How Does Down Payment Assistance Work? Types, Rules, Steps

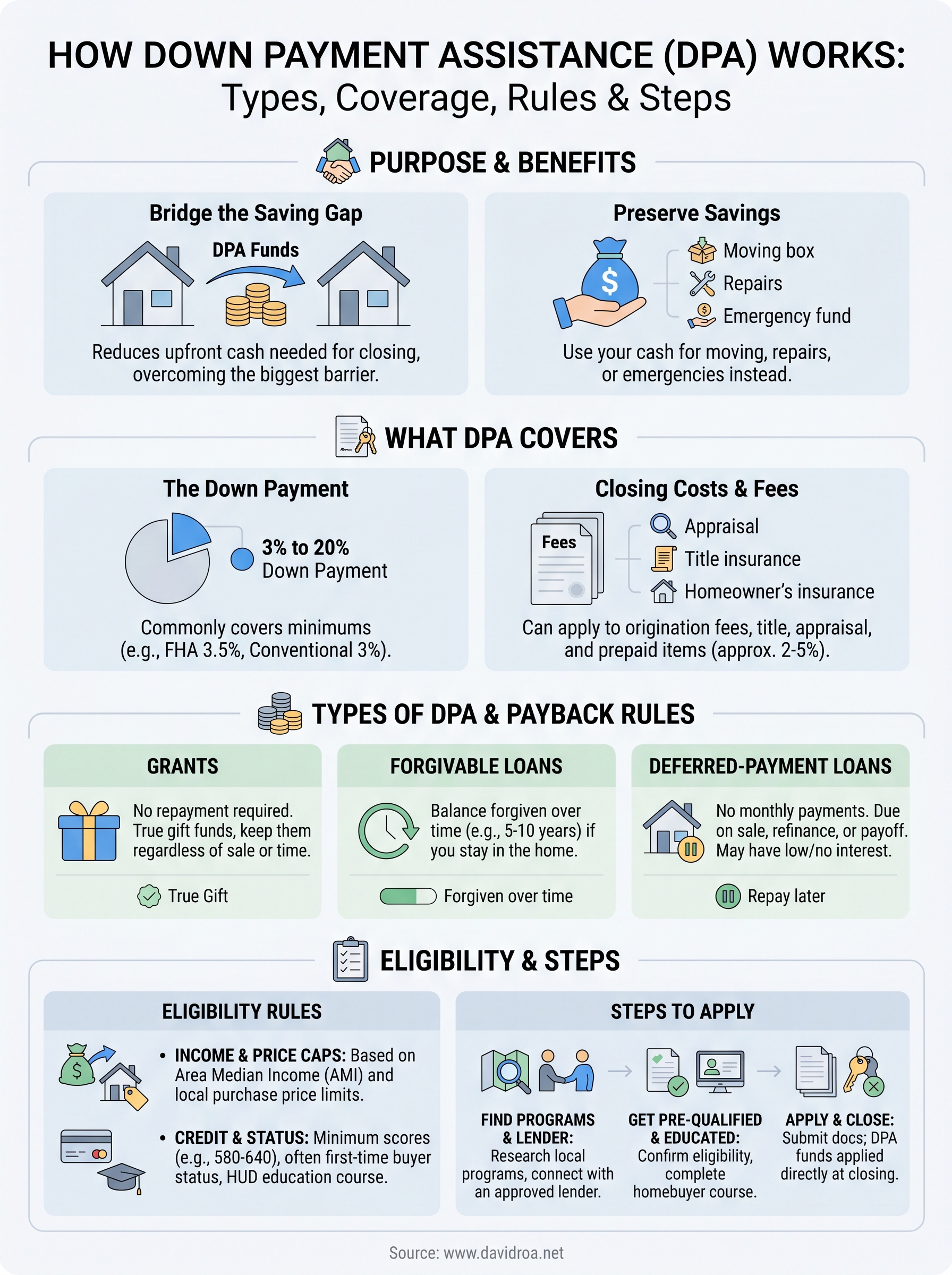

Saving enough cash to cover a down payment is one of the biggest barriers standing between renters and homeownership. But here's something many buyers don't realize: thousands of programs across the country exist specifically to reduce or eliminate that upfront cost. Understanding how does down payment assistance work gives you a real advantage, because money you don't have to bring to closing is money you can use for moving costs, repairs, or simply keeping your savings intact.

Down payment assistance (DPA) programs come in several forms, grants, forgivable loans, deferred-payment loans, and matched savings plans, each with its own eligibility rules, repayment terms, and application steps. The details matter, and getting them wrong can cost you time or disqualify you from programs you'd otherwise qualify for. That's where working with an experienced lender makes a significant difference. With over 25 years in the mortgage industry and more than $150 million funded, I've helped first-time buyers, ITIN holders, and families across the Chicago area and nationwide navigate these programs successfully.

This guide breaks down the types of down payment assistance available, who qualifies, how repayment works, and the exact steps to apply. Whether you're a first-time buyer exploring FHA options or a real estate agent advising clients, you'll walk away with a clear, practical understanding of how to put these programs to work.

Why down payment assistance matters

The down payment requirement stops more buyers than any other single obstacle in the homebuying process. For a $300,000 home with a conventional loan, a 3% to 20% down payment means you need between $9,000 and $60,000 in cash before closing costs even enter the conversation. Many qualified buyers, people with steady income, solid credit, and a genuine ability to repay a mortgage, sit on the sidelines for years simply because accumulating that lump sum takes time.

Down payment assistance directly addresses the gap between what buyers can afford monthly and what they can realistically save upfront.

The math behind the saving gap

Rent in most metro areas has climbed steadily, which means saving aggressively while renting is harder than it sounds. A household paying $1,800 a month in rent and living expenses may realistically set aside $500 to $700 monthly. At that rate, reaching a $20,000 down payment target takes nearly three years, and home prices don't pause while you save. Every month you wait, your target number can move higher, which is exactly the problem DPA programs are built to solve.

These programs don't just hand buyers a shortcut. They recognize that monthly payment capacity and upfront cash accumulation are two very different financial skills. You might qualify comfortably for a $1,400 monthly mortgage payment but still struggle to produce $15,000 in cash all at once. DPA bridges that specific divide without requiring you to deplete your savings entirely.

Who benefits most from these programs

First-time buyers represent the core audience, but many programs extend further than people expect. Moderate-income households, teachers, healthcare workers, and veterans frequently qualify under state and local initiatives designed to support stable communities and working professionals. ITIN holders and non-U.S. citizens can also qualify through certain FHA-aligned DPA programs, which is an area where having the right lender in your corner matters significantly.

Understanding how does down payment assistance work becomes especially valuable for buyers who assume these programs are rare or overly complicated. In reality, HUD tracks thousands of programs operating at the state, county, and city level, and most go underutilized simply because buyers don't know they exist.

What down payment assistance can pay for

Most buyers assume DPA only covers the down payment, but many programs cover more ground than that. Knowing exactly what the funds can apply to helps you plan your closing budget accurately and avoid last-minute surprises at the settlement table.

The down payment itself

The most direct use of these funds is reducing or eliminating the upfront cash you bring to the purchase. Depending on the program, DPA can cover the full down payment requirement or a set percentage of the purchase price. On an FHA loan, for example, the minimum down payment is 3.5%, and certain DPA programs will cover that entire amount, meaning you could close on a home with none of your own funds applied to the down payment.

Common loan types where DPA frequently covers the full down payment:

- FHA loans (3.5% minimum down)

- Conventional 97 loans (3% minimum down)

- VA loans (DPA can cover funding fees or closing costs)

Closing costs and related fees

Understanding how does down payment assistance work fully means recognizing that some programs extend coverage to closing costs as well. These costs typically include lender origination fees, title insurance, appraisal fees, and prepaid items like homeowner's insurance escrow. Closing costs generally run 2% to 5% of the loan amount, adding $6,000 to $15,000 on a $300,000 purchase.

Covering both the down payment and closing costs through a single DPA program can eliminate nearly all the cash required to close.

Some programs restrict funds strictly to the down payment, so confirm the allowed uses before counting on coverage across both categories.

Types of down payment assistance and payback rules

Understanding how does down payment assistance work starts with knowing that not all programs give you free money. Each type carries different payback obligations, and choosing one without understanding the repayment terms can create surprises when you sell or refinance later.

Grants

Grants are the most straightforward option: you receive funds with no repayment required. Many state housing finance agencies and local governments offer grants tied to first-time buyer programs or income limits. Because the funds are a true gift, you keep them regardless of how long you stay in the home or what happens to the property value.

Grants are less common than other DPA types, so confirm availability with your lender before building your budget around one.

Forgivable loans

A forgivable loan looks like a second mortgage on paper, but the balance gets forgiven over time if you meet the program's terms. Most programs forgive the loan in full after you live in the home for a set period, typically five to ten years. If you sell or refinance before that window closes, you repay the remaining unforgiven balance on a prorated basis.

Deferred-payment loans

Deferred-payment loans require no monthly payment while you live in the home as your primary residence. The balance comes due only when you sell, refinance, or pay off your primary mortgage. These loans let you preserve cash flow now while the lender recovers the funds at a natural transaction point later. Some programs charge zero interest on deferred loans; others apply a low fixed rate that accrues over time.

Eligibility rules and program limits to expect

Every DPA program sets its own qualification criteria, but most share a common framework. Understanding how does down payment assistance work from an eligibility standpoint helps you avoid wasted applications and positions you to qualify on your first attempt.

Income and purchase price caps

Most programs use area median income (AMI) as their benchmark. You'll typically need to earn below 80% to 120% of your area's AMI to qualify, though some programs target even lower income bands. Programs also set maximum purchase prices, which vary by county and housing market. A program designed for buyers in rural Illinois may cap the purchase price at $350,000, while a Chicago metro-focused program might allow higher limits to reflect local market values.

Check AMI limits for your specific county through the HUD income limits page before assuming you qualify or don't qualify.

Credit score and buyer status requirements

Minimum credit score thresholds usually sit between 620 and 640 for most DPA programs, though some FHA-aligned programs accept scores as low as 580. Your primary mortgage type also affects eligibility: most DPA programs pair specifically with FHA, conventional, VA, or USDA loans, and they won't apply to every product a lender offers. Many programs also require completion of a HUD-approved homebuyer education course, which typically runs four to eight hours and can be completed online. First-time buyer status is a common requirement, though some programs define "first-time buyer" as anyone who hasn't owned a home in the past three years.

How to get down payment assistance step by step

Knowing how does down payment assistance work in theory only helps if you can follow a clear path to actually access it. The process moves through a predictable sequence, and working through each step in order prevents wasted applications and keeps your closing timeline on track.

Find programs available in your area

Your first step is identifying which programs serve your specific county, city, or state. Your state's housing finance agency is the most reliable starting point, and HUD maintains a searchable database of local assistance programs. Bring your household income figures, target purchase price, and intended loan type to that research so you can filter out programs you won't qualify for before spending time on their applications.

Get pre-qualified and connect with an approved lender

Most DPA programs require you to work with a lender on their approved list, so your mortgage pre-qualification and program selection need to happen together rather than separately. Confirming DPA compatibility upfront prevents the common mistake of selecting a lender who isn't authorized to deliver your target program.

Choosing your lender before verifying program approval is one of the fastest ways to delay your closing date.

Once your lender confirms eligibility, complete the required HUD-approved homebuyer education course, gather your income documentation, and submit your application through the lender. From there, the DPA funds get confirmed during underwriting and applied directly at closing, with no separate disbursement process required on your end.

Final takeaway and next step

Understanding how does down payment assistance work gives you a concrete path to homeownership that doesn't depend on saving every dollar yourself. Grants, forgivable loans, and deferred-payment programs each solve the same core problem in different ways: they reduce the upfront cash required at closing so your monthly budget, not your savings account, determines what you can buy.

The most important move you can make right now is talking to a lender who knows these programs from the inside out, not just in theory. Eligibility windows, income limits, and program availability change regularly, and a single conversation can tell you exactly which options apply to your situation today. With 25-plus years of mortgage experience and a direct track record helping buyers close with assistance programs, I can walk you through your specific options quickly. Connect with David Roa to get a clear picture of what you qualify for.