On FHA loans, mortgage insurance works differently and may stay for the life of the loan depending on your down payment and loan term, so know which loan type you're getting before you commit.

HOA fees and other recurring costs

If you're buying a condo, townhouse, or a home in a planned community, HOA fees are a mandatory monthly expense. These don't run through your mortgage payment, but they directly affect your total housing cost and your debt-to-income ratio when you apply for a loan. HOA fees can range from $100 to over $1,000 per month depending on the community and amenities included.

Some lenders also roll in flood insurance or other specialized coverage if your property sits in a designated risk zone. Always ask your loan officer for a complete line-item breakdown before you lock your rate, so every dollar in your monthly obligation is accounted for before you make a decision.

Step 1. Gather your numbers before you calculate

Before you run any math, you need the right inputs in front of you. Without accurate figures, your estimate is just a guess, and guesses don't tell you whether you can actually afford the home you're looking at.

The core loan inputs

Three numbers drive your principal and interest calculation: loan amount, interest rate, and loan term. Your loan amount is the purchase price minus your down payment. If you're buying a $400,000 home with 10% down ($40,000), your loan amount is $360,000. Your interest rate is the annual rate your lender quotes you, and your loan term is typically 180 months (15 years) or 360 months (30 years).

Use the exact rate your lender has quoted rather than a national average, since even a 0.25% difference can shift your payment by $50 or more per month.

The escrow and insurance inputs

To calculate monthly mortgage payment totals accurately, you also need your property tax rate and your homeowners insurance premium. Contact your insurance agent for an annual premium quote, then divide by 12 for your monthly figure. For property taxes, look up your county assessor's rate and apply it to the home's assessed value. If you're putting less than 20% down on a conventional loan, add your PMI estimate as well, typically 0.5% to 1.5% of your loan amount annually.

Here's a reference table to organize every input before you start:

| Input | Where to get it | Example |

|---|---|---|

| Purchase price | Listing or offer | $400,000 |

| Down payment | Your savings plan | $40,000 (10%) |

| Loan amount | Price minus down | $360,000 |

| Annual interest rate | Lender quote | 7.00% |

| Loan term | Your loan choice | 360 months |

| Annual property tax | County assessor | $6,000 ($500/mo) |

| Annual homeowners insurance | Insurance agent quote | $1,800 ($150/mo) |

| PMI rate (if applicable) | Lender estimate | 0.8% annually |

| HOA fees | HOA documents | $250/mo |

Having every number in one place before you start saves you from rerunning the formula with wrong inputs. Pull confirmed figures from real sources rather than ballpark numbers, because taxes and insurance alone can add $500 to $1,000 or more per month to your total obligation.

Step 2. Calculate principal and interest with the formula

Once you have your loan inputs organized, you can calculate monthly mortgage payment costs for principal and interest using a single formula. This calculation is the foundation of everything else. Get this number right, and adding taxes, insurance, and other costs becomes straightforward math.

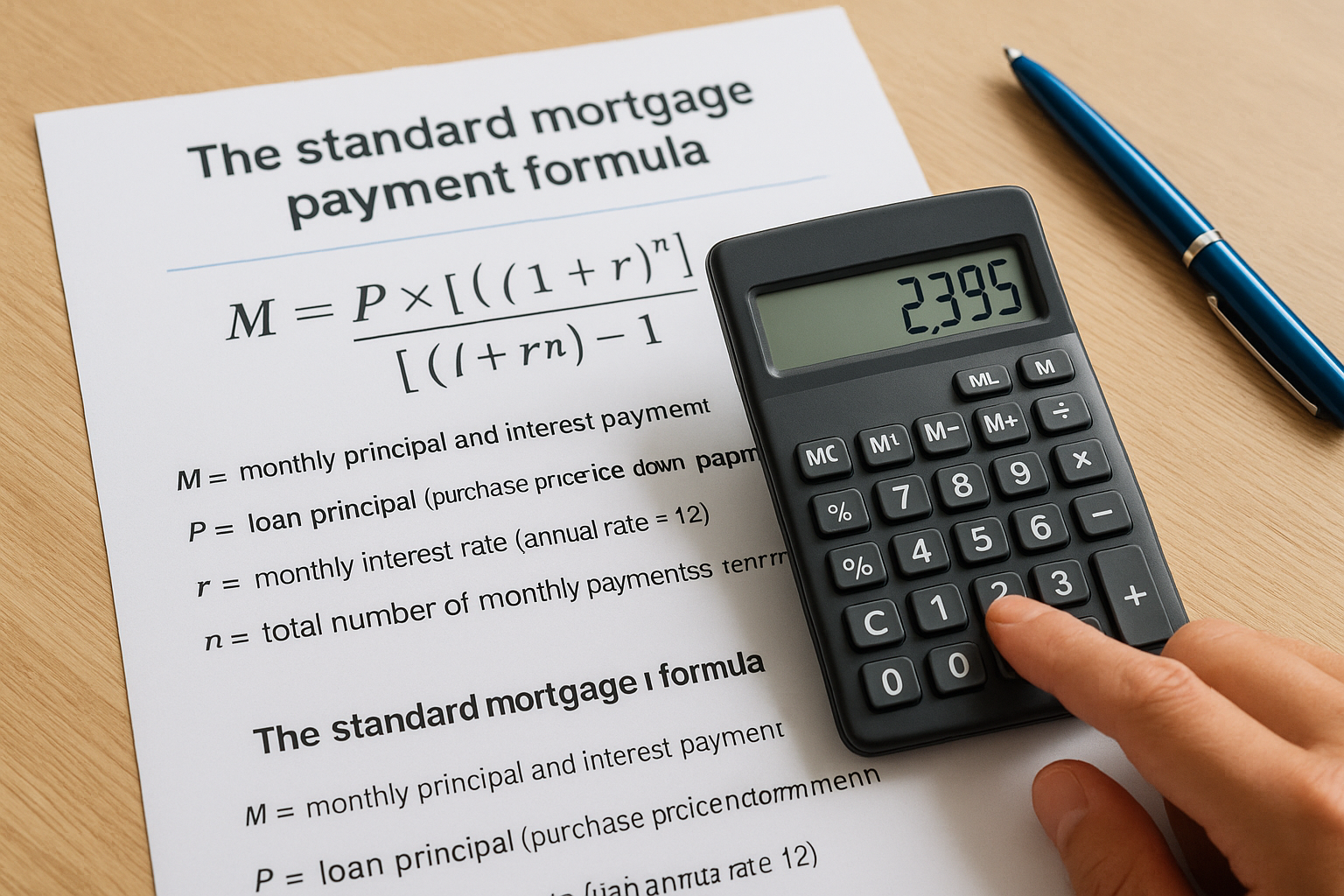

The standard mortgage payment formula

The formula lenders use is called the amortizing payment formula, and it accounts for both the declining principal balance and the interest charged on that balance each month. Every mortgage payment you make is calculated from this same equation, whether you're working with a 15-year or 30-year loan.

Knowing this formula lets you verify any number a lender or calculator gives you, which is a habit worth building before you commit to anything.

Here is the formula written out clearly:

M = P × [r(1 + r)^n] / [(1 + r)^n - 1]

M = monthly principal and interest payment

P = loan principal (purchase price minus down payment)

r = monthly interest rate (annual rate ÷ 12)

n = total number of monthly payments (loan term in years × 12)

Your annual interest rate must be converted to a monthly rate before you plug it in. A 7% annual rate becomes 0.07 ÷ 12, which equals 0.005833 per month. A 30-year term becomes 360 monthly payments.

Working through a real example

Using the numbers from Step 1, here is how the formula works with a $360,000 loan at 7% over 30 years:

- P = $360,000

- r = 0.07 ÷ 12 = 0.005833

- n = 30 × 12 = 360

Plugging those values in:

M = 360,000 × [0.005833 × (1.005833)^360] / [(1.005833)^360 - 1]

M = 360,000 × [0.005833 × 8.1165] / [8.1165 - 1]

M = 360,000 × 0.04734 / 7.1165

M = 360,000 × 0.006653

M ≈ $2,395 per month

That $2,395 figure covers only principal and interest. It does not include taxes, insurance, or PMI. The next step adds those remaining costs to give you the full monthly obligation you'll actually pay.

Step 3. Add PITI and other monthly housing costs

With your principal and interest figure confirmed, the next step is straightforward addition. You take that number and stack your escrow components on top of it to reach the actual dollar amount you'll send to your lender each month. This total is what lenders use to evaluate your debt-to-income ratio, and it's the number that needs to fit comfortably within your monthly budget.

Build the full PITI total

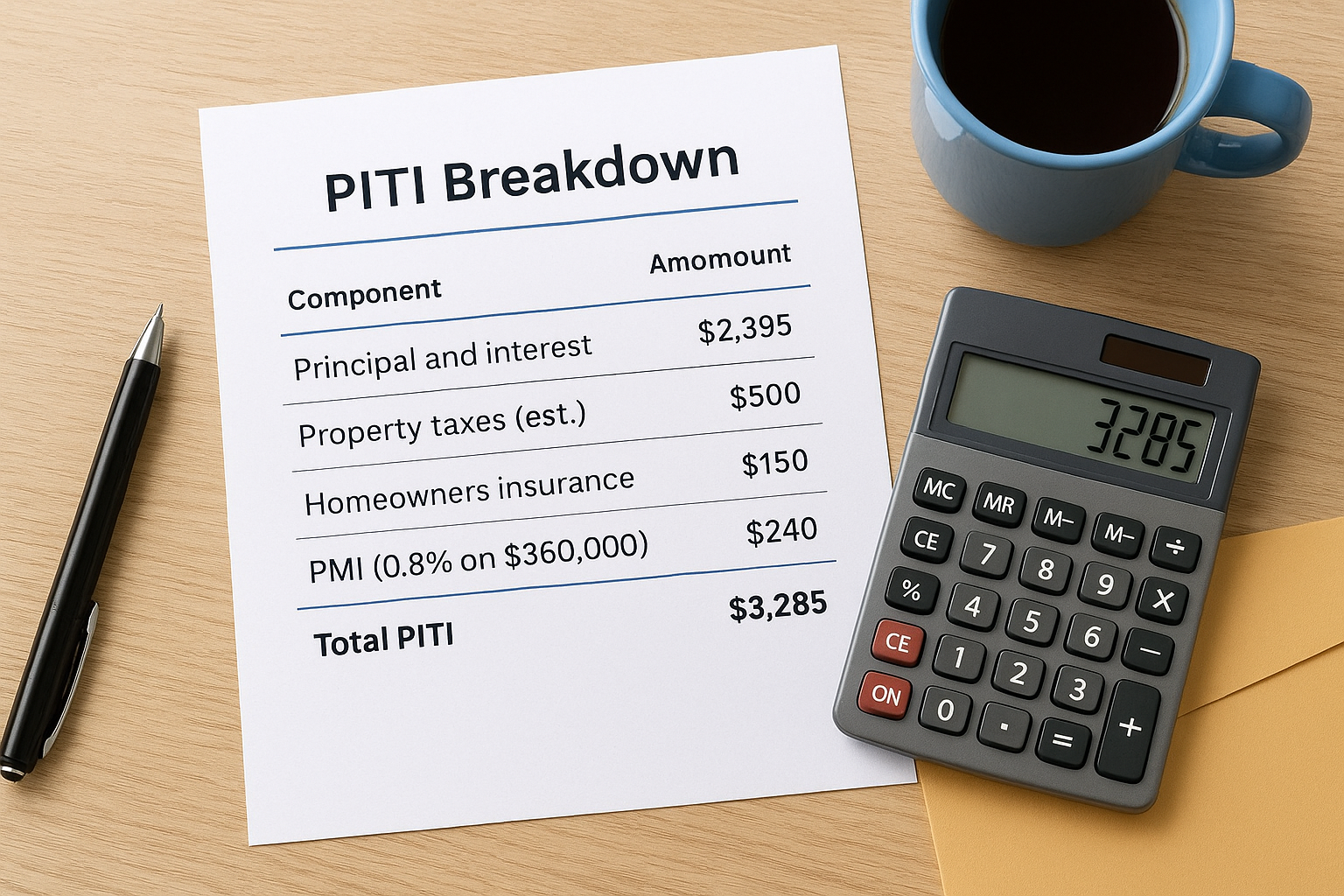

Take every figure you gathered in Step 1 and add it to your principal and interest payment. For the example loan from Step 2, a $360,000 loan at 7% over 30 years, this is what the full PITI breakdown looks like when you calculate monthly mortgage payment costs for the complete picture:

| Component | Monthly amount |

|---|---|

| Principal and interest | $2,395 |

| Property taxes (est.) | $500 |

| Homeowners insurance | $150 |

| PMI (0.8% on $360,000) | $240 |

| Total PITI | $3,285 |

Your monthly PMI figure comes from multiplying your loan amount by your PMI rate and dividing by 12. In this case: $360,000 × 0.008 ÷ 12 = $240 per month. That single line item adds nearly $3,000 per year to your housing cost, which is why many buyers prioritize reaching 20% down to eliminate it entirely.

Once you see the full PITI total, you'll often find it runs $700 to $1,000 higher than the principal and interest figure alone, and that gap is what catches buyers off guard.

Account for extras that don't go through escrow

HOA fees and any specialized insurance requirements like flood coverage don't run through your escrow account, but they still belong in your total monthly housing cost. Add your HOA fee directly on top of your PITI total to get your true monthly housing obligation. For this example, a $250 HOA fee brings the grand total to $3,535 per month.

Lenders will also count HOA fees in your debt-to-income calculation, so leaving them out of your planning creates a gap between what you think you can afford and what the underwriter actually sees. Pull the HOA documents before you make an offer so the monthly fee is confirmed, not guessed.

Step 4. Check affordability and run what-if scenarios

Now that you can calculate monthly mortgage payment totals accurately, the next step is comparing that number against your gross monthly income. Knowing your complete PITI figure is only useful if you also know whether it leaves you enough room for the rest of your financial life, including car payments, student loans, and everyday expenses.

Use the 28% rule as your starting benchmark

Most lenders evaluate affordability using the 28/36 rule. The front-end ratio says your total monthly housing costs should not exceed 28% of your gross monthly income. The back-end ratio adds all other recurring debt obligations and caps that combined total at 36% of gross income.

To apply this quickly, multiply your gross monthly income by 0.28. That result is the ceiling a traditional lender expects your PITI to stay under. If your household earns $10,000 per month before taxes, your maximum housing cost should sit at or below $2,800.

If your PITI total pushes past 28% of gross income, you have three levers: a larger down payment, a lower purchase price, or a longer loan term.

Run what-if scenarios before you lock in

Adjusting one variable at a time shows you exactly how much each factor moves your payment before you're under contract and working against a deadline. Swap a single input, record the new result, and compare the rows side by side to understand your real options. Use the formula from Step 2 each time you change an input.

Here's a comparison table showing how key variables affect the monthly principal and interest payment on a $400,000 purchase:

| Scenario | Down payment | Loan amount | Rate | Term | P&I payment |

|---|---|---|---|---|---|

| Base case | 10% ($40,000) | $360,000 | 7.00% | 30 yr | $2,395 |

| Higher down | 20% ($80,000) | $320,000 | 7.00% | 30 yr | $2,129 |

| Lower rate | 10% ($40,000) | $360,000 | 6.50% | 30 yr | $2,275 |

| Shorter term | 10% ($40,000) | $360,000 | 7.00% | 15 yr | $3,234 |

Each row changes one variable only while everything else stays constant. A 20% down payment saves $266 per month in principal and interest, and it also removes PMI entirely, pushing the real monthly savings past $500 once you factor in that line item.

A simple way to move forward

You now have the formula, the PITI breakdown, and the scenario comparison tools to calculate monthly mortgage payment costs with precision. Running the numbers yourself removes the guesswork and puts you in a stronger position before you ever sit down with a lender or make an offer on a property.

That said, real loan scenarios carry variables that no formula fully captures: credit-score-based rate adjustments, loan program differences, and local tax assessments that shift your total obligation in ways a generic calculator won't flag. Getting an accurate quote from an experienced loan officer is the step that turns your estimate into a real, closeable number.

With over 25 years of lending experience and more than $150 million funded across residential, investment, and commercial deals, David Roa works through exactly these scenarios with buyers and investors every day. Get a mortgage consultation with David Roa and build a payment structure that actually fits your goals.