Hard Money Loan Requirements: Docs, Down Payment, Credit

Hard money loans move fast, but they don't move without paperwork, equity, and a clear picture of the deal. If you're researching hard money loan requirements, you're probably weighing a time-sensitive investment and need straight answers about what lenders actually expect before they'll fund your project. The criteria look different from a conventional mortgage, and understanding those differences upfront saves you weeks of back-and-forth.

Most hard money lenders care far more about the property than your personal financial history. That said, you still need to show up prepared. Down payment expectations, documentation, credit thresholds, and exit strategies all play a role in whether your deal gets approved, and on what terms. Each lender draws the line differently, which makes knowing the baseline requirements essential before you submit anything.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment deals over 25+ years. Hard money lending is one of our core offerings, and as active real estate investors ourselves, we evaluate these deals from both sides of the table. This article breaks down exactly what you'll need to qualify, docs, down payment, credit, and property requirements, so you can walk into the process ready to close.

Why hard money loan requirements look different

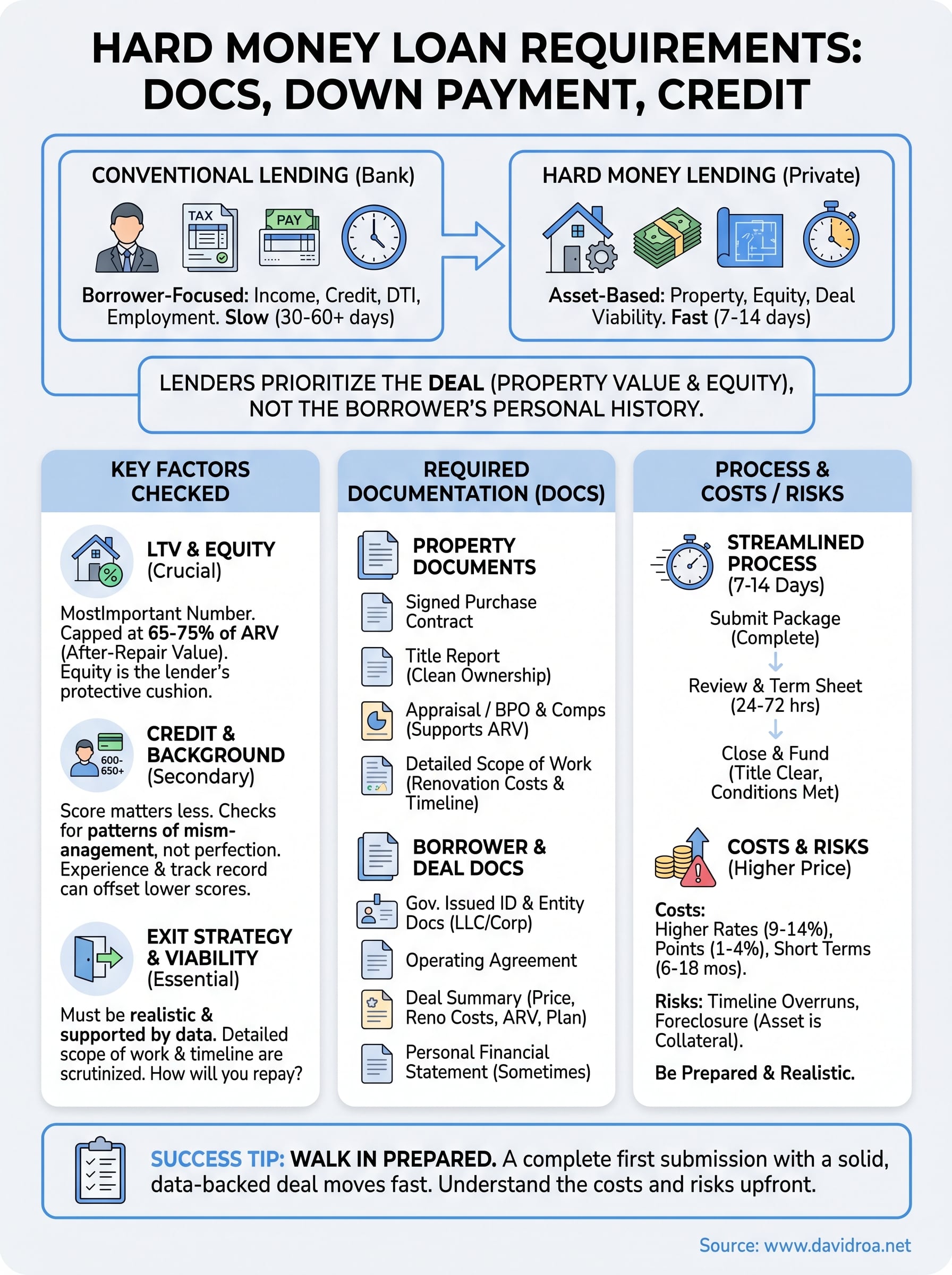

Hard money loans operate on a fundamentally different logic than conventional mortgages. Traditional bank loans are underwritten based on your income, credit score, debt-to-income ratio, and employment history. Hard money lenders flip that priority entirely: they underwrite the deal, not the borrower. That shift changes almost every requirement you'll encounter, from what documents matter to how much equity you need to bring to the table.

Asset-based lending changes what lenders prioritize

When a hard money lender reviews your application, the property is the primary collateral securing the loan. The value of the asset, specifically the after-repair value (ARV) for a fix-and-flip or the current market value for a bridge loan, determines how much you can borrow and at what loan-to-value (LTV) ratio. Most lenders will fund 65% to 75% of ARV, which means the equity buffer in the deal protects their downside if you default.

This structure allows lenders to approve borrowers who would get rejected by a bank. If you have a strong deal with a clear profit margin, past credit problems or self-employment income carry less weight than they would in a conventional underwrite. The property itself absorbs the risk, which is why the condition, location, and comparable sales of the asset matter more than your W-2.

The property is your strongest qualification in a hard money deal. A clean asset in a solid market can move a deal forward even when your personal financials are not perfect.

Speed is built into the model

Banks take 30 to 60 days to close because they run full income verification, appraisals through approved panels, and a layered review process involving underwriters, processors, and compliance teams. Hard money lenders operate on a compressed timeline, often closing in 7 to 14 days. That speed is intentional, and it shapes why hard money loan requirements are streamlined compared to conventional financing.

Your document stack won't look anything like what you'd hand to a bank. Lenders cut the process down to what actually moves the needle: proof you control the asset, a credible scope of work or exit plan, and enough skin in the game via your down payment to confirm you're serious about the deal.

Private capital means different rules apply

Hard money lenders are not banks. Most operate as private lenders or mortgage funds, which means they're not bound by the same federal lending regulations that govern conventional mortgage products. They don't need to follow Fannie Mae or Freddie Mac guidelines, and they don't sell loans on the secondary market. That independence gives them flexibility to write loans that no bank would touch.

That flexibility cuts both ways. Because there's no standardized rulebook, requirements vary significantly from one lender to the next. One lender might require a 680 credit score and 25% down; another might fund a deal with a 600 score and 30% down if the numbers are strong. Understanding this variability matters before you start applying, because the terms you accept on day one shape the return you walk away with when the deal closes.

Hard money loan requirements lenders check

When you sit down with a hard money lender, the conversation starts with the deal and moves outward from there. Lenders check a handful of core factors before they'll commit capital, and knowing where their attention lands helps you prepare the right information upfront. These hard money loan requirements aren't arbitrary; each one connects directly to the lender's ability to recover their money if the deal goes sideways.

Loan-to-value ratio and property equity

The loan-to-value ratio, or LTV, is the single most important number in a hard money deal. Most lenders cap LTV between 65% and 75% of the property's after-repair value or current market value, depending on the loan type. That gap between the loan amount and the property value is your equity cushion, and it's what protects the lender if you default and they have to foreclose and sell.

Bringing more equity to the table typically gets you better pricing on rate and fees. If you're buying a fix-and-flip at $200,000 with a projected ARV of $320,000, a lender funding 70% of ARV would lend you up to $224,000, which covers your purchase and a portion of rehab costs. Your equity position and the strength of the comparables in the area will drive that number.

The LTV cap exists to protect the lender's capital, but it also tells you whether your deal has enough margin to survive unexpected costs without blowing your profit.

Credit score and borrower background

Credit score matters less in hard money than it does in conventional lending, but it still matters. Most lenders set a minimum somewhere between 600 and 650, though some will go lower if the LTV is conservative and the deal is clean. What they're really checking is whether your credit history reveals patterns of financial mismanagement that suggest you can't execute on a project, not whether you hit a perfect score.

Your track record as an investor also factors in. Prior completed projects, real estate experience, and references from previous lenders can offset a weaker credit profile. First-time investors aren't automatically disqualified, but expect a lender to ask more questions and possibly require a lower LTV to offset their unfamiliarity with your execution capability.

Exit strategy and deal viability

Lenders want to know how you plan to repay the loan before the term ends. Your exit strategy, whether that's a sale, refinance, or rental conversion, needs to be realistic and supported by market data. A fix-and-flip exit backed by strong comparables in the neighborhood carries far more weight than a vague plan to "sell when the market is right."

The scope of work and your timeline also get scrutinized. If your rehab estimate is significantly below what comparable projects cost in that market, a lender will flag it. Underestimating costs is one of the most common reasons deals fail, and experienced lenders know exactly what renovation work should cost per square foot in a given area.

Documents you need to apply and close

Hard money lenders don't require your tax returns, pay stubs, or employment verification letters. The document stack for a hard money loan is shorter than a conventional mortgage, but it's focused on the specific information lenders need to evaluate the deal and commit capital. Knowing what to prepare before your first call shortens your timeline and signals to the lender that you're a serious operator.

Property documents

The property sits at the center of every hard money deal, and lenders need documentation that confirms its value, condition, and ownership chain. For most purchases, you'll need a signed purchase contract showing the agreed-upon price and terms. If you're refinancing or pulling cash out of a property you already own, you'll need the current deed and a title report showing the ownership history is clean with no unresolved liens or title defects.

A third-party appraisal or broker price opinion (BPO) may also be required, depending on the lender. Some lenders order their own appraisal internally, while others accept a BPO supported by comparable sales data to validate the ARV. For fix-and-flip projects, you'll also need a detailed scope of work that breaks down the repairs, materials, and estimated costs for each phase of the renovation, not a rough ballpark.

A detailed, realistic scope of work does more than satisfy a lender requirement. It protects your timeline and budget when costs shift mid-project.

Borrower and deal documents

Even though hard money loan requirements are lighter on personal financial documentation, lenders still need enough information to confirm who you are and how you plan to execute the deal. You'll need a government-issued ID, proof of entity if you're borrowing through an LLC or corporation, and the operating agreement or articles of incorporation for that entity. Most investors close in an LLC, so have these documents ready before you submit anything.

Your exit strategy needs to be in writing. A one-page deal summary covering your purchase price, estimated renovation costs, projected ARV, comparable sales, and repayment plan gives the lender a clear picture and speeds up their review. Some lenders also ask for a personal financial statement or a schedule of real estate owned, particularly for larger loan amounts. Pull these together before you apply and the process moves significantly faster.

How approval and funding work step by step

The process from first contact to funded deal typically takes 7 to 14 business days when you come prepared. Hard money lenders run a leaner review process than banks, but they still follow a clear sequence of steps before wiring funds. Knowing what happens at each stage helps you avoid delays and keeps the deal on your timeline.

Submit your deal package

Your first step is sending the lender a complete deal package. A strong submission includes the signed purchase contract, your scope of work, comparable sales supporting the ARV, and your entity documents if you're borrowing through an LLC. Lenders who receive incomplete submissions push those deals to the back of the queue. Sending everything at once signals that you run an organized operation and understand what hard money loan requirements actually look like in practice.

Some lenders offer a pre-approval or soft quote after an initial call. Take that step if it's available. Getting a soft term sheet before you're under contract lets you confirm the loan structure fits your deal before you're locked into a purchase timeline.

A complete first submission saves more time than any other single step in the process. Lenders move fastest on deals where nothing is missing.

Lender review and term sheet

Once your package is in, the lender assigns an underwriter or analyst to review the deal. They'll verify the purchase price against market comps, evaluate the scope of work, and confirm the LTV stays within their lending parameters. This review typically takes 24 to 72 hours for a straightforward deal. Complex properties or unusual markets may take longer.

After their review, the lender issues a term sheet. This document outlines the loan amount, interest rate, origination points, term length, and any conditions you need to meet before closing. Review it carefully and ask questions before signing. Once you accept the term sheet, the deal moves into title and closing preparation.

Closing and fund disbursement

Title work runs simultaneously with your lender's final review. The title company confirms ownership, checks for existing liens, and prepares the closing disclosure. Once the title is clear and all conditions on the term sheet are satisfied, the lender wires funds to close. For fix-and-flip deals, renovation draws are typically structured in scheduled disbursements tied to completed phases of work, so plan your contractor schedule around that funding structure from day one.

Costs, risks, and how to compare lenders

Hard money loans carry a higher price tag than conventional financing, and that cost is built into the model deliberately. Understanding the full cost structure before you sign prevents surprises that can erase the profit margin you underwrote into the deal.

What hard money loans actually cost

Interest rates on hard money loans typically range from 9% to 14% annually, depending on the lender, your deal structure, and how much equity you're bringing. On top of the rate, lenders charge origination points, usually 1 to 4 points (each point equals 1% of the loan amount). A $300,000 loan at 3 points means $9,000 in origination fees at closing, separate from any third-party costs like title, appraisal, and insurance.

Short loan terms amplify the effective cost. Most hard money loans run 6 to 18 months, which means the origination fee hits harder on an annualized basis than it would on a 30-year product. Factor in every line item, rate, points, title, appraisal, and carrying costs during renovation, before you confirm the deal pencils out.

Risks to account for before you close

The biggest risk in a hard money deal is a timeline overrun. Renovations that run long eat into your interest reserve and can push you past your loan maturity date, triggering extension fees or forcing a rushed sale at a price that kills your margin. Build a realistic contingency buffer into both your budget and your timeline from the start.

Hard money lenders can foreclose relatively quickly if you default, because the property is the collateral and the loan terms are direct. That's not a reason to avoid this product, but it's a reason to only move forward when your exit strategy is solid and your renovation estimates are grounded in real contractor bids, not assumptions.

Treat your exit strategy as a requirement, not an afterthought. Lenders check it closely, and your margin depends on executing it.

How to compare lenders side by side

Not every lender who meets your hard money loan requirements will offer competitive terms. When you compare lenders, focus on total cost, not just the rate. Request a full fee disclosure and compare origination points, extension fees, prepayment penalties, and draw schedules for rehab funds.

Ask each lender how many deals they've funded in your target market and how quickly they can commit to a term sheet. Lenders with a deep track record in your area understand local valuations and move faster when conditions are familiar.

Next steps

You now have a clear picture of what hard money loan requirements actually look like in practice: property equity drives the approval, your exit strategy has to be realistic, and the documents you bring to the table determine how fast your deal closes. Credit score matters, but the deal itself carries more weight than any single number in your financial history.

Before you submit anything to a lender, confirm your ARV is supported by solid comparables, get real contractor bids for your scope of work, and have your entity documents ready to go. The investors who close fastest are the ones who walk in prepared, not the ones scrambling to pull documents together after a lender asks for them.

If you're ready to move forward on a fix-and-flip, bridge loan, or investment property deal, connect with David Roa to review your deal and get terms that fit your timeline and project goals.