Minimum Credit Score for Conventional Loan: 2026 Rules

The minimum credit score for conventional loan approval is one of the first questions borrowers ask, and for good reason. That number determines whether you qualify, what interest rate you'll get, and how much you'll pay over the life of your mortgage. For 2026, the baseline remains 620, but the full picture involves more nuance than a single number suggests.

As a senior loan officer and mortgage broker with over 25 years of experience and more than $150 million in funded loans, I've worked with borrowers across the credit spectrum, from first-time buyers barely clearing the threshold to investors with near-perfect scores shopping for the best terms. At David Roa, we see firsthand how credit score requirements interact with down payment size, debt-to-income ratios, and lender overlays to shape what's actually available to you.

This article breaks down the current conventional loan credit score rules, explains how your score affects your rate and private mortgage insurance costs, and covers the exceptions worth knowing about. If you're planning a home purchase or refinance this year, this is the baseline knowledge you need before you apply.

Why the minimum credit score matters for a conventional loan

Your credit score is the first filter lenders apply when you apply for a conventional loan. It signals how reliably you've managed debt in the past, which lenders use to predict how reliably you'll manage a mortgage going forward. A score of 620 is the floor for most conventional programs, but the difference between 620 and 760 isn't just about getting approved. It shapes the rate you're offered, the cost of required insurance, and the overall loan terms available to you. Getting close to the minimum and clearing it by a wide margin are two very different financial outcomes.

How your score directly affects your interest rate

Lenders price risk into every mortgage they issue. When your score is lower, lenders treat you as a higher-risk borrower and charge a higher interest rate to offset that risk. This isn't a small gap. On a $350,000 loan, a borrower with a 620 score could pay half a percentage point or more above what a borrower with a 760 score pays. Over a 30-year term, that difference adds up to tens of thousands of dollars in additional interest payments.

A 0.5% rate difference on a $350,000 loan can cost you more than $35,000 extra over 30 years, based on standard amortization math.

Fannie Mae and Freddie Mac use loan-level price adjustments (LLPAs) to create these risk-based pricing tiers. Your score places you in a specific pricing band, and every tier lower costs you more at closing or inside your monthly payment. The adjustments stack with your down payment percentage, so a lower score combined with a smaller down payment compounds the cost quickly.

How your score determines your private mortgage insurance cost

If you put down less than 20%, conventional loans require private mortgage insurance (PMI). Your credit score directly affects what you pay for that coverage every month. A borrower with a 620 score putting 5% down will pay a significantly higher PMI premium than a borrower with a 740 score at the same down payment level.

PMI rates typically range from 0.2% to 2% of the loan amount annually, and your credit score is one of the primary variables that determines where you land in that range. For anyone evaluating the minimum credit score for conventional loan qualification, understand that clearing the minimum gets you through the door. From there, every additional point on your score translates into measurable savings on both your rate and your monthly insurance cost.

What the 2026 minimum is and why you may hear mixed answers

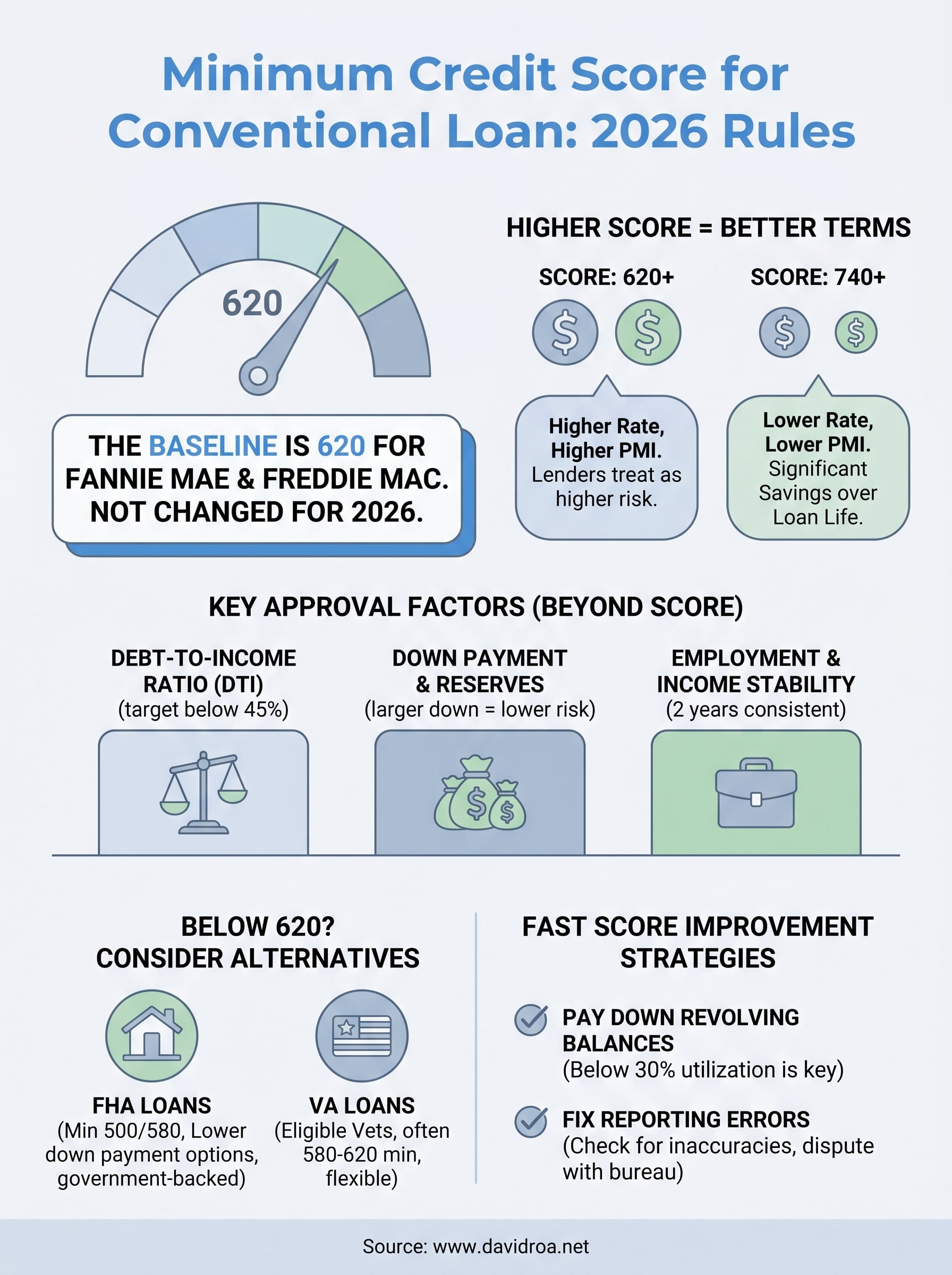

The official minimum credit score for conventional loan programs backed by Fannie Mae and Freddie Mac is 620. That number has not changed for 2026. It applies to fixed-rate and adjustable-rate conventional mortgages for both purchase and refinance transactions. If your score sits at or above 620 and you meet the other underwriting criteria, you are eligible to apply for a conventional loan under the standard guidelines.

Why lenders quote different numbers

The confusion starts because individual lenders are not required to accept every borrower who meets Fannie Mae or Freddie Mac's baseline. Many banks and mortgage companies add what the industry calls overlays, which are stricter internal requirements layered on top of the agency guidelines. One lender might tell you their minimum is 640 while another works with borrowers at 620. Both are technically correct for their own institution.

Fannie Mae sets the floor, but the lender you choose sets the ceiling on who they're willing to approve.

These overlays exist because lenders carry risk on loans before they sell them to the secondary market. A lender with a higher volume of defaults faces financial exposure, so many choose to reduce that risk by raising their internal credit floor. If one lender turns you away at 625, a different lender operating under the same Fannie Mae guidelines may approve your file without issue. Shopping your application to multiple lenders is not just about finding a better rate. It can determine whether you get approved at all when your score is close to the baseline threshold.

What lenders evaluate besides your score for approval

Meeting the minimum credit score for conventional loan programs is a necessary step, but it's only one piece of the underwriting picture. Lenders review several financial factors simultaneously, and a weakness in one area can offset a strength in another. Understanding the full picture helps you walk into the application process prepared.

Debt-to-income ratio

Your debt-to-income ratio (DTI) measures your total monthly debt payments against your gross monthly income. Conventional loan guidelines generally cap DTI at 45% for most borrowers, though automated underwriting systems may approve higher ratios when other factors are strong. If your DTI runs high, a lender may require a larger down payment or a higher credit score to compensate.

A lower DTI signals to lenders that you have room in your budget to absorb a mortgage payment without financial strain.

Down payment size and cash reserves

The down payment percentage you bring to closing directly influences your risk tier in the lender's eyes. Putting 20% down eliminates PMI entirely and places you in a lower risk bracket regardless of your score. Beyond the down payment, cash reserves also factor into the decision, referring to the liquid assets you have left after closing. Most conventional programs want to see at least two months of mortgage payments sitting in your accounts after your down payment clears.

Employment and income stability

Lenders want to see two years of consistent employment history in the same field or with the same employer. Self-employed borrowers typically need two full years of tax returns to document income. Gaps in employment or recent job changes can raise questions during underwriting, so documenting your income sources clearly before you apply saves time and prevents delays.

Options if your score is below 620 or you have thin credit

If your score falls below the minimum credit score for conventional loan eligibility, you still have paths forward. Several government-backed loan programs accept lower scores or evaluate creditworthiness differently, and understanding these alternatives keeps your homeownership goals on track while you work on strengthening your profile.

Government-backed loan programs

FHA loans, backed by the Federal Housing Administration, accept scores as low as 500 with a 10% down payment and 580 with just 3.5% down. VA loans, available to eligible veterans and active-duty service members, carry no official minimum score requirement set by the Department of Veterans Affairs, though most lenders apply their own floor between 580 and 620. USDA loans serve buyers in designated rural and suburban areas and typically work with scores in the 620 to 640 range, though some lenders process these through manual underwriting for lower-score applicants.

If conventional loan guidelines don't fit your situation today, an FHA loan can get you into a home now and give you time to build the equity and credit history needed to refinance later on better terms.

When your credit history is thin rather than damaged

Thin credit describes a credit file with few or no accounts, not one filled with negative marks. This situation is common among first-time buyers, recent immigrants, and younger borrowers who simply haven't had enough time to build a traditional credit record. Some lenders will consider alternative payment history in these cases, including documented on-time rent payments, utility bills, and insurance premiums verified through tools recognized by Fannie Mae's Desktop Underwriter system. Ask your loan officer directly about non-traditional credit documentation before you assume a thin file disqualifies you from homeownership.

How to improve your score and mortgage readiness fast

Reaching the minimum credit score for conventional loan approval doesn't require months of waiting if you focus on the right actions. Credit scores respond to specific behaviors, and the fastest gains come from targeting the factors with the highest weight in the scoring model rather than trying to fix everything at once.

Pay down revolving balances first

Your credit utilization ratio, which measures how much of your available revolving credit you're using, accounts for roughly 30% of your FICO score. Keeping your balances below 30% of your total credit limits produces noticeable score gains within one to two billing cycles after the lower balances report to the bureaus. If you can push utilization below 10%, the improvement is even more pronounced. Avoid closing old credit card accounts during this process, since that reduces your available credit and raises your utilization percentage even if your balances don't move.

Paying down a single maxed-out card can move your score by 20 to 40 points in one reporting cycle.

Fix reporting errors before you apply

Errors on your credit report are more common than most borrowers expect. You can pull your reports for free from AnnualCreditReport.com, the official federally authorized source. Look for accounts that aren't yours, incorrect late payment notations, and balances that haven't updated after a payoff. Dispute any errors directly with the bureau reporting the inaccuracy, and corrections typically process within 30 days.

Fixing errors before you submit a loan application prevents delays in underwriting and removes unnecessary risk flags from your file. Combine error corrections with the balance paydown strategy, and you build the strongest possible credit profile before your lender pulls your credit for a formal review.

Next steps

You now have the full picture on the minimum credit score for conventional loan programs in 2026. The baseline is 620, but your score shapes far more than approval alone. It determines your interest rate, your PMI cost, and which lenders will compete for your business. Knowing where you stand before you apply gives you the leverage to improve your position or choose the right loan program for your current profile.

Your next move is to pull your credit report, identify the fastest areas for improvement, and talk to a loan officer who will give you a straight assessment based on your actual file. If your score is strong, your focus should shift to rate shopping and locking in terms that match your financial goals. If you're still building toward the threshold, the strategies in this article will get you there faster than you expect. Connect with David Roa to review your options and move forward with a clear plan.