Cook County Down Payment Assistance Program: How To Qualify

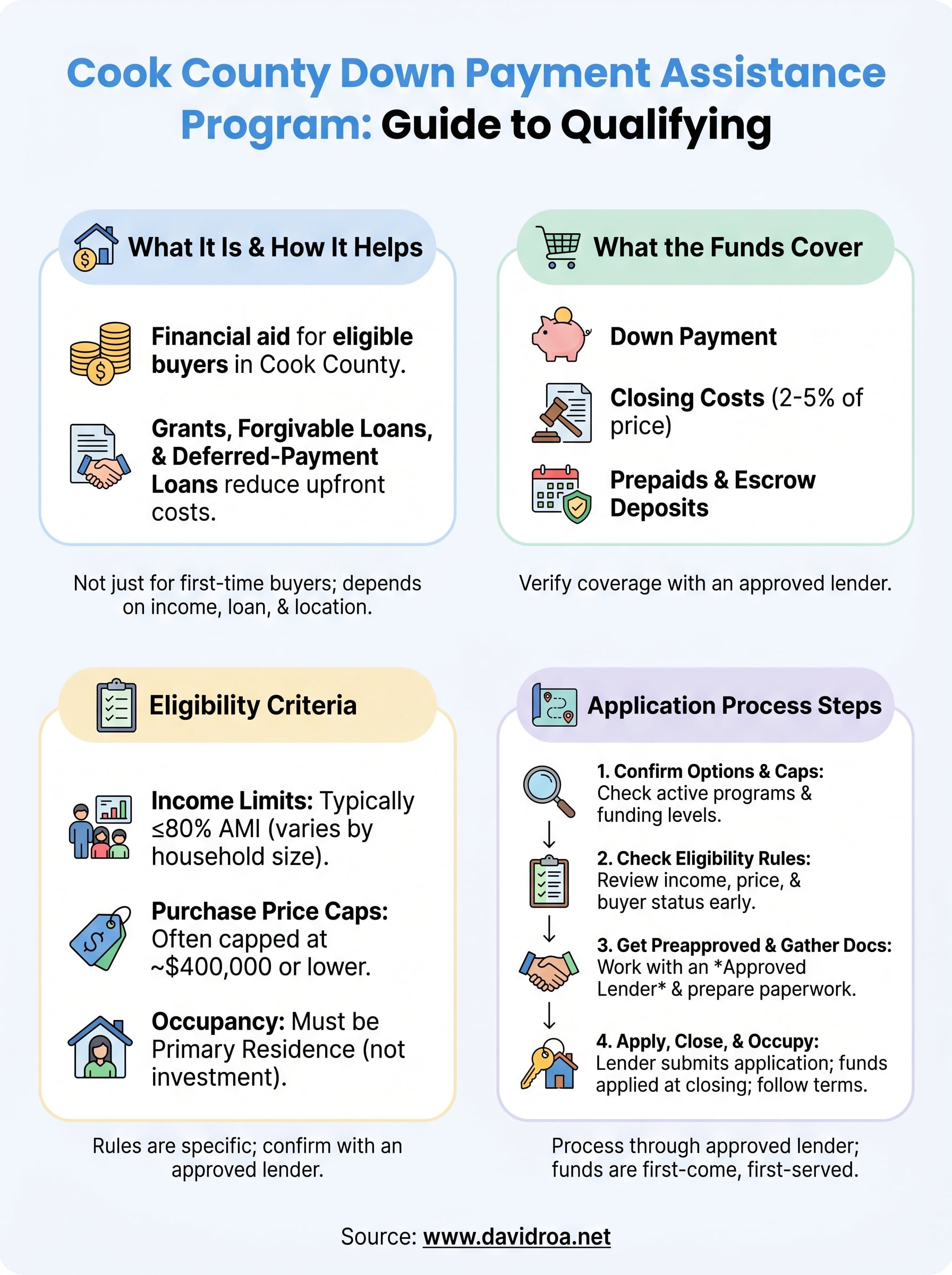

The down payment is often the biggest hurdle standing between you and homeownership, especially in a market like Chicago's. But if you're buying in Cook County, you may not have to cover that cost alone. The Cook County down payment assistance program offers eligible buyers thousands of dollars in financial help, and most people don't even know it exists or how to access it.

These programs aren't just for first-time buyers, either. Depending on your income, location, and loan type, you could qualify for grants or forgivable loans that reduce your upfront costs significantly. The catch? Eligibility rules are specific, and the application process requires working with an approved lender who knows the system inside and out.

That's where we come in. At David Roa, we've helped buyers across the Chicago metro area secure financing through programs exactly like this, backed by over 25 years of lending experience and more than $150 million in funded loans. In this guide, we'll break down how the program works, what you need to qualify, and exactly how to apply so you can move forward with confidence.

What the Cook County DPA program covers

The Cook County down payment assistance program is administered through the Cook County Department of Housing, which partners with approved lenders to deliver funds directly to eligible buyers at closing. The goal is to lower the cash you need upfront, whether that covers your down payment, your closing costs, or both. Many buyers are surprised by how much help is actually available, but you need to understand the structure before you can take full advantage of it.

The county updates program funding and caps regularly, so the specific dollar amounts available can shift from one application cycle to the next.

The two main forms of assistance

Cook County DPA funds come in two primary forms: forgivable loans and deferred-payment loans. A forgivable loan has its balance erased after you occupy the home for a required period, often between five and ten years, with no monthly payments required during that time. A deferred-payment loan also carries no monthly payments, but the balance becomes due when you sell, refinance, or no longer use the property as your primary residence.

Both structures are built to reduce your immediate out-of-pocket costs without adding to your monthly housing payment. Which type you receive depends on the specific program tier and the funding available when you apply.

What you can use the funds for

Most assistance under these programs applies directly to your down payment, your closing costs, or a combination of both. This distinction matters because closing costs in Illinois typically run between 2% and 5% of the purchase price, which is a separate expense on top of whatever down payment your loan type requires.

Certain programs also allow funds to cover prepaids and escrow deposits, which include items like homeowner's insurance premiums and property tax reserves collected at closing. Knowing exactly what the assistance can cover lets you calculate your true out-of-pocket number before you start making offers, so nothing catches you off guard when you sit down at the closing table.

Step 1. Confirm your program options and caps

Before you contact a lender or start touring homes, you need to know which programs are actually funded and what dollar amounts are currently available. Cook County operates multiple assistance tiers, and the one you qualify for depends on factors like your income level, the municipality you're buying in, and whether you combine the assistance with a specific loan type.

Programs to look into first

The Cook County Department of Housing runs the primary down payment assistance program, but several municipalities within the county also layer their own programs on top of it. For example, suburban cities like Cicero and Harvey operate separate grant funds that can sometimes be combined with county-level assistance, which increases your total benefit. Call your lender and ask specifically which programs are currently active and funded in your target ZIP code before you fall in love with a property.

Funds in these programs are distributed on a first-come, first-served basis, so confirming availability early protects your timeline.

What the caps typically look like

Assistance amounts under the cook county down payment assistance program have historically ranged from $5,000 to $10,000, though specific caps shift as funding cycles open and close. The table below shows a general framework to set your expectations:

| Assistance Type | Typical Cap | Forgiveness Period |

|---|---|---|

| Forgivable loan | Up to $10,000 | 5 to 10 years |

| Deferred-payment loan | Up to $7,500 | Due at sale or refi |

| Municipal layered grant | Up to $5,000 | Varies by city |

Verify current amounts directly with an approved program lender before building your budget around a specific number.

Step 2. Check the eligibility rules before you shop

Eligibility for the cook county down payment assistance program is determined by several concrete factors, and confirming them before you start shopping saves you from building a plan around a home or price point that disqualifies you. Reviewing these rules early keeps your timeline realistic and prevents surprises once you're under contract.

Income limits and purchase price caps

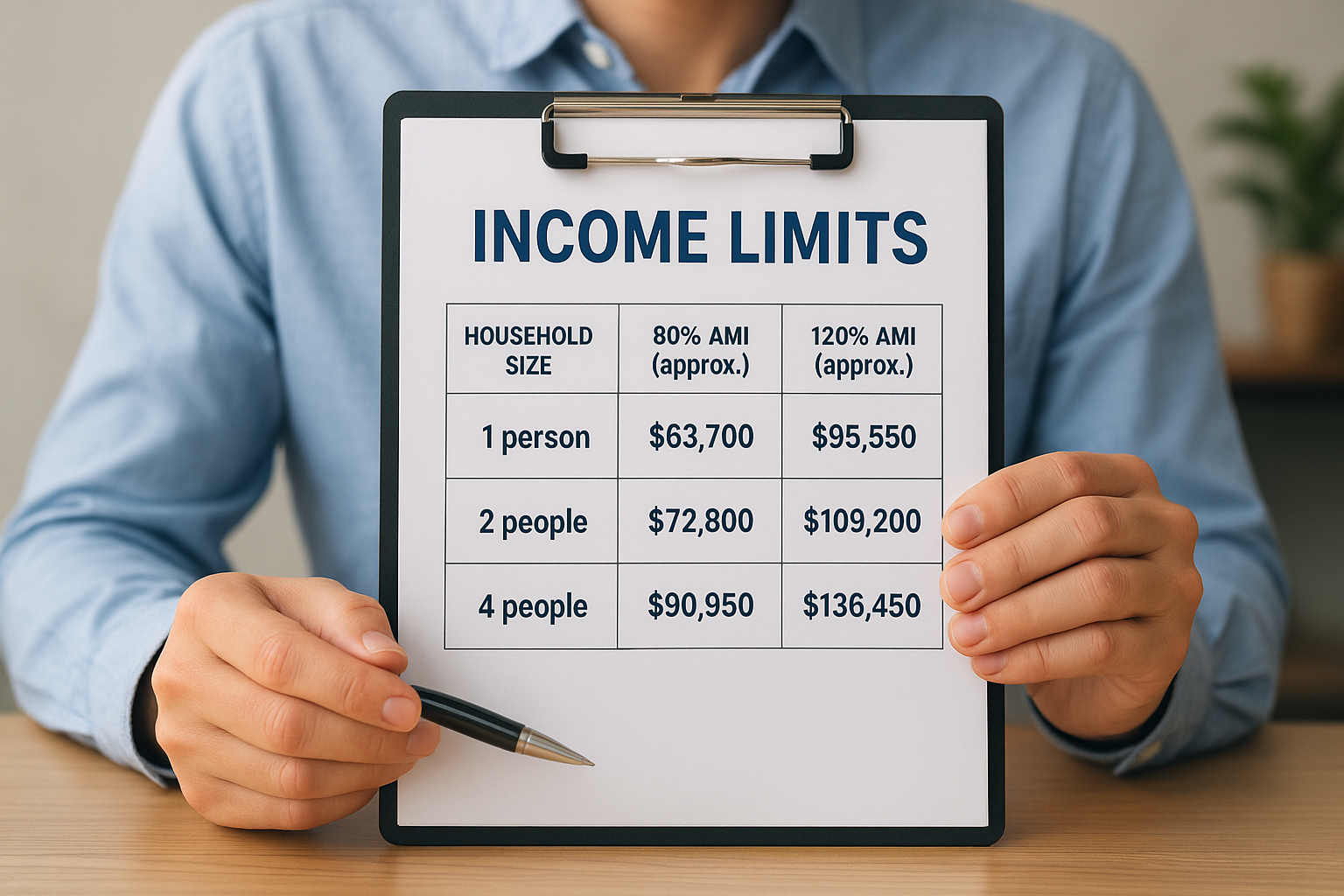

Your household income must fall at or below a percentage of the Area Median Income (AMI), which the U.S. Department of Housing and Urban Development updates annually. For most Cook County programs, the threshold sits at 80% of AMI, though some tiers allow up to 120% depending on the municipality. The table below gives you a reference point:

| Household Size | 80% AMI (approx.) | 120% AMI (approx.) |

|---|---|---|

| 1 person | $63,700 | $95,550 |

| 2 people | $72,800 | $109,200 |

| 4 people | $90,950 | $136,450 |

Always confirm current AMI limits with your lender because HUD updates these figures each year, and outdated numbers can throw off your entire eligibility calculation.

Purchase price limits also apply. Most programs cap the home's value at $400,000 or lower, depending on the specific tier.

Occupancy and buyer status requirements

You must intend to use the property as your primary residence, not as a rental or investment property. The program does not restrict assistance to first-time buyers exclusively, but prior homeownership within a defined lookback period can affect your eligibility, so confirm your specific situation with an approved lender before you assume you qualify.

Step 3. Get preapproved and gather required documents

Preapproval is not optional with the cook county down payment assistance program. You must work with a program-approved lender who is authorized to originate the specific assistance tied to your purchase, so choosing the right lender first protects your eligibility before you invest time in the application.

Find an approved lender first

Not every mortgage lender in Cook County has authorization to process down payment assistance funds. Your lender must be registered with the Cook County Department of Housing or the municipal program you're applying through. When you contact a lender, ask directly whether they are an approved originator for your target program and municipality. Getting a clear yes before you proceed prevents you from losing your spot in a funding queue.

Switching lenders mid-process can delay or disqualify your application if the new lender isn't approved, so confirm this detail on your first call.

Documents you'll need to submit

Gathering your paperwork in advance shortens the processing window significantly. Most programs require a consistent set of documents, and missing even one item can stall your file. Use the checklist below to prepare:

- Government-issued photo ID (driver's license or passport)

- Two years of federal tax returns with all schedules

- Two most recent W-2s or 1099s for all household earners

- 30 days of recent pay stubs

- Two months of bank statements for all accounts

- Proof of Social Security number or ITIN

- Signed purchase contract once you're under agreement

Having these documents ready before you submit your application moves your file to the front of the review process.

Step 4. Apply, close, and follow the program terms

Once your documents are in order and your lender confirms your eligibility, you're ready to submit your application for the cook county down payment assistance program. Your lender handles the submission on your behalf, which means your job is to respond quickly to any requests for additional information and keep your financial profile stable until closing.

Submit your application through your lender

Your lender forwards your file to the program administrator for review and approval. Processing times vary, but most applications receive a decision within two to four weeks after a complete package is submitted. During that window, avoid making large deposits, taking on new credit, or changing jobs, because any of those actions can trigger a new review of your file and delay your close date.

Inform your real estate agent about the assistance program upfront so they can build a realistic timeline into your purchase contract.

What happens at closing and after

At closing, the assistance funds are applied directly to your costs, which means you arrive at the table needing less cash than a standard transaction. Your closing disclosure will itemize exactly how the funds are credited so you can verify everything before you sign.

After closing, your primary obligation is occupancy. If you received a forgivable loan, you must live in the home as your primary residence for the full forgiveness period, which typically runs five to ten years. Selling, refinancing, or moving out before that term ends triggers repayment, so build that timeline into your plans before you commit.

Next steps

You now have a clear picture of how the cook county down payment assistance program works, what it covers, and exactly what you need to do to qualify. The process is straightforward when you follow each step in order: confirm your program options, verify your eligibility, get preapproved with an approved lender, and keep your finances stable through closing. Skipping any one of those steps creates delays that can cost you your spot in a funding queue.

Your next move is to talk to a lender who knows these programs well and can confirm which funds are currently active in your target area. Waiting costs you real money because assistance funds run out on a first-come, first-served basis, and the earlier you start, the more options you have. If you're ready to take that step, connect with a Cook County mortgage expert and get your questions answered before the next funding cycle closes.